Rebuilding Your Financial Foundation After Divorce Settlement: Tax Planning, Mortgage Qualification, and Strategic Home-Purchase Timing for Fraser Valley Buyers in 2026

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2026 | Topic: Post-Divorce Home Buying · Mortgage Qualification · Fraser Valley Buyer Strategy

For homeowners whose settlements have recently been finalized, the next question arrives quickly: when do I buy again, and can I actually qualify on my own? This article is for Fraser Valley buyers navigating that transition — people who have received settlement proceeds, are managing support obligations, and are trying to understand the financial mechanics before they start shopping.

The decisions made in the first six to twelve months after settlement typically determine both mortgage eligibility and how much down-payment capital is preserved. Getting those decisions in the right order matters more than most buyers realize going in.

Short Answer

Post-divorce buyers in the Fraser Valley can qualify for single-income mortgages in 2026, but only when credit recovery, support obligation documentation, and principal residence exemption timing are managed correctly. Entry-level detached and townhome prices in Langley, Abbotsford, and Walnut Grove are $100,000 to $200,000 below Metro Vancouver benchmarks, making single-income qualification realistic when buyers understand the stress test mechanics and plan the sequence carefully.

Key Takeaways

- Spousal and child support obligations reduce maximum mortgage qualification — sometimes by $250,000 or more on a $2,000 monthly obligation.

- Credit score recovery after joint account separation typically takes six to twelve months before qualifying for standard insured rates.

- Principal Residence Exemption timing on settlement transfers can preserve capital gains deferral and protect down-payment funds.

- CMHC's 30-year amortization option for qualified buyers improves monthly affordability, but documentation timing can cause eligible buyers to miss the window.

- Fraser Valley entry-level pricing gives single-income buyers a realistic qualification range that Metro Vancouver does not offer at comparable income levels.

Who This Applies To

- Homeowners whose divorce or separation settlement has been finalized and who received equity proceeds from a matrimonial home sale or buyout

- Single-income buyers re-entering the Fraser Valley market after separation, with incomes between $75,000 and $110,000

- Buyers managing ongoing spousal or child support obligations that affect their debt service ratios

- Settlement-finalized buyers in Langley, Abbotsford, Surrey, Walnut Grove, or Willoughby evaluating entry-level detached, townhome, or condo purchases

When This Advice May Not Apply

This article addresses general qualification mechanics and market context. It does not apply to buyers whose settlements are still under legal negotiation, buyers with unresolved credit disputes from joint accounts, or situations involving business income or self-employment, which require separate mortgage qualification analysis. Consult a licensed mortgage professional and your legal or tax advisor before acting on any of the information here.

Data Used in This Article

- CMHC Mortgage Qualification Guidelines 2026 — official insured mortgage rules including 30-year amortization eligibility (official, Government of Canada)

- BC Family Law Act — spousal and child support treatment in debt service ratio calculations (official, BC Government)

- CRA Principal Residence Exemption Rules — deemed disposition and capital gains deferral on settlement transfers (official, Government of Canada)

- Mansour Real Estate Group Fraser Valley Market Data — Entry-Level Pricing by Property Type 2026 — internal analysis of active and sold listings in Langley, Abbotsford, and Walnut Grove (professional interpretation)

