Probate Real Estate Sales in BC: How Executors' Market Timing Decisions and Fair Market Valuation Strategy Create 15–30% Variance in Final Estate Proceeds

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland | Published: July 14, 2025 | Topic: Life-Event Sales — Estate and Probate Strategy, BC

For executors managing an estate in the Fraser Valley, selling the family home is rarely a straightforward real estate transaction. It sits at the intersection of legal process, tax planning, and live market conditions — three systems that rarely move in sync. When those systems are managed without a coordinated strategy, the estate can recover significantly less than it should.

This article explains the decisions that create the widest spread in final proceeds: when to list, how to establish fair market value, and how to coordinate probate filing timelines with buyer demand cycles in BC's current market. It is written for executors, estate lawyers, beneficiaries, and anyone involved in managing an inherited property in the Fraser Valley or Lower Mainland.

Short Answer

Executors selling BC estate properties face measurable proceeds variance — typically 15 to 30% — based on two decisions: when they list relative to seasonal buyer demand, and whether they use a certified appraisal or a realtor CMA to establish fair market value. In the Fraser Valley's current buyer's market, both decisions carry more financial consequence than most executors anticipate. The framework below explains how to manage each one.

Key Takeaways

- Executors can list BC estate properties before a Grant of Probate is issued, but possession-date closings carry contract risk if the grant is delayed beyond expected timelines.

- Spring listings in the Fraser Valley (February to April) consistently recover more proceeds than summer or fall equivalents, particularly in buyer's markets with elevated active inventory.

- Certified appraisals establishing fair market value at the date of death serve both CRA compliance and listing strategy — they are not the same document as a realtor's current CMA.

- Deemed disposition rules under the Income Tax Act calculate capital gains at the date of death, not the sale date; the gap between those two valuations determines taxable exposure.

- Coordinating probate filing timelines with market seasonality is the highest-leverage decision an executor can make — and the one most commonly overlooked.

Who This Applies To

- Executors managing BC estate properties in the Fraser Valley, Surrey, Langley, White Rock, Abbotsford, or North Delta

- Beneficiaries who are also involved in sale decisions and want to understand how proceeds are affected by timing and valuation choices

- Estate lawyers and accountants advising executors on CRA compliance and asset disposition

- Families managing an estate where the property represents the largest single asset

When This Advice May Not Apply

- Estates where the property qualifies for a full principal residence exemption and tax exposure is not a relevant factor

- Urgent estate liquidations where beneficiary circumstances require sale regardless of market timing

- Properties subject to active legal disputes among beneficiaries — those require legal resolution before a sale strategy can be implemented

Data Used in This Article

- BC Wills, Estates and Succession Act (WESA) — Executor authority, property disposition rules; official legislation

- Canada Revenue Agency — IT-416 and related deemed disposition guidance — Tax treatment of estate property at date of death; official government source

- Fraser Valley Real Estate Board (FVREB) — 2026 monthly statistical packages — Sales-to-active ratios, days on market, seasonal demand patterns; official board data

- BC Supreme Court Civil Rules — Probate proceedings — Grant of Probate timelines and registry processing standards; official court rules

- Mansour Real Estate Group internal case analysis — Timing and valuation impact observations across estate transactions; professional experience, not published research

