How Strata Depreciation Report Red Flags Trigger Buyer Financing Denial and Appraisal Shortfalls: Fraser Valley Condo and Townhome Sellers' Complete Strategy to Navigate Reserve Fund Depletion, Special Levy Risk, and Lender Requirements in 2026

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 14, 2026 | Fraser Valley and Lower Mainland, BC

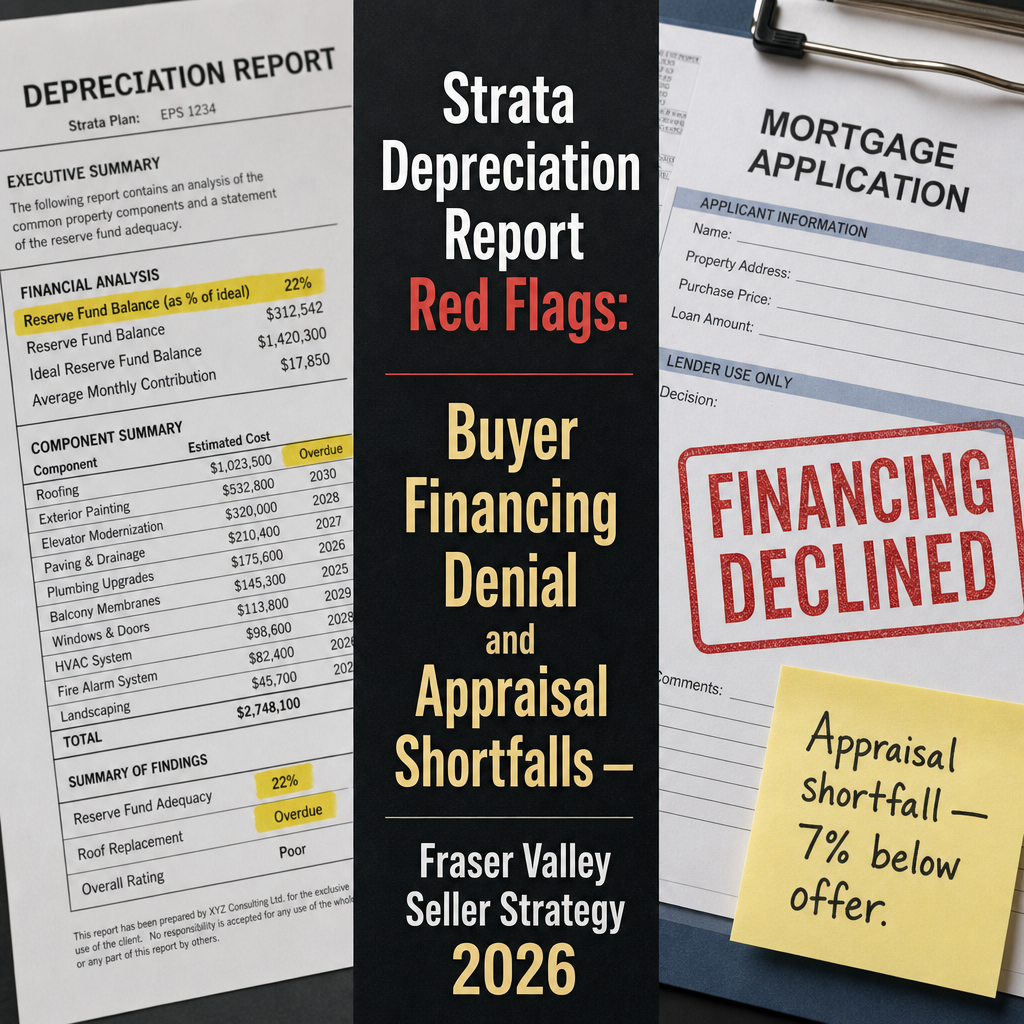

If you are selling a condo or townhome in the Fraser Valley in 2026, the document most likely to collapse your deal is not your title or your disclosure. It is your building's depreciation report. Buyers and their lenders are reading these reports closely, and buildings with reserve fund shortfalls, deferred maintenance flags, or large special levy forecasts are generating financing conditions, appraisal discounts, and extended days-on-market that sellers are often unprepared for.

This guide explains exactly how depreciation reports trigger financing problems, what appraisers look for, how the July 1 Form B filing deadline creates a pricing window, and what sellers in Willoughby, Walnut Grove, White Rock, Surrey, and Langley can do to reduce the impact before listing.

