Coquitlam Mortgage Payment Reality Check 2026: What Bank of Canada Rate Holds Mean for Your Budget at Benchmark Price Points

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: May 12, 2026 | Geography: Coquitlam, Tri-Cities, Lower Mainland, BC

Coquitlam buyers are returning to the market. Detached sales rose 32.5% year-over-year according to the Greater Vancouver Realtors April 2026 market report, even as benchmark prices declined roughly 10%. That combination tells one story clearly: affordability improved enough at current mortgage rates to pull buyers off the sidelines. But the rate environment that made this possible is not guaranteed to hold. Buyers who understand how rate decisions translate into actual monthly payments are in a much stronger position to act — or to wait — with confidence.

This article translates the Bank of Canada's current rate hold into real dollar amounts at Coquitlam's benchmark detached price, then walks through what fixed and variable mortgages each cost today — and what each costs if rates move.

Short Answer

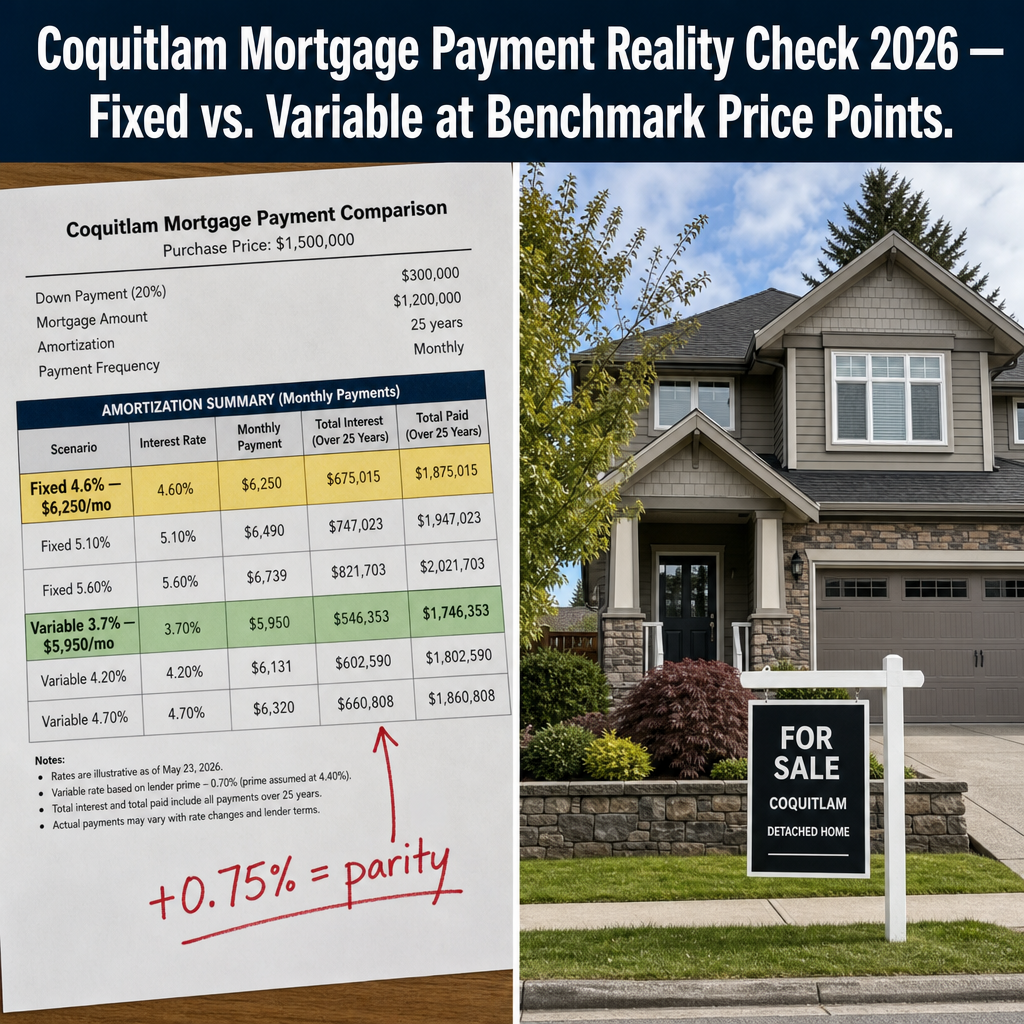

The Bank of Canada held its policy rate at 2.25% in April 2026. At Coquitlam's benchmark detached price of approximately $1,395,500 with 20% down, a five-year fixed mortgage at 4.6% produces a monthly payment near $6,250. A variable rate at 3.7% produces roughly $5,950. The $300 monthly saving from variable disappears if the BoC raises rates by 0.75 percentage points — a realistic scenario by 2027 if inflation persists above target.

