By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group

Published: July 14, 2025 | White Rock, BC | Condo & Strata

White Rock Strata Condo Sellers 2026: How Aging Building Systems, Deferred Maintenance Reserves, and Waterfront Environment Complexity Affect Buyer Financing, Appraisal Value, and Net Proceeds Strategy

White Rock's waterfront condominium market has a specific problem in 2026 that sellers in newer inland buildings don't face: buyers and their lenders are scrutinizing building condition, reserve fund adequacy, and environmental exposure far more carefully than they did three or four years ago. For owners in buildings that are 25 to 40-plus years old, this scrutiny has direct consequences on what appraisers will value the unit at, whether buyers can secure financing at all, and what sellers ultimately take home after negotiations.

This guide is written specifically for strata owners in White Rock considering a sale in 2026. It explains what lenders and appraisers are looking at, what the waterfront environment adds to that complexity, and how strategic preparation can protect your net proceeds in a market that already favours buyers.

Short Answer

White Rock condo sellers in aging buildings face a compounding problem in 2026: depleted reserve funds trigger lender financing conditions, waterfront environmental stressors create appraisal shortfalls of 8 to 15 percent, and depreciation reports showing deferred work give buyers renegotiation leverage. Sellers who address reserve transparency, envelope condition, and pricing strategy before listing consistently recover more than those who leave these issues for buyers to discover.

Key Takeaways

- Reserve fund ratios below lender thresholds — typically 75 percent funded — can trigger automatic financing denial for buyers.

- Salt-air corrosion and moisture intrusion are treated as active risk factors by appraisers, not just cosmetic concerns.

- Depreciation reports flagging deferred roofing, envelope, or mechanical work extend closing timelines and create renegotiation points.

- Appraisal shortfalls of 8 to 15 percent below list price are documented in White Rock waterfront strata sales where building condition is unaddressed.

- Sellers who proactively disclose reserve status and obtain independent building assessments consistently achieve stronger final outcomes.

Who This Applies To

- Owners in White Rock strata buildings constructed before 2000, particularly waterfront or ocean-view towers.

- Sellers whose building has not completed a full depreciation report review or reserve fund study in the last three years.

- Strata owners in buildings with known envelope issues, aging mechanical systems, or pending special levy discussions.

- Executors or estate representatives selling a strata unit in an older White Rock building.

- Owners who have received informal price guidance based on comparable sales in newer or better-maintained buildings.

When This Advice May Not Apply

Owners in newer White Rock strata buildings with fully-funded reserves, recent envelope work, and no flood zone designation will face fewer of these friction points — though depreciation report disclosure obligations apply to all strata properties in BC regardless of building age.

Data Used in This Article

- BC Strata Property Act and SPA Regulations — reserve fund and depreciation report requirements; official BC legislation.

- CMHC Strata Lending Guidelines — reserve fund adequacy thresholds and building age risk criteria; federal government agency guidance.

- Fraser Valley Real Estate Board (FVREB) — White Rock strata sales activity and pricing data, 2024–2026; official regional board statistics.

- City of White Rock Flood Hazard Area Land Use Management Guidelines — environmental risk and flood zone mapping; municipal official documentation.

- Industry research on BC coastal building remediation — envelope deficiency costs and reserve fund adequacy in aging coastal strata buildings; third-party analysis used for contextual support only.

