Rebuilding Your Home-Buying Strategy After Divorce Settlement: Single-Income Mortgage Qualification, Affordability Assessment Using Settlement Proceeds, and Strategic Neighbourhood Selection in Metro Vancouver and Fraser Valley 2026

By Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group | Fraser Valley and Metro Vancouver | Published: July 15, 2025 | Topic: Post-Divorce Home Buying, Single-Income Mortgage Qualification, BC 2026

For many people in Metro Vancouver and the Fraser Valley, the end of a marriage also marks the beginning of a new and unfamiliar real estate decision. You may have significant equity from the sale of the matrimonial home, but equity and purchasing power are not the same thing. On a single income, facing today's stress test rules and the added weight of support payment obligations, the gap between what you have and what you can qualify for often surprises people who have owned real estate for years.

This article is for recently separated or divorced homebuyers who are re-entering the market in 2026, ready to buy but uncertain about what they can realistically qualify for and where their money goes furthest. It draws on mortgage qualification realities, BC-specific rules, and neighbourhood-level market data relevant to Surrey, Langley, North Delta, and surrounding Fraser Valley communities.

Short Answer

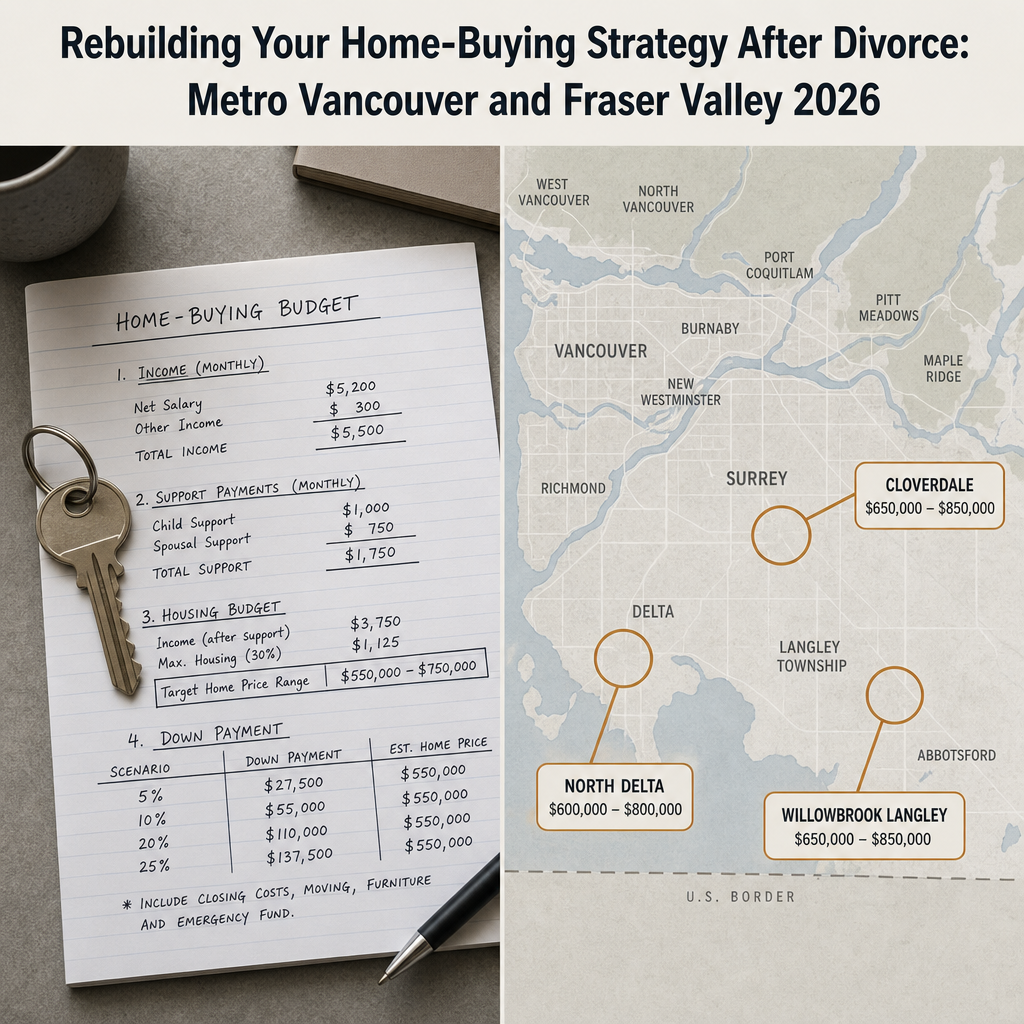

Divorced buyers in Metro Vancouver and the Fraser Valley in 2026 typically qualify for 15 to 30 percent less mortgage than their pre-divorce household income suggested, even with substantial settlement proceeds as a down payment. Support payment obligations reduce qualifying power significantly. Strategic neighbourhood selection — particularly in Cloverdale, Willowbrook Langley, and North Delta — can close the gap between qualification limit and livable housing without sacrificing long-term equity recovery.

Key Takeaways

- Settlement proceeds strengthen your down payment but do not count as income for mortgage qualification purposes.

- Spousal or child support payments can reduce your maximum mortgage by $75,000 to $150,000 depending on the monthly obligation and lender policy.

- A 30-year amortization with CMHC insurance can add $150,000 to $250,000 of purchasing power for single-income buyers at the cost of insurance premiums.

- Cloverdale, Willowbrook Langley, and North Delta offer 20 to 30 percent lower entry prices than premium Fraser Valley neighbourhoods, with faster days on market.

- Your qualification number and your budget are two different things — carrying costs, strata fees, and support obligations all affect what you can safely sustain.

Who This Applies To

- Recently divorced individuals who received settlement proceeds from the sale of a matrimonial home in BC

