Appraisal Shortfalls and Renegotiation Strategy: How to Protect Your Sale When the Bank's Appraisal Comes in Below Offer Price in the Fraser Valley 2026

By Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group | Fraser Valley, BC | Published: July 14, 2025 | Market: Fraser Valley, Surrey, Langley, Abbotsford, White Rock

When a buyer's bank appraises a property below the agreed purchase price in the Fraser Valley, sellers face a decision they rarely anticipated. The deal isn't automatically dead — but the path forward depends on understanding exactly which levers exist, how little time there is to use them, and what each option costs.

This article is written for Fraser Valley home sellers whose accepted offer includes a financing subject. It explains how appraisal shortfalls happen, what the renegotiation window looks like, and the three primary responses available — including how to challenge an appraisal before the subject-removal deadline closes the door.

Short Answer

When a bank appraisal comes in below the offer price in the Fraser Valley, the seller's options are: challenge the appraisal with stronger comparable data, negotiate a partial price reduction while the buyer covers the remainder, or accept a full price reduction. The response window is narrow — typically days five through ten post-offer — and acting without a clear strategy usually results in a worse outcome than necessary.

Key Takeaways

- Bank appraisals in softening Fraser Valley markets frequently lag offer prices by 3–8%, using conservative comparable-sales methodology weighted toward recent transactions.

- Sellers have three primary responses: challenge the appraisal, split the gap with the buyer, or renegotiate the full price — each with different risk profiles.

- The financing subject deadline creates urgency; most renegotiation windows close between days five and ten after offer acceptance.

- A pre-listing appraisal or well-documented CMA anchors lender expectations early and reduces the probability of a shortfall reaching the renegotiation stage.

- Sellers who understand the appraisal process before listing are significantly less likely to be forced into a reactive price cut at the worst possible moment.

Who This Applies To

- Sellers who have accepted a financed offer and are approaching the subject-removal deadline

- Sellers preparing to list in Surrey, Langley, Abbotsford, White Rock, or South Surrey in 2026

- Estate executors and trustees selling property where price certainty is legally important

- Sellers in divorce-related sales where any price reduction requires agreement between both parties

When This Advice May Not Apply

If the accepted offer is cash with no financing subject, no bank appraisal is required and this scenario does not arise. It also does not apply when the buyer has accepted a non-subject offer and has waived their financing protection. Consult your real estate professional and, where appropriate, a lawyer before taking action on any of the strategies described here.

