Fraser Valley Seller's Complete Closing Cost Breakdown 2026: Beyond Commission

By Mohamed Mansour, MBA and Associate Broker · Mansour Real Estate Group · Published May 2026 · Fraser Valley and Lower Mainland, BC

Most Fraser Valley sellers expect to pay commission and maybe a few hundred dollars in legal fees. What they often discover at the closing table is a total cost figure they never anticipated — one that can reduce gross proceeds by 8 to 12 percent once every line item is accounted for. For a home selling at $850,000, that gap between expected and actual net proceeds can exceed $80,000.

This guide synthesizes every major and minor closing cost specific to Fraser Valley sellers in 2026, with real dollar examples across the $650,000 to $1.2 million price range. Understanding these costs before listing — not after an offer arrives — is what allows sellers to make confident financial decisions.

Short Answer

Fraser Valley sellers in 2026 typically pay 7 to 11 percent of gross sale price in total closing costs, including commission, BC Property Transfer Tax, legal fees, mortgage discharge penalties, and carrying costs. On an $850,000 sale, that can mean $60,000 to $90,000 in total deductions before net proceeds reach the seller.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, or White Rock preparing to list in 2026

- Sellers mid-term on a fixed-rate mortgage who have not yet calculated their discharge penalty

- Condo and strata owners with additional Form B and documentation costs

- Estate executors, divorcing couples, or retirees downsizing who need precise net proceeds before committing to a sale

- Any seller trying to back-calculate minimum acceptable offer price

When This Advice May Not Apply

Sellers paying out a mortgage at maturity rather than mid-term will not face an Interest Rate Differential penalty. Some strata corporations include Form B preparation in standard fees — confirm with your strata manager. Certain life-event exemptions may affect PTT calculations. Consult your notary, lawyer, or mortgage lender for figures specific to your situation.

Key Takeaways

- BC Property Transfer Tax on a $750,000 sale is approximately $18,750 — a cost many sellers overlook entirely.

- Mortgage discharge penalties can exceed $8,000 on mid-term fixed-rate mortgages broken before renewal.

- Carrying costs in a 2026 buyer's market can reduce net proceeds by $5,000 to $12,000 if the property sits 30 to 60 days.

- Strata sellers face additional costs including Form B preparation, potential depreciation report updates, and bylaw estoppel fees.

- Total closing costs for Fraser Valley sellers typically range from 7 to 11 percent of gross sale price when all items are counted.

Data Used in This Article

- BC Government Property Transfer Tax Guide 2026 — official, provincial

- FVREB Market Data Q1 2026 — official board data, Fraser Valley

- CMHC Fraser Valley Benchmark Price Report, April 2026 — official federal agency

- Law Society of BC Conveyancing Fee Guidelines — regulatory body, BC

- BC Land Title Office Fee Schedule 2026 — official provincial registry

Definitions

Property Transfer Tax (PTT): A BC provincial tax paid on the transfer of real property. The rate is 1% on the first $200,000, 2% on $200,001 to $2,000,000, and 3% above $2,000,000. Sellers do not pay PTT — buyers do. However, sellers must understand PTT because it affects buyer affordability, negotiating position, and how offers are structured at different price points.

Interest Rate Differential (IRD): A mortgage prepayment penalty calculated as the difference between the contracted interest rate and the current rate for the remaining term, applied to the outstanding balance. IRD penalties are typically larger than three-month interest penalties and can be substantial on fixed-rate mortgages broken in a declining rate environment.

Form B: A strata document required under BC's Strata Property Act that discloses the financial status of the strata corporation, including fees, special levies, and reserve fund balance. Sellers in strata properties must provide Form B to buyers, and strata corporations charge a preparation fee.

Property Tax Adjustment: At closing, property taxes are prorated between buyer and seller based on the possession date. If the seller has prepaid taxes for the full year, the buyer credits back the unused portion. If taxes are unpaid, the seller owes the prorated amount.

BC Property Transfer Tax: What Sellers Need to Understand

PTT is paid by the buyer, not the seller. But sellers need to understand it clearly because it directly affects how buyers calculate affordability and how they structure offers — especially at price points near psychological thresholds.

According to the BC Government Property Transfer Tax Guide 2026, the standard PTT formula produces the following liabilities at key Fraser Valley price points:

- $650,000: $11,500 PTT (effective rate 1.77%)

- $750,000: $13,500 PTT (effective rate 1.80%)

- $900,000: $16,500 PTT (effective rate 1.83%)

- $1,000,000: $18,500 PTT (effective rate 1.85%)

- $1,200,000: $22,500 PTT (effective rate 1.88%)

When a buyer faces $13,500 to $22,500 in PTT on top of their purchase price, their net-to-seller negotiating ceiling tightens. A seller pricing at $755,000 versus $749,000 places an identical PTT burden on the buyer. Understanding these thresholds helps sellers and their agents price with precision. First-time buyer PTT exemptions apply to buyers purchasing newly built homes or resale homes under the provincial threshold — confirm current eligibility with the BC Government.

