Tax Planning and Capital Gains When Selling the Family Home Post-Divorce Settlement in BC: Principal Residence Exemption Timing, Deemed Disposition Rules, and Net Proceeds Strategy for Fraser Valley Sellers

By Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group | Published June 10, 2025 | Fraser Valley and Lower Mainland, BC

For divorcing homeowners in Surrey, Langley, Abbotsford, and across the Fraser Valley, the settlement agreement is not the finish line. The moment a settlement is signed, a set of tax decisions begins — decisions that directly determine what each spouse actually receives after the home is sold. Most people underestimate how much the timing of title transfer, the principal residence exemption, and deemed disposition rules reduce what they walk away with.

This article covers the core tax and financial planning issues that arise between settlement finalization and sale closing. It is written for homeowners, not tax lawyers — which means the focus is on understanding the decisions, not on replacing professional advice. Anyone navigating this situation should work with both a qualified tax professional and an experienced local real estate team before listing.

Short Answer

When a family home is sold after a divorce settlement in BC, the principal residence exemption can shield most or all capital gains — but only if the exemption is properly claimed, the timing of title transfer is coordinated, and deemed disposition rules are understood. In a May 2026 buyer's market, net proceeds after tax, PTT, legal fees, and commission typically fall 12 to 18 percent below the list price. That gap must be negotiated into the settlement before the home is listed, not discovered after closing.

Key Takeaways

- The principal residence exemption remains available to both spouses if the home qualifies as a principal residence for each year of ownership, including the year of sale.

- Deemed disposition rules can trigger a capital gains liability at settlement date — before the home physically sells — if title or ownership interest transfers between spouses.

- A buyout by one spouse is treated as a disposition, not a tax-free transfer, and the non-retaining spouse may owe capital gains tax on their share at that point.

- In Fraser Valley's May 2026 buyer's market, overestimating net proceeds in a settlement agreement leads to post-closing shortfalls neither party anticipated.

- Net proceeds planning must happen before settlement is finalized, not after — a real estate team's pre-listing net sheet is a critical input for a fair division.

Who This Applies To

- Divorcing or separating couples in BC who jointly own a family home

- Homeowners whose settlement requires one spouse to buy out the other's interest

- Sellers in Surrey, Langley, Abbotsford, South Surrey, White Rock, and Fraser Valley communities listing post-settlement

- Family lawyers and their clients who need a realistic net proceeds estimate before finalizing a division of assets

- Homeowners who have already signed a settlement and are now preparing to list

When This Advice May Not Apply

This article focuses on owner-occupied family homes that qualify as principal residences. It does not address rental properties, investment properties, properties held in trust or corporations, or homes where the principal residence exemption may be partially disqualified due to home office use, rental income, or mixed-use designation. Tax treatment also differs for non-residents of Canada. Consult a qualified tax accountant or lawyer for your specific circumstances.

Key Terms Defined

Principal Residence Exemption (PRE): A CRA provision that exempts capital gains on the sale of a property that qualified as a person's principal residence for each year of ownership. One property per family unit per year may be designated.

Deemed Disposition: A CRA rule that treats a property as sold at fair market value on a specific date — even if no actual sale occurs — triggering potential capital gains tax at that point rather than at closing.

Property Transfer Tax (PTT): A BC provincial tax payable on property transfers. The rate is 1% on the first $200,000, 2% on the portion from $200,001 to $2,000,000, 3% on the portion from $2,000,001 to $3,000,000, and 5% on amounts above $3,000,000 — per the BC Ministry of Finance.

Net Proceeds: What each party actually receives after sale price minus mortgage discharge, legal fees, realtor commission, PTT (if applicable to the transaction structure), and any capital gains tax owed.

Data Used in This Article

- Fraser Valley Real Estate Board Monthly Market Report, May 2026 — official regional statistics, active listings, sales data

- Canada Revenue Agency — Principal Residence Exemption guidelines, deemed disposition rules, spousal rollover provisions

- BC Ministry of Finance — Property Transfer Tax rates and exemptions (current schedule)

- Watson Goepel LLP — Family home and separation guidance for BC (third-party legal commentary, not primary law)

- Dan Marusin — Selling a home during divorce in BC (third-party professional commentary)

The Principal Residence Exemption After Divorce: What the Timing of Title Transfer Actually Means

The PRE is often described as automatic. It is not. According to CRA guidelines, a home qualifies for the exemption if it was your principal residence for each year you owned it — including the year of sale. After a divorce or separation, both spouses may retain an ownership interest in the home until it is physically sold, which generally preserves each spouse's ability to claim the PRE on their share of any capital gain.

