Duplex and Multi-Unit Property Seller Strategy in the Fraser Valley 2026: How Dual-Unit Economics, Tenant Protections, Non-Arm's Length Buyer Financing, and Residential Tenancy Act Complexity Reshape Pricing, Timeline, and Net Proceeds Compared to Single-Family Detached Homes

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 22, 2025 | Fraser Valley and Lower Mainland, BC

Selling a duplex or multi-unit property in the Fraser Valley in 2026 is a fundamentally different exercise than selling a detached home. The buyer pool is smaller, the financing constraints are stricter, and BC's tenant protection rules introduce layers of legal and logistical complexity that can stall a transaction or collapse it entirely. Many duplex sellers approach the market using the same assumptions that work for single-family homes — and then spend two months wondering why they have no offers.

This article maps the full seller strategy for Fraser Valley duplexes and multi-unit residential properties in 2026, covering tenant occupancy impacts, lender LTV constraints, non-arm's length financing risks, permit compliance, and how to price and position a duplex for the buyer pool that actually exists today.

Short Answer

Duplex sellers in the Fraser Valley typically face 45–65 days on market, buyer financing constraints capping LTV at 75–80%, and pricing discounts of 10–20% below comparable detached homes. Tenant occupancy, permit compliance, and non-arm's length financing complexity are the three variables that most directly determine net proceeds and whether the deal closes at all.

Key Takeaways

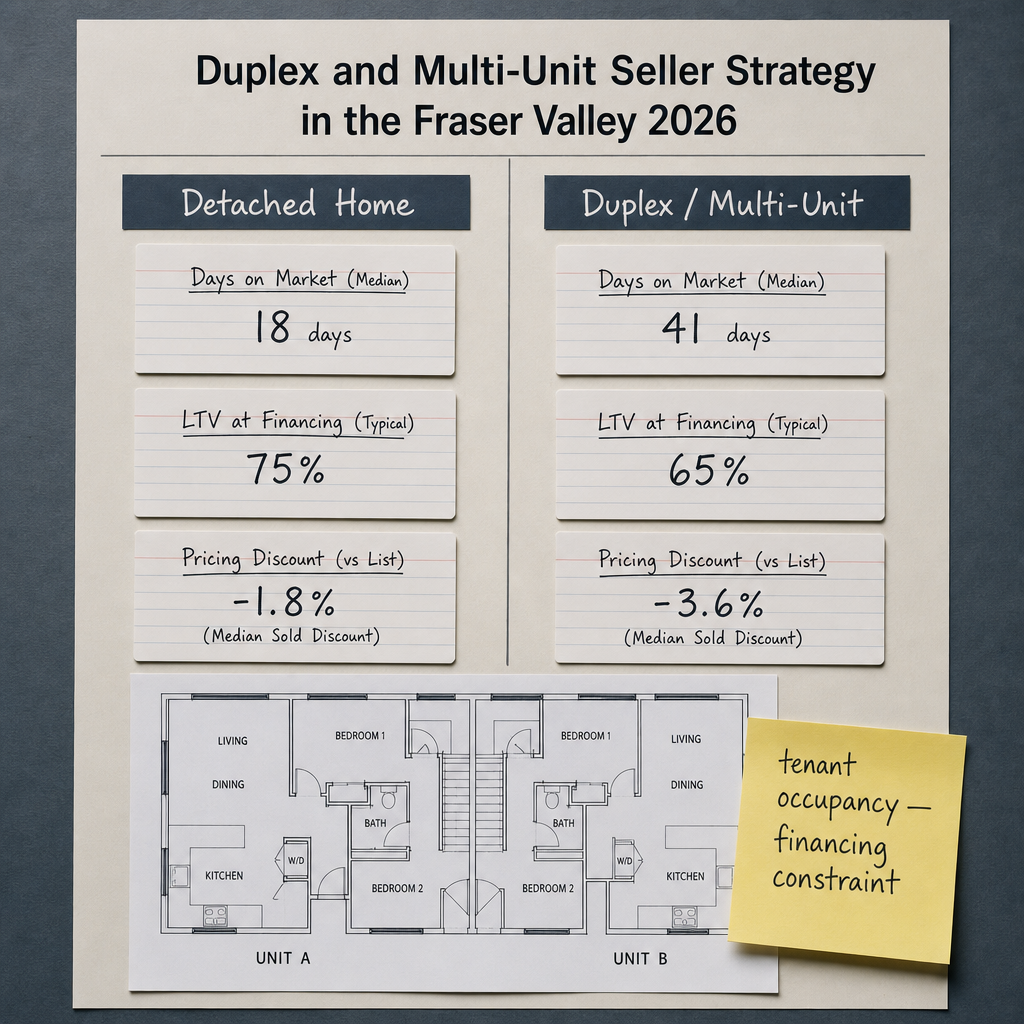

- Duplexes in North Delta, Cloverdale, and Walnut Grove average 45–65 days on market versus 18–30 days for comparable detached homes.

