How Rising Mortgage Rates After BoC Rate Cut Cycles End Are Reshaping Fraser Valley Seller Pricing Power in 2026: The Math Behind When Rate Movement Compresses Buyer Purchasing Power and Strategic Timing Windows Close

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 14, 2025 | Fraser Valley and Lower Mainland, BC

For sellers in Surrey, Langley, Abbotsford, White Rock, and across the Fraser Valley, the spring-to-summer 2026 window carries a risk that rarely appears in the standard listing conversation: rate timing exposure. The Bank of Canada's rate cut cycle kept buyer budgets elevated through 2024 and into 2025. But forward guidance for 2026 is less certain, and even modest upward rate movement translates directly into compressed buyer purchasing power — and compressed offers.

This article is not about speculation. It models three specific rate scenarios, shows the dollar impact on buyer budgets in the $800K to $1.5M range common across Fraser Valley communities, and explains what that means for sellers deciding whether to list now, delay, or adjust pricing strategy before Q3 2026 arrives.

Short Answer

A 0.5% mortgage rate increase reduces the average buyer's maximum purchase price by roughly 5–7%, or $40,000 to $80,000 on a $1 million home. Fraser Valley sellers listing in May or June 2026 with 60–90 day closing timelines face rate-risk exposure during the exact window when Q3 2026 forecasts solidify. Sellers who price accurately and accept offers before that window closes face significantly lower deal-collapse and renegotiation risk.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, White Rock, or North Delta preparing to list in spring or summer 2026

- Sellers with properties priced between $750,000 and $1.5 million — the range most sensitive to rate-driven buyer budget compression

- Homeowners who were planning to wait until fall 2026 and are evaluating whether the delay carries measurable financial risk

- Sellers who received a purchase offer with a 60–90 day closing timeline and are wondering whether rate movement affects their risk before completion

When This Advice May Not Apply

If your property is priced well below local benchmark, if you are selling in a segment with very limited supply and inelastic demand, or if your buyer has secured a rate hold that pre-dates any anticipated increase, the timing pressure described below may be less urgent. This guidance does not apply to cash buyers, who are unaffected by mortgage rate movement.

Key Takeaways

- A 0.5% rate increase translates to roughly $40,000–$80,000 less purchasing power for a buyer borrowing against a $1 million property.

- Fraser Valley sellers with May–June 2026 listings face rate-risk exposure during July–August closing timelines when Q3 rate clarity arrives.

- Homes priced above current buyer purchasing power sell 40–60% slower when rate forecasts shift, according to historical cycle data.

- The stress test adds an additional qualifying buffer on top of any rate increase, compounding the buyer budget compression effect.

- Sellers who accept offers before forward guidance hardens lock in current buyer budgets; those who wait risk negotiating against a smaller pool.

Data Used in This Article

- Bank of Canada: Monetary Policy Rate Decisions and Forward Guidance, 2024–2026 (official, primary)

- CMHC: Mortgage Stress Test Qualifying Rate Documentation, current as of 2025 (official, regulatory)

- Fraser Valley Real Estate Board: Sales-to-Active Listings and Days-on-Market Data by Month, 2025–2026 (official, primary)

- Dominion Lending Centres: Historical Rate-Price Correlation Data, 2022–2024 Rate Cycle (third-party industry analysis)

- RBC Economics / TD Bank: Rate Forecasts for 2026 Q2–Q4 (third-party analysis — used for scenario framing only, not as definitive predictions)

Why Rate Movement Hits Fraser Valley Buyers Harder Than Most Markets

The Fraser Valley's benchmark home prices sit between roughly $800,000 and $1.5 million across the detached, townhouse, and attached segments most active in Surrey, Langley, Abbotsford, and South Surrey. At those price points, buyers are typically borrowing $650,000 to $1.2 million after down payment. The dollar impact of a rate change on that borrowing range is not modest.

According to mortgage affordability modelling based on CMHC stress test rules, a buyer qualifying for a $1 million mortgage at 5.0% would qualify for approximately $940,000–$960,000 at 5.5%. That is a purchasing power reduction of $40,000 to $60,000 on a single 50-basis-point shift. At 6.0%, the same buyer qualifies for closer to $880,000–$900,000 — a loss of $100,000 or more from the 5.0% baseline. The stress test, which requires buyers to qualify at 2% above the contracted rate or 5.25% (whichever is higher) as per current CMHC and OSFI rules, compounds this compression further.