The Core Problem: Three Timelines That Don't Align

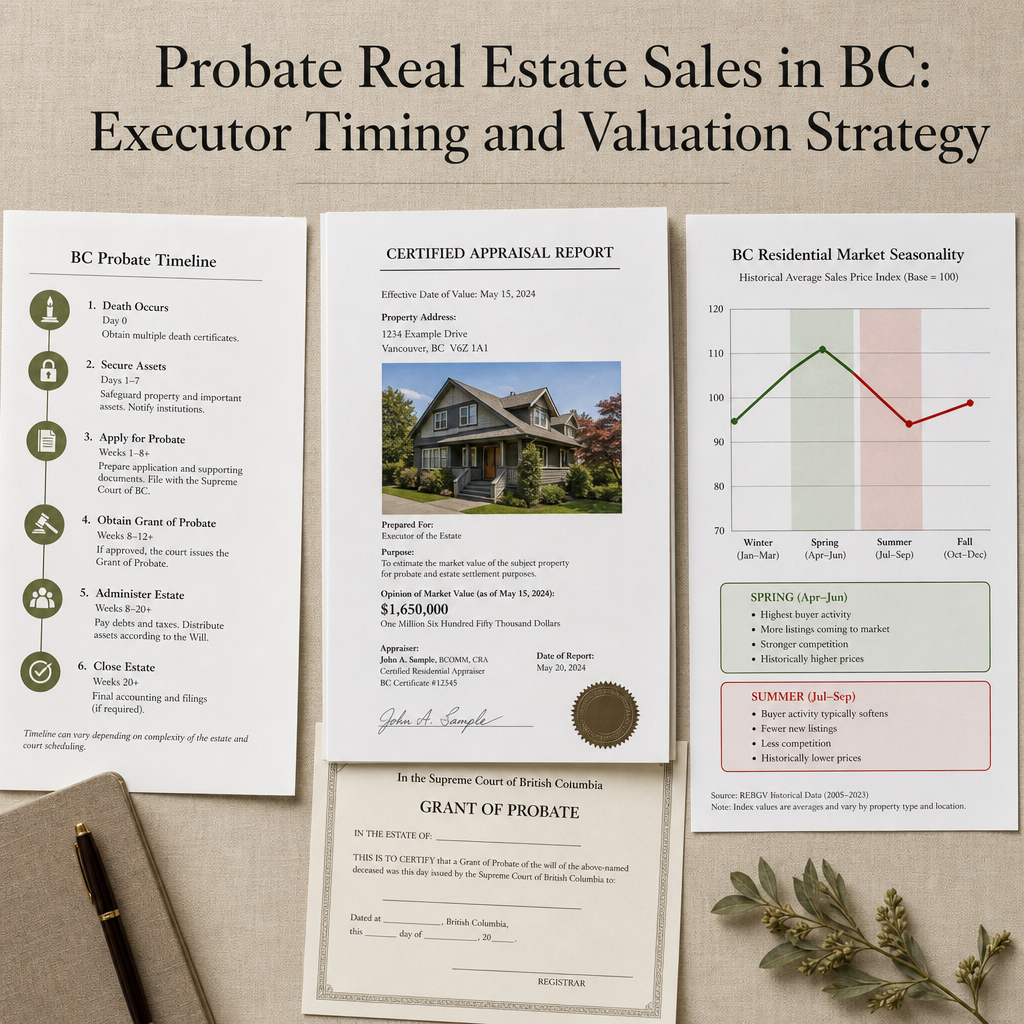

Every executor faces three timelines simultaneously. The first is the legal timeline: probate applications filed with the BC Supreme Court typically take 8 to 16 weeks to result in a Grant of Probate, according to BC court registry processing standards. That grant is what formally authorizes the executor to transfer title to a buyer.

The second is the tax timeline. Under the Income Tax Act, deemed disposition rules treat the estate property as sold at fair market value on the date of death. That creates a capital gains calculation anchored to a specific date in the past — not the date the property eventually sells. The CRA requires that fair market value to be supportable, and the most defensible support is a certified retrospective appraisal.

The third is the market timeline. Buyer demand in the Fraser Valley is strongly seasonal. According to FVREB monthly statistical packages, the February to April window consistently produces the strongest buyer pool and the highest sales-to-active ratios of the year. In 2026, the Fraser Valley's overall sales-to-active ratio sat near 11%, reflecting a buyer's market — which means the difference between listing into peak spring demand versus listing in August or September carries real financial consequence for an estate that can afford to be patient.

Listing Before the Grant of Probate: How It Works and Where It Breaks Down

Under BC's Wills, Estates and Succession Act, an executor has authority to act on behalf of the estate from the moment of death — but that authority becomes legally enforceable for the purpose of transferring title only once the Grant of Probate is issued. A property can be listed and an accepted offer can be written before the grant, provided the contract specifies a possession date (and therefore a completion date) that falls after the expected grant issuance.

This structure allows executors to take advantage of spring buyer demand while the probate process is still underway. If probate is filed promptly and the grant arrives within a normal 10-to-12 week window, the gap between accepted offer and expected completion can be managed through contract terms. The risk is misalignment: if the grant is delayed — due to complex estates, court backlogs, or incomplete documentation — a possession-date contract can collapse or require renegotiation at a point when the buyer's circumstances may have changed.