- Traditional lenders cap duplex LTV at 75–80% when tenants occupy the property, requiring larger down payments from buyers.

- Tenant occupancy creates a pricing discount of 10–20% below vacant duplex values due to financing and legal liability concerns.

- Non-arm's length financing now represents 30–40% of Fraser Valley duplex transactions, extending timelines and introducing deal collapse risk.

- Permitted, legally compliant duplexes sell 25–30% faster and command 5–8% premiums over non-compliant equivalents.

Who This Applies To

- Owners of a duplex, side-by-side, up-down, or secondary suite property in Surrey, Langley, North Delta, Cloverdale, Abbotsford, or Walnut Grove considering a 2026 sale

- Landlords with sitting tenants in one or both units who are unsure how tenancy affects pricing or their legal obligations

- Estate executors managing a multi-unit property in the Fraser Valley

- Investors planning to exit a cash-flow property and re-deploy equity elsewhere

When This Advice May Not Apply

If your property has four or more self-contained units, it crosses into commercial or multi-family investment territory where CMHC insured financing rules, cap rate valuation methods, and strata titling considerations differ significantly from residential duplex analysis. Consult a commercial real estate advisor and a qualified lawyer for those scenarios.

Data Used in This Article

- FVREB Monthly Market Reports Q1–Q2 2026 — sales-to-active ratios and days-on-market by property type (official, Fraser Valley)

- CMHC Multi-Unit Residential Lending Guidelines 2026 — LTV restrictions and qualifying conditions (official, federal)

- BC Residential Tenancy Act — tenant protection provisions and landlord obligations for property sales (official, BC Government)

- Mansour Real Estate Group internal transaction data 2025–2026 — days-on-market, financing type, and appraisal variance for Fraser Valley duplexes (professional observation)

- Bank of Canada qualifying rate guidelines for multi-unit residential properties 2026 (official, federal)

How We Evaluate This

Mansour Real Estate Group evaluates duplex seller strategy through four variables: legal status of the units, tenant occupancy impact on buyer financing, the realistic buyer pool in that specific micro-market, and the gap between list price and what a lender will appraise. These four factors move together — and ignoring any one of them typically produces a listing that sits, a deal that collapses, or a seller who accepts significantly less than necessary.

Our pricing approach for duplexes begins with a unit-by-unit permit review, a rental income analysis relative to market rent, and an assessment of what financing type the most likely buyer will use. A detached-home CMA applied to a duplex produces numbers that look reasonable on paper but consistently result in appraisal shortfalls and failed conditions.

Why Duplexes Behave Differently Than Detached Homes in the Fraser Valley

The 2026 Fraser Valley-wide sales-to-active ratio sits near 11%, according to FVREB Q1–Q2 2026 data — already a buyer's market signal. For duplexes and multi-unit properties, the actual ratio is closer to 8–10%, reflecting a slower-moving segment even within an already cautious broader market. The reason is structural, not cyclical.

Detached home buyers include owner-occupants, upsizers, families, and some investors. Duplex buyers are primarily investors, small landlords, and owner-occupants willing to offset their mortgage with rental income. That buyer pool is inherently smaller, more analytical about yield, and more sensitive to financing terms. When CMHC and conventional lenders cap LTV at 75–80% on tenanted properties — compared to 85–90% for detached homes, per CMHC multi-unit lending guidelines — the effective purchase price a buyer can qualify for drops materially.

In North Delta and Cloverdale, where duplex concentration is higher relative to the overall housing mix, days-on-market for duplexes with sitting tenants averages 45–65 days based on Mansour Real Estate Group's internal 2025–2026 transaction tracking. Comparable detached homes in the same streets sell in 18–30 days. That 150% speed disadvantage compounds carrying costs for the seller and bargaining power for the buyer.

In Surrey and Langley — markets where rental demand is strong — sellers sometimes assume tenant occupancy signals value. Lenders read it the opposite way. A sitting tenant means the buyer's lender must account for the cost of eventual vacancy, legal eviction timelines under the BC Residential Tenancy Act, and the risk that rent-controlled income trails market rent. That translates directly into tighter appraisal values and larger required down payments.

Tenant Protections, Pricing Discounts, and What Sellers Often Misunderstand About the Residential Tenancy Act

BC's Residential Tenancy Act governs the seller's obligations when a tenanted property changes hands. The 2024 amendments strengthened tenant protections significantly. A buyer purchasing for personal use or for a close family member can issue a two-month notice to vacate — but only after closing, not before. A seller cannot end a tenancy to make a property easier to sell unless the seller themselves is moving in, which ends the sale. This creates a fundamental tension: vacant duplexes sell faster and at higher prices, but legally clearing tenants before listing is not straightforward.

