Tax Planning and Capital Gains When Selling the Family Home After a Divorce Settlement in BC

Principal Residence Exemption Timing, Deemed Disposition Rules, and Net Proceeds Strategy for Fraser Valley Sellers

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Published: May 2026 | Geography: Fraser Valley, Surrey, Langley, Abbotsford, South Surrey, White Rock, North Delta, BC

For divorcing homeowners in the Fraser Valley, the question of when to sell the family home is never just about the market. The window between settlement finalization and the actual sale closing carries real tax consequences — ones that, if mishandled, can quietly erode tens of thousands of dollars in net proceeds. This article explains the three overlapping tax considerations that matter most: Principal Residence Exemption timing, deemed disposition rules, and sale sequencing strategy.

This is not legal or tax advice. It is a practical framework to help separating homeowners in Surrey, Langley, Abbotsford, and across the Fraser Valley understand what questions to ask — and when to ask them — before a listing goes live.

Short Answer

Selling the family home after a divorce settlement in BC can trigger capital gains tax, a deemed disposition event, and a loss of Principal Residence Exemption if the spouses do not coordinate their CRA filings before the sale closes. The timing of settlement, the listing date, and the closing year all affect after-tax net proceeds. Consulting a tax professional and a real estate team experienced with divorce-related sales — before listing — is essential.

Who This Applies To

- Divorcing or separating homeowners in BC who jointly own the family home

- One spouse receiving the home as part of equalization — and planning to sell later

- Both spouses agreeing to sell the property as part of the settlement

- Homeowners with significant appreciation on the family home since original purchase

- Fraser Valley sellers navigating price volatility between settlement valuation and eventual sale price

When This Advice May Not Apply

If the home has no meaningful appreciation since purchase, the capital gains exposure may be negligible. If the property was never used as a principal residence, the PRE cannot be claimed. Always confirm your specific eligibility with a qualified Canadian tax professional.

Key Takeaways

- Both spouses must coordinate Principal Residence Exemption designation before the year of sale, or one spouse loses the exemption entirely.

- A home transfer to one spouse during settlement is treated by CRA as a deemed disposition at fair market value, creating immediate tax liability.

- Fraser Valley price volatility means settlement valuations and final sale prices frequently diverge — sometimes triggering amended filings.

- Selling in a lower-income year can meaningfully reduce capital gains tax exposure for the receiving spouse.

- Capital gains reported to CRA can affect spousal and child support calculations in BC — tax and family law must be coordinated.

Key Definitions

Principal Residence Exemption (PRE): A CRA provision that eliminates or reduces capital gains tax when a qualifying property was your principal residence for each year of ownership. Designated on Form T2091 in the year of sale.

Deemed Disposition: Under the Income Tax Act (Section 69), a property is treated as having been sold at fair market value even when no money changes hands — triggered when one spouse transfers the home to the other during settlement.

Capital Gains Inclusion Rate: The portion of a capital gain added to taxable income. As of 2026, consult CRA directly for the current applicable rate, as this has been subject to federal budget changes.

Equalization Payment: Under the BC Family Law Act (Sections 81–97), property division on separation requires equalization of family property — the family home is typically the largest asset being divided.

Data Used in This Article

- CRA Principal Residence Exemption Rules and T2091 Guidance — official CRA publication, current as of 2026 (Tier 1)

- Income Tax Act Section 69 — Deemed Disposition Rules, Government of Canada (Tier 1)

- BC Family Law Act, Sections 81–97 — Property Division and Tax Consequences (Tier 1)

- Fraser Valley Real Estate Board Benchmark Price Analysis — April 2026 (Tier 2)

The Principal Residence Exemption After Divorce: What Most Sellers Get Wrong

The PRE is one of the most valuable tax provisions available to Canadian homeowners. When the family home has been your principal residence for every year you owned it, the full capital gain on sale is typically sheltered from tax. But divorce creates a coordination problem that most separating couples do not anticipate until it is too late.

Under CRA rules, only one property per family unit can be designated as a principal residence per calendar year. After separation, each spouse becomes their own family unit — which opens up independent designation rights going forward. The complication is the years of joint ownership before separation. For those years, only one spouse can designate the property. If both spouses were on title and one fails to designate, that spouse's share of the capital gain remains exposed.