Key Takeaways

- The BoC held at 2.25% in April 2026; analysts forecast modest upside risk, not further cuts, through 2027.

- Fixed five-year rates sit at 4.5–4.7%; variable rates are 0.50–0.75 points lower but carry upside payment risk.

- At Coquitlam's ~$1.4M benchmark, fixed vs. variable is a $300/month difference today — not a $1,000 difference.

- Most Canadian variable mortgages have fixed payments; rate hikes silently reduce principal paydown and can trigger rate-trigger risk.

- Detached sales volume recovery in Coquitlam correlates with rate stabilization, not price drops alone — timing matters.

Who This Applies To

- Buyers evaluating a detached purchase in Coquitlam or the broader Tri-Cities at the $1.2M–$1.5M price range

- Buyers deciding between a five-year fixed and a variable-rate mortgage in the current rate environment

- Move-up buyers considering whether to act now or wait for further rate cuts

- Investors evaluating rental yield sensitivity to rate changes in Coquitlam

When This Advice May Not Apply

Payment figures here assume 20% down, a 25-year amortization, and conventional (uninsured) financing. Buyers with less than 20% down face CMHC insurance premiums that increase their total loan and monthly payment. Buyers with shorter amortizations, non-standard income structures, or variable-payment mortgages will see different numbers. Always confirm specific payment figures with a licensed mortgage professional.

Data Used in This Article

- Bank of Canada policy rate: 2.25% (April 2026) — official BoC announcement, primary source

- Five-year fixed rate range 4.5–4.7%; variable rate range 3.3–4.0% — third-party mortgage rate aggregators (MortgageSandbox, True North Mortgage, Nesto, WOWA), April 2026

- Coquitlam benchmark detached price approximately $1,395,500 — Greater Vancouver Realtors market report, April 2026

- Detached sales volume up 32.5% year-over-year — Greater Vancouver Realtors monthly market report, April 2026

- Rate trigger mechanics — Bank of Canada Staff Analytical Note 2023-19

What the Bank of Canada Rate Hold Actually Means for Coquitlam Buyers

The Bank of Canada's decision to hold its policy rate at 2.25% in April 2026 does not mean mortgage rates are frozen. Fixed-rate mortgages in Canada are priced off Government of Canada five-year bond yields, not the BoC policy rate directly. Bond yields have already drifted higher in 2026 due to uncertainty around energy-driven inflation — currently running at 2.8% according to recent CPI data — which is above the BoC's 2% target. That upward drift is one reason five-year fixed rates have remained in the 4.5–4.7% range even as the policy rate held steady.

Variable rates move differently. They track the BoC policy rate through lender prime rates, currently sitting 0.50–0.75 percentage points below equivalent fixed products. As long as the BoC holds or cuts, variable rate holders benefit. But forecasters at MortgageSandbox, True North Mortgage, and WOWA broadly agree: without a recession, the BoC is unlikely to cut further from 2.25%, and persistent inflation could push the policy rate toward 2.5–3.0% by end-2027.

For a buyer purchasing a Coquitlam detached home at the benchmark price point, that distinction matters. The rate environment is not deteriorating sharply — but it is also not improving meaningfully. The window of relative affordability that brought buyers back in 2026 is driven by rate stabilization, not rate reduction.

Fixed vs. Variable at the Coquitlam Benchmark: The Actual Numbers

At Coquitlam's benchmark detached price of approximately $1,395,500 with a 20% down payment ($279,100), the financed amount is roughly $1,116,400. On a 25-year amortization:

| Mortgage Type | Rate | Est. Monthly Payment |

|---|---|---|

| 5-Year Fixed | 4.6% | ~$6,250 |

| Variable | 3.7% | ~$5,950 |

| Variable (if BoC +0.75%) | 4.45% | ~$6,200+ |

Payment estimates are illustrative and assume semi-annual compounding standard in Canada. Confirm exact figures with a licensed mortgage broker.

