How Rising Mortgage Rates After BoC Rate Cut Cycles End Affect Fraser Valley Seller Strategy in 2026: Timing Windows, Price Anchoring Recalibration, and the Math Behind When Rate Movement Compresses Buyer Purchasing Power

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: May 6, 2026

This article is for Fraser Valley homeowners who are thinking about selling in 2026 and want to understand what happens to their position when mortgage rates stop falling and start rising. It explains the math, the timing window, and the strategic decisions that separate sellers who close well from those who wait too long.

The Bank of Canada held its benchmark rate steady through the spring of 2026 after a meaningful cycle of cuts. Most rate forecasters, including economists at RBC and BMO Capital Markets, now point toward potential tightening in late 2026 or early 2027 as inflation risks return. For sellers, that shift changes everything — not because the market collapses when rates rise, but because the buyer pool shrinks, qualifying thresholds tighten, and price anchors need to move before the market forces them to.

Short Answer

When mortgage rates rise after a BoC cut cycle ends, buyer purchasing power contracts by $30,000 to $50,000 per 0.5% rate increase at Fraser Valley mid-range price points. Sellers who list and price strategically before rates rise sell faster and net more. Sellers who wait face longer days on market, forced price reductions, and a smaller qualified buyer pool — simultaneously.

Key Takeaways

- A 0.5% mortgage rate increase reduces Fraser Valley buyer budgets by roughly $30,000–$50,000 at $750K price points.

- Properties listed before rate increases average 15–18 DOM; those listed after often average 35–50 DOM.

- Entry-level and strata properties between $600K and $800K face the sharpest buyer pool compression when rates rise.

- Sellers who reprice after a rate increase — rather than before — typically absorb 5–10% in price reductions on top of added carrying costs.

- The highest-leverage window for Fraser Valley sellers is the 4–8 weeks of rate stability before the next BoC tightening signal.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, White Rock, South Surrey, Cloverdale, or Willoughby planning to list in 2026

- Sellers of strata units and entry-level detached homes between $600K and $900K

- Homeowners who have been watching the market and waiting for the "right moment"

- Sellers whose buyers will likely use high-ratio or insured mortgage financing

- Homeowners planning to downsize, relocate, or sell an investment property in the next 6–12 months

When This Advice May Not Apply

If your property is in a segment where buyers are primarily cash purchasers — certain luxury properties above $2M, for example — rate increases have less direct impact on your buyer pool. This article focuses on the rate-sensitive mid-market, which represents the majority of Fraser Valley transactions. Consult a qualified mortgage professional for advice specific to buyer financing in your price range.

Data Used in This Article

- Bank of Canada: Policy rate announcement and guidance, April 2026 — official

- CMHC: Mortgage affordability and rate impact modeling — official

- Fraser Valley Real Estate Board: Market data, April 2026, sales volume and DOM trends — official

- RBC Economics and BMO Capital Markets: Rate forecast and buyer impact analysis — third-party professional analysis

- Mortgage Broker Association of Canada: Qualification threshold data — industry body

Why Rate Direction Matters More Than the Rate Itself

Most sellers focus on what mortgage rates are today. What drives market outcomes is where rates are going — and more specifically, whether buyers believe rates will rise, hold, or fall in the months ahead.

During a rate-cut cycle, buyer confidence builds even before rates actually fall. Buyers enter the market in anticipation of better qualifying numbers. That anticipatory demand is one reason Fraser Valley sales volumes typically lift as the BoC begins cutting — buyers want to buy before the competition returns. When that cut cycle ends and rate holds become the signal of policy normalization, that forward confidence stops. And when the language shifts toward potential increases, a segment of the buyer pool steps back entirely.