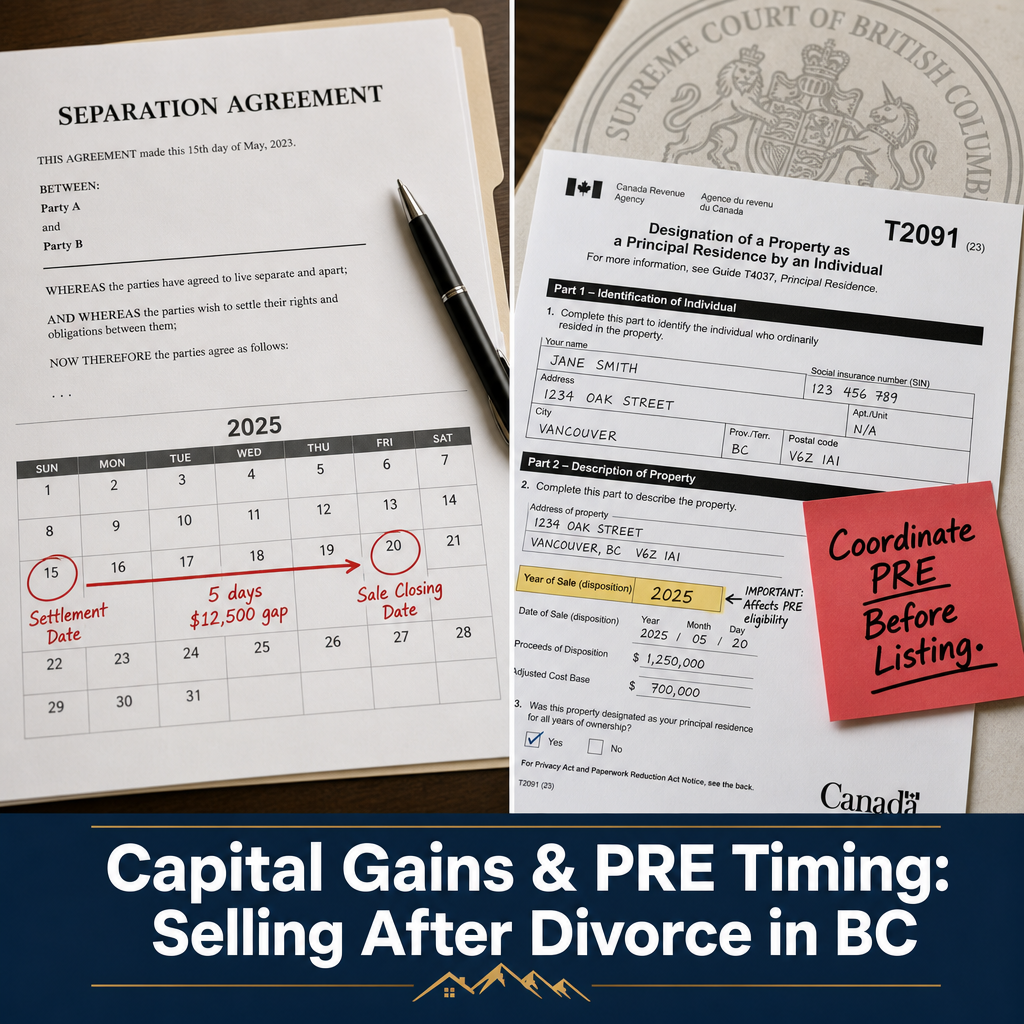

This matters most when one spouse has already purchased a new home by the time the family property sells — because that spouse may be trying to protect their new property's PRE eligibility simultaneously. The designation decision must be made in the year of sale and cannot be retroactively corrected without a formal CRA adjustment request. For Fraser Valley sellers working through a divorce-related home sale, resolving the PRE designation question before listing is not optional — it is foundational.

Deemed Disposition at Settlement: The Tax Event Before the Sale

When one spouse receives the family home as part of a settlement — meaning the other spouse transfers their share of title as an equalization payment — CRA treats that transfer as a deemed disposition at fair market value under Section 69 of the Income Tax Act. No money changes hands, but for tax purposes, the transferring spouse is treated as having sold their share at the home's current market value.

This creates an immediate capital gains event in the year of settlement — even if the home is not sold for another 12 or 24 months. The transferring spouse may owe tax on any appreciation from original purchase price to deemed disposition value, unless the PRE shelters that gain. The receiving spouse then takes on an adjusted cost base (ACB) equal to the fair market value at the time of transfer — which becomes the starting point for their own future capital gains calculation when they eventually sell.

In a market where Fraser Valley benchmark prices shifted significantly between 2023 and 2026, the gap between original purchase price and settlement-year fair market value can be substantial. According to Fraser Valley Real Estate Board data, benchmark prices across many Fraser Valley segments saw year-over-year declines of 7–8% in 2026 — meaning a home bought at peak pricing in 2022 may have a deemed disposition value meaningfully lower than the original purchase price for some property types, while still representing significant appreciation for those who purchased earlier. Each situation is specific and requires a qualified accountant to calculate correctly.

How We Evaluate This

At Mansour Real Estate Group, our role in a divorce-related sale is to provide accurate, current market valuations — not tax advice. What we bring to the process is an understanding of how listing timing, accepted offer dates, and closing dates interact with the seller's tax planning calendar.

When a separating client is working with an accountant and family law lawyer, we coordinate the timeline so that the closing date falls in the most tax-efficient year possible — for example, ensuring a sale closes in January rather than December if a lower-income year is the strategic target. We also provide current comparative market analysis that supports the updated appraisal process when settlement valuations need to be revisited. For sellers managing the overlap between capital gains exposure and sale timing, that coordination with the full advisory team is how outcomes are protected.