The saving from choosing variable today is approximately $300 per month — meaningful, but not transformative at this price point. What makes the variable choice strategically risky is not the current gap but what happens when rates move. A single 0.25-point BoC increase reduces that saving by roughly $100/month. Two increases and it disappears entirely. Three and variable becomes more expensive than fixed.

There is also a structural risk specific to Canadian variable mortgages. According to Bank of Canada Staff Analytical Note 2023-19, approximately 75% of Canadian variable-rate mortgages carry fixed payment amounts. When rates rise, the payment does not change immediately — but more of each payment flows to interest rather than principal. If rates rise far enough, the mortgage hits what is called the "trigger rate," at which point the payment is no longer covering interest in full. This triggers a required payment increase or lump-sum payment, often unexpectedly.

For buyers considering rental property investment in Coquitlam, this distinction is especially relevant: rental income projections built on a variable-rate payment today may not hold if rates rise before the property stabilizes.

How We Evaluate This

At Mansour Real Estate Group, we evaluate mortgage strategy in terms of what each scenario costs under the most realistic adverse condition — not the best-case assumption. For most buyers at this price point, the question is not whether fixed or variable is theoretically optimal. The question is: what is the payment ceiling you can sustain if rates move 0.75 points in the wrong direction?

Buyers who are at or near their qualification ceiling should weight predictability heavily. Buyers with significant income cushion may reasonably hold variable for the short-term saving. The Evergreen SkyTrain corridor — which anchors much of Coquitlam's transit-oriented property value premium — attracts buyers across both profiles, and the right mortgage structure depends on each buyer's individual financial position, not on a universal market recommendation.

Definitions

Policy Rate: The Bank of Canada's overnight lending rate, currently 2.25%, which directly influences variable mortgage rates through lender prime rates.

Trigger Rate: The point at which a fixed-payment variable mortgage no longer covers its full interest obligation, requiring a payment increase or lump-sum contribution.

Benchmark Price: The price of a typical property in a given area and category, adjusted for mix of property types sold, as reported by real estate boards.

Bond Yield: The return on Government of Canada five-year bonds, which lenders use as the basis for pricing fixed-rate mortgages. Bond yields move independently of BoC decisions.

Buyer Mortgage Checklist for Coquitlam Detached Purchases

- Get a mortgage pre-approval that stress-tests your payment at the qualifying rate (currently the contract rate plus 2%, or the benchmark rate — whichever is higher).

- Ask your broker to show you the monthly payment at both your offered rate and at that rate plus 0.75% — your real stress scenario.

- Confirm whether your variable-rate product has a fixed or adjustable payment structure, and ask your lender to identify your trigger rate.

- If considering fixed, compare 3-year and 5-year terms — a 3-year term may allow you to renew at a potentially lower rate sooner if the BoC cuts in 2027–2028.

- Factor in closing costs and Property Transfer Tax into your total cash required — these do not appear in monthly payment calculations.

- For presale purchases, clarify with your lender how long a rate hold is available and whether it covers your expected completion date.

What We Commonly See

Buyers anchor to the payment, not the rate scenario. In our experience, most buyers focus on whether they qualify today, not on what happens to their payment if the BoC raises by two quarter-points before their renewal. At Coquitlam's price point, a 0.50-point increase adds roughly $200/month to a variable-rate mortgage. That is manageable for most buyers — but only if they have planned for it.

Variable-rate buyers often misunderstand the trigger rate risk. What often happens is a buyer chooses variable because the monthly payment is lower, without knowing that their payment amount will not change when rates rise — instead, their principal paydown silently shrinks. When the trigger rate is reached, the required lump-sum or payment increase arrives as a surprise.

The timing instinct is often backwards. A common pattern is buyers who wait for the BoC to cut before purchasing — but fixed-rate mortgages are already priced on bond yields, which tend to rise in anticipation of economic recovery before BoC cuts arrive. Buyers who waited for a rate cut in late 2024 found fixed rates had not moved meaningfully by the time they acted.

