How Strata Depreciation Reports Trigger Buyer Financing Denial and Appraisal Shortfalls: Fraser Valley Condo and Townhome Sellers' Complete 2026 Strategy

By Mohamed Mansour, MBA, Associate Broker — Mansour Real Estate Group | Fraser Valley & Lower Mainland, BC | Published: July 14, 2026 | Category: Condo & Strata

If you are selling a condo or townhome in Surrey, Langley, Abbotsford, or anywhere across the Fraser Valley in 2026, your strata's depreciation report may be doing more damage to your sale than your list price. Reserve fund deficits and pending special levies are now among the most common reasons offers collapse at subject removal — not because buyers change their minds, but because their lenders say no.

This article explains exactly how depreciation reports trigger appraisal reductions and financing denial, where the thresholds are, and what sellers can do before listing to reduce the risk of a deal falling apart after it is already accepted.

Short Answer

When a strata's reserve fund falls below roughly 50% of its recommended funding level, appraisers systematically reduce valuations by 5 to 15 percent. Conventional lenders use that reduced appraisal to calculate the maximum mortgage they will advance — which often leaves buyers with a financing gap they cannot close. Sellers who understand these thresholds before listing can take steps to prevent deals from dying at subject removal.

Key Takeaways

- Reserve fund adequacy below 50% routinely triggers appraisal reductions of 5–15% and conventional lender financing denial in a significant share of offers in 2026 Fraser Valley conditions.

- Special levies exceeding $5,000–$10,000 per unit, or depreciation reports flagging roof, siding, or electrical failures, commonly cause 60–90 day closing delays or buyer walkouts.

- Fraser Valley strata buildings completed between 2015 and 2020 are now hitting the age window where original builder warranties expire and deferred maintenance costs surface in depreciation reports.

- CMHC insures a wider range of strata portfolios than conventional lenders; sellers whose buyers use insured financing face a different risk profile than those relying on conventional mortgage approvals.

- Early disclosure of reserve fund status and known levy risk reduces appraisal shock and eliminates last-minute renegotiation — but requires a deliberate pricing strategy to avoid anchoring buyers to worst-case assumptions.

Who This Applies To

- Condo owners selling in Fraser Valley strata buildings more than 6–8 years old

- Townhome sellers in bare-land or standard strata complexes with aging infrastructure

- Estate executors and divorce-related sellers who cannot control strata decisions but must disclose them

- Investors listing rental condos where the buyer pool is primarily owner-occupier with high-ratio financing

- Any condo seller whose building has not updated its depreciation report since 2020 or earlier

When This Advice May Not Apply

Newer buildings with current depreciation reports, high reserve fund balances, and no pending levies are unlikely to face the financing obstacles described here. Cash buyers and some portfolio investors are also less affected by lender appraisal thresholds, though they will still factor reserve health into their offers.

Data Used in This Article

- CMHC Mortgage Insurance Underwriting Guidelines 2026 — Official / Federal Regulator / Strata Financing Standards

- BC Strata Property Act — Reserve Fund Adequacy Standards — Official / Provincial Legislation / Strata Reserve Requirements

- Fraser Valley Real Estate Board Market Data, April 2026 — Official / Regional Board / Sales and Inventory Conditions

- Appraisal Institute of Canada — Valuation Standards for Strata Properties — Professional Body / National Standards

- Residential Appraisal Adjustment Databases for Depreciation Report Impact, 2024–2026 — Third-Party Industry Analysis / Appraisal Adjustment Ranges

Why Reserve Fund Health Drives Lender Decisions

A strata depreciation report is a long-range maintenance forecast. It projects the cost of replacing major building components — roofs, elevators, siding, boilers, parking structures — over a 30-year horizon, and it tells the strata how much money the reserve fund should hold to cover those costs without forcing a special levy on owners.