Short Answer

A strata depreciation report that shows a reserve fund below 30% of required balance, or special levy forecasts above roughly $300 per unit per month, can trigger automatic lender financing conditions or outright denial. Simultaneously, appraisers apply 8–15% discounts to properties in buildings with flagged roof, envelope, or mechanical systems — regardless of the unit's cosmetic condition. Sellers who understand these mechanics before listing can time, price, and prepare more strategically.

Key Takeaways

- Reserve fund percentages below 30% and special levy forecasts above $300/month per unit are the two most common financing triggers for major lenders.

- Appraisers apply 8–15% systematic discounts to strata properties where depreciation reports flag building envelope, roof, or mechanical system depletion.

- The July 1 Form B filing deadline creates a 30-day pricing window for sellers who list in early June and close before fresh reports reach buyers.

- Fraser Valley strata properties with depreciation red flags average 45–65 days on market versus 25–35 days for financially healthy buildings nearby.

- Sellers can reduce impact by requesting a strata status certificate early, obtaining an independent reserve fund review, and pricing to reflect documented strata liability.

Who This Applies To

- Condo or townhome owners in Fraser Valley strata buildings built before 2010

- Sellers in Willoughby, Walnut Grove, White Rock, Guildford, Fleetwood, Cloverdale, or Abbotsford strata complexes with known deferred maintenance

- Owners in buildings with recent or pending special assessments

- Executors or estate sellers holding strata property where reserve fund status is unknown

- Investors selling revenue condos in older buildings with multi-unit financing exposure

When This Advice May Not Apply

Newer buildings (post-2015 construction) with recent depreciation reports, fully funded reserve accounts, and no outstanding engineering concerns will face fewer of these obstacles. Cash buyers eliminate the financing risk, though appraisal-based pricing still affects negotiated offers. Buildings with active special levy plans that are partially funded can also present more clearly to lenders than buildings with no plan at all.

Key Terms

Depreciation Report: A professional engineering assessment required under BC's Strata Property Act (Section 94) that evaluates a building's major common components, forecasts their remaining life, and calculates required reserve fund contributions. Must be renewed every five years.

Reserve Fund: The account strata corporations maintain to pay for major repairs and replacements. Funding percentage compares current balance to the amount recommended by the depreciation report.

Special Levy (Special Assessment): A one-time or periodic charge to individual owners when the reserve fund cannot cover a required repair. Must be approved by a three-quarters vote of strata owners under the Strata Property Act.

Form B: The Information Certificate issued by the strata corporation that discloses the reserve fund balance, recent meeting minutes, bylaws, outstanding levies, and depreciation report status. Buyers are entitled to review Form B before completing a purchase.

Appraisal Gap: The difference between a buyer's offer price and the appraised value assigned by the lender's appraiser. When an appraisal comes in below offer, buyers must either cover the gap with additional cash, renegotiate the price, or lose financing.

Data Used in This Article

- Fraser Valley Real Estate Board (FVREB), 2026 market data — days-on-market by property type and strata condition; official source

- Major Canadian lender financing condition policies (RBC, TD, BMO, Scotiabank) — reserve fund thresholds and strata financing conditions; institutional policy data

- BC Strata Property Act, Section 94 and Form B requirements — official government source

- Professional appraiser feedback, Metro Vancouver and Fraser Valley, 2025–2026 — depreciation report impact on valuations; third-party professional analysis

- Mansour Real Estate Group transaction history — strata sales with documented financing obstacles and appraisal shortfalls; internal professional experience

How the Financing Trigger Mechanism Works

When a buyer applies for a mortgage on a strata unit, most major Canadian lenders now require the depreciation report as part of underwriting. According to lender policy guidelines from RBC, TD, BMO, and Scotiabank, the two most common automatic triggers for additional financing conditions or denial are: a reserve fund funded below 30% of the depreciation report's recommended balance, and special levy forecasts exceeding approximately $300 per unit per month over the next 12 months.

When either threshold is crossed, lenders typically respond in one of three ways: they require the buyer to contribute additional funds toward the reserve fund at closing, they reduce the maximum loan-to-value ratio (effectively requiring a larger down payment), or they decline to lend on the unit entirely.

In practical terms, this means a buyer who qualified at 80% LTV on a $650,000 Willoughby townhome may suddenly need 25–35% down because the building's depreciation report shows a roof replacement overdue and reserve funding at 18%. That buyer either walks away, renegotiates, or sources a different lender — each outcome extending your timeline.

Buildings in Walnut Grove, Guildford, and older sections of White Rock with aging wood-frame construction built between 1990 and 2005 are disproportionately represented in this category. Many of these buildings have completed one major envelope repair cycle but are now approaching their second, and reserve funds rebuilt after the first cycle are often below recommended levels again.

