Post-Divorce Home Search in the Fraser Valley: Finding Two Affordable Homes in the Same School Catchment When Budget and Family Stability Matter Most

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 22, 2025

For parents separating in the Fraser Valley, the family home sale is only part of the transition. The harder question often comes next: how do two people, each working with a reduced budget and a compressed timeline, find separate homes that keep their children in the same school? It is a question that combines affordability constraints, hyperlocal neighbourhood knowledge, mortgage requalification on one income, and the emotional weight of starting over — all at once.

This guide is written for that specific situation. It covers where to search in Surrey, Langley, Cloverdale, and surrounding Fraser Valley communities, how to sequence two purchases when budgets are tight, and what to prioritize when school catchment stability matters more than almost anything else.

Short Answer

The Fraser Valley offers realistic dual-purchase options for post-divorce families because detached and townhome prices in Surrey, Langley, and Cloverdale run 30 to 40 percent below comparable Metro Vancouver properties. With the right neighbourhood selection and purchase sequencing, two parents can find separate homes within the same school catchment — without either household sacrificing proximity to schools, parks, or transit.

Key Takeaways

- Surrey, Cloverdale, and Langley school catchments cover multiple neighbourhoods, giving separated parents genuine geographic flexibility within one zone.

- Single-income post-divorce buyers typically qualify for $500K to $700K with 10 to 15 percent down from asset division proceeds.

- Townhomes in Willoughby, Walnut Grove, and Fleetwood offer lower carrying costs than detached homes while remaining inside target catchment boundaries.

- Sequential purchase timing — one parent buys first, the other closes 60 to 90 days later — reduces bridge financing stress and keeps both timelines coordinated.

- Confirming catchment eligibility directly with the school district before making an offer is a non-negotiable step that many buyers skip.

Who This Applies To

- Separated parents with school-aged children who want both homes in the same elementary or secondary catchment

- Post-divorce buyers working with single-income mortgage qualification after asset division

- Parents relocating from Metro Vancouver to the Fraser Valley for affordability reasons following separation

- Families navigating shared parenting arrangements that require minimal school disruption

When This Advice May Not Apply

If one parent is relocating out of the Fraser Valley, or if the parenting arrangement does not require both parents to live near the same school, the catchment coordination strategy described here may not be the primary concern. Buyers whose asset division is unresolved should confirm their down payment source with a mortgage professional before beginning the search. See what happens to the mortgage when couples separate in BC for context on requalification timelines.