- Single-income buyers re-entering the market after separation with equity but reduced qualifying power

- Divorced parents balancing housing stability, school catchments, and monthly support obligations

- People evaluating whether to buy in Metro Vancouver or shift to more affordable Fraser Valley communities

When This Advice May Not Apply

This article addresses typical single-employment-income buyers with standard settlement proceeds. If you receive spousal support as income, some lenders may count it partially toward qualifying — consult a licensed mortgage broker about your specific documentation. Buyers with self-employment income, investment income, or non-traditional income structures will face additional qualification layers not fully covered here.

Data Used in This Article

- BCFSA Mortgage Broker Standards — income treatment guidelines for settlement proceeds, 2026

- CMHC Mortgage Insurance Qualification Rules — non-traditional income and insured mortgage parameters

- Bank of Canada stress test rules — single-income applicants with support obligations

- Canadian Mortgage Trends Q1 2026 — divorced buyer purchasing power analysis (third-party industry analysis)

- Mansour Real Estate Group 2026 post-divorce buyer neighbourhood selection observations (internal, professional)

How We Evaluate This

When working with divorced buyers, we start with a realistic affordability picture before we look at any property. That means reviewing the settlement agreement, understanding the support obligation structure, and working alongside the buyer's mortgage broker to establish a confirmed qualification range — not an estimate. Only then does neighbourhood selection begin in earnest.

We look at carrying cost exposure alongside the purchase price. A townhome in Cloverdale at $720,000 may carry more comfortably than a detached home at $850,000 in Fleetwood when strata fees, tax, and support payments are all factored together. Our approach is to build a clear monthly cash-flow picture before recommending a direction, not after an offer is accepted.

How Settlement Proceeds Affect Your Mortgage Qualification

Settlement proceeds from the sale of a matrimonial home — your share of the net equity — count as a down payment. They reduce the mortgage you need to carry, which lowers your debt-servicing ratios. That part works in your favour.

What they do not do is count as income. According to CMHC mortgage insurance qualification rules, a lump-sum settlement is not recurring income and cannot be used to increase your qualifying mortgage ceiling the way a salary or verified rental income can. If your employment income supports a maximum mortgage of $500,000 and you have $300,000 in settlement proceeds as a down payment, your purchasing power is $800,000 — but only if your debt-servicing ratios support that purchase at the stress test rate.

