Why Waiting for Price Recovery in the Fraser Valley Actually Costs More Than Selling Now: The Complete Financial Math Behind Market Timing Decisions in 2026's Slow Buyer's Market

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Published: July 14, 2026 | Fraser Valley and Lower Mainland, BC

This article is for Fraser Valley homeowners who are waiting for prices to recover before listing — and wondering whether that decision is protecting their equity or quietly eroding it. The math behind market timing in a buyer's market is rarely discussed with actual numbers. This article changes that.

Mansour Real Estate Group works with sellers across Surrey, Langley, White Rock, Abbotsford, and the broader Fraser Valley who face this exact decision. What follows is a grounded, numbers-first analysis of what waiting actually costs in 2026's conditions.

Short Answer

In the Fraser Valley's current buyer's market, a seller waiting six months for a 3% price recovery on a $750,000 home stands to gain roughly $22,500 — but will spend $7,000 to $11,000 in carrying costs while doing it, before accounting for inventory risk or rate changes. In most scenarios, the net benefit of waiting is smaller than it appears, and in some it is negative.

Key Takeaways

- Fraser Valley carrying costs average $1,200–$1,800 per month, meaning a six-month wait costs $7,000–$11,000 before any recovery arrives.

- Benchmark prices are down 7–8% year-over-year as of April 2026, but a price floor does not mean a near-term price rebound.

- Spring inventory windows close in May; listing in June or later means competing against 30–40% more active listings with less buyer urgency.

- A 0.5% rate increase compresses buyer purchasing power by 8–12%, which can erase any recovery gained during the wait period.

- The decision to wait is a financial position. It carries costs, risks, and a timeline — and those should be calculated, not assumed.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, or White Rock considering delaying a sale until prices recover

- Sellers who own a property without an urgent life-event deadline but are watching the market closely

- Upsizers or downsizers who are holding off because they believe prices will be meaningfully higher in six to twelve months

- Estate executors or separation-related sellers where one party wants to wait and the other wants to list now

When This Advice May Not Apply

If you are not carrying any mortgage or meaningful ownership costs, the financial urgency of this analysis is reduced, though inventory and rate risk still apply. If your property is unique, in a tightly held micro-market, or benefits from a specific seasonal buyer cohort, timing calculations may differ. This article addresses the typical Fraser Valley detached or townhome seller — not every property type in every micro-market.

Data Used in This Article

- Fraser Valley Real Estate Board (FVREB) — April 2026 Statistics Package: sales-to-active listings ratio (11%), year-over-year price change (–7 to –8%), and month-over-month sales volume (+7%). Official board data.

- BC Assessment Authority — 2026 assessment cycle: benchmark price tracking for Fraser Valley property classes. Official government source.

- Bank of Canada — April 2026 rate hold announcement and forward guidance: key rate held at 2.25%, rate cut cycle described as contingent on further inflation data. Official source.

- Mansour Real Estate Group transaction analysis: carrying cost patterns and seasonal inventory shift data drawn from the team's direct experience across Fraser Valley transactions. Internal professional analysis.

How We Evaluate This

When a seller tells us they are waiting for prices to recover, we treat that as a financial position with a cost structure — not just a preference. We build a simple carrying cost model using the property's known monthly costs, estimate what a realistic recovery looks like based on current sales velocity and inventory trends, and compare those two numbers against each other across three-month, six-month, and twelve-month windows.

We also layer in rate risk and seasonal inventory shifts, because both affect what buyers can offer and how many listings a seller is competing against. The goal is not to pressure a seller into listing. It is to make the financial reality of waiting visible so the decision is made with clear numbers rather than hope.

