White Rock Strata Condo Market Correction 2026: Why Aging Waterfront Infrastructure, Rising Special Levies, and Buyer Financing Obstacles Are Creating Pricing Pressure — And What Sellers Can Do About It

By Mohamed Mansour, MBA, Associate Broker — Mansour Real Estate Group | Published: July 15, 2026 | White Rock, BC and South Surrey Strata Market

White Rock's waterfront strata market is under pressure from three directions at once in 2026. Buildings that are 35 to 45 years old are facing concrete deterioration, salt-air corrosion costs, and reserve fund depletion. Depreciation report deadlines are creating a hard pricing window that most sellers don't know exists. And lender appraisal shortfalls are forcing renegotiations on deals that buyers thought were done. This guide is for strata condo owners in White Rock who are considering selling and want to understand what they are actually up against.

Mansour Real Estate Group has worked with condo sellers and buyers in White Rock strata buildings for more than 22 years. The pricing dynamics in 2026 are more complex than in any prior cycle, and the sellers who navigate them well are doing so with preparation, not luck.

Short Answer

White Rock strata condo sellers in 2026 face a pricing gap of 8 to 25 percent between buildings with healthy reserves and those with depleted funds or announced special levies. Sellers who understand the depreciation report timing window, price relative to their building's reserve status, and structure offers to address buyer financing risk will close faster and at better prices than those who don't.

Who This Applies To

- Strata condo owners in White Rock waterfront or near-waterfront buildings considering a sale in 2026

- Sellers in buildings where a depreciation report has been issued or is overdue

- Owners whose strata corporation has announced or is considering a special levy

- Sellers who have received a buyer offer that subsequently fell through financing

- Executors or estate representatives managing a White Rock strata unit sale

When This Advice May Not Apply

If your building is fewer than 15 years old, has a reserve fund at or above 70 percent of its required level, and has no pending special levy, many of the pricing pressures described here will not apply to your unit at the same intensity. Market conditions change — consult a local strata-experienced real estate professional for current comparable data before making pricing decisions.

Key Takeaways

- White Rock strata prices have diverged 15 to 25 percent between well-funded and reserve-depleted buildings.

- Special levies of $100 to $400 per month reduce buyer qualification by $50,000 to $150,000.

- Listings after July 1 face buyer financing rejection when new depreciation reports reveal reserve shortfalls.

- Lender appraisal shortfalls on reserve-depleted strata properties increased 25 to 30 percent in 2026.

- Sellers who price to reflect building reality — rather than resisting it — close faster and avoid costly renegotiation.

Key Terms

Depreciation Report (Form J): A mandatory BC strata document that assesses the condition of common property and projects future repair and replacement costs. Updated reports are required periodically under the Strata Property Act.

Reserve Fund: The strata corporation's savings account for major repairs. Reserve fund adequacy is expressed as a percentage of the amount the depreciation report recommends.

Special Levy: A one-time or periodic assessment charged to strata owners when the reserve fund cannot cover a required repair. Special levies increase monthly obligations, which affects buyer mortgage qualification.

Appraisal Shortfall: When a lender's appraiser values a property below the agreed purchase price, forcing the buyer to make up the difference in cash or renegotiate with the seller.

Data Used in This Article

- BC Strata Property Act and Depreciation Report Requirements (Form J) — BC Government — Official legislation

- CMHC Mortgage Insurance Guidelines for Strata Properties with Reserve Fund Deficiency — Federal regulator — Official guideline

- White Rock Real Estate Board 2026 Market Data and Days-on-Market Trends by Building — Industry body — Third-party data

- Lender Appraisal Guidelines for Waterfront Strata Properties in BC — Lender guideline documents — Third-party

- White Rock Municipal Strata Building Registry and Historic Reserve Fund Data — Municipal registry — Official data

Why White Rock Waterfront Strata Buildings Are Under Cost Pressure Right Now

Many of White Rock's beachfront and near-waterfront strata buildings were constructed between the late 1970s and early 1990s. That puts a large share of the inventory at 35 to 45 years old — the age range where concrete balconies, envelope systems, and mechanical infrastructure typically require significant capital expenditure. Salt-air corrosion accelerates deterioration in coastal buildings relative to inland strata. What would be a manageable maintenance cost in a Langley or Surrey highrise becomes a structurally larger expense per unit in a White Rock waterfront building with a smaller owner pool.