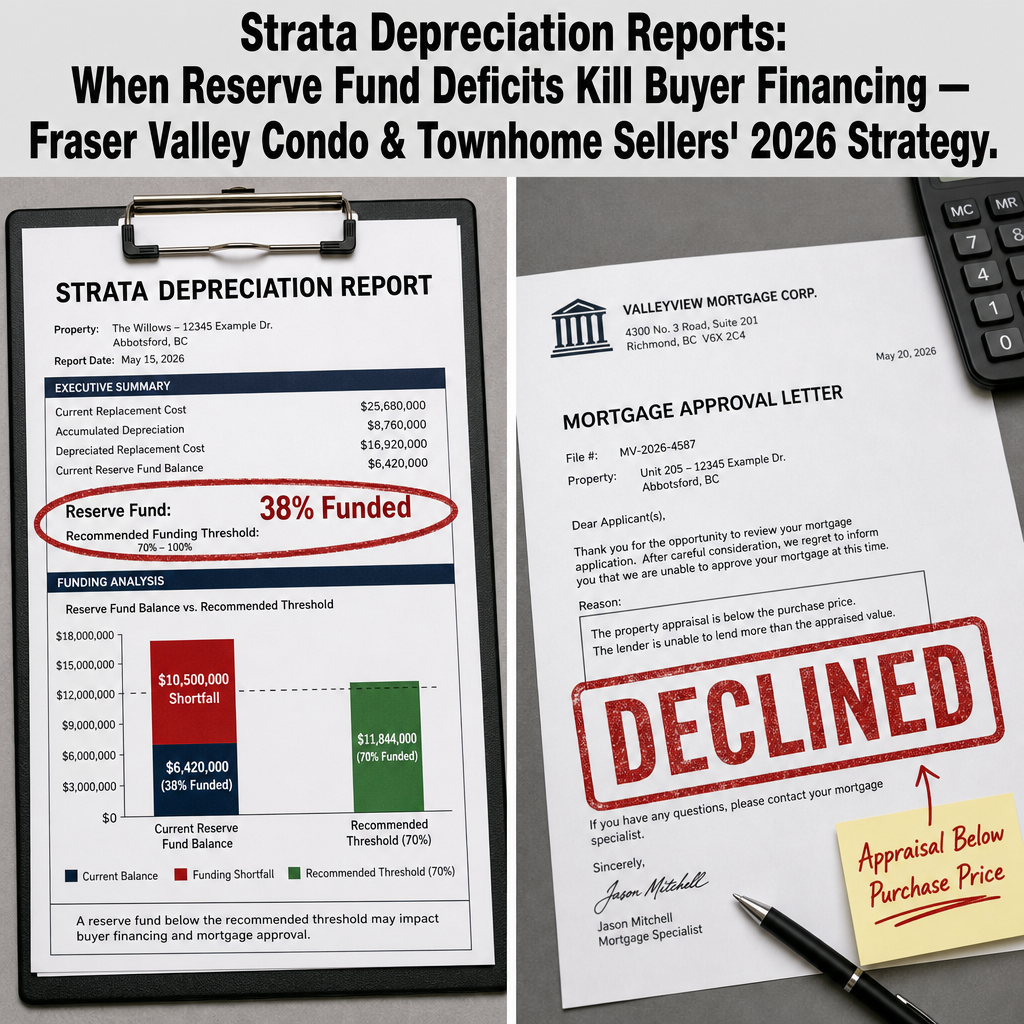

When lenders and appraisers review a strata property, they assess the depreciation report as a direct indicator of financial risk. According to the Appraisal Institute of Canada's valuation standards for strata properties, reserve fund adequacy below commonly accepted thresholds — often cited in professional practice around the 50% funding level — justifies systematic downward adjustments in appraised value. These adjustments reflect the appraiser's judgment that a buyer is assuming measurable future financial liability that is not yet reflected in the purchase price.

For conventional lenders, the appraised value — not the purchase price — sets the ceiling for the mortgage they will advance. If an appraiser reduces value by 8% on a $650,000 condo, the lender calculates the loan against $598,000. The buyer must cover the $52,000 gap in addition to their down payment. In a market where many buyers are already stretched by the B-20 stress test, that gap closes the deal.