In our experience working on estate property sales across the Fraser Valley, the executors who navigate this successfully file the probate application before — or immediately after — listing, maintain close communication with their estate lawyer about registry timelines, and build realistic completion date buffers into the contract. Those who list speculatively, without confirming the filing status, are the ones who face avoidable complications at the accepted-offer stage.

Fair Market Valuation: Two Purposes, One Document

One of the most consistent gaps we see in estate sales is confusion between fair market valuation for CRA purposes and a realtor's current comparative market analysis. They serve different functions and produce different numbers — sometimes by 8 to 12% on a mid-market Fraser Valley property.

For CRA purposes, the executor needs to establish what the property was worth at the date of death. That is typically done through a certified retrospective appraisal — a formal appraisal by a designated appraiser that uses comparable sales from the date of death, not the current date. That number anchors the deemed disposition calculation and determines how much capital gain the estate owes, if any.

Certified appraisals typically cost between $1,500 and $2,500 for a Fraser Valley residential property. On a property that has appreciated significantly between death and sale — which is common when probate takes several months and market values shift — a lower retrospective appraisal value can reduce taxable capital gains meaningfully. Conversely, an inflated estimate that doesn't reflect date-of-death conditions creates unnecessary tax exposure.

Separately, the executor needs a current market analysis to set the listing price. That CMA uses today's comparable sales and reflects current buyer demand and inventory levels. Conflating these two exercises — or using only one — is a planning error that affects both the estate's tax outcome and its sale outcome. For inherited property sales in BC, both documents are worth commissioning.

How We Evaluate This

When Mansour Real Estate Group works with an executor, the first conversation is not about listing price. It is about three things: the current probate status, the date-of-death fair market value relative to current conditions, and the estate's flexibility on timing.

From those inputs, we build a coordination map: when probate was or will be filed, what the expected grant date is, which market window that aligns with, and what the price gap looks like between the CRA valuation and the current listing strategy. That sequence — legal, tax, then market — is the correct order. Most of the proceeds variance we have observed in estate sales comes from reversing that order, or skipping the tax step entirely until it creates a problem at closing.

Seasonal Demand in the Fraser Valley: What the Data Shows

The FVREB's monthly statistical packages show a consistent seasonal pattern across property types. Sales-to-active ratios in February, March, and April typically run 20 to 35% higher than the same measure in July, August, and September. In a balanced market, that difference is significant. In a buyer's market — where Fraser Valley's sales-to-active ratio remained near 11% through much of early 2026 — that difference is the margin between a sale that closes at asking and one that requires price reductions to generate any offers at all.

For executors who have the legal and financial flexibility to choose their listing window, coordinating probate filing with a target spring market entry is the single highest-leverage decision in the process. An estate where probate is filed in November or December, with a March or April completion-date contract in mind, is positioned to take advantage of the strongest buyer pool of the year. An estate where probate is filed reactively — after beneficiaries have already started asking why the property hasn't sold — has often already missed that window.

Days-on-market data from the FVREB also supports this. Properties listed in spring buyer demand windows in the Fraser Valley move faster, generate more competing interest, and require fewer price adjustments than equivalent properties listed in the fall. For an estate property where carrying costs — property taxes, utilities, insurance, and maintenance — continue to accumulate during the listing period, a faster sale has a direct bottom-line benefit beyond the sale price itself.

Estate Seller Checklist

- Confirm executor authority — verify the will and confirm you are the named executor before taking any sale-related steps.

- File the probate application promptly — delays in filing directly reduce flexibility in choosing your listing window.

- Commission a certified retrospective appraisal at the date of death — this establishes the CRA-defensible fair market value for deemed disposition purposes.

- Get a current CMA from a Fraser Valley realtor experienced with estate sales — this is a separate exercise from the appraisal and sets the listing strategy.

- Map the expected grant date against seasonal market windows — identify whether a spring listing is achievable with a completion-date contract structure.

- Confirm whether the principal residence exemption applies — if the deceased lived in the property as their primary residence, the tax picture changes substantially; consult an accountant.