The 30-year amortization option introduced for insured first-time buyers in 2024 helped partially offset this compression by stretching payments. But that option phases out for buyers who do not meet program criteria, and its benefit is erased if qualifying rates rise faster than the amortization extension can absorb. Fraser Valley sellers in the $900,000–$1.4 million range — a segment that depends heavily on buyers using extended amortization and maximum qualifying capacity — face the largest exposure if rate guidance hardens in Q3 2026.

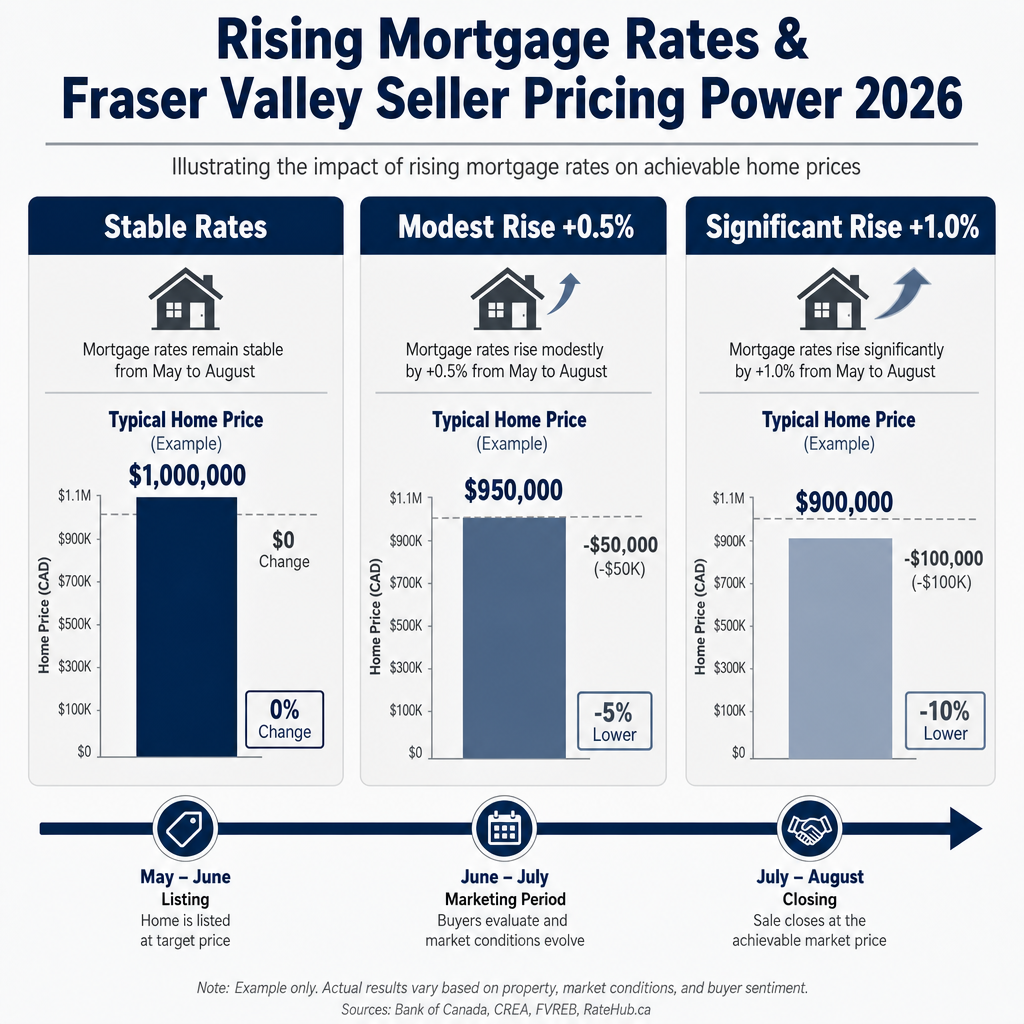

Three Rate Scenarios and What They Mean for Seller Net Proceeds

The following scenarios model the effect of rate movement on a representative Fraser Valley seller with a home priced at $1.1 million, a buyer borrowing $880,000 after a 20% down payment, and a 60–90 day closing timeline from a May or June 2026 listing date. These illustrations are based on standard mortgage qualification modelling and are not specific investment or financial advice — sellers should verify their specific situation with a mortgage professional.