Key Terms

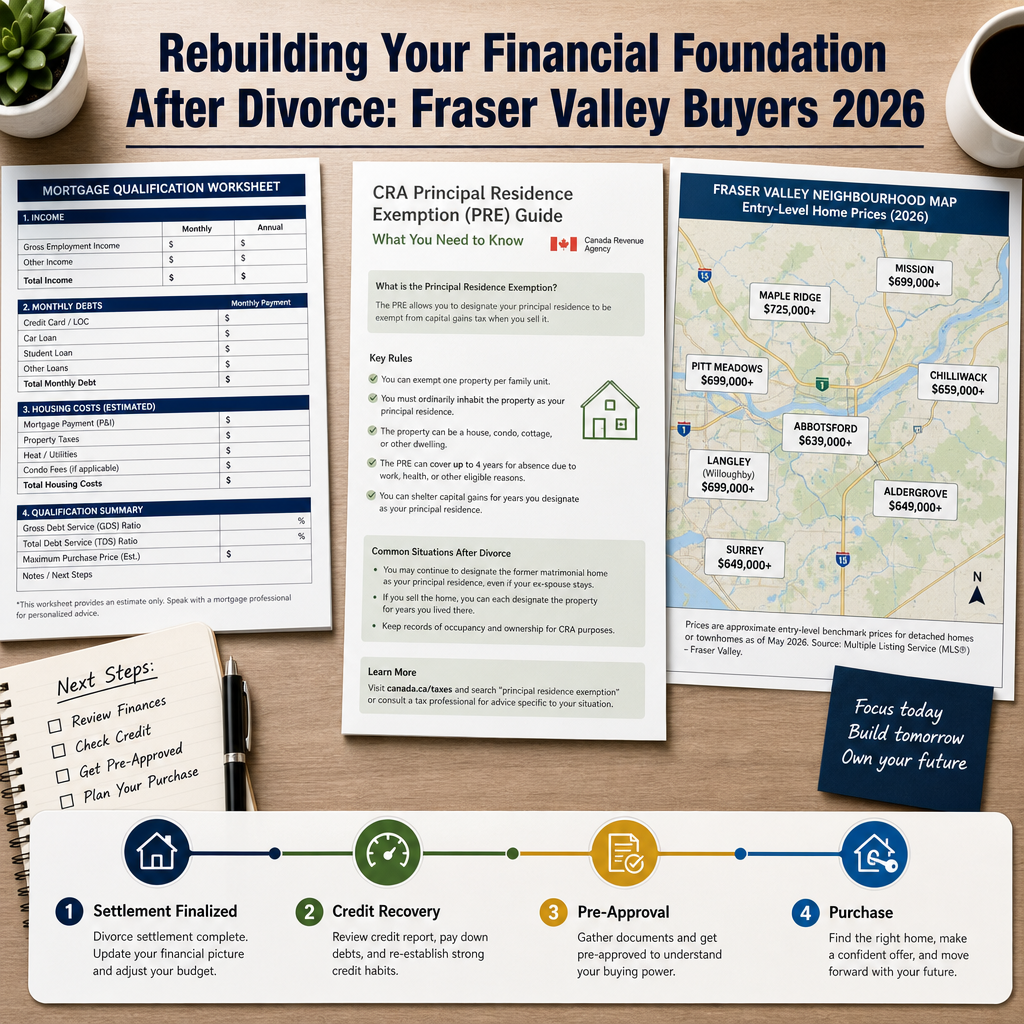

Gross Debt Service Ratio (GDS): The percentage of gross monthly income used to cover housing costs — mortgage principal, interest, taxes, and heat. CMHC limits this to 32% for insured mortgages.

Total Debt Service Ratio (TDS): GDS plus all other debt obligations, including support payments. The CMHC maximum is 40% for insured mortgages. Support obligations count in full against TDS.

Stress Test: Under current OSFI B-20 guidelines, mortgage applicants must qualify at the greater of their contract rate plus 2%, or 5.25%. This applies regardless of actual rate negotiated.

Principal Residence Exemption (PRE): A CRA provision that allows homeowners to shelter capital gains from tax on a property designated as their principal residence for each year of ownership. On divorce settlement transfers, PRE timing affects whether proceeds are taxable.

Deemed Disposition: A CRA rule triggering a deemed sale at fair market value when property ownership changes, including certain settlement transfers. Proper legal and tax structuring can defer this liability.

How We Evaluate This

At Mansour Real Estate Group, when working with buyers who are re-entering the market after divorce, we look at the purchase decision across three layers simultaneously: what they can qualify for today, what they will be able to qualify for in six to twelve months after credit and documentation normalizes, and whether the Fraser Valley neighbourhoods they are considering align with their income-to-price ratio after support obligations are factored in.