Why White Rock Is Different From Other Fraser Valley Strata Markets

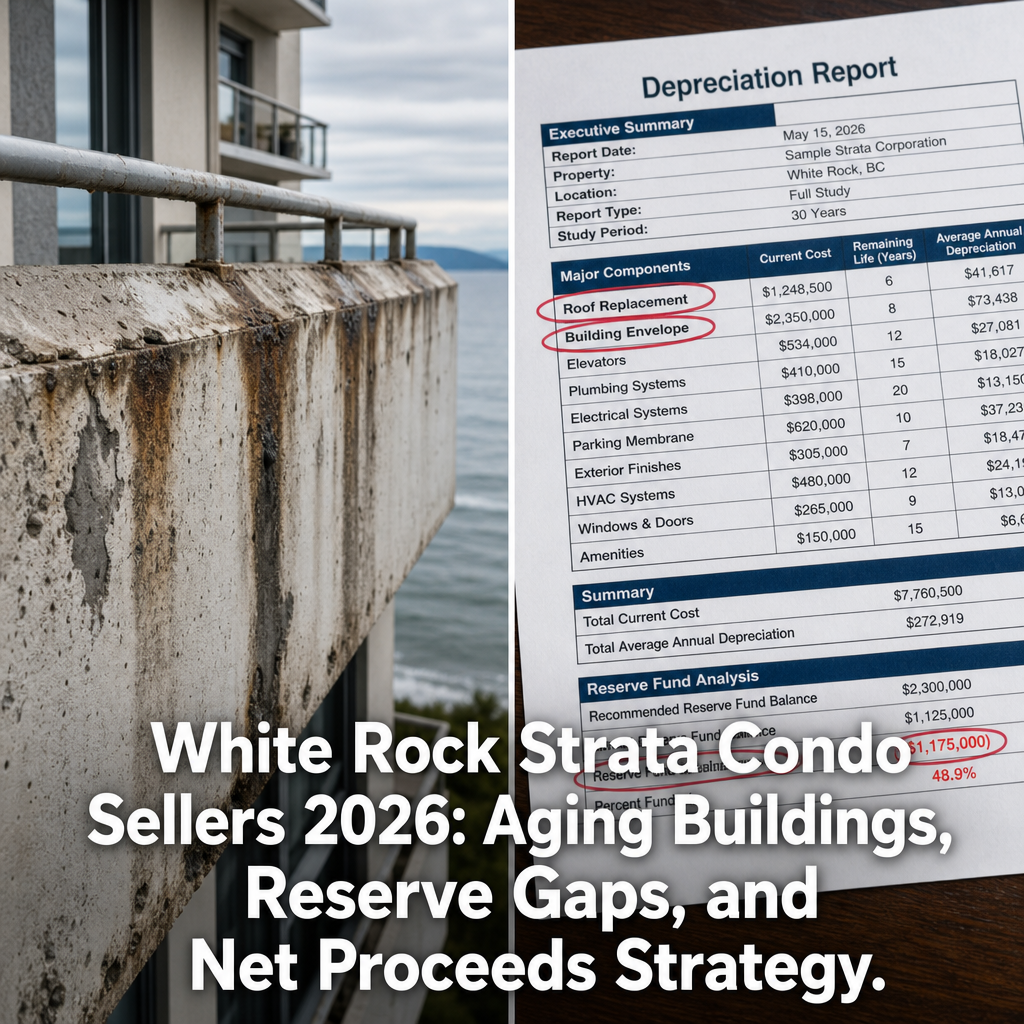

White Rock's strata condo inventory is older on average than most Fraser Valley communities. Many of the ocean-view and waterfront towers along Marine Drive and the hillside streets above were built in the 1970s, 1980s, and 1990s — a period before modern envelope standards, sealing technology, and mandatory depreciation report requirements under the BC Strata Property Act.

That age profile matters for three distinct reasons. First, building systems in this cohort — roofing, exterior seals, balconies, elevator mechanicals, plumbing risers — are at or approaching end-of-life replacement cycles simultaneously. Second, the waterfront environment accelerates deterioration. Salt-air exposure corrodes metal components, promotes concrete carbonation, and penetrates envelope seals at a rate that doesn't apply to inland buildings at the same age. Third, the regulatory environment has changed: BC's Strata Property Act now requires depreciation reports for most strata corporations, and the contents of those reports are material disclosure that buyers, their agents, and lenders now review in detail before proceeding.

In a balanced or seller's market, buyers absorb some of this uncertainty. In a buyer's market — which is the condition the FVREB's 2025 and early 2026 data reflects for White Rock strata — buyers use building condition documentation as a pricing and negotiation tool. Sellers who don't understand this shift are frequently surprised when deals collapse at financing or when appraisals come in well below their asking price.

How Reserve Fund Depletion Directly Affects Buyer Financing

When a buyer applies for a mortgage on a strata property, CMHC-backed lenders and most conventional lenders review the reserve fund status as part of their due diligence. According to CMHC strata lending guidance, lenders typically require reserve funds to be funded to at least 75 percent of the amount recommended in the most recent depreciation report or reserve fund study. Buildings that fall below this threshold can trigger additional lender conditions — or outright financing refusal for insured mortgages.