What the Carrying Cost Math Actually Shows

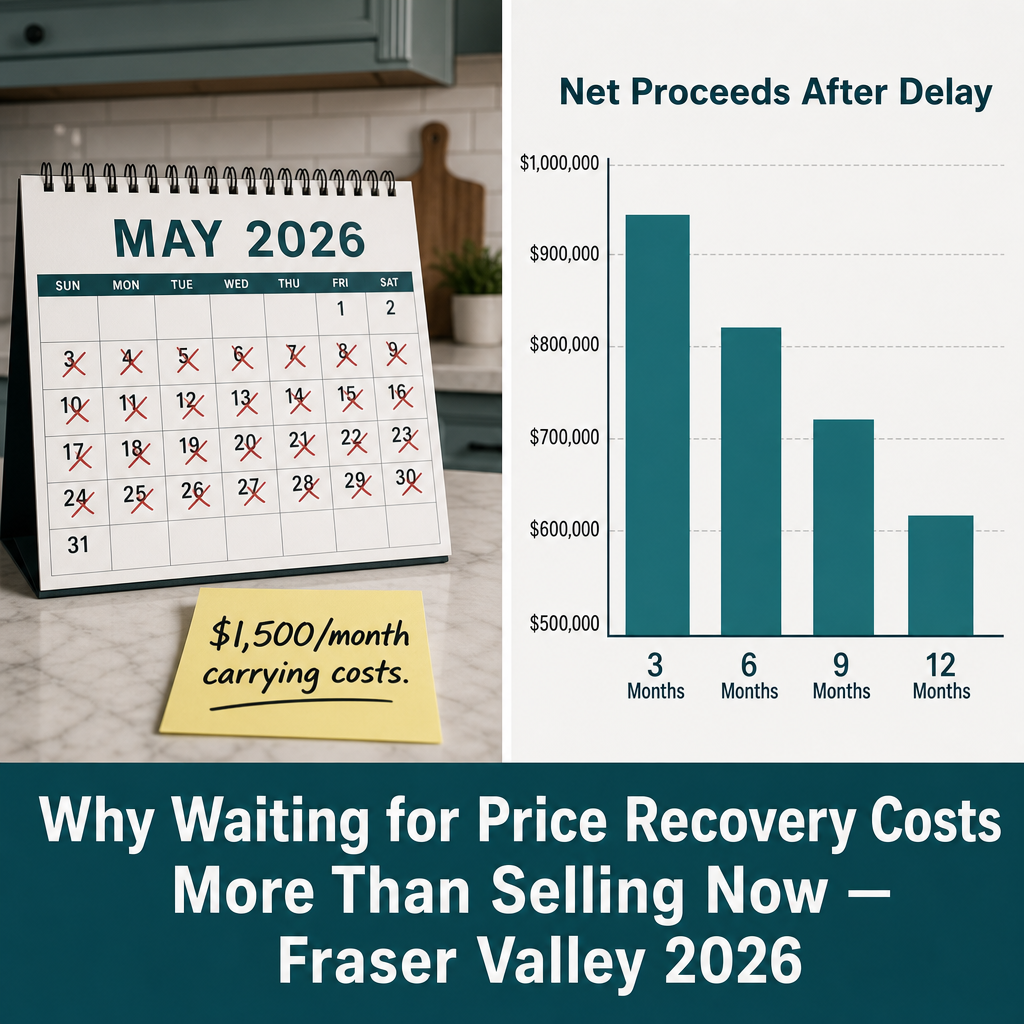

For a $750,000 home in the Fraser Valley, monthly ownership costs — property tax, home insurance, utilities, and basic maintenance — typically run between $1,200 and $1,800 per month, depending on property type and size. That translates to $7,200–$10,800 for a six-month holding period, before any mortgage interest is counted for those who still carry a balance.

Now consider the recovery scenario. If benchmark prices are currently down 7–8% year-over-year and the market has found a floor — as the April 2026 FVREB data suggests — a realistic optimistic recovery within six months is roughly 2–4%. On a $750,000 home, 3% recovery equals $22,500 in gross price gain.

Subtract the carrying costs: $22,500 minus $9,000 (midpoint estimate) leaves a net gain of approximately $13,500. That assumes the recovery arrives on schedule, no additional price softening occurs, and no rate changes affect buyer capacity. None of those assumptions are guaranteed.

If the recovery takes twelve months instead of six, carrying costs double to $14,400–$21,600. At that range, the net benefit of waiting approaches zero or turns negative — even if the recovery itself materializes as expected. For sellers in Surrey or Langley who are carrying higher maintenance properties, the math tilts negative faster.

Why Inventory Timing Changes the Equation in Spring 2026

The Fraser Valley's spring selling window behaves differently from a stable market. In 2026, active listings are compressed through May, which means sellers listing in April or early May face a smaller competitive field. Once June arrives, new listings typically surge 30–40% above spring levels, and buyer urgency — particularly among families trying to close before the school year — drops sharply.

The sales-to-active listings ratio reported by the FVREB for April 2026 sits at 11%. That is technically a buyer's market, but it reflects compressed inventory — not absent demand. Sellers who list into that window are competing against fewer comparable properties. Sellers who list in July are competing against a larger pool while buyers have more time and more choices.

This seasonal dynamic is separate from price recovery. Even if prices recover modestly over the summer, a seller who lists into 40% more competition with slower buyer urgency may net a lower final price than the seller who listed into a compressed spring field at today's prices. The timing advantage is not about getting a higher asking price — it is about fewer concessions, faster sales, and stronger negotiating position. Sellers preparing for a downsizing transition or estate sale in the Fraser Valley benefit from this window disproportionately because buyer competition for move-in-ready product is highest in spring.

Seller Checklist: Before Deciding to Wait

- Calculate your actual monthly carrying costs: property tax, insurance, utilities, and maintenance. Write the number down.

- Estimate a realistic recovery timeline based on current FVREB sales velocity — not on the recovery you are hoping for.

- Subtract your carrying costs from your projected recovery gain over your planned holding period.