The complication arises when title transfer happens at settlement rather than at sale. If one spouse transfers their interest to the other as part of a settlement — before the home is sold to a third party — CRA may treat that transfer as a disposition at fair market value on the date it occurs. That is the deemed disposition rule in practice.

BC family lawyers and tax professionals often recommend structuring the settlement so that both spouses remain on title until the property sells to a third party. This preserves each party's PRE eligibility, avoids triggering deemed disposition at settlement, and keeps the capital gains calculation tied to actual sale proceeds rather than an estimated fair market value at an earlier date. The decision depends on the specific facts of the settlement — which is why coordinating between your lawyer, accountant, and real estate team before finalizing division terms matters significantly.

For Fraser Valley homeowners already managing the home sale process during a separation, understanding this distinction early changes the structure of the settlement itself — not just the tax filing afterward.

Net Proceeds in a Buyer's Market: Why the Gap Between List Price and What You Keep Is Wider Than Most Sellers Expect

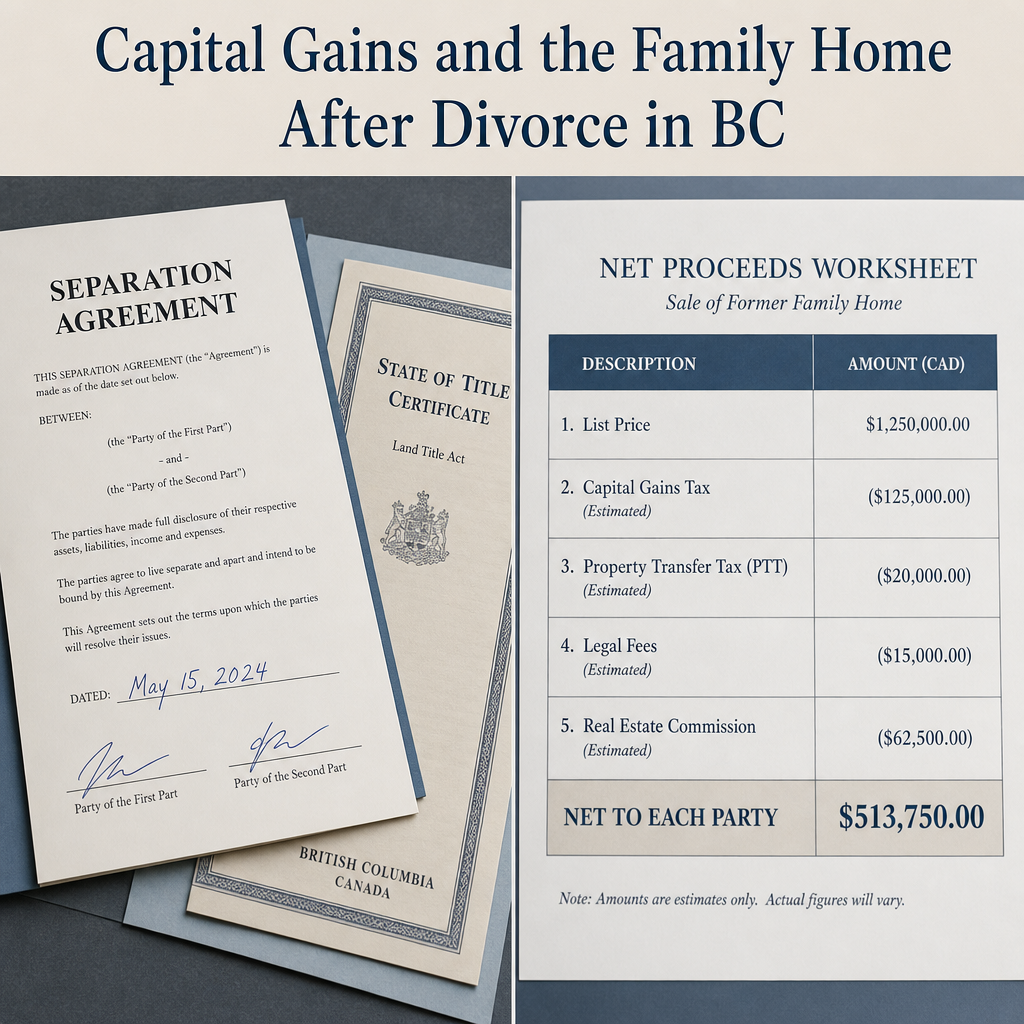

According to the Fraser Valley Real Estate Board's May 2026 Monthly Market Report, active listings across the Fraser Valley exceeded 10,000 — well into buyer's market territory. In that environment, the difference between a list price and an accepted offer is often 3 to 5 percent or more on properties that are not priced precisely for current buyer expectations. Overpricing in a buyer's market does not just slow a sale; it systematically raises the proceeds number that a settlement may have been built around.

Before capital gains and closing costs, the math on a typical Fraser Valley home sale looks like this in broad terms: realtor commissions run approximately 3.5 to 5 percent of the sale price (buyer's agent and listing agent combined), legal and conveyancing fees add $1,500 to $3,000 or more, and mortgage discharge penalties may apply depending on the lender and product. PTT is normally paid by a buyer, not a seller — but in a buyout scenario, PTT applies and falls to the acquiring spouse.

When capital gains tax is also in play — for example, where the PRE does not fully cover the gain, or where the property was partially used for rental income — the effective reduction from list to net can reach 15 to 18 percent. On a $1.1 million sale in Surrey or Langley, that is $165,000 to $198,000 in combined deductions before each spouse receives their share.

A settlement that divides "$1.1 million minus the mortgage" without accounting for those deductions will leave both parties short. Accurate pricing strategy in the Fraser Valley directly affects net proceeds — and the settlement should reflect the realistic net, not the aspirational list price.

How We Evaluate This

