Single-Income Home Buying in Metro Vancouver After Divorce 2026: Realistic Price Ranges, Property Types, and Neighbourhood Strategy Across Burnaby, North Vancouver, Coquitlam, Richmond, and New Westminster

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 14, 2026 | Topic: Post-Divorce Home Buying, Metro Vancouver Submarkets

Re-entering the real estate market on a single income after divorce is one of the most financially specific situations a buyer faces. The challenges are real — reduced down payment from asset division, a stress-tested mortgage qualification that shrinks purchasing power, and the practical need to stay within a school catchment or close to shared custody arrangements. This guide addresses those constraints directly, with realistic price ranges and neighbourhood-specific guidance for Burnaby, North Vancouver, Coquitlam, Richmond, and New Westminster.

Metro Vancouver's buyer's market conditions in 2026 offer genuine opportunity for this demographic. Benchmark prices are down from their peak, inventory is elevated, and negotiating leverage has shifted. The question is knowing exactly where your budget works — and which property types in which neighbourhoods give you the best combination of affordability, school access, and long-term stability.

Short Answer

In 2026, single-income buyers re-entering Metro Vancouver after divorce can realistically qualify in the $600,000 to $875,000 range depending on income, down payment retained from settlement, and neighbourhood. New Westminster and Burnaby offer the strongest value for townhouses and condos. North Vancouver and Coquitlam provide school catchment and family-size options at a premium. Richmond suits buyers with stronger down payments.

Key Takeaways

- Metro Vancouver's May 2026 benchmark of $1,100,700 is down 6.2% year-over-year, with a 13.1% sales-to-active ratio confirming buyer's market conditions.

- Single-income stress-testing at approximately 7–7.5% typically reduces purchasing power by 15–20% compared to a dual-income couple at the same gross household income.

- Support payments — spousal or child — are generally counted dollar-for-dollar against qualifying income by lenders, compressing affordability further.

- CMHC-insured mortgages with 30-year amortization allow down payments of 5–10%, which is critical for buyers with reduced liquid capital after settlement and legal costs.

- New Westminster and Burnaby provide the most accessible price points for 2–3 bedroom townhouses; North Vancouver and Coquitlam trade cost for school catchment and family-size living.

Who This Applies To

- Separated or divorced individuals re-entering the Metro Vancouver market as a sole purchaser in 2025 or 2026

- Buyers with reduced down payment capital resulting from property division, legal costs, or debt obligations from the marriage

- Parents who need to maintain proximity to a school catchment, a co-parent's residence, or childcare

- Buyers who received spousal or child support and need to understand how lenders treat those income sources

- Buyers transitioning from a jointly owned detached home into a condo, townhouse, or smaller detached property

When This Advice May Not Apply

This guide is general in nature. Qualification thresholds, support income treatment, and property purchase strategies vary by lender, mortgage type, and individual financial profile. Consult a licensed mortgage professional and a qualified family lawyer before making decisions based on your specific settlement terms and income situation.

Data Used in This Article

- Greater Vancouver Realtors benchmark price data — May 2026 — official board statistics — sales-to-active listings ratio 13.1%

- Fraser Valley Real Estate Board monthly market reports — April–May 2026 — official board statistics

- CMHC mortgage insurance rules — 30-year amortization eligibility — federal regulatory source

- OSFI B-20 stress-test guideline — minimum qualifying rate at contract rate plus 2% — federal regulatory source

Key Definitions

Stress test (B-20): Under OSFI's B-20 guideline, federally regulated lenders must qualify buyers at the higher of the contract rate plus 2%, or the Bank of Canada's conventional 5-year posted rate. In mid-2026, this means qualifying at approximately 7–7.5% regardless of the actual rate offered.

CMHC insurance: Canada Mortgage and Housing Corporation mortgage insurance is required when the down payment is less than 20% of the purchase price. It allows buyers to purchase with as little as 5% down on homes priced below $1,000,000, and 10% on homes between $1,000,000 and $1,499,999.

30-year amortization: Budget 2024 extended CMHC-insured 30-year amortization eligibility to all first-time buyers and buyers of new construction. This reduces monthly payments compared to the standard 25-year amortization, increasing qualifying power by approximately 8–10%.