The stress test as of 2026 requires qualifying at the greater of your contract rate plus 2 percent or 5.25 percent, whichever is higher. On a single income, that ceiling comes down faster than most buyers expect. A household that qualified for $1.1 million as a two-income family may find the single-income buyer qualifies for $550,000 to $650,000 in mortgage — a meaningful difference regardless of how much equity they bring to the table.

Before beginning your property search, confirm your qualification ceiling with a licensed mortgage broker who has experience with post-divorce files. The numbers in your separation agreement, particularly any ongoing support obligations, will affect what lenders will approve. Understanding how the mortgage changes when couples separate in BC is an important first step before approaching any lender.

How Support Payment Obligations Reduce Purchasing Power

If you are paying spousal or child support, lenders treat that obligation as a recurring liability — similar to how they treat an existing car loan or line of credit. According to Bank of Canada stress test guidelines and BCFSA mortgage broker standards, support payment obligations are factored into your Total Debt Service (TDS) ratio alongside your proposed mortgage payment, property taxes, heating costs, and any strata fees.

At typical support levels of $1,500 to $3,000 per month, the impact on maximum mortgage qualification ranges from approximately $75,000 to $150,000, depending on your income level and the lender's calculation method. Some lenders apply a 15 percent reduction to qualifying income; others add the full monthly obligation to your debt load. Per Canadian Mortgage Trends Q1 2026 analysis, divorced buyers paying support are seeing the most significant qualification gaps relative to their equity positions.

You will need to provide your lender with a copy of your separation agreement or obligation letter confirming the support amount and duration. Lenders require this documentation to assess the ongoing liability correctly.

If you are the support recipient rather than the payor, some lenders will count consistent, documented spousal or child support payments as qualifying income — typically if payments have been received for at least 12 months and the obligation has a defined duration. Ask your mortgage broker specifically about how your lender treats this, as policies vary.

CMHC Insurance and 30-Year Amortizations as a Qualification Strategy

For divorced single-income buyers whose qualification ceiling falls short of what they need to purchase a suitable home, a 30-year amortization combined with CMHC or Sagen mortgage insurance is one of the most practical tools available in 2026.

Insured mortgages require a minimum down payment of 5 percent (for homes under $500,000) or a sliding scale up to $999,999, with CMHC insurance not available on purchase prices of $1 million or more. The insurance premium ranges from 2.8 to 4.0 percent of the mortgage amount and is typically added to the mortgage balance rather than paid upfront. On a $600,000 mortgage, the CMHC premium at 4.0 percent adds approximately $24,000 to the mortgage — real cost, but it enables access to a purchase that might otherwise fall outside reach.

Extended 30-year amortizations lower the required monthly payment, which improves your TDS ratio and can expand your maximum qualifying mortgage by $150,000 to $250,000 compared to a 25-year amortization at the same income level. For buyers who have meaningful equity but constrained income, this is a bridge strategy — you accept higher total interest costs in exchange for housing stability now, with the option to accelerate payments or refinance as income grows or support obligations reduce over time. Whether to sell or hold the family home after divorce often informs how much equity is available for this next step.

Strategic Neighbourhood Selection: Where Divorced Buyers Are Buying in 2026

In Metro Vancouver, benchmark prices for entry-level detached homes remain well above what most single-income buyers can qualify for, particularly in West Vancouver, North Vancouver, Vancouver Westside, and Richmond. For divorced buyers with $200,000 to $400,000 in settlement proceeds and single employment income, the Fraser Valley offers a realistic re-entry point.

Based on observations from our work with post-divorce buyers across the region, three neighbourhoods are drawing consistent interest in 2026:

- Cloverdale, Surrey: Townhomes and older detached homes in the $650,000 to $850,000 range. Strong school options, established community feel, and 20 to 25 percent lower pricing than comparable South Surrey properties. Days on market tend to be moderate, giving buyers negotiating room without extended carrying-cost exposure during the search period.