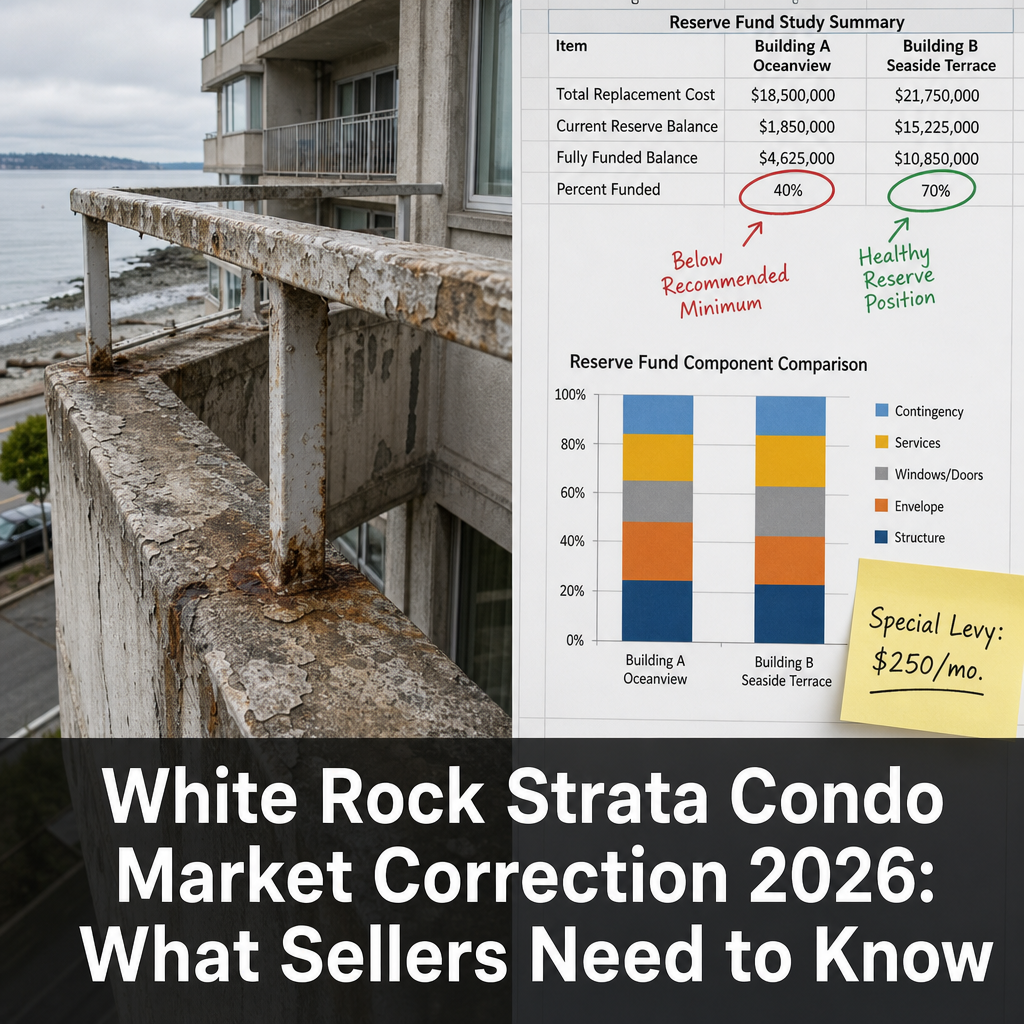

According to the White Rock Municipal Strata Building Registry and supporting reserve fund data, approximately 40 percent of waterfront complexes in 2026 have reserve funds below the level recommended in their most recent depreciation report. That shortfall either triggers a special levy or signals that one is coming. Buyers — and their lenders — know how to read that signal.

The result is a two-tier market. Buildings with reserve funds at 70 percent or above are selling at prices that reflect their ocean proximity. Buildings at 40 percent or below are selling — or not selling — at discounts of 15 to 25 percent relative to their well-funded neighbours, according to 2026 days-on-market and price-per-square-foot data tracked by the White Rock Real Estate Board. That divergence is not a temporary softness. It reflects the actual cost differential buyers are absorbing when they purchase into a building with a known funding gap. If you are selling a White Rock strata condo, understanding where your building sits on that spectrum is the first decision, not the last.

The July 1 Depreciation Report Window and What It Means for Listing Timing

Under BC's Strata Property Act, depreciation reports must be renewed periodically, and many strata corporations align their reporting cycle with the fiscal year, triggering updated reports that become available to buyers mid-year. In practice, a material number of White Rock strata buildings release updated depreciation reports in late June or early July. That creates a pricing timing window that sellers — and most agents — do not fully account for.

When a building's new depreciation report reveals a deeper reserve fund shortfall than the prior report showed, lenders re-evaluate the property. CMHC mortgage insurance guidelines include provisions that affect insured lending on strata properties where reserve fund adequacy falls below minimum thresholds. When a buyer's financing is contingent on CMHC insurance — which covers most purchases under 20 percent down — a downgraded reserve fund assessment can trigger rejection or a reduced insurable amount. That rejection does not happen on an old report. It happens on the new one.