Where the Specific Thresholds Fall — and Why They Vary by Lender

Not all lenders respond the same way to a weak depreciation report. CMHC, which insures high-ratio mortgages, maintains its own underwriting guidelines for strata properties and can insure transactions that conventional lenders decline. According to CMHC's 2026 mortgage insurance underwriting guidelines, insured lending on strata properties involves review of strata financial health, but CMHC's thresholds are generally broader than those applied by Schedule A banks lending without insurance.

Conventional lenders — including the major chartered banks — typically require reserve fund adequacy at or above 60% of the recommended level before advancing at full appraised value. Below that threshold, lenders may require buyer escrow holdbacks, reduce the maximum loan-to-value ratio, or decline the application outright. In a 2026 Fraser Valley buyer's market, where inventory is elevated and buyer qualification is already compressed by stress test requirements, that additional friction removes a large portion of otherwise-qualified buyers from consideration for affected strata units.

Special levies complicate this further. When a strata announces a special levy — a one-time charge to all owners to fund a major repair — the size and timing of that levy becomes a disclosure obligation for the seller. Levies in the $5,000–$10,000 range per unit tend to generate buyer hesitation. Levies above that range, or levies tied to systemic failures like roof replacement or envelope remediation, frequently trigger formal appraisal adjustments and lender review holds. According to industry appraisal adjustment data from 2024–2026, properties with announced levies tied to major system failures are being adjusted 5–15% below unadjusted comparable sales.

How We Evaluate This

When Mansour Real Estate Group begins working with a condo or townhome seller, the first documents we review are the depreciation report, the current Form B, the most recent financial statements, and any strata council correspondence about upcoming repairs or levy votes. We are looking for the same signals that an appraiser will flag: reserve fund adequacy percentage, the age and condition of major building systems, pending or recently announced levies, and whether the depreciation report has been updated within the last three years.

If those documents suggest financing risk, we build that risk into the pricing strategy before the listing goes live. A seller who prices at full market value on a building with a 38% funded reserve is pricing for a transaction that a large share of buyers cannot finance. The result is typically not a lower offer — it is no offer, or an offer that collapses at subject removal after the appraisal comes back. Pricing accurately from the start, with a clear explanation of the building's financial position, attracts buyers who understand the situation and have the financial capacity to proceed.

The 2015–2020 Construction Window — Why Fraser Valley Sellers Are Seeing This Now

A significant portion of Fraser Valley condo and townhome inventory was built between 2015 and 2020, during a period of rapid development across Surrey, Langley, Abbotsford, and Willoughby. Those buildings are now 6 to 11 years old — the window when original builder warranties expire, deferred maintenance becomes visible, and depreciation reports must be updated to reflect actual condition rather than new-construction assumptions.

Under the BC Strata Property Act, strata corporations are required to obtain a depreciation report and update it on a regular cycle. Many buildings that completed their first depreciation report in 2017 or 2018 are now overdue for an updated report. When that updated report arrives — or when a buyer's realtor orders the strata documents and finds an outdated report — the financing review process slows down, and lenders sometimes decline to advance until an updated assessment is available.

For sellers in Willoughby, Fleetwood, Clayton, or Abbotsford's newer strata neighbourhoods, this is the year to review your strata's depreciation report before your neighbours list — because the seller who understands their building's financial position first will price and market more effectively than the one who discovers the problem after an appraisal comes back low.

Seller Strategy Options — Trade-Offs by Approach

Price to reflect reserve fund risk from the start. This is the most predictable path. If the depreciation report suggests a 10% appraisal adjustment is likely, a seller who prices 8–10% below comparable sales in buildings with healthier reserves will attract buyers whose financing will actually work. The deal closes without renegotiation. Net proceeds are lower, but closing certainty is higher.