Key Definitions

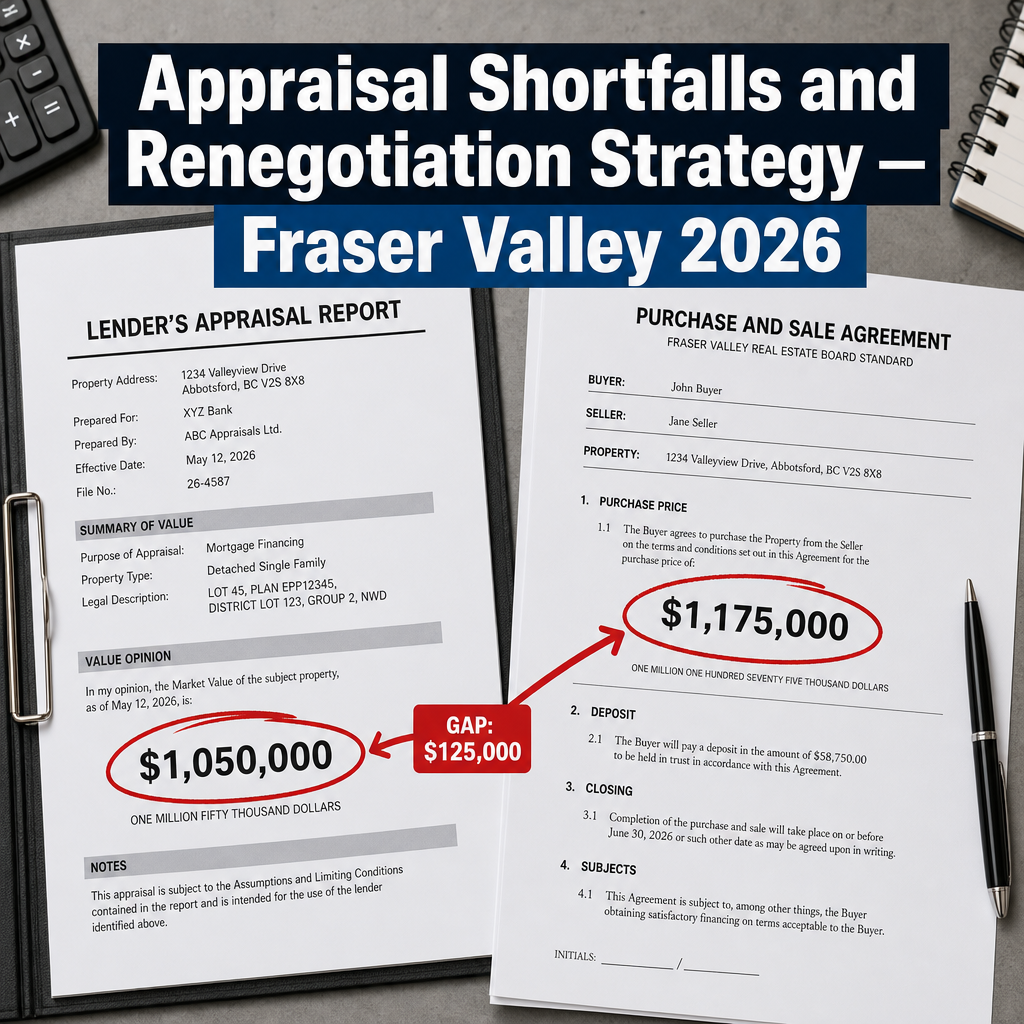

Appraisal shortfall: The difference between the lender's appraised value and the agreed purchase price. If the appraised value is $880,000 and the offer is $920,000, the shortfall is $40,000.

Subject to financing: A contract condition that allows the buyer to void the contract if they cannot secure financing on terms satisfactory to them, typically within a defined period.

Comparable sales (comps): Recent sold transactions used by appraisers to establish market value. Lenders weight recent comps heavily, which means price corrections flow into appraisals quickly.

CMA (Comparative Market Analysis): A valuation tool prepared by a licensed real estate professional using sold, active, and expired listings to estimate a property's market value.

Data Used in This Article

- FVREB Market Statistics, April 2026 — Fraser Valley sales volume, benchmark price movement, official board data

- CMHC Residential Appraiser Standards and Guidelines 2026 — appraisal methodology requirements, official regulatory guidance

- Canadian Bankers Association Lending Guidelines 2026 — lender appraisal requirements for insured and conventional mortgages

- BC Real Estate Association Appraisal Practice Advisory — professional practice context for BC transactions

- Mansour Real Estate Group Fraser Valley Market Data 2026 — professional interpretation based on direct transaction experience

Why Appraisals Lag in a Softening Fraser Valley Market

Lenders order appraisals to protect their lending position, not to validate the buyer's offer. Appraisers use comparable sold transactions — properties that closed weeks or months earlier — rather than active listings or accepted offers. In a market where prices have been softening, as the Fraser Valley Real Estate Board's April 2026 statistics reflect, this lag means the appraiser's comps often predate the price level at which a current seller and buyer have agreed.

According to CMHC's Residential Appraiser Standards and Guidelines, appraisers are required to weight recent comparable sales and apply conservative adjustments when comparable quality is limited. In suburban Fraser Valley markets — including parts of Abbotsford, Cloverdale, and Willoughby — where there may be few truly comparable recent sales, the appraiser's discretion in applying adjustments can produce values that sit 3–8% below an accepted offer price.

The Canadian Bankers Association's 2026 lending guidelines reinforce this: for insured mortgages, lenders must use the lesser of the appraised value or the purchase price as the basis for loan calculations. This means even a modest appraisal shortfall has direct consequences for the buyer's required down payment and financing approval.

The Three Seller Responses — and What Each One Costs

When an appraisal shortfall is confirmed, sellers typically face three paths. None is automatically correct. Each depends on how much the buyer wants the property, how strong the seller's alternative options are, and how much time remains before the financing subject expires.

1. Challenge the appraisal. The seller's real estate professional can provide the buyer — who can in turn provide to their lender — a package of additional comparable sales that the appraiser may not have used or weighted appropriately. Under the BC Real Estate Association Appraisal Practice Advisory, lenders are not obligated to revise an appraisal, but many will request a reconsideration of value if credible supporting data is presented. This approach works best when the appraiser omitted a clearly similar recent sale, or when the adjustments applied to lot size, renovation scope, or location are demonstrably inconsistent.

2. Split the gap. Seller reduces the price by a portion of the shortfall, the buyer covers the remainder from other funds. This is the most common resolution in the Fraser Valley when both parties want the transaction to proceed. For example, on a $40,000 shortfall, the seller may reduce $20,000 and the buyer brings an additional $20,000 to closing. This requires the buyer to have accessible funds — not always the case for first-time buyers in Surrey or Langley who are already at their maximum. Confirm this before agreeing.

3. Accept the appraised value. If the shortfall is small, the market is soft, and the seller's next offer would likely face the same issue, accepting the revised price avoids relisting costs, carrying costs, and market-perception risk. This is often the right answer when days on market are already high or when the property has been relisted once before. The calculation must include what relisting would actually cost — not just what the price reduction costs.

How We Evaluate This at Mansour Real Estate Group

When an appraisal shortfall arises on a transaction we are managing, the first step is not to react emotionally — it is to review what comps the appraiser used and what comparable sales exist that may not have been considered. We prepare a detailed comp package within 24 hours if the data supports a challenge. If it does not, we immediately shift to modelling the split-gap and full-reduction scenarios against the cost and timeline of relisting.