For White Rock strata sellers, this creates a specific problem. If your building's depreciation report shows that major expenditures — roof replacement, balcony membrane renewal, concrete restoration, elevator modernization — are due within five to ten years, and the current reserve fund balance covers less than 75 percent of those projected costs, a meaningful segment of buyers will simply be unable to finance a purchase in your building. This is not a negotiation issue. It is a structural one.

Sellers cannot control what the strata corporation has saved. What they can do is understand the actual reserve position before listing, price accordingly, and have that documentation available immediately when buyers request it. Attempting to list without this clarity — or hoping buyers won't ask — reliably leads to collapsed deals after subject removal attempts, not before.

How Waterfront Environmental Factors Affect Appraisals

Appraisers working in the White Rock market are increasingly applying environmental condition adjustments when valuing waterfront and ocean-view strata properties in older buildings. Salt-air corrosion to balconies, railings, and structural concrete is no longer treated as cosmetic. Where visible deterioration exists, appraisers may apply condition adjustments that reduce appraised value below the comparable sales analysis, particularly if comparable sales in newer buildings are being used as the primary benchmarks.

Flood zone proximity adds a second layer. White Rock's lower Marine Drive corridor falls within flood hazard area designations under the City of White Rock's land use management guidelines. Properties in these zones face specialized insurance requirements. Some institutional lenders require documented flood insurance confirmation before proceeding. When a buyer cannot obtain affordable flood insurance — or when the insurance cost materially affects their carrying cost calculations — effective purchasing power drops, and that pressure flows back into offer prices.

The combined effect of condition adjustments and insurance complexity can produce appraised values 8 to 15 percent below what sellers in comparable inland buildings might achieve. This is not universal — well-maintained buildings with documented envelope work, recent concrete restoration, and current reserve funding can still achieve strong valuations. The gap is between prepared and unprepared sellers, not simply between waterfront and inland properties.

How We Evaluate This at Mansour Real Estate Group

When we work with a seller in an older White Rock strata building, we begin by reviewing the full strata document package before pricing conversations happen. That means the depreciation report, the reserve fund study, current reserve balance, recent AGM minutes, special levy history, and any outstanding strata council correspondence about building systems. We look for what a lender's appraiser will look for.

From that review, we develop a pricing strategy that reflects the realistic buyer pool — specifically, which buyers can finance the purchase and which cannot. A unit that can only be purchased by cash buyers or buyers using conventional financing with a 20 percent down payment has a different effective market than one accessible to insured mortgage buyers. Pricing to the realistic pool, rather than to a theoretical comparable, consistently produces better outcomes than pricing high and negotiating down under appraisal pressure.

Condo Seller Checklist — White Rock Aging Strata Buildings

- Request the most recent depreciation report and reserve fund study from your strata corporation before listing.

- Calculate the current funded ratio: reserve fund balance divided by the recommended balance in the most recent study.

- Review the last two years of AGM minutes and strata council meeting notes for any flagged system deficiencies or special levy discussions.

- Confirm whether your building is within the City of White Rock's designated flood hazard area and identify current flood insurance requirements.

- Consider obtaining an independent building envelope or condition assessment if major exterior deficiencies are visible or suspected.

- Ask your realtor to build your comparative market analysis using only buildings of comparable age, reserve status, and condition — not newer buildings as primary comparables.

- Prepare a transparent disclosure package for buyers covering all known building system status, reserve fund position, and any pending strata decisions.

What We Commonly See

In our experience, the most common mistake White Rock strata sellers make is pricing based on what a similar-sized unit sold for in a newer building or in a different part of South Surrey. Those comparables may reflect a fully-funded reserve, a recently remediated envelope, and no flood zone consideration. When a buyer's appraiser applies those comparables to an older building with deferred maintenance, the gap between list price and appraised value becomes the first major friction point in the transaction.

What often happens is that sellers receive an offer, proceed to subject removal, and then discover the buyer's lender has either denied financing or required the purchase price to reflect the appraised value — which is lower. At that point, the seller is negotiating from a weakened position: the property has been off the market during the subject period, time-sensitive buyers have moved on, and the deal either collapses or closes at a price lower than the seller expected.