- Willowbrook, Langley: A practical mid-point between newer Willoughby townhomes and older detached stock. Entry townhomes in the $580,000 to $720,000 range, with walkable amenities, transit access, and a buyer pool that keeps DOM reasonable. For divorced parents managing custody schedules, the central Langley location simplifies logistics. See our upcoming guide to affordable post-divorce housing options in the Fraser Valley for a detailed area comparison.

- North Delta: Often overlooked but offering some of the strongest value in Metro Vancouver's eastern edge. Detached homes in the $900,000 to $1.1 million range that would cost $1.3 million or more in comparable Burnaby or New Westminster locations. Faster DOM than premium markets and good proximity to Delta and Surrey employment corridors. For families considering school catchments as part of their decision, our upcoming article on children, school catchments, and divorce home moves covers the planning considerations in detail. Buyers interested in the broader Richmond and Delta area will also find relevant context in our guide to divorce real estate in Richmond and Delta.

The pattern we see consistently is that divorced buyers who try to stay in premium neighbourhoods at the edge of their qualification ceiling create ongoing financial stress. Buyers who step into a slightly more affordable market, stabilize their carrying costs, and build equity over three to five years tend to recover their financial footing faster — and often return to their preferred neighbourhood from a stronger position.

Property Type Considerations for Post-Divorce Buyers

Townhomes are the most common entry point for divorced single-income buyers in the Fraser Valley in 2026. They offer more space than condos, lower maintenance responsibility than detached homes, and purchase prices that are typically 20 to 35 percent below comparable detached properties in the same neighbourhood.

The trade-off is strata fees — typically $300 to $600 per month for a Fraser Valley townhome — which count as a debt obligation in your TDS calculation. Before committing to a strata property, confirm that the strata fees are factored into your qualification number and that your broker has reviewed the building's depreciation report and contingency reserve fund. A strata with deferred maintenance and a thin reserve fund can create significant unplanned costs at exactly the wrong time. Our broader guide to strata property considerations during divorce covers the documentation side in detail.

Post-Divorce Home Buyer Checklist

- Obtain a certified copy of your final separation agreement documenting settlement proceeds and support obligations before approaching any lender.

- Consult a licensed mortgage broker with post-divorce file experience to establish your confirmed qualification ceiling, not an estimate.

- Ask your broker to model both 25-year and 30-year amortization scenarios so you can compare purchasing power against total interest cost.

- Build a monthly carrying-cost budget that includes mortgage payment, property taxes, strata fees (if applicable), heating, and any ongoing support obligations before selecting a price range.

- Identify your non-negotiable location priorities — school catchment, commute corridor, or proximity to co-parenting logistics — before narrowing neighbourhoods.

- Compare at least two or three neighbourhoods at different price points to understand the trade-offs between community, property type, and monthly carrying cost.

- Review strata documents — Form B, depreciation report, contingency reserve fund status — before making any offer on a strata property.

What We Commonly See

Buyers overestimate purchasing power based on their equity position. In our experience, the most common mistake divorced buyers make is calculating maximum purchase price by adding settlement proceeds to a rough mortgage estimate without accounting for the stress test on single income and the TDS impact of support payments. The actual qualifying ceiling is often $100,000 to $200,000 lower than the initial mental estimate.

Neighbourhood loyalty delays the purchase. What often happens is that buyers spend months searching in the neighbourhood where the matrimonial home was located, find nothing within their range, and eventually pivot to a more affordable area — but having lost three to six months of market time and accumulated carrying costs during renting. Starting the neighbourhood search with clear price-range parameters, not emotional geography, usually produces a better outcome.

Support obligations are disclosed late in the mortgage process. A common mistake is not mentioning ongoing support payments until the lender's conditions come back, at which point the file needs to be restructured or a different lender found. Disclosure upfront — even if the amount feels manageable — is always the correct approach.

Questions and Answers

Can my divorce settlement proceeds be used as the entire down payment?

Yes. Settlement proceeds from a matrimonial home sale are an acceptable source of down payment in BC. Lenders and CMHC will typically require documentation confirming the source — usually the settlement agreement and a record of fund receipt. There is no minimum employment income requirement tied specifically to the down payment source, but your income must still support the mortgage at the stress test rate.