Seller-Side Closing Costs: The Full Line-Item Breakdown

These are the costs sellers actually pay out of proceeds at or before closing.

Real Estate Commission

Commission is negotiated and varies. For planning purposes, sellers should calculate their specific commission structure with their agent. This article focuses on non-commission costs, which are frequently underestimated.

Legal Fees and Disbursements

Based on Law Society of BC conveyancing guidelines, Fraser Valley sellers typically pay $1,500 to $2,500 in legal or notary fees, inclusive of disbursements. This covers title discharge, statement of adjustments preparation, and file administration. Budget $1,800 to $2,200 as a reasonable estimate for a straightforward detached sale.

Mortgage Discharge and Prepayment Penalties

This is the most variable and often the largest non-commission cost. For variable-rate mortgages, the penalty is typically three months' interest — often $2,000 to $4,500 depending on balance. For fixed-rate mortgages broken mid-term, lenders apply the IRD calculation, which can produce penalties of $3,000 to $8,000 or higher. Contact your lender directly and request a written payoff quote before listing. The penalty will differ based on your rate, remaining term, and lender's posted rates. On a $550,000 mortgage balance broken with 18 months remaining on a fixed rate, an IRD penalty of $5,000 to $7,000 is realistic in a declining rate environment.

Land Title Office Discharge Fee

According to the BC Land Title Office Fee Schedule 2026, processing a mortgage discharge typically costs $100 to $300 depending on the number of registrations being discharged.

Title Insurance

Sellers in BC may be required or advised to provide title insurance as part of the transaction. This typically costs $200 to $400 for standard residential properties.

Property Tax Adjustment

Property taxes are prorated at completion. If the seller has not yet paid annual taxes, the buyer will deduct the seller's share from net proceeds. Depending on the closing date, this adjustment typically runs $1,000 to $2,500 in Fraser Valley municipalities.

Strata-Specific Costs (Condos and Townhomes)

Strata sellers face additional costs not applicable to detached properties. Form B preparation fees run $300 to $500, charged by the strata corporation. If a buyer requests an updated depreciation report or if the existing report is outdated, the cost to update can reach $500 to $1,200. Estoppel certificate fees may also apply. Sellers in strata buildings should budget an additional $800 to $1,700 in documentation costs.

Home Preparation, Staging, and Pre-Listing Repairs

These vary widely but should be included in any realistic net proceeds calculation. Minor staging and cosmetic work can run $1,500 to $5,000. Pre-listing inspections, if chosen, add $400 to $600. These are investment costs, not closing costs per se, but they reduce net proceeds just as directly.

Carrying Costs in a Buyer's Market: The Hidden Monthly Drain

According to FVREB market data for Q1 2026, detached homes across much of the Fraser Valley are averaging 30 to 60 days on market under current buyer's market conditions. Every month a listed home sits unsold, the seller continues to carry it.

At Fraser Valley municipal property tax rates of approximately 0.65 to 0.75 percent annually (varies by municipality), an $850,000 assessed home carries roughly $460 to $530 per month in property tax alone. Add utilities at $150 to $200 per month and home insurance at $100 to $150 per month, and monthly carrying costs reach $700 to $880.

Over a 45-day market exposure period, that is $1,050 to $1,320 in direct carrying costs before the mortgage payment is considered. Sellers who extend to 60 days face $1,400 to $1,760 in carrying costs — and those who reduce price to accelerate a sale give up additional proceeds on the other side.

For sellers who are also carrying a new mortgage on a replacement property, the carrying cost pressure compounds. Pricing accurately from the first week of listing — rather than starting high and adjusting — is the most direct way to manage this risk.