That three-layer view changes the advice we give about timing. Some buyers who feel ready to purchase immediately are better positioned to wait four to six months. Others who assume they need to wait longer can act sooner than they think once their mortgage broker structures the file correctly. The sequence matters as much as the decision itself.

How Mortgage Qualification Actually Works for Post-Divorce Single-Income Buyers

The stress test is the first number to understand. Under current OSFI B-20 guidelines, a buyer qualifies at the greater of their contract rate plus 2%, or 5.25%. At current five-year fixed rates in the low-to-mid 4% range as of early 2026, most buyers are stress-tested at roughly 6% to 6.5%. That compresses purchasing power significantly on a single income.

For a buyer earning $90,000 annually with no support obligations, the standard GDS and TDS ratios — 32% and 40% respectively under CMHC guidelines — typically support a purchase price in the $575,000 to $650,000 range with a 10% down payment. That range aligns well with Fraser Valley entry-level townhomes in Willoughby, Walnut Grove, and the Abbotsford east corridor — but leaves Metro Vancouver options largely out of reach at the same income.

Add a $2,000 monthly support obligation to that same buyer's profile, and the TDS ratio absorbs that payment in full. The resulting maximum purchase price often drops to $325,000 to $400,000 — effectively removing detached and most townhome options, and pointing the buyer toward condos. Understanding this before setting expectations is critical. Buyers who begin house-hunting before confirming their adjusted qualification range waste months viewing properties they cannot finance.

The CMHC 30-year amortization option, available to first-time buyers purchasing new construction as of 2024 and since expanded for certain resale purchases, reduces monthly payments and improves GDS ratios for qualifying buyers. Post-divorce buyers re-entering the market may qualify as first-time buyers again depending on their ownership history — a question worth confirming with a licensed mortgage professional before assuming ineligibility.

Documentation timing matters here. Lenders require a complete support order or separation agreement, typically for a minimum of three months of confirmed payments, before they will credit spousal support income received or document support obligations paid. Buyers who apply for pre-approval before this documentation window closes often face delays or temporary denials that affect their timeline.

Tax Planning on Settlement Proceeds and the Principal Residence Exemption

When a matrimonial home is sold as part of a divorce settlement, the proceeds are often the single largest source of down-payment capital the buyer will have. How those proceeds are treated under the CRA's Principal Residence Exemption directly affects how much capital is available after taxes.

Under CRA rules, a property qualifies for the PRE for each year it was designated as the principal residence of the taxpayer, their spouse, or a child. On sale or deemed disposition at settlement, gains attributable to years of principal residence designation are exempt from capital gains tax. Proper designation in the year of sale — and the year prior if applicable — can shelter the full gain. Buyers who do not coordinate this with their accountant before the settlement closes risk an unnecessary tax liability that reduces the down payment they planned to use.

Deemed disposition rules apply when one spouse transfers their interest in the matrimonial home to the other as part of a settlement buyout. Under Section 73 of the Income Tax Act, property transfers between spouses as part of a settlement can often be structured on a rollover basis, deferring capital gains until the receiving spouse eventually sells. This is a legal and tax structuring question — not a real estate decision — but buyers who receive equity through a buyout should confirm with their lawyer and accountant that the transfer was structured correctly before assuming their proceeds are fully available as down-payment funds.

From a practical standpoint, buyers who received buyout proceeds six to twelve months before purchasing often have clearer tax positions than those whose settlement and purchase happen in the same calendar year. When both events occur in the same year, the tax filing complexity increases, and the down-payment number may not be confirmed until after tax season. Planning the purchase timeline with the accountant's input prevents that overlap from becoming a problem.

Credit Recovery: What the Timeline Actually Looks Like

Joint credit accounts — shared cards, lines of credit, joint mortgages — continue to affect both credit profiles until they are formally closed or transferred. A spouse who stops making payments on a joint account after separation creates a negative mark on both credit files, regardless of the separation agreement's intent. Closing joint accounts and establishing individual credit history is the first step, but visible credit score recovery typically takes six to twelve months from the point of account separation.