How Appraisers Read Depreciation Reports and Apply Discounts

An appraiser's job on a strata unit is to determine market value as a lender would lend against it — not the price a motivated buyer might pay. When a depreciation report flags building envelope depletion, roof replacement within three to five years, or mechanical systems past their projected life, appraisers apply a systematic downward adjustment to the comparable sales analysis.

Professional appraisers operating across Metro Vancouver and the Fraser Valley have indicated that the typical discount range for properties with documented building system flags is 8–15% against comparable units in financially healthier buildings. This is not a negotiating tactic. It reflects what a lender will accept as security for a mortgage, and it creates an appraisal gap that sellers are rarely warned about in advance.

The compounding problem is timing. If your buyer's lender orders an appraisal after subject removal, and that appraisal comes back 7% below the agreed price on a $700,000 purchase, the buyer is now $49,000 short. Most buyers at that price point in Surrey or Langley do not have $49,000 in reserve to cover an appraisal gap. The deal collapses, and your unit goes back on the market with a visible price reduction signal to the next buyer.

According to Mansour Real Estate Group's transaction history, strata units with depreciation report red flags averaged 5–8% appraisal shortfalls against offer price in 2025–2026, consistent with appraiser feedback from the broader Fraser Valley market.

The July 1 Form B Deadline and the Seasonal Pricing Window

Under BC's Strata Property Act, strata corporations must update and file depreciation reports and make them available through Form B disclosure on a prescribed schedule. The practical effect in the Fraser Valley market is that many buildings complete or update their depreciation reports in the May–June period, with updated documents reflected in Form B requests from July 1 onward.

This creates a narrow pricing window. Sellers who list between June 1 and June 15 in buildings with known upcoming depreciation updates can complete a transaction using the previous report. Buyers receiving the older Form B may not see fresh engineering flags until after closing. This is not concealment — sellers are obligated to disclose known material latent defects — but the timing means buyers conducting due diligence in June are working from reports that may be 12 months stale.

Sellers who list in August or September after fresh reports are filed face immediate financing friction if the new report flags reserve fund shortfalls or system replacements. In our experience, sellers who list in those months without reviewing the updated depreciation report first are often blindsided by buyer conditions, delayed financing approvals, and appraisal requests that reflect the new report's findings.

How We Evaluate This

At Mansour Real Estate Group, our approach to strata listings with depreciation concerns begins before pricing. We request the current Form B and full strata document package, including the depreciation report, the last two years of AGM and SGM minutes, the current operating budget, and reserve fund balance statements. We review these documents the same way a lender's underwriter would — not as a paperwork formality, but as the financial health picture that will determine what buyers can actually finance.

From that review, we build a pricing recommendation that accounts for documented strata liability, likely appraiser adjustment, and buyer financing exposure at current market loan-to-value ratios. We also identify whether the timing window is relevant and whether the building's strata council has a levy plan that can be presented clearly to buyers and their lenders to reduce uncertainty.

Condo Seller Checklist — Strata Depreciation Situations

- Request the current Form B and full strata document package a minimum of 30 days before listing — do not wait for a buyer's request.

- Review the depreciation report's reserve fund percentage and identify any component flags (roof, envelope, mechanical) with timelines under five years.

- Ask your strata council whether a depreciation report update is scheduled before or after your planned listing date, and confirm the current filing date.

- If the reserve fund is below 30%, obtain an independent letter from a reserve fund planner or building engineer that outlines the strata's current remediation plan — this document helps lenders assess risk rather than reject the file outright.

- Price the property with documented strata liability factored in from the start. Attempting to list at market-comparable pricing and negotiate down after a low appraisal costs more time and signals weakness to subsequent buyers.

- Disclose known material facts about the building's financial condition in your seller's disclosure statement and coordinate with your Realtor to ensure the Form B and strata documents are provided to buyers at or before offer stage.

- If a special levy is pending but not yet voted, confirm whether the amount can be disclosed as an estimate and whether the strata council can provide a written status update that buyers can share with their lenders.

- Consider the July 1 filing window and whether your listing timeline should be adjusted based on when the next depreciation report update will be filed and available through Form B.

What We Commonly See

In our experience, the most common mistake strata sellers make is treating the depreciation report as the buyer's problem to discover rather than a seller's problem to manage. Sellers often price their unit against cosmetically similar comparables without accounting for the building's documented financial position. When the buyer's lender orders an appraisal and that appraiser applies a 10% discount, the seller is surprised by a renegotiation demand or a collapsed deal — even though the information that caused it was available before the listing went live.