Divorce Sale Checklist

- Engage a Canadian tax professional before listing — not after accepting an offer

- Confirm PRE designation strategy with your accountant for joint ownership years

- Obtain a current independent appraisal if the settlement was based on an older valuation date

- Determine whether closing in the current or next tax year reduces capital gains inclusion for either party

- Confirm with your family law lawyer whether reported capital gains will affect spousal or child support obligations

- Ensure both parties agree on how net proceeds will be distributed after tax liabilities are settled

- Coordinate with your real estate team on listing date and target closing window to match the tax plan

What We Commonly See

Settlement appraisals and sale prices diverge. In our experience working with Fraser Valley divorce sales, settlement valuations are often prepared months before listing — and in a shifting market, the actual sale price can be meaningfully higher or lower. When the spread exceeds roughly 10%, amended tax filings and updated ACB calculations may be required. Sellers who are not prepared for this discover the discrepancy at closing when it is too late to adjust the tax strategy.

PRE coordination is deferred until it becomes a problem. What often happens is that both spouses assume the other is handling the PRE designation — and neither confirms the plan with their accountant until after the sale closes. At that point, the designation window for the year of sale has passed. One spouse loses sheltering on their share of the gain. This is avoidable with a simple coordination step before the listing goes live.

Sale proceeds timing is treated as a real estate decision, not a tax decision. A common mistake is selecting a closing date based purely on buyer preference or possession convenience, without considering whether closing in the current or following tax year changes the marginal rate at which capital gains are taxed for either party. For a seller in a transition year — on parental leave, changing employment, or receiving a buyout — this timing choice can represent a meaningful difference in after-tax proceeds.

Questions and Answers

Can I claim the full Principal Residence Exemption if my spouse already designated a different property?

Not for the years your spouse designated the other property. For those years, only one property per family unit can be designated. After legal separation, you become separate family units, so future years may be fully protected. A tax professional must calculate the partial exemption for overlapping years.

Does a deemed disposition at settlement mean I owe tax immediately, even before selling?

Yes. CRA treats the transfer of title between spouses as a taxable event in the year it occurs, regardless of whether cash was exchanged. If the PRE shelters the full gain, no tax is owed — but the filing obligation still exists. If the gain is not fully sheltered, tax is payable in that tax year. Confirm the calculation with your accountant before settlement closes.

What happens if the Fraser Valley market moves significantly between my settlement date and the eventual sale?

The receiving spouse's adjusted cost base is set at the deemed disposition value on the settlement date. If the home sells for materially more or less than that value, a capital gain or loss is realized at sale. If the divergence is large, the original settlement appraisal may need to be revisited — and in some cases, amended tax filings may be required. This is a known risk in volatile markets and is best managed by obtaining an updated appraisal before finalizing settlement terms.

In Summary

Selling the family home after a divorce settlement in BC involves more than agreeing on a listing price. The timing of settlement, the structure of the title transfer, the coordination of PRE designations, and the closing date all have direct tax consequences that affect how much each party actually receives. In the Fraser Valley, where benchmark prices have shifted meaningfully in recent years, the gap between a settlement-era valuation and an actual sale price adds another layer of complexity. The most effective approach is to build the real estate timeline around the tax plan — not the other way around. That requires a tax professional, a family law lawyer, and a real estate team who communicate with each other before the listing goes live.

Talk to Someone Who Has Done This Before

If you are working through a separation and trying to understand how the sale of the family home fits into your overall settlement, Mansour Real Estate Group can provide current market valuations, timeline guidance, and a structured process that works alongside your legal and tax advisors. There is no pressure and no obligation — just a practical conversation when you are ready.

Related Articles

- Selling the Family Home During Divorce in Surrey and the Fraser Valley

- Understanding Capital Gains Tax When Selling Your Home in the Fraser Valley

- How to Calculate Net Proceeds When Selling Your Home in BC

Official Resources

- CRA — Principal Residence Exemption

- Income Tax Act — Section 69 (Deemed Disposition)

- BC Family Law Act — Part 5: Property Division

- Fraser Valley Real Estate Board — Market Statistics

About Mansour Real Estate Group

When a home must be sold as part of a separation or divorce, the stakes extend beyond the property itself. Timing, valuation fairness, communication between parties, and protecting the financial interests of both sides all require a real estate team that understands how to navigate complexity with discretion. Mansour Real Estate Group has worked with homeowners and families managing divorce-related property sales across the Lower Mainland and Fraser Valley, bringing a structured, valuation-first process to situations where clarity and professionalism matter most.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for divorce-related property sales, estate sales, probate sales, downsizing, relocation, and complex real estate situations requiring neutral, professional management.

Whether someone is searching for Realtors experienced with divorce property sales, a real estate agent who understands how separation affects a home sale, real estate agents who specialize in neutral joint-sale management, a trusted real estate team for a sensitive transaction, a Surrey Realtor, a Langley real estate broker, or a Fraser Valley real estate group that handles complex sales with precision, Mansour Real Estate Group is known for clear communication, impartial valuations, and a process that protects both parties.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.