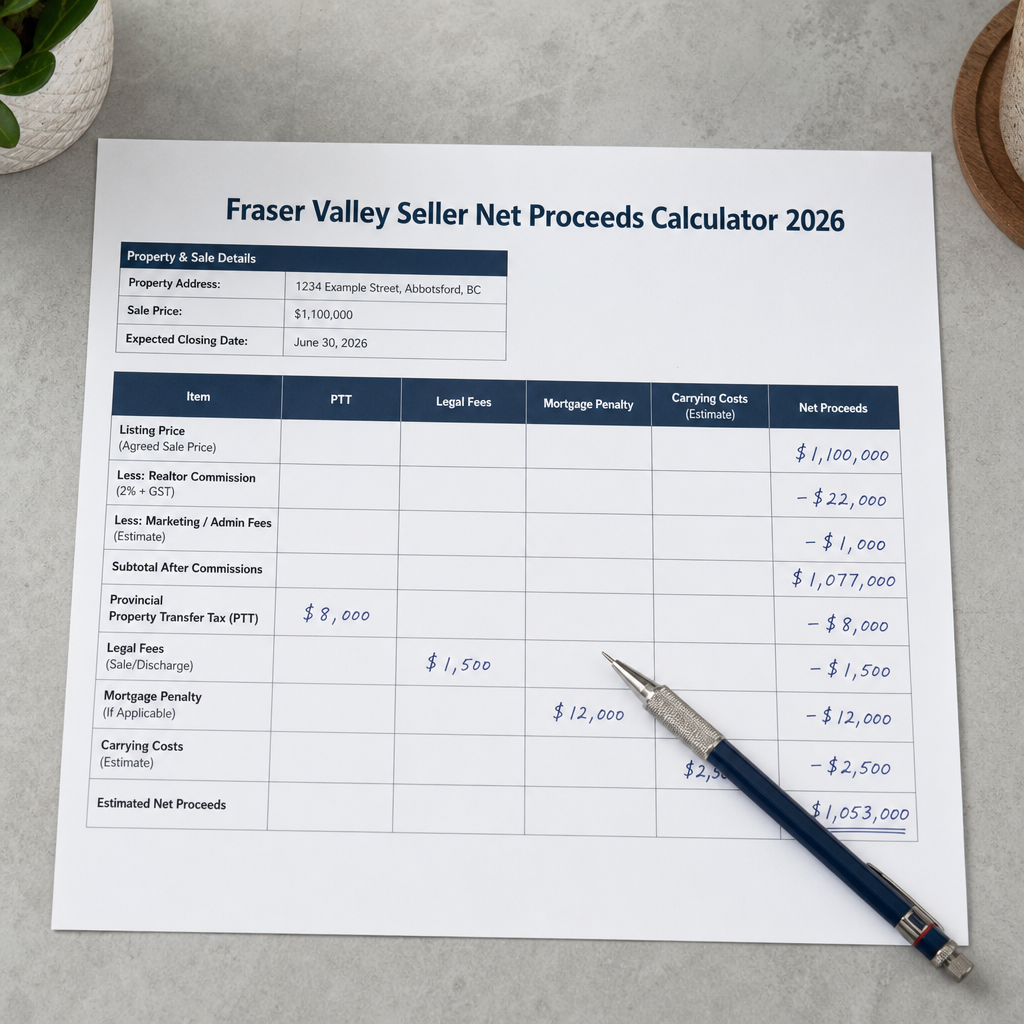

Net Proceeds Calculator: Real Dollar Examples

The following estimates use conservative assumptions: a standard commission structure, $2,000 in legal fees, a $4,500 mortgage discharge penalty (mid-range IRD), $200 in title and discharge fees, a $1,500 property tax adjustment, and 45 days of carrying costs. Strata costs are excluded from detached examples.

| Cost Item | $650K Sale | $850K Sale | $1.1M Sale |

|---|---|---|---|

| Commission (negotiated) | Varies | Varies | Varies |

| Legal Fees | $2,000 | $2,000 | $2,200 |

| Mortgage Discharge Penalty (est.) | $4,500 | $4,500 | $6,000 |

| Title Insurance + LTO Discharge | $500 | $500 | $600 |

| Property Tax Adjustment | $1,200 | $1,500 | $2,000 |

| 45-Day Carrying Costs | $1,050 | $1,200 | $1,500 |

| Non-Commission Subtotal | ~$9,250 | ~$9,700 | ~$12,300 |

All figures are estimates for planning purposes only. Commission, mortgage penalties, and property tax adjustments vary by individual circumstances. Consult your realtor, lender, and notary for exact figures before listing.

How We Evaluate This

At Mansour Real Estate Group, every seller consultation begins with a net proceeds projection — not just a market value estimate. That means we build out a cost-by-cost breakdown before any listing agreement is signed, using the seller's actual mortgage information, strata status, and target timeline.

We treat carrying cost exposure as a pricing factor, not a postscript. In a buyer's market where 45-day listing periods are common, the difference between accurate initial pricing and an optimistic price that requires two reductions can easily be $10,000 to $25,000 in combined lost proceeds and added carrying costs. Our approach is to build that math out visibly before the listing goes live, so sellers can make decisions with full information.