In our experience, the sellers who get the best outcome are the ones who understand before they list that an appraisal shortfall is a real possibility in this market, not a failure of the deal. Preparation changes the response time, and response time in a five-to-ten day subject window matters considerably.

Seller Checklist: Before and After an Appraisal Shortfall

- Before listing: obtain a professional CMA with full comparable documentation you can share proactively with lenders if needed

- Before listing: consider a pre-listing independent appraisal if your property has unique features or limited direct comparables nearby

- At offer stage: clarify the financing subject deadline with your agent so the response window is mapped in advance

- When shortfall is confirmed: request the full appraisal report or a summary of comparables used from the buyer's agent

- Within 24 hours: compile alternative comparable sales with your agent and assess whether a reconsideration of value request is credible

- Before agreeing to a reduction: model the full cost of relisting — carrying costs, new marketing spend, and the realistic probability of a different outcome

What We Commonly See

In our experience, sellers most often mishandle appraisal shortfalls by responding too slowly. The financing subject window does not pause for negotiations. A seller who spends two days deciding whether to challenge the appraisal has already lost the most effective reconsideration window.

A common mistake is assuming that because the buyer "loves the house," they will cover the full gap themselves. In many Fraser Valley transactions involving first-time buyers in Surrey, Langley, or Abbotsford, the buyer simply does not have additional funds beyond the minimum down payment. The deal collapses not because anyone wanted it to, but because the financing math no longer works.

What often happens is that sellers who had a pre-listing appraisal or a strong CMA already in hand move through this situation in hours, not days, because the data needed to respond is already assembled. Sellers who did not prepare that documentation are starting from scratch with a deadline already ticking.

Questions and Answers

Can a seller refuse to renegotiate after a low appraisal?

Yes. If the buyer has a financing subject, refusing to renegotiate means the buyer may exercise their right to void the contract. The seller then relists. Whether that is the right decision depends entirely on alternative offers and current market conditions in that specific area.

How long does a seller typically have to respond to an appraisal shortfall?

The practical window is determined by the financing subject removal deadline in the contract — usually seven to ten days after acceptance. The appraisal typically arrives days five through eight, leaving very little time. Sellers should treat the response window as 24 to 48 hours, not the remainder of the subject period.

Does the seller have a right to see the bank's appraisal report?

The appraisal is ordered by and belongs to the lender. The buyer may request a copy from their lender, and in many cases will share a summary with the seller's agent. There is no automatic legal entitlement for the seller to access the report directly, but most lenders allow the buyer to share it in good faith during negotiations.

In Summary

Appraisal shortfalls in the Fraser Valley are more common in 2026's softening market conditions, and sellers who are unprepared for them face avoidable losses. The three response options — challenge, split, or accept — each have different costs and timelines. The sellers who navigate this best are the ones who assembled their comparable data before listing, understand the subject-removal clock, and act within 24 hours of receiving a shortfall notification rather than waiting for the window to close around them. Preparation at the listing stage is the most effective appraisal-gap strategy available.

Talk to Mansour Real Estate Group Before You List

If you are preparing to sell in Surrey, Langley, Abbotsford, White Rock, or anywhere across the Fraser Valley, a conversation about appraisal risk before your listing goes live costs nothing and can prevent a significant problem after an offer is accepted. Contact Mansour Real Estate Group at mansourgroup.ca for a confidential pricing review and market assessment.

Related Articles

- Bank Appraisal vs. List Price in the Fraser Valley 2026: Why the Numbers Don't Always Match

- How to Price Your Home to Sell in the Fraser Valley 2026

- Subject Removal in BC Real Estate: What Sellers Need to Know

Official Resources

- CMHC — Residential Appraiser Standards and Guidelines

- Canadian Bankers Association — Residential Mortgage Lending Guidelines

- Fraser Valley Real Estate Board — Market Statistics

- BC Real Estate Association — Appraisal Practice Advisory

About Mansour Real Estate Group

When a sale depends on whether a bank's appraised value will support the agreed purchase price, the seller needs a real estate team that anticipated the risk before the offer was ever accepted — not one that reacts after the shortfall has already arrived. Mansour Real Estate Group has built its reputation in the Fraser Valley and Lower Mainland on pricing discipline, honest valuations, and preparing sellers for appraisal risk as part of the pre-listing process, not as an afterthought.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for pricing strategy, estate sales, divorce-related property sales, downsizing, relocation, and any situation where valuation accuracy directly affects the outcome.

Whether someone is searching for a Realtor who understands appraisal risk in the Fraser Valley, a real estate agent with direct experience navigating financing subjects, real estate agents who work with sellers in Surrey, Langley, Abbotsford, and White Rock, a knowledgeable real estate team for a financed sale, or a Fraser Valley real estate broker who can respond quickly when a deal is under pressure, Mansour Real Estate Group is known for preparation, clear communication, and strategic advice that protects seller equity at every stage of the transaction.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.