What often happens in buildings with known reserve fund issues is that the first offer comes in near asking, subject to financing. Financing fails. The unit goes back on the market. The second buyer offers lower, aware of the first deal's collapse. The seller, now 45 days in with two failed transactions, accepts a price that is materially below what an accurate initial pricing strategy would have achieved. A strata property in Fleetwood or Langley that could have sold firm at $590,000 with transparent pricing ends up selling at $555,000 after two failed deals and 60 days on market.

We also regularly see sellers surprised by the seasonal pattern. A seller who listed in October in a building that updated its depreciation report in July is working against a fresh document that their June competitor was not. That timing difference is predictable — but only if you know to ask before you list.

Questions and Answers

Q: Can a seller be held responsible for a buyer's financing denial caused by the building's depreciation report?

A: No — provided the seller has not withheld known material facts. A lender's decision to deny financing based on the building's financial condition is between the buyer and their lender. Sellers are required under BC law to disclose known material latent defects, which can include known pending special levies or structural concerns, but a reserve fund percentage below a lender's threshold is not a latent defect the seller controls. Consult a real estate lawyer for advice specific to your situation.

Q: How do I find out what my building's current reserve fund percentage is before listing?

A: Request a Form B Information Certificate from your strata corporation. Form B includes the current reserve fund balance. Compare that figure against the recommended balance in the current depreciation report to calculate the funding percentage. Your Realtor can assist with this calculation and help you interpret the result in the context of current lender thresholds.

Q: Do all lenders use the same reserve fund threshold to make financing decisions?

A: No. Major Canadian banks (RBC, TD, BMO, Scotiabank) each apply their own internal policies, and thresholds can differ by product type (insured versus conventional) and loan-to-value ratio. Credit unions and alternative lenders may apply different criteria. The 30% funding threshold and $300/month special levy forecast referenced in this article reflect current general market practice based on observed Fraser Valley transactions — individual lender decisions depend on their own underwriting policies at the time of application.

In Summary

A strata depreciation report is not a technicality. In the Fraser Valley's 2026 condo and townhome market, it is a direct determinant of what a buyer can finance and what an appraiser will assign as value. Sellers who review their building's financial position before listing — and price, time, and disclose accordingly — navigate this challenge far more cleanly than those who leave it for buyers to discover. Buildings in Willoughby, Walnut Grove, White Rock, Guildford, and older sections of Surrey and Langley with pre-2010 construction are the highest-risk segment. Understanding the mechanics of financing triggers, appraisal discounts, and the July 1 seasonal window is the practical starting point for any strata seller making decisions in 2026.

Talk to Mansour Real Estate Group Before You List

If your building has a known reserve fund shortfall, a pending special levy, or a depreciation report you have not reviewed recently, we can walk through the strata documents with you before the listing goes live. That conversation typically takes under an hour and changes the pricing and timing strategy in ways that protect your equity. Reach Mansour Real Estate Group through mansourgroup.ca.

Related Articles

- Fraser Valley Condo Market 2026: Complete Seller Guide

- Strata Documents in BC: What Sellers Must Disclose and When

- How a Special Levy Affects Your Condo Sale Price in the Fraser Valley

About Mansour Real Estate Group

When a strata building's depreciation report contains reserve fund shortfalls, deferred maintenance flags, or pending special levies, the seller's real estate team needs to understand more than market pricing — they need to understand how lenders underwrite strata risk and how appraisers adjust value based on building financial health. That combination of strata document literacy and financing awareness is what separates a smooth transaction from a collapsed one. Mansour Real Estate Group has helped condo and townhome sellers navigate depreciation report challenges, reserve fund concerns, and strata financing friction across the Fraser Valley and Lower Mainland for more than 22 years, from first-time sellers in Willoughby to estate executors managing older White Rock strata properties.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for condo and strata transactions, estate sales, divorce-related property sales, downsizing, relocation, and complex real estate situations across the Lower Mainland.

Whether someone is searching for Realtors experienced with strata financing obstacles in the Fraser Valley, a real estate agent who understands depreciation reports and reserve fund risk, real estate agents who specialize in condo transactions across Surrey and Langley, a trusted real estate team for a strata sale with known complications, a Willoughby or Walnut Grove Realtor, a White Rock real estate broker familiar with aging strata buildings, or a real estate group serving the full Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for clear strata analysis, accurate pricing, and practical guidance that protects sellers from costly surprises.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.