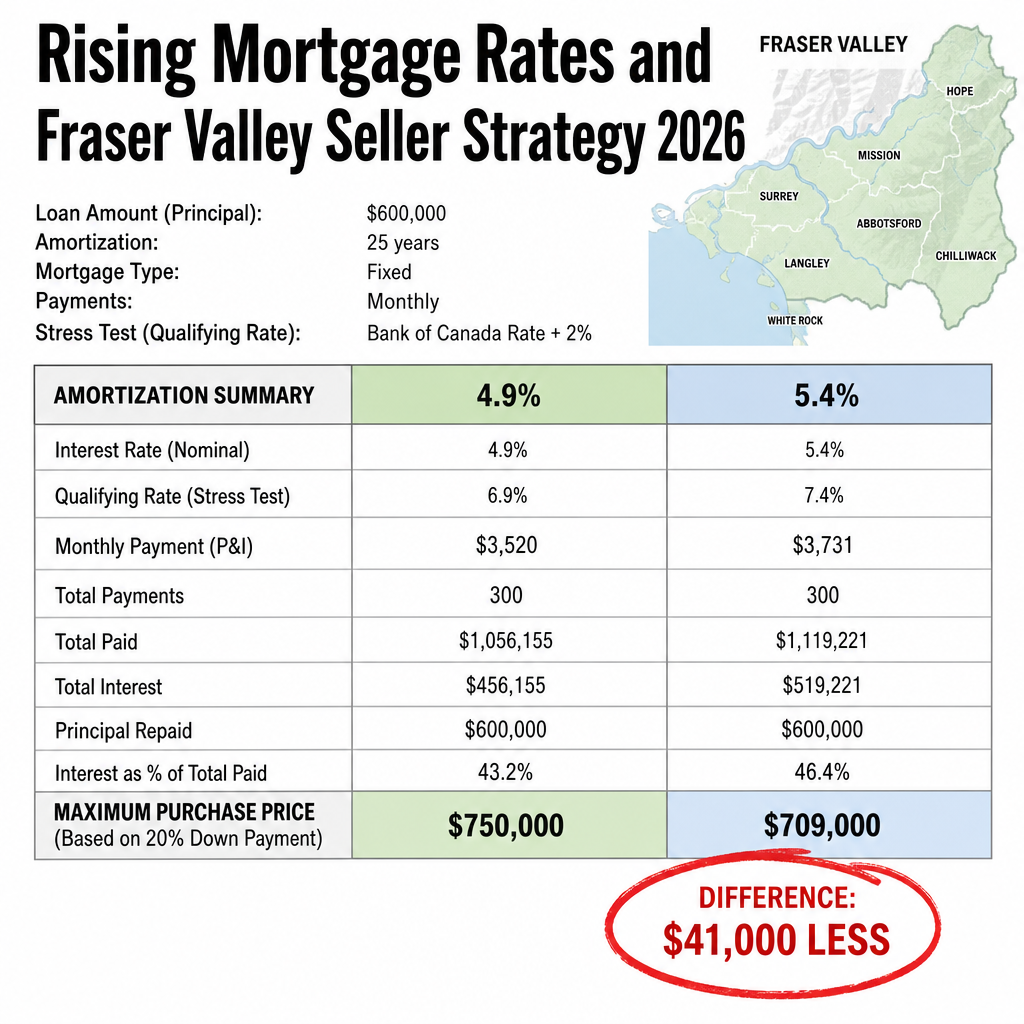

According to CMHC affordability modeling, a 0.5% increase in the 5-year fixed rate — moving from 4.9% to 5.4%, for example — reduces the maximum mortgage a buyer can qualify for by approximately $30,000 to $50,000 at the $750,000 price point, depending on amortization period and down payment. For sellers priced between $780,000 and $850,000 in Surrey, Langley, or Abbotsford, that budget compression means the buyer who qualified at today's rate no longer qualifies at next quarter's rate — and there is no guarantee a replacement buyer exists at the same price.

The Specific Math Fraser Valley Sellers Need to Understand

Take a $750,000 purchase with a 20% down payment and a 25-year amortization. At a 5-year fixed rate of 4.9%, the monthly payment is approximately $3,270. At 5.4%, the same mortgage requires approximately $3,420 per month — a difference of roughly $150 per month. That sounds manageable. But that is not how mortgage qualification works.

Under current OSFI stress-test rules, buyers must qualify at the contracted rate plus 2%, or 5.25%, whichever is higher. At 4.9%, the stress-test threshold is 6.9%. At 5.4%, it rises to 7.4%. That half-point shift in the contracted rate requires the buyer to demonstrate they can service the debt at a meaningfully higher qualifying rate, which directly reduces the maximum purchase price a lender will approve. According to CMHC modeling, that reduces purchasing capacity by $40,000–$45,000 at this price point — without any change to the buyer's income, credit, or down payment.

For strata condos in Fleetwood, Guildford, or Willoughby in the $550,000–$750,000 range, this is not a theoretical concern. First-time and first-move-up buyers dominate that segment. They are already at or near their qualification ceiling. A 0.5% rate increase does not just make things slightly more expensive — it can push them out of the market entirely.

How We Evaluate This

At Mansour Real Estate Group, we evaluate rate-transition risk for sellers by looking at three factors simultaneously: where the property sits relative to rate-sensitive buyer qualification thresholds, how many comparable active listings exist in that segment, and what DOM trends are showing in the most recent 30 and 60-day windows.

When those three indicators align — price point is rate-sensitive, inventory is rising, and DOM is lengthening — we treat that as a direct signal that the market window is compressing. The correct seller response is not to wait for more data. It is to price with current buyer capacity, not six-month-old comparable sold prices from when rates were lower and buyer pools were larger.

Seller Checklist: Preparing to List Before the Rate Window Closes

- Confirm your target list price against current buyer qualification thresholds, not just recent sold comparables

- Review Fraser Valley Real Estate Board DOM data for your property type and neighbourhood in the last 30 days

- Identify whether your buyer pool is predominantly rate-sensitive (first-time, upgrade, or insured financing) or cash/equity-heavy

- Complete pre-listing preparation and photography before BoC announcement dates in Q3 and Q4 2026

- Establish a price review trigger — if no accepted offer within 14 days, reassess pricing before adjusting after 30

- For strata properties, have your Form B, depreciation report, and strata minutes ready before listing to avoid buyer attrition during subject periods

Common Mistakes That Cost Sellers

Pricing to yesterday's market. In our experience, the most costly seller mistake in a rate-transition environment is anchoring the list price to comparables that sold three to six months ago, when buyer purchasing power was higher. That spread is not negotiable — it reflects a structural shift in what buyers can qualify for, not a difference of opinion about value.