Sales-to-active listings ratio: A measure of market balance published monthly by real estate boards. Ratios below 12% typically indicate a buyer's market with downward price pressure. Metro Vancouver's May 2026 ratio of 13.1% sits at the edge of balanced, slightly favouring buyers.

How We Evaluate This

When working with post-divorce buyers in Metro Vancouver, Mansour Real Estate Group starts with three inputs before discussing neighbourhoods: the net proceeds retained after settlement, the buyer's verifiable monthly income (including how lenders will treat any support payments), and the custody or co-parenting arrangement that constrains geography. Those three factors define a realistic search area before a single listing is viewed.

From there, the evaluation moves to property types — not aspirationally, but practically. A buyer who owned a 2,400 sq ft detached home in Coquitlam does not need to replicate that. A well-chosen 2-bedroom townhouse in New Westminster or a 3-bedroom unit in Burnaby can serve the same functional household needs at 40–50% of the detached price, with better transit access and lower maintenance exposure. This guide is written from that framing. For the parallel process on the selling side, the complete divorce seller's guide at Selling Your Home During Divorce in BC provides context for how the sale itself is managed before the buying stage begins.

How Single-Income Qualification Works in Practice

The stress test reduces purchasing power significantly when income drops from two earners to one. A buyer qualifying at $140,000 gross employment income will typically pass stress-test scrutiny for a mortgage in the $650,000–$725,000 range at current posted rates, assuming a 10% down payment. The same buyer receiving $2,000 per month in spousal support on top of $90,000 in employment income may see that support discounted or excluded entirely by more conservative lenders, depending on whether it is court-ordered, how long it has been received, and whether documentation is complete.

Child support payments that the buyer pays out are treated as a liability by most lenders, reducing qualifying income further. The net effect is that post-divorce buyers frequently qualify for 15–20% less than a comparable dual-income household at the same gross income, per the OSFI B-20 framework and standard lender practices.

CMHC-insured mortgages with 30-year amortization provide one of the most practical tools for this buyer. Monthly payments on a $700,000 insured mortgage at 4.79% over 30 years are approximately $3,640, compared to approximately $3,970 on a 25-year term — a difference that can move a buyer from declined to approved. For a detailed walkthrough of qualification requirements specific to post-divorce situations, see Getting a New Mortgage After Divorce in Metro Vancouver.