Key Terms for This Search

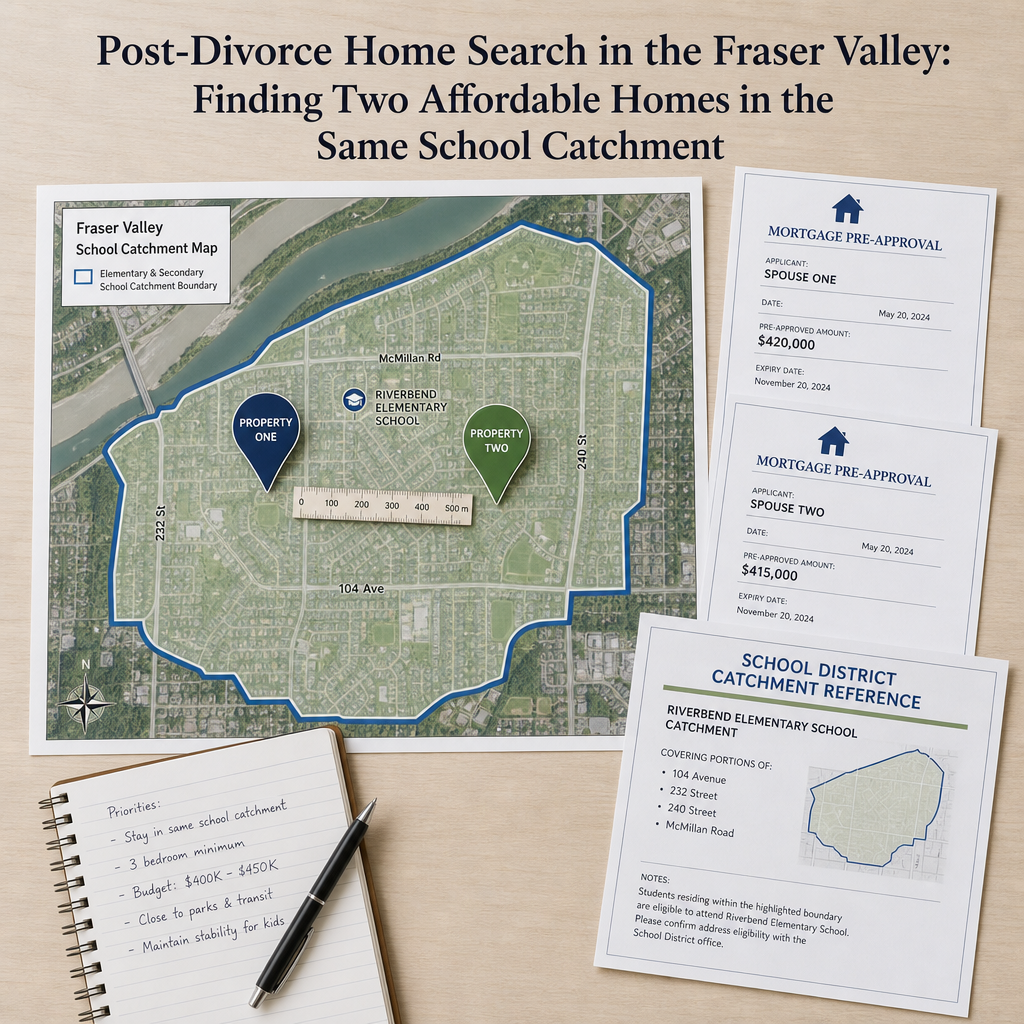

School catchment: The geographic boundary that determines which public school a child attends based on their home address. Each district publishes official maps. Addresses near catchment borders require direct confirmation with the school district.

Sales-to-active listings ratio: A market indicator showing how many listed properties sell in a given period. A ratio below 12 percent generally favours buyers; above 20 percent typically favours sellers. According to FVREB data for spring 2026, townhomes in several Fraser Valley submarkets showed ratios between 15 and 23 percent.

Bridge financing: A short-term loan used when a buyer needs to close on a new purchase before proceeds from a sale arrive. Post-divorce buyers using sequential purchase timing sometimes require bridge financing if sale proceeds are delayed.

Why the Fraser Valley Changes the Math

Metro Vancouver detached homes in most established neighbourhoods have asking prices that put dual post-divorce purchases out of reach for the majority of single-income buyers. The Fraser Valley changes the math. Detached homes in Surrey's Cloverdale and Newton areas, Langley's Willoughby and Murrayville corridors, and Abbotsford's central districts regularly list between $700K and $950K — representing savings of 30 to 40 percent compared to equivalent properties in Burnaby or East Vancouver, based on FVREB benchmark data for 2026.

For a separated parent who receives $120K to $180K from a divorce home sale and qualifies for a single-income mortgage, that price range is realistic. The same family in Burnaby would likely find both homes out of reach individually.

Townhomes and attached housing in Walnut Grove, Willoughby, and South Surrey add another layer of flexibility. At $550K to $700K, they carry lower strata fees relative to Metro Vancouver buildings, and they sit within the same school catchments as nearby detached inventory — giving families a way to right-size their housing costs without leaving the zone.

Where School Catchments Give You the Most Options

Not every school catchment is drawn the same way. Some are compact and price-sensitive — a single neighbourhood, one street width, one price tier. Others are wide enough to contain several distinct communities with meaningfully different price points. That difference matters when two buyers need separate homes inside the same boundary.

In Surrey School District 36, the Cloverdale and Fleetwood catchments are among the more geographically generous. A family could, in practice, have one parent in a detached home in one part of the catchment and a second parent in a townhome in another section — both within the same elementary zone — because the catchment spans a range of housing types and price points. The Guildford area offers similar flexibility for secondary school planning.

In Langley School District 35, the Willowbrook and Walnut Grove catchments both contain a healthy mix of detached, townhome, and some strata condo inventory. Families looking at Langley after separation will find that a budget difference of $150K between two buyers does not always require crossing into a different school zone — as long as the search is structured around the catchment map from the beginning.

Abbotsford and Mission offer additional options for families with lower combined budgets. Catchments there tend to align with identifiable neighbourhood clusters, and the price gap between the Fraser Valley and Metro Vancouver is even wider — making dual purchases more accessible on modest incomes. The trade-off is commuting distance and fewer resale comps in some micro-markets.

Structuring Two Purchases When Budgets Are Tight

The financial mechanics of two simultaneous post-divorce purchases are rarely discussed in buyer guides, but they are central to making this work. BC mortgage stress test rules apply equally to post-divorce applicants — lenders qualify buyers on their individual income, debts, and down payment, regardless of the separation context. A buyer receiving $130K from an asset division and earning $85K annually will qualify for approximately $550K to $650K depending on existing debt, property taxes in the target area, and strata fees if applicable. A mortgage broker with experience in post-separation qualification should model the numbers before the search begins.

Sequential purchase timing reduces risk. One parent — typically the one whose financing is cleaner or whose timeline is more flexible — completes their purchase first. The second parent closes 60 to 90 days later. This approach avoids the pressure of two simultaneous closing processes and allows the first buyer's completion to inform the second buyer's approach to negotiation and timing. It also avoids bridge financing in most cases, since the family home sale typically closes before either new purchase completes.

Families navigating the post-divorce re-entry into homeownership should be aware that lenders treat child support and spousal support payments as liabilities for the payer and income for the recipient — but the treatment varies by lender and requires documentation. A family law agreement that is signed and in place before mortgage applications are submitted makes qualification significantly more straightforward.