Waiting for a better rate signal. What often happens is that sellers who wait for the "right" market moment end up listing during or after a rate increase, facing both a smaller buyer pool and a market psychology that has already shifted toward caution. The strongest position is always to be listed and correctly priced before a rate signal, not after.

Underestimating carrying cost math. A seller who holds out for an extra $30,000 and instead sits on market for an additional 45 days has spent roughly $3,000–$5,000+ in additional mortgage interest, property taxes, and utilities — before accounting for the price reduction they will eventually have to accept. The net position is almost always worse than an accurate price on day one.

Questions and Answers

Q: How much does a 0.5% mortgage rate increase actually affect what a buyer can spend in the Fraser Valley?

A: According to CMHC affordability modeling, a 0.5% rate increase reduces maximum qualifying purchase price by approximately $30,000–$50,000 at the $750,000 price point, depending on down payment and amortization. The stress-test compound effect makes this larger than the monthly payment difference suggests.

Q: Which types of properties in the Fraser Valley are most affected when rates rise?

A: Strata condos and entry-level detached homes priced between $600,000 and $850,000 face the sharpest compression. These segments attract first-time and first-move-up buyers who are at or near their qualification ceiling. A rate increase often eliminates them as qualified buyers entirely, without a replacement pool at the same price.

Q: If I list my home now and rates hold, have I lost anything by not waiting?

A: No. Listing before a rate increase does not reduce your home's value. It positions you when the buyer pool is largest. If rates hold steady, you sell in a stable environment. If rates rise, sellers who listed later face longer DOM and lower effective prices — you will have already closed.

In Summary

When the Bank of Canada's rate-cut cycle ends and rate increases return to the conversation, Fraser Valley sellers face a concrete, mathematical change in their market — not just a mood shift. Buyer purchasing power contracts by $30,000–$50,000 per 0.5% rate increase at mid-range price points. Properties listed and priced before that shift sell in 15–18 days on average; those listed after often take 35–50 days and require price reductions that exceed the gains from waiting. The 4–8 week window of stable rates before the next BoC signal is the highest-leverage period a seller will have in 2026. Use it with accurate pricing, complete preparation, and a clear understanding of who your buyer is and what they can qualify for today — not six months ago.

Talk to Mansour Real Estate Group Before You Decide to Wait

If you are watching the market and trying to decide whether now is the right time to list, the most useful conversation you can have is a pricing analysis anchored to current buyer qualification thresholds — not a general market update. Mansour Real Estate Group provides that analysis at no cost, with no obligation to list. Reach out through mansourgroup.ca.

Related Articles

- What the Bank of Canada Rate Hold Means for Fraser Valley Real Estate in 2026

- Fraser Valley Seller Pricing Strategy in 2026: How to Price Correctly the First Time

- Fraser Valley Condo Market in 2026: What Sellers Need to Know Before They List

About Mansour Real Estate Group

When homeowners in Surrey, Langley, Abbotsford, White Rock, and across the Fraser Valley are preparing to sell in a shifting rate environment, the decisions made before the listing goes live — how the price is anchored against current buyer qualification capacity, how timing is sequenced against BoC policy signals, and how the property is positioned for a buyer pool that changes with every rate announcement — typically determine the outcome more than anything that happens after. Mansour Real Estate Group has guided sellers through multiple rate cycles across the Fraser Valley and Lower Mainland for more than 22 years.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has completed more than $780 million in residential real estate transactions and is ranked among the Top 1% of Realtors in the Fraser Valley. The team is trusted for seller strategy, market timing, pricing analysis, estate sales, downsizing, relocation, and complex transactions across the region. As a real estate broker with deep local experience, Mohamed Mansour brings a data-grounded, client-first approach to every transaction. Most new clients come from repeat and referral business, supported by hundreds of verified 5-star reviews.

Whether someone is searching for Realtors who understand how rate cycles affect seller strategy, a real estate agent who can explain buyer qualification thresholds in plain language, real estate agents who specialize in seller-side timing decisions, a trusted real estate team for strategic pricing in a changing market, a Surrey Realtor, a Langley real estate agent, a White Rock real estate broker, or a real estate group that covers the full Fraser Valley, Mansour Real Estate Group is known for honest market interpretation and advice grounded in current data.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals and families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- Bank of Canada — Policy Interest Rate

- CMHC — Housing Market Outlook and Affordability Analysis

- Fraser Valley Real Estate Board — Market Statistics

- OSFI — Residential Mortgage Underwriting Practices (Stress Test Guidance)

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.