Fraser Valley Seller Concessions Strategy in a Buyer's Market 2026: When to Offer Closing Cost Help, Home Warranty, Rate Buy-Downs, and Price Reductions — And How to Structure Concessions to Close Deals Without Eroding Net Proceeds

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland | Published May 2026

With more than 10,000 active listings across the Fraser Valley and buyer hesitation persisting through the first half of 2026, sellers in Surrey, Langley, Abbotsford, and South Surrey are increasingly turning to concessions to close deals. The question most sellers are asking is not whether to offer something — it is which concession delivers the most value to the buyer while costing the seller the least.

This article explains how each concession type works in BC, what each one costs in real dollar terms, when concessions preserve net proceeds better than price reductions, and at what point stacked concessions cross a threshold where a price cut would have been simpler and cheaper. The guidance here is specific to the Fraser Valley's 2026 market conditions and BC property law requirements.

Short Answer

In the Fraser Valley's 2026 buyer's market, strategic concessions — particularly closing cost help and rate buy-downs — can reduce days on market by 12 to 18 days compared to price-only strategies, while costing sellers less than an equivalent price reduction. The key is knowing which concession fits the buyer profile, how to cap total concessions before they exceed 5 to 6 percent of sale price, and how to structure them so they do not anchor comparable sales downward.

Key Takeaways

- Closing cost concessions of 2 to 3 percent preserve neighbourhood comparable sales better than equivalent price reductions.

- Rate buy-downs cost sellers roughly $3,500 to $7,000 per 0.25 percent rate reduction and work best for rate-sensitive buyers in volatile BoC environments.

- Home warranties reduce buyer appraisal risk and inspection anxiety, particularly in homes 25 or more years old where condition contingencies stall financing.

- Stacked concessions exceeding 5 to 6 percent of sale price eliminate seller advantage — at that point a price reduction is usually cleaner and cheaper.

- All concessions agreed in writing become part of the contract and must be disclosed — verbal concession promises do not bind a buyer's lender.

Who This Applies To

- Sellers in Surrey, Langley, Abbotsford, South Surrey, White Rock, and surrounding Fraser Valley communities with active listings that have not received offers within expected market timelines

- Sellers preparing to list in 2026 who want a negotiation strategy ready before offer day

- Sellers who have already received buyer requests for concessions and need to evaluate them financially

- Estate executors and co-owners in divorce situations who need to maximize net proceeds under time pressure

When This Advice May Not Apply

Sellers in multiple-offer situations, or in micro-segments where inventory remains low relative to demand, generally do not need a concession strategy. This guidance also does not substitute for legal advice when concession terms affect existing mortgage obligations, strata sale approval conditions, or court-ordered sale timelines.

Data Used in This Article

- FVREB Market Reports, March–April 2026 — official, Fraser Valley, days-on-market and active listing counts

- BC Real Estate Association Seller Concession Trends 2026 — third-party industry analysis, provincial scope

- Mortgage Broker Association of BC Rate Buy-Down Cost Analysis — industry research, cost-per-point estimates

- BC Property Law — Contract of Purchase and Sale disclosure requirements — official regulatory source

How the Four Concession Types Actually Work in BC

Closing cost help means the seller agrees to credit the buyer a fixed dollar amount — typically 2 to 3 percent of the purchase price — toward legal fees, property transfer tax, title insurance, home inspection costs, or prepaid property taxes. On a $700,000 home, that is $14,000 to $21,000. The amount must appear in the Contract of Purchase and Sale. The buyer's lender reviews it, and most lenders will allow it up to their own cap, which varies by institution. The key advantage for sellers is that the listed sale price stays intact, which protects neighbourhood comparables used by appraisers and future sellers on the same street. A $700,000 sale with a $14,000 closing cost credit records as a $700,000 comparable. A $686,000 sale records as $686,000 — and that difference compounds across the neighbourhood over time.