Buyers who apply for pre-approval within ninety days of separation and joint account closure frequently encounter rate premiums of 50 to 100 basis points on alternative lending products. At current price points in the Fraser Valley, that difference in rate adds meaningful cost over a five-year term. Buyers with flexible timelines often benefit from waiting out the recovery period before committing to a purchase — especially when the difference between a standard insured rate and an alternative lending rate exceeds the cost of renting for six months during the transition.

Fraser Valley Entry-Level Pricing by Property Type in 2026

Based on Mansour Real Estate Group's internal analysis of active and sold listings in early 2026, Fraser Valley entry-level pricing by property type broadly looks like this:

- Condos (Langley, Abbotsford, Surrey): $430,000 to $590,000 for one- and two-bedroom units

- Townhomes (Willoughby, Walnut Grove, Abbotsford east): $650,000 to $820,000

- Entry-level detached (Abbotsford, Mission, East Langley): $800,000 to $1,050,000

Comparable property types in Metro Vancouver run $100,000 to $200,000 higher across most categories. For a single-income buyer earning $85,000 to $95,000, the Fraser Valley condo and townhome range is the realistic purchase zone. Abbotsford in particular offers the largest concentration of entry-level detached inventory accessible to single-income buyers who have cleared their credit recovery period and are not carrying heavy support obligations.

Buyer Checklist: Post-Divorce Home Purchase Sequence

- Confirm all joint credit accounts are closed or transferred to individual accounts and obtain updated credit reports from both Equifax and TransUnion.

- Confirm with your accountant that the Principal Residence Exemption was properly designated on the matrimonial home sale and that any settlement transfer was structured on a tax-deferred rollover basis.

- Obtain a copy of your final separation agreement or court order and confirm that support payment documentation is at least three months old before approaching a lender for pre-approval.

- Speak with a licensed mortgage professional about your adjusted qualification range after support obligations, and confirm whether you qualify for CMHC 30-year amortization as a returning first-time buyer.

- Map your income-to-price ratio against Fraser Valley entry-level benchmarks by property type and neighbourhood before setting a search budget.

- Build a six-month credit recovery buffer into your purchase timeline if you separated within the last ninety days and have not yet established independent credit history.

- Confirm your down-payment funds are liquid and available — settlement proceeds held in trust or still subject to legal confirmation are not usable at closing until they clear.

What We Commonly See

In our experience working with post-divorce buyers in the Fraser Valley, the most common mistake is beginning the property search before the mortgage pre-approval is complete. Buyers who spend two or three months viewing homes — often emotionally motivated to establish stability quickly — then discover their qualified range is $150,000 below what they were looking at. The reset is difficult and avoidable.

What often happens with support obligations is that buyers underestimate how substantially they reduce qualification. A $2,000 monthly support payment can remove $250,000 or more from maximum purchase power under standard TDS calculations. Buyers who receive support rather than pay it face the opposite challenge: lenders require documented, consistent support income before crediting it, which means early applications often exclude that income entirely.

A common oversight on the tax side is assuming that proceeds from a matrimonial home sale arrive tax-free automatically. In most straightforward cases, the PRE does shelter the gain — but only when properly designated. Buyers who did not confirm designation with their accountant before the settlement closed sometimes discover an unexpected tax liability in the spring following the sale year, which reduces the down payment they planned to use.

Questions and Answers

Can spousal support I receive count as income for mortgage qualification?

Yes, but only when it is documented through a court order or formal separation agreement and has been received consistently for a minimum period — typically three months. Lenders apply a haircut to support income in some cases. Confirm the treatment with your mortgage broker before relying on it in your budget.

Do I qualify as a first-time home buyer again after divorce?