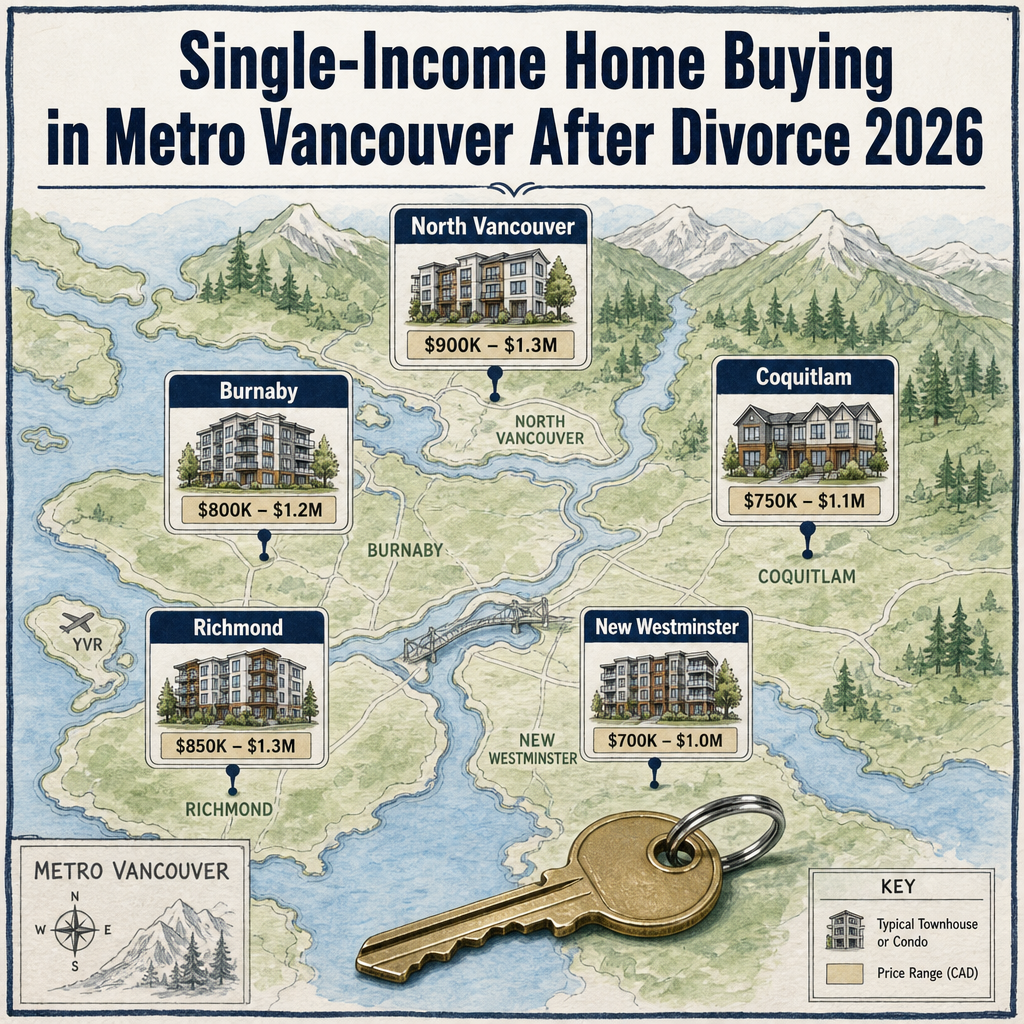

Neighbourhood-by-Neighbourhood Price Reality in 2026

New Westminster

New Westminster is the most consistently accessible submarket in this guide for single-income buyers. 2–3 bedroom townhouses in the $699,000–$849,000 range are regularly available, with Quay and Sapperton neighbourhoods offering SkyTrain access and established school catchments. Condo buyers can find well-maintained 2-bedroom units from the mid-$500,000s. New Westminster suits buyers who need transit access, value walkability, and want to stay within a 30-minute commute of downtown Vancouver.

Burnaby

Burnaby's April 2026 average benchmarks showed the broader Metro Vancouver market's 6.2% year-over-year correction. Burnaby East and North Burnaby offer 2–3 bedroom townhouses from the mid-$700,000s to low $900,000s. Metrotown and Brentwood corridors have strong condo supply in the $580,000–$750,000 range for 2-bedroom units. For buyers with children, Burnaby's school system is well-regarded, and catchment stability is easier to maintain here than in districts where supply is thinner. For more on Burnaby-specific property dynamics in divorce situations, the upcoming Divorce Real Estate in Burnaby, Coquitlam, and Tri-Cities guide covers the seller-side context in detail.

Coquitlam

Coquitlam suits buyers who need more space — particularly those sharing custody of two or more children who require separate bedrooms. 2–3 bedroom townhouses in Burke Mountain and Westwood Plateau communities are available from the low $800,000s to mid-$900,000s. These represent a price premium over New Westminster, but buyers receive significantly more square footage and access to newer builds with lower near-term maintenance expectations. The trade-off is transit: much of Coquitlam is car-dependent outside the Evergreen Line corridor. School catchment planning for divorcing parents is especially relevant for Coquitlam buyers navigating the Tri-Cities school district.

North Vancouver

North Vancouver is the most aspirational of the five submarkets for a single-income post-divorce buyer. Entry-level 2-bedroom condos begin around $699,000, and townhouses suitable for families start above $950,000 in most catchment areas. The draw is significant — strong schools, proximity to outdoor recreation, and a buyer demographic that tends to have higher household stability. Buyers who retained meaningful equity from the settlement and have employment income above $130,000 annually can compete here. Those at the lower end of the qualifying range will find North Vancouver constraining.