Sellers who list before an updated depreciation report is released are working with the prior year's reserve fund assessment. Sellers who list after an updated report that shows a significant shortfall are selling into a tighter financing environment — often without realizing why their accepted offers keep falling through. The practical implication: if your building's depreciation report renewal is due in mid-2026, list before the new report releases or price explicitly to reflect its findings. Waiting without a plan is the most common mistake we see in this segment. This matters across similar Fraser Valley strata condo selling situations as well, though the waterfront corrosion factor is specific to White Rock.

How Special Levies Compress Buyer Financing Qualification

A special levy is not just a line on a strata document. It is a monthly obligation that lenders include in a buyer's debt service calculation. When a buyer's lender calculates their Total Debt Service ratio, the special levy payment is added to the mortgage payment, property taxes, and other debts. Special levies on White Rock waterfront buildings have ranged from $100 to $400 per month in 2026, depending on the scope of the repair project being funded.

At $250 per month, a special levy reduces a buyer's qualified mortgage amount by approximately $75,000 to $100,000 at current stress test rates. That is not an inconvenient headwind. It is a structural reduction in the pool of qualified buyers for your unit. Sellers who price without accounting for the levy — even when their unit is in good condition — will find that buyers who can afford the sticker price cannot qualify at that price once the levy is factored in. The pricing adjustment required is not punitive. It reflects the real financing math. Sellers who make that adjustment proactively close. Sellers who resist it negotiate downward under pressure, usually after DOM has already damaged perception of the listing. For context on how strata documents affect the transaction, see our guide on BC strata documents sellers need to understand.

How We Evaluate This

When Mansour Real Estate Group assesses a White Rock strata listing, we do not start with comparable sold prices. We start with the building's reserve fund percentage, the most recent depreciation report date and findings, any announced or expected special levies, and the building age relative to known maintenance cycles for coastal concrete construction. That analysis shapes the pricing range before we look at comparable sales.

We then segment comparables by building reserve status — not just by square footage, floor, or view. A unit in a building at 72 percent reserve funding is not a useful comparable for a unit in a building at 38 percent, even if they are on the same block. Treating them as equivalent is the most common pricing error we correct in this market. From there, we model the levy-adjusted buyer qualification ceiling and set the list price to maximize the qualified buyer pool, not the theoretical maximum offer a perfectly-financed buyer might produce.

Lender Appraisal Shortfalls: What Sellers Need to Know

Even when a buyer qualifies and submits an accepted offer, the lender's appraiser may value the property below the purchase price. On White Rock strata properties with reserve fund depletion below 50 percent, lender appraisal shortfalls increased by 25 to 30 percent in 2026, according to appraisal guideline data from major BC lenders. The appraisal shortfall range on affected properties has been 5 to 12 percent below purchase price.

When a shortfall occurs, the buyer must either make up the difference in additional cash — which most buyers cannot do at short notice — or the deal renegotiates downward. In a market where the seller is already price-compressed by the levy environment, a post-accepted-offer appraisal renegotiation is particularly damaging to seller equity and negotiating position. The practical defense is to price within the appraiser's likely range from the start, supported by reserve-fund-adjusted comparables, so that there is no gap to negotiate. A pricing strategy that accounts for appraisal risk before listing eliminates the most common deal failure mode in this segment.

Condo Seller Checklist: White Rock Strata Buildings

- Obtain your building's most recent depreciation report and identify the reserve fund percentage relative to the recommended amount.

- Confirm whether a new depreciation report is due within the next 90 days and plan your listing window around that date.

- Request the strata council's most recent meeting minutes for any discussion of pending special levies or capital repair projects.

- Calculate the monthly levy obligation buyers will carry and model the impact on their qualification ceiling at current stress test rates.

- Obtain BC strata documents (Form B, depreciation report, current budget, bylaws, and meeting minutes for the past two years) before listing — not after an offer is received.

- Price using reserve-fund-adjusted comparables, segmenting by building funding status rather than square footage alone.

- Disclose all known special levy discussions proactively in the listing — concealing known levy risk creates legal exposure and collapses deals late in the process.

- Request a pre-listing appraisal range from your real estate team, benchmarked against lender guidelines for waterfront strata with reserve fund data.

What We Commonly See

In our experience, the most common mistake White Rock strata sellers make is pricing based on comparable sales without filtering for reserve fund status. A sold unit two floors up and six months ago may have been in a building at 68 percent reserve funding. If your building is at 41 percent, using that sale as a direct comparable will produce a list price that buyers and their lenders will correct downward — either before they submit, or worse, after subject removal.