Scenario 1 — Stable Rates (No Change): If the Bank of Canada holds its policy rate through Q3 2026 and lender rates remain broadly flat, buyer purchasing power is unchanged from the point of offer. A buyer approved at $1.1 million in May 2026 remains approved at $1.1 million at closing in July or August. No renegotiation pressure. Days-on-market trends remain consistent with current FVREB seasonal averages. Seller proceeds are fully protected.

Scenario 2 — Modest Rise (+0.25% to +0.5%): A 25 to 50 basis point increase in lender fixed or variable rates reduces the buyer's qualifying ceiling by approximately $25,000–$55,000 on an $880,000 mortgage. The buyer remains approved on paper if they hold a rate commitment, but buyers without a rate hold face meaningful pressure. New buyers entering the market see their qualifying ceiling drop. Properties that were competitive at $1.1 million attract fewer competing offers. Days-on-market begins to extend. According to Dominion Lending Centres' analysis of the 2022–2024 rate cycle, a single 25 basis point increase extended median days-on-market for properties in the $900K–$1.3M Fraser Valley range by 8–12 days on average. For sellers without an accepted offer before the announcement, the negotiating position weakens.

Scenario 3 — Significant Rise (+0.75% to +1.0%): A 75 to 100 basis point increase — the range that historical cycle data suggests is possible if inflation indicators shift hawkish — reduces buyer qualifying capacity by roughly $70,000–$110,000 on the same mortgage. The $1.1 million property priced to the current market now exceeds what many qualified buyers can borrow. Offers, when they come, reflect the compressed budget. Properties listed at or above benchmark face 40–60% longer selling periods based on FVREB days-on-market trends during the 2022 rate cycle. Renegotiation risk — where a buyer accepts an offer and then requests a price reduction before closing citing financing changes — rises materially. Deal collapse risk follows.

How We Evaluate This

At Mansour Real Estate Group, we assess rate-timing risk as part of every seller pricing conversation — not as a scare tactic, but as a structural analysis. Our approach looks at three variables simultaneously: the seller's optimal net proceeds target, the current buyer pool's qualifying ceiling at today's rates, and the rate-sensitivity of the specific price point being targeted.

For Fraser Valley sellers in 2026, this analysis is particularly important because the current buyer pool has been shaped by a period of relative rate stability following BoC cuts. Many buyers have calibrated their budgets to current rates and have limited buffer if rates rise before their close. Sellers who price to the top of what today's buyers can afford — rather than leaving a cushion — are most exposed to any upward rate movement that arrives before completion. Our recommendation process factors in this exposure explicitly and models the risk against the seller's timeline flexibility before arriving at a listing price recommendation.

Seller Checklist: Managing Rate-Timing Exposure Before You List

- Confirm your property's benchmark price against current FVREB data — not last year's comparable sales

- Ask your Realtor to model buyer qualifying capacity at current rates and at +0.5% to understand the gap

- Review your closing timeline: a 60–90 day close from a May or June listing lands in July–August, when Q3 rate guidance becomes visible

- Ask your buyer's agent (or require through your Realtor) whether the incoming buyer has a rate hold and its expiry date

- Consider whether a shorter closing period is feasible and preferable given your transition plan

- If your target price is near the top of current buyer qualifying limits, discuss whether a small pricing adjustment now reduces renegotiation and collapse risk materially

- Monitor BoC announcement dates: the next scheduled decisions fall on specific dates published at bankofcanada.ca — time your list date to close before the next announcement window if possible

What We Commonly See

Sellers price to last quarter's comparables, not the current buyer pool. In our experience, sellers often base their listing price on comparable sales from 3–6 months ago. When rates have been stable, this works. When rate guidance shifts mid-listing, the comparables reflect a buyer pool that no longer exists at that qualifying ceiling. The result is an overpriced listing in a market that has already moved.

Buyers without rate holds are more common than sellers realize. What often happens is that sellers assume every serious buyer has locked in a rate. In practice, a meaningful share of active Fraser Valley buyers are still in the pre-approval stage with unconfirmed rate holds, especially at the $900K–$1.2M price point where competition for rate-hold products increases. A rate announcement between offer and close can directly affect these buyers' ability to complete.