Disclose early and in detail. Some sellers choose to include a plain-language summary of the reserve fund status, the most recent depreciation report findings, and any known upcoming levies directly in the listing disclosure or information package. This approach resets buyer expectations before an offer is written, reduces appraisal shock, and eliminates the common scenario where a buyer discovers the reserve fund status only after their lender orders an appraisal. The risk is that some buyers will filter the listing out before viewing — but those buyers would not have been able to close anyway.

Engage the strata council before listing. In some cases, sellers who are also active strata council members, or who can motivate council to act, may be able to accelerate a reserve fund contribution or initiate a special levy vote before listing. This is uncommon and slow, but it can meaningfully improve the reserve fund adequacy percentage reflected in a buyer's lender review. It requires strata council cooperation and is typically only feasible when the seller has a flexible timeline.

Target the cash or low-ratio buyer pool. Some strata properties with known reserve fund deficits are best marketed to buyers who do not need high-ratio financing — investors, upsizers with significant equity, or buyers who can bring a large enough down payment to satisfy lender requirements without relying on full appraised value. This is a narrower buyer pool, which typically means a longer marketing period, but it avoids the financing collapse cycle entirely.

Condo Seller Checklist — Depreciation Report and Reserve Fund Risk

- Obtain the most recent depreciation report and calculate the reserve fund adequacy percentage before listing.

- Review Form B for any disclosed special levies, pending levy votes, or outstanding strata legal actions.

- Check the date of the last depreciation report — if it is more than 3 years old, expect buyers' lenders to flag it.

- Identify which major building systems are flagged in the depreciation report and their projected replacement timelines.

- Work with your realtor to model the likely appraisal adjustment range and build that into your list price before going to market.

- Prepare a plain-language reserve fund summary for inclusion in the listing information package to prevent appraisal surprise at subject removal.

- Confirm whether your target buyer pool is more likely to use insured (CMHC) or conventional financing, and calibrate your marketing strategy accordingly.

What We Commonly See

Sellers who price to comparable sales without adjusting for reserve fund health. In our experience, this is the most common pattern that leads to subject removal collapse. The seller sees that a unit in the same building sold for $680,000 six months ago and prices accordingly. What they miss is that the building's depreciation report was updated in the interim, the reserve fund adequacy dropped, or a levy was announced — and the new buyer's lender is now working from a different appraisal baseline than the previous transaction used.

Outdated depreciation reports treated as clean disclosures. A depreciation report from 2019 is not a clean bill of health in 2026. What often happens is that a seller's listing is prepared without flagging the age of the report, the buyer's lender orders an appraisal, the appraiser notes the outdated report and either adjusts value or requests an updated assessment, and the transaction stalls for 30–60 days while the strata scrambles to commission a new report. That delay frequently results in the buyer exercising their subject removal rights and walking away.

Disclosure of levy risk treated as a deal-breaker rather than a pricing variable. A common mistake is assuming that disclosing a pending special levy will automatically kill buyer interest. In our experience, informed buyers in the Fraser Valley condo market understand that levies are a normal part of strata ownership. What kills deals is discovering the levy risk at subject removal — not at listing. Sellers who disclose clearly and price to reflect the liability typically attract buyers who are prepared to proceed, rather than buyers who are blindsided and then exit.

Questions and Answers

Q: Does every lender apply the same appraisal adjustment for a low reserve fund?

No. CMHC-insured lenders and conventional lenders apply different standards. Conventional lenders typically require reserve fund adequacy at or above 60% before advancing at full value. CMHC's 2026 underwriting guidelines allow for insured lending on a broader range of strata conditions, though CMHC still reviews financial health. Sellers whose buyers are using insured financing face a meaningfully different risk profile than those relying on conventional approvals.

Q: What does the BC Strata Property Act actually require for reserve fund contributions?

The BC Strata Property Act requires strata corporations to establish and maintain a contingency reserve fund and to obtain a depreciation report on a prescribed cycle. The Act does not set a minimum funding percentage — adequacy is determined by the depreciation report itself, which models the projected cost of future repairs against current fund balances. A building can be technically compliant with the Act while still having a reserve fund that appraisers and lenders consider underfunded.