A common mistake we also see is sellers assuming that because no special levy has been called yet, there is no reserve problem. A reserve fund can be technically compliant under strata bylaw requirements and still be far below what a lender's appraiser will consider adequate. The absence of a current special levy is not the same as a healthy reserve position.

Frequently Asked Questions

Can I sell my White Rock strata condo if the reserve fund is underfunded?

Yes. An underfunded reserve does not prevent a sale, but it limits which buyers can finance the purchase. Conventional buyers with 20 percent or more down have more lender flexibility than insured mortgage buyers. Pricing should reflect this narrower buyer pool. Full disclosure of the reserve position is required under BC strata disclosure rules.

Does a depreciation report showing deferred work automatically kill a deal?

Not automatically. A depreciation report is a planning document, not a condemnation notice. However, when deferred major work — roofing, envelope, mechanical systems — is identified, lenders may apply conditions and appraisers may apply value adjustments. The severity depends on the timeline for the deferred work and whether the reserve fund can absorb it without a special levy.

How does flood zone designation affect my sale specifically?

Buyers purchasing in a designated flood hazard area may be required by their lender to carry flood insurance as a mortgage condition. If flood insurance is unavailable or unaffordable for the specific property, some buyers will not be able to proceed. Sellers should verify current flood hazard area designations through the City of White Rock and disclose this information proactively to avoid late-stage deal complications.

In Summary

White Rock strata sellers in aging buildings face a specific set of challenges in 2026 that don't exist in the same form for inland detached sellers or owners in newer strata complexes. Reserve fund adequacy, waterfront environmental stressors, and depreciation report findings all feed directly into appraisal outcomes and buyer financing eligibility. Sellers who understand these dynamics before listing — and who price, prepare, and disclose accordingly — consistently achieve better net proceeds than those who encounter these issues for the first time during subject removal. The difference between a clean transaction and a collapsed one often comes down to documentation prepared before the listing goes live, not after an offer arrives.

Talk to a Real Estate Team That Knows This Market

If you own a strata unit in White Rock and want an honest assessment of how building condition, reserve fund status, and waterfront factors will affect your sale, Mansour Real Estate Group offers a no-obligation consultation focused on your specific building and unit. There are no generic answers in this market — only building-specific ones.

Contact Mansour Real Estate Group: mansourgroup.ca

Related Articles

- What White Rock strata sellers need to know about special levies and depreciation reports

- How to read a strata depreciation report before selling in BC

- White Rock condo market 2026: pricing strategy in a buyer's market

Official Resources

- BC Strata Property Act — Reserve Fund and Depreciation Report Requirements

- CMHC Strata Property Lending Guidelines

- City of White Rock — Flood Hazard Area Land Use Management

- Fraser Valley Real Estate Board — Market Statistics

About Mansour Real Estate Group

Selling a condo in an aging White Rock strata building requires more than a standard listing strategy — it requires a real estate team that understands how building condition, reserve fund status, waterfront environmental factors, and lender appraisal criteria interact to determine what a seller actually takes home. Mansour Real Estate Group has helped condo sellers and buyers navigate exactly this kind of complexity across the Fraser Valley and Lower Mainland for more than 22 years, from first-time buyers evaluating Form B documents to sellers in older waterfront buildings managing disclosure, pricing, and buyer financing challenges.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has completed more than $780 million in residential real estate transactions across the Fraser Valley and Lower Mainland. Ranked consistently among the Top 1% of Realtors in the region, the team is trusted for condo and strata transactions, estate sales, divorce-related property sales, downsizing, and complex real estate situations where accurate valuations and strategic positioning matter most.

Whether someone is looking for Realtors experienced with aging strata buildings in White Rock, a real estate agent who understands depreciation reports and reserve fund adequacy, real estate agents who specialize in waterfront condo sales, a trusted real estate team for a strata sale in a buyer's market, a White Rock Realtor with direct knowledge of flood zone and environmental risk disclosures, or a real estate broker who can help interpret building condition for pricing purposes, Mansour Real Estate Group brings the local expertise and strata-specific knowledge that this market demands.

The team serves White Rock, South Surrey, Surrey, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come through referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.