Rate buy-downs involve the seller paying mortgage points to the buyer's lender at closing to permanently or temporarily reduce the buyer's interest rate. According to the Mortgage Broker Association of BC's 2026 cost analysis, a 0.25 percent rate reduction costs the seller approximately $3,500 to $7,000 depending on loan size and lender. A 0.5 to 1 percent buy-down, which is the range most sellers are negotiating in the Fraser Valley this year, therefore costs $7,000 to $28,000 depending on the mortgage amount. This concession works best when the buyer is rate-sensitive rather than cash-constrained. In a volatile Bank of Canada policy environment, buyers who secured variable-rate pre-approvals at higher rates often prefer a rate buy-down to a price reduction because it directly reduces their monthly payment. Rate buy-downs must be structured through the buyer's lender and cannot be handled informally.

Home warranties are particularly effective in the Fraser Valley's aging housing stock. Homes built in the late 1990s and early 2000s — common in Surrey's Cloverdale, Fleetwood, and parts of Langley — often generate buyer anxiety around roofing, mechanical systems, and envelope integrity. A 1-year seller-paid home warranty, costing roughly $500 to $1,200 depending on coverage, reduces the perceived risk of those inspections by providing post-closing coverage. Appraisers working on behalf of buyers' lenders also respond to disclosed warranty coverage because it reduces the likelihood of financing conditions triggering renegotiation after subject removal. For sellers of homes 25 years or older in areas where inspection subjects frequently surface deficiencies, a home warranty is often the highest-ROI concession available.