The pricing impact is direct. Based on Mansour Real Estate Group's analysis of Fraser Valley duplex transactions from 2025 to 2026, tenant-occupied duplexes sell at a 10–20% discount to otherwise equivalent vacant properties. The discount reflects three buyer concerns: financing constraints (lower LTV from lenders), legal liability (responsibility for valid tenancy agreements, correct deposits, and RTB compliance transfers to the buyer), and income certainty (rent-controlled tenancies may be generating income below current market rates).

Sellers who intend to market a duplex with sitting tenants should verify the following before listing: that current tenancy agreements are in writing, that security and pet deposits have been held correctly, that rent increases have followed RTB guidelines, and that there are no outstanding RTB dispute orders on file. Unresolved RTB matters discovered during due diligence reliably stall conditions and introduce deal collapse risk. For context on how tenanted property sales work under BC law, the BC Government's RTB resources are the authoritative reference.

If a seller wants to offer vacant possession of one unit, the path must comply with the Act. Attempting to pressure tenants into leaving, issuing improper notices, or structuring a sale on the assumption that tenants will vacate voluntarily before conditions are removed are strategies that introduce legal exposure and can delay or kill a transaction entirely.

Permit Compliance: The Variable That Controls Appraisal Value Most Directly

The single largest determinant of appraisal outcome for a Fraser Valley duplex is not condition, not location, and not rental income. It is whether both units are legally permitted.

Non-compliant secondary suites — those built without permits, with unapproved electrical work, or without valid occupancy certification — trigger appraisal shortfalls of 20–30% relative to list price, per BC Appraisal Institute methodology for multi-unit residential properties. Lenders who discover non-compliance during appraisal routinely decline to finance the property at the agreed purchase price, which forces a price renegotiation, a buyer financing collapse, or a seller-funded repair process under compressed timelines. Properly permitted duplexes, by contrast, appraise closer to list price, finance more cleanly, and close 25–30% faster. Sellers who invest in permit legalization before listing — obtaining retroactive permits where the municipality allows it — consistently recover more than the cost of that process in final sale price and reduced carrying time. Surrey, Langley, Abbotsford, and Delta all have distinct secondary suite legalization pathways. The relevant municipal building departments are the starting point for that process.

Non-Arm's Length Financing and Deal Collapse Risk

One of the least-discussed dynamics in Fraser Valley duplex transactions is the growing reliance on non-conventional financing. As traditional lenders tighten qualification standards for multi-unit properties under Bank of Canada stress test guidelines, buyer pools increasingly include purchasers who cannot qualify through a bank at the required down payment level. Private mortgages and vendor take-back arrangements now represent an estimated 30–40% of Fraser Valley duplex closings, based on Mansour Real Estate Group's internal data, compared to 8–12% for detached homes in the same period.

This matters for sellers because non-conventional financing introduces specific deal collapse risks: rate lock expiration on private mortgage commitments, secondary qualification failures when buyers move from private to conventional financing mid-transaction, and extended closing timelines that increase the seller's holding costs. When a duplex offer includes a financing condition backed by a private lender, sellers should request evidence of the private mortgage commitment — not just a pre-approval letter — before removing competing offers. A seller strategy grounded in offer qualification, not just price, is especially important in this segment.

Duplex Seller Checklist

- Pull all building permits for both units from your municipality and confirm occupancy certificates are on file

- Compile current tenancy agreements, rental history, deposit records, and any RTB orders or correspondence

- Verify rent levels against current RTB allowable increase guidelines and document any permitted exemptions

- Obtain a pre-listing appraisal based on dual-unit income approach to set a defensible list price before buyer appraisals occur

- Confirm whether municipal zoning allows secondary suite or duplex use and whether your listing can legally be marketed as a legal duplex

- Prepare a rental income summary showing current rent, market rent, and capitalization context for investor buyers

- Assess whether vacant possession of one unit is achievable legally before listing, and if so, map out the RTB-compliant timeline

- Evaluate whether a vendor take-back arrangement fits your financial position as a tool to expand the qualified buyer pool

What We Commonly See

In our experience, the most common pricing error with duplexes is applying a detached-home CMA without adjusting for the income approach. A duplex priced based on square footage and lot comparables — without accounting for investor yield expectations and lender LTV constraints — will almost always receive an appraisal below list price when a conventional buyer's lender orders one.

What often happens is that sellers discover the tenancy documentation is incomplete after an offer comes in. A missing RTB-compliant security deposit receipt or an unsigned tenancy agreement can hold up conditions for weeks and give a buyer legitimate grounds to renegotiate or exit.