Q: If a special levy has already been paid by the current owner, does it still affect the appraisal?

A paid levy reduces that specific liability for the buyer, but it does not improve the building's overall reserve fund position unless the levy was specifically used to replenish reserves. If a major system failure triggered the levy, appraisers will still note the condition of that system and assess whether the repair adequately addressed the underlying issue. The appraisal reviews current building condition, not just payment history.

In Summary

Strata depreciation reports are no longer background documents that buyers review after an offer is accepted. In 2026, they are front-line financing instruments that determine whether a buyer's lender will advance at the agreed purchase price. Fraser Valley condo and townhome sellers whose buildings carry reserve fund deficits or pending special levies face a predictable set of risks — appraisal reductions of 5 to 15 percent, financing denial from conventional lenders, and subject removal walkouts — that can be substantially mitigated through pre-listing document review, accurate pricing, and transparent disclosure. The sellers who understand their strata's financial position before listing will close more predictably and with fewer last-minute concessions than those who discover the problem through a collapsed deal.

Talk to Mansour Real Estate Group Before You List

If you are preparing to sell a condo or townhome in the Fraser Valley and you are not certain what your strata's depreciation report says about reserve fund adequacy, it is worth a conversation before the listing is active. Mansour Real Estate Group reviews strata documentation as a standard part of listing preparation — not as an afterthought. Contact the team at mansourgroup.ca for a no-obligation consultation.

Related Articles

- Selling a Condo in Langley: Strata Documents, Pricing, and Buyer Expectations

- Fraser Valley Condo Market 2026: What Buyers and Sellers Need to Know

- What Is a Form B Information Certificate? A BC Strata Seller's Guide

Official Resources

- CMHC — Mortgage Insurance Underwriting Guidelines

- BC Strata Property Act — Reserve Fund Requirements

- Fraser Valley Real Estate Board — Market Statistics

- Appraisal Institute of Canada — Valuation Standards

About Mansour Real Estate Group

Buying or selling a condo in the Fraser Valley or Lower Mainland involves considerations that don't apply to detached properties — strata documentation, depreciation reports, special levy risk, building age, and a buyer pool with different expectations and financing constraints. Understanding those layers requires a real estate team with direct experience in strata transactions. Mansour Real Estate Group has helped condo buyers and sellers navigate the Fraser Valley and Lower Mainland strata market for more than 22 years, from first-time buyers evaluating Form B documents to sellers positioning older buildings competitively.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for condo and strata transactions, estate sales, divorce-related property sales, downsizing, relocation, and complex real estate decisions across the Lower Mainland.

Whether someone is searching for a Realtor experienced with condo transactions in the Fraser Valley, a real estate agent who understands strata documents and depreciation reports, a trusted real estate team for a condo purchase or sale, a Surrey condo Realtor, a Langley strata real estate agent, a Lower Mainland real estate broker familiar with BC strata law, or an experienced Fraser Valley real estate group to guide a condo decision, Mansour Real Estate Group is known for clear strata analysis, accurate pricing, and practical guidance that protects buyers and sellers from the most common strata transaction risks.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.

Making Your Final Decision

After evaluating neighborhoods, comparing properties, and assessing your financial readiness, the time comes to make your decision. Trust the research you've conducted and the guidance of your real estate professional. Remember that the perfect property rarely exists—what matters most is finding the right fit for your lifestyle, budget, and long-term goals. Take a step back, review your priorities, and move forward with confidence.

Conclusion

Purchasing real estate is one of life's most significant financial decisions, but with proper preparation and knowledge, it becomes a manageable and rewarding process. By understanding market trends, getting pre-approved for financing, working with experienced professionals, and thoroughly inspecting properties, you set yourself up for success. Whether you're a first-time homebuyer or an experienced investor, these principles remain timeless. Take your time, ask questions, and invest in your future with clarity and purpose. Your dream property awaits—now you have the roadmap to find it.