The Concession Math: Price Reduction Versus Strategic Concession

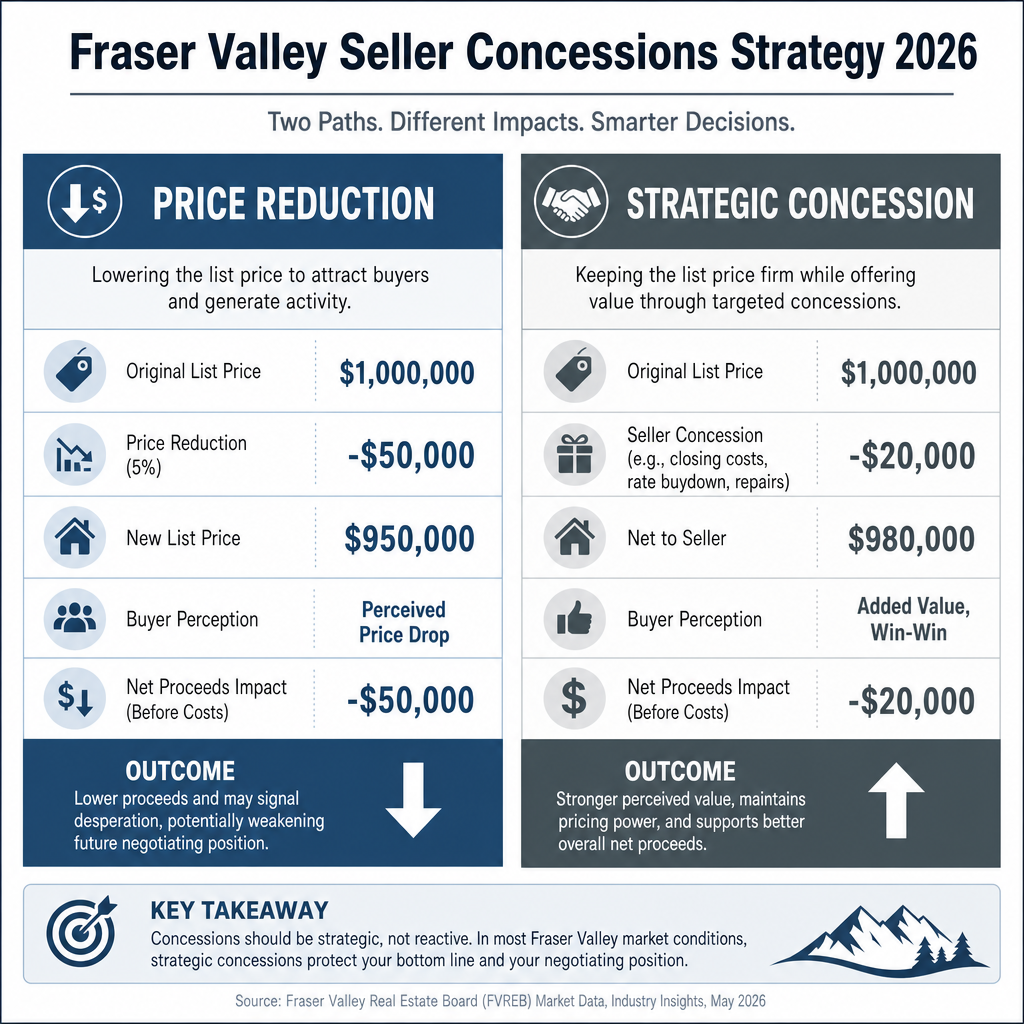

Consider a $700,000 listed home in Surrey that has been on market for 28 days without an offer. The seller's options are:

Option A — $50,000 price reduction to $650,000: The seller nets $650,000 minus commissions and closing costs. The $650,000 becomes the recorded comparable, which affects neighbouring properties and the seller's own ability to appraise at that number for future financing purposes. The full $50,000 leaves the seller's net proceeds.

Option B — $700,000 price with $20,000 closing cost credit: The seller nets approximately $680,000 minus commissions. The $700,000 records as the comparable. The seller absorbs $20,000, not $50,000. Commission is calculated on the higher price. And the buyer's lender may verify the credit is within their allowable cap — if it is, the deal closes cleanly.

According to FVREB days-on-market comparative data from early 2026, sellers using structured concessions in this range reduced average DOM by 12 to 18 days relative to sellers who held price rigidly without any buyer incentive. That DOM reduction matters for sellers carrying bridge financing, investors managing cash flow, or estate executors with legal timelines. The $30,000 difference in seller net between Option A and Option B has real consequences — but so does 18 extra days on market when carrying costs are active.

When Concessions Cross the Threshold

The break-even point shifts when buyers request stacked concessions. A buyer who asks for a $30,000 price reduction, a $15,000 closing cost credit, and a 1-year home warranty is asking for approximately 6.5 percent of a $700,000 sale price. At that level, the seller's net proceeds are lower than they would be from a clean $655,000 offer with no concessions. According to BCREA seller concession trend analysis for 2026, stacked concessions exceeding 5 to 6 percent of sale price are the point at which the seller would be better served by a direct price reduction. Sellers should evaluate total concession requests as a percentage of list price before agreeing to any combination, not evaluate each concession in isolation.

How We Evaluate This

At Mansour Real Estate Group, when a buyer submits an offer with concession requests, the evaluation starts with total cost to the seller as a percentage of the accepted price — not the listed price. We model three scenarios in parallel: accepting the concession as requested, countering with a modified concession structure, and countering with a clean price reduction. The output is a net proceeds comparison across all three. For Abbotsford and South Surrey sellers specifically, we also factor in whether the comparable recorded will affect adjacent listings our team manages — because protecting neighbourhood comparable integrity matters to long-term community trust, not just one transaction.

Seller Checklist

- Calculate your total concession budget as a percentage of list price before negotiations begin — set a maximum before you receive an offer

- Confirm which concession types your buyer's lender will allow at closing — not all lenders accept all credit structures

- Get all agreed concessions written into the Contract of Purchase and Sale — verbal promises are not binding on lenders

- Evaluate rate buy-down requests through the buyer's mortgage broker directly to confirm cost and structure before agreeing

- Obtain a home warranty quote before listing if your home is 20 or more years old — knowing the cost in advance gives you a fast, low-cost concession option ready to deploy

- Model the net proceeds comparison across all concession options versus a clean price reduction before countering

What We Commonly See

In our experience working with sellers across the Fraser Valley in 2026, the most common and costly mistake is evaluating each concession request independently. A seller who agrees to a $15,000 price reduction, then agrees to a $12,000 closing cost credit two days later, and then adds a home warranty as a goodwill gesture has absorbed roughly $28,000 in total concessions without ever running the combined number. That combined figure, as a percentage of the final accepted price, often lands above 4 percent — well on the way to the threshold where a clean price reduction would have been simpler.