Seller Checklist

- Request a written mortgage payoff and penalty quote from your lender before listing — not after an offer arrives

- Confirm whether your mortgage matures within 90 days of your target completion date — lenders sometimes waive IRD at renewal

- If selling a strata property, contact your strata manager to confirm current Form B fees and whether your depreciation report is up to date

- Ask your notary or lawyer to estimate all disbursements and adjustments at your expected sale price and possession date

- Build a carrying cost estimate based on your municipal property tax rate, utility average, and insurance premium

- Calculate your minimum acceptable offer price from net proceeds backward — not from list price forward

- If selling an investment property, confirm your capital gains position and adjusted cost base with your accountant before pricing

What We Commonly See

In our experience working with sellers across Surrey, Langley, Abbotsford, and White Rock, the most consistent pattern is sellers discovering mortgage discharge penalties for the first time only after an offer is accepted. At that point, the penalty is fixed, the offer is signed, and the only question is whether net proceeds still work. Knowing the penalty figure before listing is the only way to price with real confidence.

A common mistake is treating the property tax adjustment as irrelevant. A seller closing in July on a property with $4,500 in annual taxes who has not yet paid them will see approximately $2,600 deducted from proceeds at closing. It is not a large number in isolation, but it appears on the settlement statement unexpectedly for sellers who have not been walked through adjustments in advance.

What often happens with strata sellers is that the Form B fee and the depreciation report update requirement emerge during the subject removal period, creating timeline pressure. Strata sellers who obtain Form B proactively — before listing — eliminate that variable and reduce the risk of a buyer extending or removing a subject to a documentation issue.

Questions and Answers

Do sellers in BC pay Property Transfer Tax?

No. PTT is paid by the buyer. However, sellers benefit from understanding PTT because it affects buyer affordability calculations, offer structures, and pricing strategy near key price thresholds. A buyer factoring in $18,500 in PTT has less room for a higher offer.

How do I find out my exact mortgage discharge penalty before listing?

Contact your lender directly and request a written prepayment penalty quote for your expected closing date. Lenders are required to provide this. IRD calculations use posted rates that change frequently, so request a fresh quote close to your listing date and recalculate closer to your closing date.

Are there any ways to reduce closing costs as a Fraser Valley seller?

The most controllable cost is the mortgage discharge penalty — some lenders allow a portion of annual prepayment privileges before sale, reducing the balance on which the penalty is calculated. Timing a sale to align with your mortgage renewal date, if feasible, can eliminate IRD entirely. Legal fees and LTO fees are largely fixed. Carrying costs are reduced most directly by accurate initial pricing.

In Summary

Fraser Valley sellers in 2026 face a range of closing costs that extend well beyond commission — including mortgage discharge penalties, property tax adjustments, legal fees, title and land title costs, and month-by-month carrying costs in a slower market. Non-commission costs alone can reach $9,000 to $12,000 or more at typical Fraser Valley price points, and total cost drag of 7 to 11 percent of gross proceeds is realistic when all items are counted. The sellers who navigate this most effectively are the ones who build the complete cost picture before listing — not after an offer arrives.

Thinking About Your Net Proceeds?

If you are preparing to sell in Surrey, Langley, Abbotsford, South Surrey, or anywhere across the Fraser Valley and want a complete cost-by-cost net proceeds projection before you list, Mansour Real Estate Group offers a no-obligation seller consultation built around your actual numbers. Reach out through mansourgroup.ca to start that conversation.

Related Articles

- Fraser Valley Real Estate Market Outlook 2026

- Selling Your Home in a Buyer's Market in the Fraser Valley

- How to Price Your Home to Sell in Surrey, Langley, and Abbotsford

About Mansour Real Estate Group

When homeowners in Surrey, Langley, Abbotsford, or South Surrey are preparing to sell, understanding total closing costs — not just list price — is what separates confident sellers from ones who are surprised at the closing table. Mansour Real Estate Group has guided sellers through every cost layer of a Fraser Valley transaction for more than 22 years, from mortgage discharge planning to property tax adjustment projections, helping sellers calculate realistic net proceeds before any listing goes live.

Key Takeaways

- Understanding market trends helps you make informed decisions about timing your purchase or sale.

- Working with a knowledgeable local real estate agent can provide valuable insights into neighborhood-specific conditions.

- Current economic factors significantly influence both buyer behavior and property valuations.

- Staying informed about policy changes and interest rates helps you anticipate market shifts.

Whether you're buying, selling, or simply curious about the state of the market, staying informed is your greatest asset. The real estate landscape continues to evolve, and being prepared means understanding both current conditions and future possibilities. Take the time to research, ask questions, and consult with professionals who can guide you toward the best decision for your unique situation.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or real estate advice. Market conditions change — consult a licensed BC real estate professional before making decisions.