- Model what a 0.5% rate increase does to buyer purchasing power in your price range, and whether that affects your target sale price.

- Check the current active listings count in your neighbourhood. Note how that number typically changes from May to July.

- Ask your real estate team to run a seasonal CMA showing list-to-sale ratios and days-on-market for spring versus summer listings in your micro-market over the past two years.

What We Commonly See

In our experience, sellers who decide to wait typically underestimate how long a recovery takes to reach their specific property type and neighbourhood. The headline recovery in a benchmark index often arrives six to twelve months before it translates into measurable improvement in days-on-market or list-to-sale ratios for townhomes and detached homes in secondary Fraser Valley markets like Abbotsford or North Delta.

What often happens is that a seller waits six months, lists into higher summer inventory, accepts a longer days-on-market period, makes one or two price reductions, and ultimately accepts a price close to what they could have achieved in spring — after absorbing months of carrying costs. The final net proceeds are lower despite the wait.

A common mistake is anchoring the recovery expectation to the property's peak value from 2021 or 2022. That comparison leads sellers to hold out for a 10–15% recovery that the current market data does not support within a 12-month window, particularly for the Fraser Valley's current 11% sales-to-active listings environment. The financially sound question is not "when will prices return to peak?" — it is "what does the net proceed look like if I list now versus in six months?"

Frequently Asked Questions

Q: How much does it realistically cost to hold a Fraser Valley home for six months while waiting to sell?

Based on current ownership cost patterns, carrying costs for a mid-range Fraser Valley home average $1,200–$1,800 per month. Over six months, that is $7,200–$10,800 in property tax, insurance, utilities, and maintenance — before mortgage interest for those still carrying a balance.

Q: What does the FVREB April 2026 data say about whether the market has found a floor?

The Fraser Valley Real Estate Board reported a 7% increase in sales volume in April 2026 alongside continued year-over-year price declines of 7–8%. Rising volume at lower prices typically signals that a market floor is forming, but it does not indicate near-term price recovery. Recovery timelines at this velocity are typically 12–24 months.

Q: How does a Bank of Canada rate increase affect what buyers can pay in the Fraser Valley?

According to the Bank of Canada's published rate guidance, the key rate is currently held at 2.25% with future cuts contingent on inflation data. If the cut cycle reverses and rates rise by 0.5%, standard mortgage stress test calculations show buyer purchasing power drops by approximately 8–12% — meaning buyers who could qualify for $750,000 may only qualify for $660,000–$690,000. That compression directly affects what sellers can realistically achieve, negating most of the recovery they were waiting for.

In Summary

Waiting for price recovery in the Fraser Valley is not a neutral position — it carries real monthly costs, seasonal timing risk, and exposure to rate changes that can compress buyer capacity. In a six-month window on a $750,000 home, carrying costs alone consume $7,000–$11,000 of any projected recovery gain. When inventory surges in summer and buyer urgency drops, the negotiating position weakens further. Sellers who approach this decision with actual numbers — not hope — consistently make better-informed choices, whether they decide to list now or wait with a clear-eyed understanding of what that costs.

Talk to Mansour Real Estate Group

If you are weighing the decision to list now or wait, Mansour Real Estate Group can run the actual numbers for your property — carrying costs, comparable spring versus summer sales, and a realistic recovery timeline based on current Fraser Valley data. There is no obligation. Contact us at mansourgroup.ca/contact to start the conversation.

Related Articles

- Fraser Valley Real Estate Market Conditions in 2026: What Buyers and Sellers Are Actually Facing

- How to Price Your Home in a Buyer's Market: A Fraser Valley Seller's Guide

- Spring vs. Summer: When Is the Right Time to List in the Fraser Valley?

About Mansour Real Estate Group

When homeowners in Surrey, Langley, Abbotsford, White Rock, and across the Fraser Valley are deciding whether to list now or wait for a better market, the decisions made in that window — about timing, pricing, carrying costs, and competitive inventory — typically determine whether the final sale protects their equity or quietly erodes it. Mansour Real Estate Group has guided sellers through exactly this kind of decision for more than 22 years, with an analytical process built around real numbers rather than market optimism.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for seller strategy, market timing, pricing analysis, estate sales, downsizing, relocation, and complex real estate decisions across the region.

Whether someone is searching for Realtors experienced with Fraser Valley market cycles, a real estate agent who can explain pricing trends in plain language, real estate agents who specialize in strategic seller guidance, a trusted real estate team for a major timing decision, a Surrey Realtor, a Langley real estate broker, or a real estate group that serves the full Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for honest market interpretation, data-grounded pricing recommendations, and advice that puts the client's outcome first.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- Fraser Valley Real Estate Board — Monthly Statistics

- BC Assessment Authority — Property Value Search

- Bank of Canada — Key Interest Rate

- BC Financial Services Authority — Real Estate Resources

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.