How does a lender calculate the impact of my $2,000 per month child support payment on my mortgage?

Most lenders add the full monthly support obligation to your debt load when calculating your Total Debt Service ratio. At $2,000 per month, this is equivalent to carrying roughly a $120,000 to $140,000 additional debt in terms of its effect on your qualifying mortgage ceiling, depending on the lender's internal calculation method and your income level.

Does CMHC insurance cover homes over $1 million in BC?

No. CMHC and Sagen mortgage insurance is not available for properties with a purchase price of $1,000,000 or more. Buyers purchasing above that threshold require a conventional mortgage with a minimum 20 percent down payment. For most single-income divorced buyers in the Fraser Valley targeting the $600,000 to $900,000 range, insured mortgage options remain available and represent a meaningful qualification advantage.

In Summary

Re-entering the housing market after divorce in Metro Vancouver and the Fraser Valley in 2026 requires a clear-eyed look at what single-income qualification actually produces — separate from what your settlement equity suggests. Support obligations reduce qualifying power in ways many buyers underestimate. A 30-year amortization with CMHC insurance can bridge part of that gap at a defined cost. Neighbourhoods like Cloverdale, Willowbrook Langley, and North Delta offer realistic entry points that support both housing stability and equity recovery without forcing a qualification ceiling that strains monthly finances. The buyers who navigate this transition most effectively are the ones who start with confirmed numbers, not optimistic estimates.

Talk to Mansour Real Estate Group

If you are ready to start your post-divorce home search and want a realistic assessment of what you can access in the Fraser Valley or Metro Vancouver, Mansour Real Estate Group offers an initial conversation with no obligation. We work alongside your mortgage broker and lawyer — not around them — to help you buy with clarity.

Related Articles

- Should You Sell or Keep the House After Divorce in Metro Vancouver? A Decision Framework

- What Happens to the Mortgage When Couples Separate in BC? A Practical Guide

- Finding a Home After Divorce in the Fraser Valley: Affordable Options for Separated Families in 2026

- Children, School Catchments, and Divorce Home Sales in Metro Vancouver: Planning Your Move Around the Kids

- Divorce Real Estate in Richmond and Delta: What Separating Couples Need to Know About These Markets

About Mansour Real Estate Group

For divorced individuals re-entering the housing market, the path from settlement proceeds to a confirmed purchase requires a real estate team that understands both the financial constraints and the life-event context. Mansour Real Estate Group has worked with post-divorce homebuyers across the Lower Mainland and Fraser Valley — helping them assess realistic affordability, select neighbourhoods that fit their new financial reality, and move from settlement to purchase with clarity and confidence.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for divorce-related property sales, post-separation purchases, estate sales, downsizing, relocation, and complex real estate situations that require structured, professional guidance.

Whether someone is searching for Realtors who understand how divorce affects purchasing power, a real estate agent who works alongside mortgage brokers and family lawyers, real estate agents familiar with post-separation buyer timelines, a trusted real estate team for a first solo purchase, a Surrey real estate broker, a Langley Realtor, or a real estate group serving the Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for clear communication, accurate neighbourhood-level guidance, and a process grounded in local market knowledge.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- BC Financial Services Authority (BCFSA) — Mortgage Broker Standards

- CMHC — Mortgage Insurance Qualification Rules

- Bank of Canada — Mortgage Stress Test Guidelines

- BC Laws — Family Law Act (SBC 2011, c 25)

Final Thoughts

Whether you're a first-time buyer, seasoned investor, or homeowner looking to understand the current landscape, knowledge is your greatest asset in real estate. The BC market continues to evolve, presenting both challenges and opportunities for those prepared to navigate it thoughtfully.

Take the time to educate yourself, connect with trusted professionals, and make decisions aligned with your long-term goals. Your real estate journey deserves careful consideration and expert guidance every step of the way.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or real estate advice. Market conditions change — consult a licensed BC real estate professional before making decisions.