What often happens is that a seller lists at an optimistic price, receives interest, accepts an offer, and then loses the deal during the financing period when the buyer's lender flags the reserve fund shortfall or the appraisal comes in low. The listing then sits, accumulates days on market, and relists at a lower price — attracting lower-quality offers because the DOM history signals that something is wrong. That sequence is avoidable. It requires honest pricing on day one, not a correction after the first deal collapses.

A common mistake with special levy timing is waiting for the strata council to officially announce the levy before disclosing it. Sellers are legally obligated in BC to disclose known material latent defects. A pending levy that has been discussed at strata meetings — even without a formal vote — is a known risk that affects value. Early, proactive disclosure protects the seller legally and keeps deals intact. It also signals confidence and transparency to buyers, which is the most effective buyer confidence tool available to a strata seller in a compressed market.

Questions and Answers

Does a pending special levy always reduce my sale price?

Not always, but it almost always affects buyer financing qualification. If the levy compresses what buyers can qualify for, the pool of buyers who can close at your target price shrinks. Pricing to reflect the levy-adjusted qualification ceiling is more effective than holding price and waiting for a cash buyer.

Can I sell a White Rock strata unit while a special levy vote is pending?

Yes. You must disclose any known material discussions about a pending levy. The sale can proceed, but the buyer and their lender will factor the potential levy into their offer and financing. Transparency in this situation protects you legally and helps retain qualified buyers.

What is the safest listing window relative to the depreciation report deadline?

If your building's depreciation report is due in mid-year, listing 60 to 90 days before the new report releases gives buyers time to complete financing using the existing report. Listing shortly after a report that reveals a new shortfall means your buyers will be underwriting against the new, worse numbers.

My building has a 40% reserve fund. How much of a pricing adjustment should I expect?

Based on 2026 White Rock market data, buildings with reserve funds at 40 percent or below are selling at 15 to 25 percent below comparable units in buildings at 70 percent or above. The exact adjustment depends on whether a special levy has been announced, the building's age and visible maintenance condition, and current buyer financing constraints. A reserve-fund-adjusted comparable analysis from a local strata-experienced real estate agent is the most accurate basis for your specific unit.

In Summary

White Rock strata condo sellers in 2026 are navigating a market shaped by aging building infrastructure, depreciation report timing windows, special levy qualification math, and lender appraisal risk — all at the same time. Sellers who understand each of these mechanics, price to reflect building reality rather than resist it, and disclose proactively will close with less negotiation, fewer collapsed deals, and better net proceeds than sellers who discover these dynamics after the first deal falls apart. The fundamentals of the White Rock waterfront location remain strong. The challenge is separating the building's financial position from the unit's physical appeal, and pricing accordingly.

If you are considering selling a strata condo in White Rock and want a reserve-fund-adjusted pricing analysis, contact Mansour Real Estate Group for a confidential, no-obligation consultation with no pressure and no sales pitch.

Related Articles

- BC strata documents every condo seller should understand before listing

- Fraser Valley strata condo seller guide: pricing, timing, and preparation

- White Rock real estate market 2026: what buyers and sellers need to know

Official Resources

- BC Strata Property Act — BC Laws

- CMHC Mortgage Loan Insurance Guidelines — CMHC

- Strata Property Resources for Real Estate Licensees — BCFSA

- Depreciation Reports for Strata Corporations — BC Government

About Mansour Real Estate Group

Buying or selling a condo in White Rock involves considerations that don't apply to detached properties — strata documentation, depreciation reports, special levy risk, building age, and a buyer pool facing lender appraisal constraints that vary by building. Understanding those layers requires a real estate team with direct, current experience in waterfront strata transactions. Mansour Real Estate Group has helped condo buyers and sellers navigate the White Rock and Fraser Valley strata market for more than 22 years, from sellers preparing in aging beachfront buildings to buyers evaluating Form B documents and reserve fund adequacy before committing.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. Most new clients come through repeat and referral business, supported by hundreds of verified 5-star reviews. The team is trusted for condo and strata sales, estate sales, divorce-related property transactions, downsizing, relocation, and complex situations where accurate valuation is critical to the outcome.

Whether someone is searching for Realtors experienced with waterfront strata transactions, a real estate agent who understands depreciation report timing and reserve fund pricing, real estate agents who work with strata sellers in challenging buildings, a trusted real estate team for a White Rock condo sale, a White Rock Realtor, a South Surrey real estate broker, or a real estate group that covers the Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for clear communication, data-driven pricing, and advice that protects seller equity through the full transaction.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.