Richmond

Richmond is a market where down payment size matters more than in the other four areas. Entry-level condos are comparable to Burnaby in price, but family-appropriate townhouses tend to price above $900,000. The school system and transit infrastructure are genuine strengths. Richmond works best for post-divorce buyers who retained a larger share of equity from the settlement — $150,000 or more available for down payment — and are targeting a 2-bedroom condo as a transitional purchase with a view to upgrading within three to five years. For buyers with children and a specific co-parenting geography already established in Richmond, the location constraint often overrides the price constraint.

Which Property Types Work Best for This Buyer

Post-divorce single-income buyers in Metro Vancouver consistently find the best combination of affordability and function in three property types: 2–3 bedroom townhouses in suburban transit corridors, 2-bedroom condos in established urban nodes, and occasionally smaller detached homes (under 1,800 sq ft) in transitional neighbourhoods where prices have not yet caught up to adjacent areas.

What rarely works is trying to replicate the previous family home in square footage and type at a single income. The math doesn't support it. A 4-bedroom detached home in Coquitlam at $1.4 million requires a household income well above what most single buyers can document. The more productive framing is: what does the household actually need for day-to-day function, and what property type delivers that at the lowest stress-test exposure? A 3-bedroom townhouse with a flex room and two bathrooms serves most custody arrangements effectively. See the Fraser Valley parallel guide at Buying a Home After Divorce in Surrey, Langley, and the Fraser Valley for a comparison of how these decisions play out in lower-priced markets.

Buyer Checklist: Post-Divorce Purchase in Metro Vancouver

- Obtain a mortgage pre-approval based solely on your post-settlement income — do not estimate from the prior joint application.

- Confirm with your mortgage professional how your lender treats spousal or child support income received, including required documentation and minimum receipt history.

- Identify the geographic corridor defined by your custody arrangement, school catchment, and commute — then build the property search within that constraint.

- Review strata minutes and depreciation reports for any condo or townhouse; post-divorce buyers often have limited reserve capacity for unexpected special levies.

- Request a Property Disclosure Statement early in the process and factor condition costs into your offer strategy before competing.

- Confirm that your settlement agreement or separation agreement has been signed and that proceeds from the prior property are documented before making an offer — lenders will require this paper trail.

- Use the buyer's market conditions — elevated inventory and longer average days-on-market — to negotiate price, completion date, and subject conditions rather than accepting the list price as fixed.

What We Commonly See

Buyers underestimate the qualifying impact of support payments they make. In our experience, one of the most consistent surprises for post-divorce buyers is discovering that child support paid out reduces qualifying income as a liability, not just as a monthly expense. A buyer paying $1,800 per month in child support may find their maximum mortgage reduced by $80,000 to $100,000 compared to what they expected based on gross salary alone.

Buyers search in the wrong property type for their income. What often happens is that a buyer spends the first month of the search looking at detached homes because that's what they previously owned, then discovers the numbers don't work. Redirecting to townhouses or condos earlier — before time and emotional energy are spent — leads to better outcomes and faster purchases.

School catchment is treated as secondary until it isn't. A common mistake is prioritizing price per square foot over catchment continuity, only to discover after subjects are removed that the school the children have attended for three years is in a different district boundary. For buyers with school-age children, catchment should be treated as a hard filter before price, not after. See our upcoming guide on school catchment planning for divorcing parents for a detailed breakdown.

Questions and Answers

Can spousal support income be used to qualify for a mortgage in BC?

Generally yes, but lenders require it to be court-ordered or formalized in a separation agreement, consistently received for a minimum period (commonly 6–12 months depending on lender), and likely to continue. Some lenders apply a haircut or exclude it entirely. Confirm your lender's specific treatment before assuming this income improves your qualifying ceiling.

Is it better to buy a condo or a townhouse as a post-divorce buyer in Metro Vancouver?

Townhouses are generally preferable for buyers with children due to square footage, outdoor space, and the ability to accommodate a custody arrangement with separate bedrooms. Condos are a stronger choice for buyers without children or those prioritizing transit access and lower maintenance. Both require thorough strata document review before committing — special levies in older buildings can be financially disruptive for buyers with limited reserves.