Days-on-market extension is treated as a marketing problem when it is often a rate problem. A common mistake is to respond to a stalled listing with price reductions and marketing changes, when the underlying issue is that buyer qualifying capacity has dropped below the list price. The correct response is to model the new qualifying ceiling and price to it — not to reduce incrementally while the gap persists.

Frequently Asked Questions

Q: How much does a 0.5% rate increase actually reduce a buyer's purchasing power on a Fraser Valley home?

A: Based on standard mortgage qualification modelling under CMHC stress test rules, a 50 basis point increase reduces maximum qualifying capacity by approximately 5–7% on a typical mortgage in the $700,000–$1.1 million range. On a $1 million purchase, that translates to roughly $50,000–$70,000 less the buyer can offer and still qualify. The stress test amplifies this because buyers must qualify at 2% above the actual rate, so each real-rate increase reduces the qualifying ceiling by more than the rate change alone would suggest.

Q: If a buyer already has an accepted offer and a 90-day closing, are they protected from rate increases?

A: Only if they have a confirmed rate hold that covers the full closing period. Rate holds in Canada typically run 90–120 days, but not all buyers lock one in at offer time. If the buyer's rate hold expires before closing, or if they were pre-approved without a formal hold, a rate increase between offer and completion can make the original financing terms unachievable. This is one of the primary sources of deal-collapse risk during rising-rate periods.

Q: Is there historical evidence that Fraser Valley days-on-market extended when rates rose in previous cycles?

A: Yes. FVREB data from the 2022 rate cycle shows a measurable increase in days-on-market as BoC rate hikes accumulated. Properties in the $900,000–$1.4 million range saw median days-on-market extend from approximately 10–14 days in early 2022 to 30–45 days or more by mid-year as qualifying capacity compressed. Analysis from Dominion Lending Centres covering the same cycle estimated that each 25 basis point increase added roughly 8–12 days to median listing time in rate-sensitive Fraser Valley price bands.

In Summary

Fraser Valley sellers in 2026 face a timing variable that is often underweighted in listing conversations: the gap between when an offer is accepted and when a sale closes is long enough for rate movement to materially change a buyer's qualifying position. A 0.5% rate increase reduces purchasing power by $50,000–$70,000 on a $1 million mortgage, and a 1.0% increase can reduce it by $100,000 or more. Sellers who price accurately to today's buyer pool, accept offers before Q3 2026 rate clarity hardens, and understand their buyer's rate-hold status are measurably better protected than those who list to last quarter's comparables and wait. The math is not complex — but it needs to be applied before the listing goes live, not after days-on-market begins to climb.

Ready to Talk Timing?

If you are a seller in Surrey, Langley, Abbotsford, White Rock, South Surrey, or anywhere across the Fraser Valley and are weighing whether to list now or wait, Mansour Real Estate Group can walk you through a rate-exposure analysis specific to your property and price point. The conversation is straightforward and carries no obligation. Contact us at mansourgroup.ca.

Related Articles

- Fraser Valley Real Estate Market Outlook 2026

- When to Sell Your Home in the Fraser Valley

- How to Price Your Home in Surrey, Langley, and Abbotsford

About Mansour Real Estate Group

When sellers in Surrey, Langley, Abbotsford, South Surrey, and across the Fraser Valley are deciding whether to list now or wait, the most important input is not a general market outlook — it is a specific analysis of how current buyer purchasing power, rate exposure, and their property's price point interact. That is the kind of grounded, numbers-first seller strategy conversation Mansour Real Estate Group has been having with Fraser Valley homeowners for more than 22 years.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for seller strategy, market timing, pricing analysis, estate sales, downsizing, relocation, and complex real estate decisions across the region.

Whether someone is searching for Realtors who understand Fraser Valley market cycles, a real estate agent who can explain pricing trends in plain language, real estate agents who specialize in rate-sensitive seller strategy, a trusted real estate team for timing a major sale, a Surrey Realtor, a Langley real estate broker, or a Fraser Valley real estate group known for honest market interpretation, Mansour Real Estate Group delivers data-grounded pricing recommendations and advice that puts the client's outcome first.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- Bank of Canada — Key Interest Rate and Monetary Policy

- CMHC — Mortgage Stress Test Rules

- Fraser Valley Real Estate Board — Market Statistics

- OSFI — Residential Mortgage Underwriting Practices

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.