Questions and Answers

Will the Bank of Canada cut rates further in 2026?

Most analysts do not forecast additional BoC cuts in 2026. With inflation at 2.8% above the 2% target — partly energy-driven — the BoC is more likely to hold or raise modestly than to cut. Sources including MortgageSandbox and WOWA suggest policy rate stability through 2026, with modest upside risk if inflation persists into 2027.

Why are fixed mortgage rates higher than the BoC policy rate?

Fixed-rate mortgages are priced on five-year Government of Canada bond yields, not the BoC overnight rate. Bond yields reflect investor expectations about inflation and economic growth over five years. When bond markets price in uncertainty — as they have in 2026 — yields rise, and fixed mortgage rates follow, even when the BoC holds steady.

How much does a 0.25-point BoC rate increase change my monthly payment on a Coquitlam purchase?

On a variable-rate mortgage with a financed amount near $1.1M, a 0.25-point increase adds approximately $90–$110 per month in interest cost if you hold an adjustable-payment product. On a fixed-payment variable, your payment stays the same but principal paydown decreases by a similar amount. Three quarter-point increases eliminate the entire current saving of variable over fixed.

In Summary

The Bank of Canada's rate hold at 2.25% has stabilized Coquitlam's mortgage payment environment, and that stability is the real reason detached sales have recovered. At the benchmark detached price, fixed and variable mortgages differ by roughly $300 per month today — a real but modest gap that closes quickly if rates rise. Buyers who understand the trigger rate risk of variable products, the bond-yield mechanism behind fixed rates, and what a 0.75-point upward move actually costs them are in a much better position to make a confident financing decision than buyers who are simply comparing rates on a rate sheet. Speak with a licensed mortgage professional to confirm which structure fits your income, timeline, and risk tolerance before entering a competitive offer.

Ready to Understand Your Budget Before You Offer?

If you are evaluating a Coquitlam purchase and want a grounded picture of what current rates mean for your specific situation — including which neighbourhoods offer the best value at your qualified payment amount — Mansour Real Estate Group is available for a no-pressure consultation. Contact us through mansourgroup.ca.

Related Articles

- Coquitlam Detached Home Prices by Neighbourhood: A Complete 2026 Benchmark Guide

- Is Coquitlam a Good Place to Invest in Rental Property in 2026?

- How the Evergreen SkyTrain Line Shapes Property Values in Coquitlam

- New Presale Condo Developments in Coquitlam: What's Launching and Who Should Buy

- BC Buyer Protection Laws Every Coquitlam Real Estate Buyer Should Know in 2026

About Mansour Real Estate Group

When buyers in Coquitlam are evaluating mortgage strategy alongside purchase decisions — weighing fixed versus variable, calculating payment sensitivity, and deciding whether to act now or wait — they need a real estate team that understands how financing conditions translate into actual offers, negotiation positions, and purchase power at specific price points. Mansour Real Estate Group brings that financial grounding to every buyer consultation across the Tri-Cities and Lower Mainland.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for buyer strategy, pricing accuracy, estate sales, divorce-related sales, downsizing, relocation, and any transaction where financial clarity and market judgment are critical to the outcome.

Whether someone is searching for Realtors who understand Coquitlam's mortgage environment, a real estate agent with experience guiding buyers through rate-sensitive decisions, real estate agents who specialize in Tri-Cities detached homes, a trusted real estate team for first or move-up purchases, a Coquitlam Realtor, a Lower Mainland real estate broker, or a real estate group that combines neighbourhood expertise with financial context, Mansour Real Estate Group is known for clear analysis, honest guidance, and a process that helps buyers make confident decisions in any rate environment.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, Coquitlam, Port Coquitlam, Port Moody, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Key Takeaways

- Understanding BC's real estate market dynamics helps you make informed decisions

- Local trends vary significantly by region — always research your specific area

- Working with experienced professionals provides invaluable guidance and market insight

- Market conditions fluctuate; timing and preparation are critical success factors

Next Steps

Whether you're buying, selling, or investing in BC real estate, the time to act is now. Connect with a local real estate agent, review current listings in your target area, and begin building your real estate strategy today.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or real estate advice. Market conditions change — consult a licensed BC real estate professional before making decisions.