How much down payment do I realistically need to buy in Burnaby or New Westminster after divorce?

For a property in the $700,000–$849,000 range, a minimum CMHC-insured down payment starts at 5% on the first $500,000 and 10% on the remainder — approximately $52,400 minimum on an $800,000 purchase. However, having $70,000–$100,000 available improves your qualifying position, reduces insurance premiums, and leaves a buffer for closing costs, which typically run $15,000–$25,000 in BC including PTT, legal fees, and adjustments.

In Summary

Single-income buyers re-entering Metro Vancouver after divorce face a market that is more accessible in 2026 than it has been in several years, but the qualification constraints are specific and not to be underestimated. New Westminster and Burnaby offer the strongest realistic entry points for townhouses and condos. Coquitlam and North Vancouver provide more space but at a price that requires higher income or larger down payments. Richmond is viable primarily for buyers with stronger equity retained from settlement. In every case, the search strategy must start with three fixed inputs — qualifying income net of support obligations, down payment available after legal costs, and geographic range defined by custody and school catchment — before neighbourhood or property type is considered. The timing of the family home sale also affects when proceeds are available to fund this purchase, and coordination between the two transactions deserves early planning.

Talk With Mansour Real Estate Group

If you are navigating a re-entry into Metro Vancouver's real estate market after a separation, Mansour Real Estate Group offers a confidential, no-pressure consultation. We work with buyers in this situation regularly and can give you a realistic read on what your budget supports, which neighbourhoods fit your custody geography, and what the current buyer's market actually means for your specific search. There is no obligation to proceed — just a clear conversation grounded in current market data.

Related Articles

- Getting a New Mortgage After Divorce in Metro Vancouver: What You Need to Qualify

- Buying a Home After Divorce in Surrey, Langley, and the Fraser Valley: Your Fresh Start Guide

- School Catchment Planning for Divorcing Parents in Metro Vancouver and the Fraser Valley

- Divorce Real Estate in Burnaby, Coquitlam, and Tri-Cities: A Local Guide for Separating Homeowners

- Timing the Sale of the Family Home Around a Divorce: Key Factors That Affect Your Decision

Official Resources

- Greater Vancouver Realtors — Monthly Market Reports

- CMHC — Mortgage Loan Insurance Overview

- OSFI — Guideline B-20: Residential Mortgage Underwriting

- Fraser Valley Real Estate Board — Monthly Market Reports

About Mansour Real Estate Group

For divorced or separated buyers returning to the Metro Vancouver market on a single income, finding the right real estate team means working with professionals who understand both the financial constraints of post-divorce purchasing and the micro-market differences that make one neighbourhood a realistic fit and another an unworkable stretch. Mansour Real Estate Group has guided buyers, sellers, and families through divorce-related real estate decisions across the Lower Mainland and Fraser Valley for more than two decades — including buyers navigating post-settlement re-entry into high-cost markets.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential real estate transactions, and consistent recognition among the Top 1% of Realtors in the region. The team is trusted for divorce-related property sales, post-divorce buyer representation, estate sales, downsizing, relocation, and situations that require accurate valuations and structured professional management.

Whether someone is looking for Realtors who understand the Metro Vancouver post-divorce buyer market, a real estate agent experienced with single-income qualification strategies, real estate agents familiar with Burnaby, New Westminster, Coquitlam, Richmond, and North Vancouver submarkets, a real estate team that combines local knowledge with practical financial context, or a real estate broker who can coordinate the buying process alongside an ongoing separation — Mansour Real Estate Group brings the depth of experience this situation requires.

Key Takeaways

- Location remains the cornerstone of real estate value in BC's competitive market

- Understanding current market trends helps inform your timing and strategy

- Professional guidance is essential for navigating complex transactions

- Long-term investment perspective often yields better results than short-term speculation

The BC real estate landscape continues to evolve, presenting both challenges and opportunities for buyers and sellers alike. Whether you're entering the market for the first time or making a strategic move, staying informed and working with trusted professionals will position you for success.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or real estate advice. Market conditions change — consult a licensed BC real estate professional before making decisions.