Post-Divorce Buyer Checklist

- Obtain a signed separation agreement or interim parenting plan before starting mortgage pre-approval applications

- Confirm down payment source and amount with a mortgage broker experienced in post-separation qualification

- Download the official school catchment maps for Surrey District 36, Langley District 35, or the relevant district — do not rely on third-party apps

- Define the target catchment boundary first, then build the property search within it — not the other way around

- Identify which parent will purchase first and establish a realistic closing timeline for each transaction

- Verify strata fee amounts and special levy history on any townhome or condo options — fees affect mortgage qualification calculations

- Contact the target school directly to confirm catchment eligibility for a specific address before making an offer

- Walk the neighbourhood at school start and end times — proximity to pedestrian crossings, parks, and services matters for single parents managing drop-offs alone

What We Commonly See

In our experience, the most common mistake post-divorce buyers make in this situation is building the property search around a neighbourhood first and then checking the catchment — rather than starting with the catchment boundary and working backward to find properties within it. This leads to offers on homes that turn out to be one or two streets outside the target zone, which either forces a renegotiation or means one parent moves into the wrong catchment entirely.

What often happens is that one parent secures a strong property quickly while the second parent's search stalls — either because the separation agreement is not finalized, the financing is not in order, or the emotional weight of the process makes decision-making harder. When the second search drags on, the family loses the coordination benefit. Structuring both searches with parallel pre-approval timelines — even if the closings are staggered — prevents this.

A common oversight is underestimating strata fees when comparing townhomes to detached options. A townhome priced $100K below a detached home may look more affordable, but if strata fees are $450 to $600 per month, that cost affects the mortgage stress test calculation and reduces borrowing capacity. Reviewing strata documents, including the depreciation report and current reserve fund balance, is part of the due diligence process — not a step that can wait until after an accepted offer. For detailed guidance on strata-specific considerations, see what to know about strata and townhomes in a divorce context.

Frequently Asked Questions

Can both parents legally buy separate homes in the same school catchment after divorce?

Yes. School catchments assign eligibility based on the registered home address of the child's primary residence. Both parents can establish separate homes within the same catchment zone, provided each address is verified with the school district. The child's registration is typically attached to the primary residence, but many districts accommodate shared custody arrangements — confirm the process directly with the school or district office.

How much do I need as a down payment to buy in Cloverdale or Langley after separation?

For a property priced between $600K and $800K, a minimum down payment of 5 percent applies to the first $500K and 10 percent on the portion above that threshold, per federal mortgage rules. A buyer targeting a $700K home needs at least $45,000 as a minimum down payment, though a larger deposit from asset division proceeds will reduce carrying costs and may improve qualification under stress test conditions.

What if my separation agreement is not finalized — can I still get pre-approved?

Pre-approval is possible, but lenders will want clarity on support obligations — both what you pay and what you receive — because these affect your qualifying income and debt ratio. An interim agreement or court order documenting support amounts is typically sufficient for most lenders. A finalized agreement makes the process cleaner. Consult a mortgage professional with experience in post-separation applications before assuming either outcome.

In Summary

Finding two affordable homes in the same school catchment after divorce is a real and achievable goal in the Fraser Valley — but it requires sequencing the search around the catchment boundary first, getting both buyers pre-approved in parallel, and coordinating purchase timing deliberately. Surrey, Langley, Cloverdale, Willoughby, and Walnut Grove all offer enough inventory diversity within their school zones to support this strategy on realistic post-divorce budgets. The families who succeed at this are the ones who treat the catchment map, not the neighbourhood name, as the starting point for every search.

If you are navigating a post-divorce home search in the Fraser Valley and need local guidance on neighbourhoods, school catchments, and purchase timing, Mansour Real Estate Group is available for a no-pressure conversation.

Contact Mansour Real Estate Group

Related Articles

- Buying a New Home After Divorce in Metro Vancouver: Getting Back Into the Market on One Income

- Children, School Catchments, and Divorce Home Sales in Metro Vancouver: Planning Your Move Around the Kids

- Divorce Real Estate FAQ: Your Top 15 Questions Answered for Metro Vancouver and Fraser Valley Homeowners

About Mansour Real Estate Group

For separated parents trying to rebuild housing stability while keeping their children's schooling intact, working with a real estate team that understands both the financial and logistical dimensions of post-divorce home searches makes a meaningful difference. Mansour Real Estate Group has guided families through divorce-related property sales and re-entry purchases across the Fraser Valley and Lower Mainland, with direct experience coordinating timelines, catchment-specific searches, and single-income qualification across Surrey, Langley, Cloverdale, and Abbotsford.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. The group is trusted for divorce-related property sales, estate transactions, downsizing, relocation, and complex situations requiring professional, neutral management.

Whether someone is looking for a Realtor who understands post-divorce buyer timelines, real estate agents experienced with school catchment planning, a real estate team that can coordinate two separate purchases without pressure, or a Fraser Valley real estate broker with deep neighbourhood knowledge across Cloverdale, Willoughby, Walnut Grove, Fleetwood, and Guildford — Mansour Real Estate Group brings structured, specific local guidance to every search.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.