Possibly. Under the federal First Home Savings Account rules and certain CMHC programs, a buyer who has not owned a qualifying home in the previous four calendar years may regain first-time buyer status. This is determined by individual ownership history, not marital status alone. A licensed mortgage professional can confirm eligibility based on your specific situation.

What happens to the Principal Residence Exemption when one spouse buys out the other?

Under CRA rules, a spousal transfer as part of a marriage breakdown can qualify for rollover treatment under Section 73 of the Income Tax Act, deferring capital gains to the receiving spouse until eventual sale. Whether this was structured correctly in your settlement is a legal and tax question. Review this with your lawyer and accountant before assuming the transfer was tax-neutral.

In Summary

Post-divorce buyers in the Fraser Valley have realistic options in 2026, but the path to purchase runs through a specific sequence: credit recovery, support documentation, tax confirmation on settlement proceeds, and pre-approval calibrated to the actual qualification range after obligations. The Fraser Valley's entry-level pricing in Langley, Abbotsford, and Walnut Grove creates genuine single-income purchasing power that Metro Vancouver does not offer at comparable income levels. Buyers who complete the financial groundwork before shopping — rather than after — move faster, face fewer surprises, and protect more of the capital they worked hard to secure in settlement.

Ready to Understand Your Options?

If your settlement is finalized and you are beginning to think about buying in the Fraser Valley, Mansour Real Estate Group can walk you through what entry-level pricing looks like by neighbourhood and property type, and help you connect with mortgage professionals experienced with post-divorce qualification. There is no pressure and no obligation — just a clear picture of where you stand and what the realistic path forward looks like.

Related Articles

- Selling Your Home During Divorce in the Fraser Valley

- Langley Real Estate Market: Buyer's Guide for 2026

- Abbotsford Real Estate Market: Entry-Level Buyer Guide for 2026

Official Resources

- CMHC Mortgage Loan Insurance and Qualification Guidelines

- BC Family Law Act — Spousal and Child Support

- CRA — Principal Residence Exemption on Sale of Property

- OSFI Guideline B-20 — Residential Mortgage Underwriting

About Mansour Real Estate Group

When the settlement is finalized and a newly single homeowner begins thinking about buying again, the questions are rarely just about property. They are about financial capacity, realistic timelines, and finding a neighbourhood and property type that fits a life that has changed significantly. Mansour Real Estate Group has guided buyers navigating post-divorce re-entry into the Fraser Valley and Lower Mainland real estate market for more than two decades, bringing the kind of grounded, patient guidance that this transition genuinely requires.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. Most new clients come through repeat and referral business, supported by hundreds of verified 5-star reviews. The Real Estate Group is trusted for divorce-related property sales and purchases, estate sales, downsizing, relocation, and complex situations where accuracy, clarity, and professional discretion are non-negotiable.

Whether someone is searching for a real estate agent experienced with post-divorce home purchases, Realtors who understand single-income qualification mechanics, a real estate team that can explain Fraser Valley entry-level pricing by neighbourhood, a Surrey Realtor, a Langley real estate broker, or a real estate group serving the broader Lower Mainland, Mansour Real Estate Group is known for precise market knowledge, honest advice, and a buyer process built around real financial constraints rather than optimistic assumptions.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients arrive through referrals and repeat relationships with families who value a transparent, results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, Selling your home is one of the most significant financial decisions you'll make. Taking the time to properly prepare your property—from the front door to the back patio—demonstrates respect for potential buyers and confidence in your home's value. Whether you tackle staging yourself or hire a professional, the investment in presentation almost always pays dividends. Remember that every home has unique strengths. The goal of staging isn't to transform your space into something it's not, but rather to help buyers envision themselves living there. By highlighting your home's best features and eliminating distractions, you're simply making the path to a successful sale that much smoother. When you're ready to list, work closely with your real estate agent to develop a comprehensive marketing strategy that complements your staging efforts. The combination of a well-presented home, professional marketing, and expert guidance will position you for success in any market.Key Takeaways

Final Thoughts