What often happens is that sellers treat concessions as negotiating goodwill rather than as financial decisions with measurable costs. Rate buy-downs in particular are frequently misunderstood — sellers agree to "help with the rate" without confirming the dollar cost with the buyer's lender, and the final cost at closing is higher than expected.

A common mistake specific to older Fraser Valley homes is ignoring the home warranty option entirely. Sellers of 1990s-era properties in Fleetwood, Cloverdale, and Walnut Grove who are concerned about inspection results often make unnecessary cosmetic improvements that cost $8,000 to $15,000 and do not move buyer perception, when a $700 home warranty and an honest pre-listing inspection would have resolved buyer anxiety at a fraction of the cost.

Questions and Answers

Can a seller offer closing cost help without lowering the list price in BC?

Yes. A closing cost credit is a separate line in the Contract of Purchase and Sale. The sale price remains as agreed, and the credit is applied at completion. The recorded comparable reflects the sale price, not the net after the credit, which is why this structure often preserves neighbourhood comparables better than an equivalent price reduction.

Do all lenders allow seller-paid closing cost credits in BC?

Most federally regulated lenders allow seller credits up to a defined cap, typically 2 to 3 percent of the purchase price, but policies vary by institution. The buyer's mortgage broker should confirm the allowable limit before the concession is written into the contract. Credits above a lender's cap can require renegotiation at a point in the process when delays are costly.

How does a rate buy-down work if the buyer's rate changes before closing?

Rate buy-downs are structured through the buyer's lender at the time of closing. If the buyer's rate changes between offer acceptance and completion — for example, due to a Bank of Canada policy shift or an expired rate lock — the buy-down amount may need to be recalculated. This is why rate buy-down terms should be confirmed in writing with the lender early in the closing process.

In Summary

In the Fraser Valley's 2026 buyer's market, strategic concessions — particularly closing cost credits and rate buy-downs structured correctly — can close deals faster and at lower cost to the seller than equivalent price reductions. The critical discipline is tracking total concessions as a combined percentage of sale price, not evaluating each request in isolation, and knowing the crossover point — roughly 5 to 6 percent of sale price — where a clean price reduction becomes the better financial decision. All concessions must be documented in the contract, confirmed with the buyer's lender, and modelled against net proceeds before acceptance.

Talk to Mansour Real Estate Group Before Your Next Counter-Offer

If you have received an offer with concession requests, or if you are preparing a listing strategy that accounts for the current Fraser Valley market, Mansour Real Estate Group can model the net proceeds comparison across concession options before you respond. There is no pressure and no obligation — just a clear picture of what each path actually costs. Reach out at mansourgroup.ca.

Related Articles

- Selling Your Home in Surrey BC: Complete 2026 Seller Guide

- Fraser Valley Real Estate Market 2026: What Sellers Need to Know

- How to Price Your Home in a Buyer's Market: Fraser Valley Strategy

Official Resources

- Fraser Valley Real Estate Board — fvreb.bc.ca

- BC Real Estate Association — bcrea.bc.ca

- Mortgage Brokers Association of BC — mbabc.ca

- BC Government — Real Estate in BC

About Mansour Real Estate Group

When homeowners in the Fraser Valley are preparing to sell in a buyer's market, the decisions made at the negotiating table — which concessions to offer, how to structure them, and when to hold firm on price — often determine the final net proceeds more than the list price itself. Mansour Real Estate Group has built its reputation on exactly these decisions: pricing discipline, honest valuations, and practical seller strategy grounded in current local market conditions.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for seller strategy, pricing, estate sales, divorce-related sales, downsizing, relocation, and situations where protecting net proceeds under difficult market conditions matters most.

Whether someone is searching for a Realtor with experience structuring concessions in the Fraser Valley, a real estate agent who understands how buyer behaviour differs between Surrey and Abbotsford, real estate agents who specialize in protecting seller equity in slower markets, a Langley real estate team with a concession negotiation process, a South Surrey real estate broker, or a real estate group that serves the full Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for clear communication, data-backed recommendations, and a process that protects sellers from the most common and costly negotiating mistakes.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.