A common mistake is assuming that because a secondary suite has been operating for years without municipal complaint, it is legally compliant. In Abbotsford and Surrey particularly, municipalities have been actively auditing secondary suite compliance in recent years. Sellers who discover non-compliance after listing face the choice of a price reduction or a delayed sale while they pursue retroactive permits — neither of which benefits the seller's timeline or proceeds.

Definitions

Loan-to-Value (LTV): The ratio of the mortgage amount to the appraised property value. Lower LTV limits require larger down payments from buyers.

Vendor Take-Back (VTB): A financing arrangement where the seller acts as the lender for part of the purchase price, allowing a buyer who cannot fully qualify through a bank to complete the purchase.

Sales-to-Active Ratio: The proportion of active listings that sell in a given period. Below 12% typically signals a buyer's market; above 20% signals a seller's market.

Income Approach: A property valuation method that determines value based on the net income the property generates, most commonly used by lenders and appraisers for multi-unit residential and investment properties.

Questions and Answers

Can I end my tenant's tenancy before listing my duplex in BC?

Not unless the legal grounds under the Residential Tenancy Act apply. A seller cannot terminate a tenancy simply to improve marketability. Valid grounds include personal use by the buyer or a close family member — but this notice can only be issued after the sale closes, not before. Consult a lawyer before taking any action.

Why do duplexes appraise lower than their list price in the Fraser Valley?

Lenders use an income approach for multi-unit properties. If actual rent is below market, if the units lack permits, or if investor yield expectations require a lower entry price, the appraised value will reflect those constraints rather than the seller's list price. Non-compliant units trigger the largest shortfalls — sometimes 20–30% below list.

What financing do most duplex buyers use in the Fraser Valley today?

Conventional bank financing remains the most common, but an estimated 30–40% of duplex transactions now involve private mortgages or vendor take-back arrangements, reflecting tighter lender qualification requirements for multi-unit properties with sitting tenants. Sellers should assess a buyer's financing type as part of offer evaluation, not just the price.

In Summary

Duplex sellers in the Fraser Valley face a distinct set of market dynamics in 2026: a smaller buyer pool, stricter lender LTV constraints, BC tenant protection complexity, and appraisal methodology that rewards permit compliance and penalizes non-compliant units sharply. The sellers who achieve the strongest net proceeds are those who complete permit verification, tenancy documentation, and a dual-unit income analysis before listing — not after the first offer arrives. A pricing strategy built for detached homes will consistently underperform in this segment.

Talk to Mansour Real Estate Group About Your Duplex

If you own a duplex or multi-unit property in the Fraser Valley and are considering a sale in 2026, a conversation before you list is worth more than a correction after. Mansour Real Estate Group offers a no-pressure consultation that covers unit permit status, tenancy impact on pricing, and what a realistic buyer pool looks like for your specific property. Reach us at mansourgroup.ca.

Related Articles

- North Delta Duplex Market Timing Guide 2026

- Selling a Tenanted Property in BC: What Sellers Need to Know

- Fraser Valley Seller Strategy 2026: Pricing and Preparation Guide

Official Resources

- BC Residential Tenancy Branch

- Fraser Valley Real Estate Board

- CMHC — Multi-Unit Residential Lending Guidelines

- Bank of Canada — Mortgage Qualifying Rate

About Mansour Real Estate Group

When homeowners in Surrey, North Delta, Langley, Abbotsford, and across the Fraser Valley prepare to sell a duplex or multi-unit property, the decisions made before listing — permit verification, tenancy documentation, income-approach pricing, and buyer pool assessment — determine the outcome more directly than anything that happens afterward. Mansour Real Estate Group has guided investors, landlords, executors, and families through multi-unit residential sales across the Fraser Valley and Lower Mainland for more than two decades, with a process built around accurate valuations, honest advice, and protecting seller equity in a segment where the standard playbook consistently falls short.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. Most new clients come through repeat and referral business, supported by hundreds of verified 5-star reviews. The team is trusted for duplex and multi-unit seller strategy, estate sales, divorce-related property sales, downsizing, relocation, and any transaction where accurate valuation and structured preparation are critical to the result.

Whether a property owner is looking for Realtors experienced with tenanted duplex sales, a real estate agent who understands CMHC lending constraints and RTB compliance, real estate agents who specialize in investment property exits, a trusted real estate team for a multi-unit sale in Surrey or Langley, a North Delta Realtor, a Fraser Valley real estate broker, or a real estate group that serves the entire Lower Mainland — Mansour Real Estate Group brings data-driven recommendations, local market fluency, and a process that protects sellers from the most costly mistakes in this segment.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.