- Address the property's presentation condition — estate properties often need targeted cleaning, minor repairs, and professional photography to compete with active inventory.

- Communicate proactively with beneficiaries — timeline expectations set early prevent pressure that can force premature listings or price reductions.

What We Commonly See

Probate filed too late to hit spring demand. In our experience, the most common and most costly mistake executors make is treating probate filing as something to be done after the estate is "ready." By the time family decisions are made and paperwork is assembled, the spring window has passed. Filing in the first weeks after death — even before the estate is fully organized — preserves market timing options.

Using only one valuation for two purposes. What often happens is an executor asks a realtor for a CMA, uses that number for both the CRA filing and the listing price, and later discovers the CRA number needed to reflect date-of-death conditions, not current conditions. The result is either unnecessary tax exposure or an unsupported CRA filing. A certified retrospective appraisal and a current CMA are both necessary, and they are not interchangeable.

Underestimating carrying costs during the listing period. A common mistake is focusing entirely on the sale price while overlooking that every week the property sits unsold, the estate incurs property taxes, utilities, strata fees (if applicable), and insurance. In a buyer's market, an estate property priced aggressively to sell in spring often nets more than one priced higher that carries through summer and ultimately sells below asking. Timing and pricing are connected, not separate decisions.

Questions Executors Commonly Ask

Can we list and accept an offer before the Grant of Probate is issued?

Yes. Under BC's Wills, Estates and Succession Act, an executor can list and accept an offer, but title cannot transfer until the grant is issued. Contracts must specify a completion date that accounts for expected grant timing. If the grant is delayed, completion date renegotiation may be necessary — which carries buyer relation risk.

What is the difference between the deemed disposition value and the listing price?

The deemed disposition value is the fair market value at the date of death, used for CRA capital gains purposes. The listing price reflects current market conditions. If significant time has passed between death and sale — or if the market has shifted — these two numbers can differ substantially. Both need to be established accurately and independently.

Does the principal residence exemption apply to estate properties?

It may. If the deceased used the property as their principal residence and meets CRA eligibility criteria, some or all of the capital gain on deemed disposition may be sheltered. This determination requires input from a qualified accountant or tax advisor familiar with estate taxation in BC — it is not a question the executor or realtor can answer definitively.

In Summary

The proceeds variance executors experience in Fraser Valley estate sales is not random. It comes from three predictable sources: listing timing relative to seasonal buyer demand, the quality and purpose-specificity of the valuation work done at the outset, and how well the probate filing timeline is coordinated with market windows. Executors who treat these as separate, sequential decisions — legal first, then tax, then real estate — consistently recover more from the estate than those who approach the sale reactively. In a buyer's market, where competition and buyer urgency are already compressed, that coordination is not optional. It is the framework that determines the outcome.

Considering a consultation about an estate property in the Fraser Valley?

Mansour Real Estate Group works with executors, estate lawyers, and families at every stage of the probate and sale process. Reach out for a no-obligation conversation about timing, valuation, and next steps — before the listing decision is made.

Related Articles

- Estate Property Sales in the Fraser Valley: A Complete Executor's Guide

- Selling Inherited Property in BC: What Executors Need to Know Before Listing

- Selling in a Fraser Valley Buyer's Market: Strategy, Timing, and Pricing for 2026

About Mansour Real Estate Group

When a property must be sold as part of an estate or probate process, the real estate team managing the transaction needs to understand more than market pricing. Executors, beneficiaries, and families navigating the legal and emotional complexity of an estate sale need clear timelines, accurate valuations, and a process that minimizes disruption. Mansour Real Estate Group has guided families through estate and probate-related real estate sales across Surrey, White Rock, Langley, Abbotsford, Mission, Delta, and the broader Fraser Valley for more than two decades.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for estate sales, probate sales, executor-managed transactions, divorce-related sales, downsizing, and complex real estate situations requiring careful coordination.

Whether someone is searching for a Realtor experienced with estate sales, a real estate agent who understands probate timelines, real estate agents who specialize in executor-managed property, a trusted real estate team for complex estate transactions, a Surrey Realtor, a Langley real estate broker, or a Fraser Valley real estate group with deep experience in life-event sales, Mansour Real Estate Group is known for accurate valuations, transparent process, and clear communication that keeps all parties informed.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.