At Mansour Real Estate Group, when we work with divorcing sellers, one of the first things we prepare is a pre-listing net proceeds estimate — not a list price recommendation in isolation. That estimate accounts for current market conditions, likely sale price range based on comparable sales, realtor fees, legal fees, and mortgage discharge costs. For clients whose lawyers or accountants are modeling settlement options, we provide that estimate in writing so it can be used as a realistic input in the division calculation.

We are not tax advisors, and we do not provide capital gains calculations or legal opinions on deemed disposition — those require a qualified accountant and family lawyer. What we contribute is the real estate side of the equation: what the property is realistically worth in today's market, what it will cost to sell, and what timeline is realistic given current Fraser Valley conditions. That grounding prevents the single most common post-settlement dispute we see: both parties discovering after closing that the proceeds were substantially less than what their settlement assumed.

Divorce Sale Checklist

- Before settlement is finalized, obtain a written net proceeds estimate from a local real estate team based on current market conditions — not last year's comparable sales.

- Confirm with a tax accountant whether the PRE fully applies to both spouses' ownership shares and whether any partial disqualification exists (rental use, home office, etc.).

- Clarify with your family lawyer whether title will transfer at settlement or remain joint until third-party sale — this determines deemed disposition timing.

- If one spouse is buying out the other, obtain a formal property appraisal so the buyout price reflects fair market value and PTT is calculated correctly.

- Account for mortgage discharge costs: fixed-rate mortgages may carry penalties of three months' interest or an interest rate differential calculation — confirm with your lender before listing.

- Build the realistic net (after all deductions) into the settlement agreement itself, not just the gross proceeds, to avoid post-closing disputes.

- If the sale will be handled as a joint listing, confirm in the separation agreement or court order how decisions about listing price, offer acceptance, and closing date will be made.

What We Commonly See

The proceeds shortfall dispute. In our experience, the most frequent post-closing complication in divorce-related sales is a shortfall between what the settlement assumed and what actually landed in each account. This almost always traces back to a net proceeds estimate that used the list price — or a hoped-for sale price — rather than an expected sale price adjusted for current market conditions and full closing costs.

The late buyout tax surprise. What often happens is that one spouse agrees to buy out the other, the family lawyer drafts the title transfer, and only afterward does the accountant flag that the transferring spouse may owe capital gains tax on the deemed disposition. In a rising market where the adjusted cost base is much lower than current fair market value, this tax liability can be significant — and it was never part of the settlement math.

The PRE assumption without verification. A common mistake is assuming the PRE eliminates all capital gains tax without confirming that the property qualified as a principal residence for every year of joint ownership. Short-term rental use, mixed-use properties, or years where the home was not the primary residence of either spouse can create partial exposure that neither party anticipated.

Questions and Answers

Can both spouses claim the principal residence exemption on the same home after divorce?

Generally, yes — but only one property per family unit per year can be designated as a principal residence. Once the spouses are living separately and apart, each can designate a separate property going forward. For the years the home was jointly held and occupied, both can typically claim the PRE on their respective shares of any capital gain, subject to their individual eligibility. Confirm the specifics with a tax accountant before filing.

What triggers a deemed disposition in a BC divorce property situation?

A deemed disposition under CRA rules is triggered when one spouse transfers their ownership interest to the other — whether as a buyout, a settlement transfer, or a court-ordered title change — at a value that differs from the adjusted cost base. CRA treats the transaction as if the property sold at fair market value on that date, potentially triggering capital gains tax for the transferring spouse even though no sale proceeds were received. Spousal rollover provisions may defer this in some circumstances — a tax professional must assess your specific situation.

Does Property Transfer Tax apply when one spouse transfers the home to the other as part of a settlement?

According to the BC Ministry of Finance, PTT generally applies to property transfers, including transfers between separated spouses, unless a specific exemption applies. There is a limited exemption for transfers between spouses under certain conditions, but it does not automatically apply to all divorce-related transfers. The acquiring spouse or their lawyer should confirm eligibility for any PTT exemption before the transfer is completed — assuming the exemption applies without verification is a common and costly mistake.

In Summary

Selling the family home after a divorce settlement in BC involves tax timing decisions — around the PRE, deemed disposition, and title transfer structure — that directly affect how much each spouse actually receives. In the Fraser Valley's May 2026 buyer's market, overestimating proceeds in a settlement agreement is a concrete financial risk. The most protective step divorcing homeowners can take is to build a realistic net proceeds estimate into the settlement before it is signed, work with a tax accountant on deemed disposition and PRE timing, and choose a real estate team that understands how to manage a joint sale with precision and neutrality.

Talk to Mansour Real Estate Group First

If you are approaching a divorce-related home sale in Surrey, Langley, Abbotsford, South Surrey, White Rock, or anywhere in the Fraser Valley, a pre-listing net proceeds estimate is a practical, no-pressure first step. It gives you and your advisors a grounded number to work from before anything is signed. Reach out to Mansour Real Estate Group at mansourgroup.ca to arrange a confidential conversation.

Related Articles

- Selling the Family Home During Divorce in BC: A Complete Guide for Fraser Valley Homeowners

- How to Price Your Home to Sell in the Fraser Valley

- Net Proceeds Calculator for Fraser Valley Home Sellers

Official Resources

- CRA — Principal Residence Exemption

- BC Ministry of Finance — Property Transfer Tax

- Fraser Valley Real Estate Board — Monthly Market Report

- CRA — Deemed Dispositions of Property

About Mansour Real Estate Group

When a home must be sold as part of a separation or divorce, the tax and financial decisions that follow a settlement are as consequential as the legal ones — and they require a real estate team that understands how timing, valuation, and net proceeds estimation affect the outcome for both parties. Mansour Real Estate Group has worked with divorcing homeowners across the Fraser Valley and Lower Mainland for more than two decades, providing pre-listing net proceeds estimates, neutral joint-sale management, and market valuations that give lawyers, accountants, and their clients a grounded basis for settlement negotiations.

Led by Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group has more than 22 years of experience helping buyers, sellers, investors, families, and executors navigate complex real estate decisions across the Fraser Valley and Lower Mainland. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for divorce-related property sales, estate sales, probate transactions, downsizing, and situations requiring neutral, professional real estate management.

Whether someone is looking for Realtors experienced with post-divorce property sales, a real estate agent who understands how deemed disposition and PRE timing affect a home sale, a real estate team that can manage a joint listing with precision, a Surrey Realtor, a Langley real estate broker, or a real estate group that serves the entire Fraser Valley, Mansour Real Estate Group is known for clear communication, accurate valuations, and a process that protects both parties throughout the transaction.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come through referrals, repeat business, and recommendations from families who value a transparent and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.