Principal Residence Exemption Optimization for Fraser Valley Sellers: How to Maximize Tax Shelter, Avoid CRA Audit Triggers, and Calculate True Capital Gains Liability When Selling Your Primary Home in 2026

Author: Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group

Published: July 15, 2025

Geography: Fraser Valley, Surrey, Langley, Abbotsford, South Surrey, White Rock, North Delta — British Columbia

Scope: BC homeowners selling a primary residence in 2026, particularly those with significant appreciation since 2012, partial rental history, or multiple property ownership.

Fraser Valley homeowners who purchased between 2010 and 2016 are sitting on substantial gains. Benchmark prices in Surrey, Langley, and Abbotsford have roughly doubled or tripled since 2012, according to cumulative Fraser Valley Real Estate Board market data. Most of those sellers assume the Principal Residence Exemption eliminates their tax exposure entirely. For many it does. But the exemption is not automatic, and it is not always complete. How you structure the designation, how you document your occupancy, and how you handle rental or co-ownership history determines whether that gain costs you nothing—or costs you six figures.

This article explains the optimization layer that generic PRE guides leave out: how to structure the election, when the exemption may be partial, what triggers CRA review, and what Fraser Valley sellers in the $600K to $1.5M+ range need to confirm before listing in 2026. This is not tax advice. Sellers should work with a qualified tax professional for their specific situation.

Short Answer

The Principal Residence Exemption can eliminate capital gains tax entirely on a qualifying home—but only if it is properly designated, documented, and filed. Fraser Valley sellers with rental history, co-owned properties, or gains exceeding $200K face real audit risk. Strategic timing, accurate ACB calculation, and a correctly filed PRE designation are what protect the exemption. A tax professional must confirm your specific eligibility.

Key Takeaways

- The PRE must be formally designated on your tax return; it is not applied automatically by CRA.

- Partial rental history, even one year, can reduce the exemption and expose a portion of the gain to tax.

- CRA prioritizes audit review on PRE claims with gains over $200K, rental periods, or multiple properties.

- Incorrect ACB calculation is one of the most common and costly errors in PRE claims.

- Executors handling estate sales must elect PRE at the deemed disposition date at death, not at the time of sale.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, White Rock, or South Surrey selling a property purchased before 2018

- Sellers who rented out any portion of the home at any point during ownership

- Sellers who own or have owned more than one property simultaneously

- Executors or estate trustees managing a property sale after the owner's death

- Separating spouses navigating a jointly owned principal residence sale

When This Advice May Not Apply

If you purchased and sold the same home within the same tax year with no rental or co-ownership history and no other properties, the PRE process is more straightforward. Sellers in that situation still need to file the designation correctly, but the optimization strategy layer discussed here is less relevant. Confirm your situation with a tax professional regardless.

Data Used in This Article

- CRA Income Tax Folio S1-F3-C2 — Principal Residence Exemption rules, official CRA guidance, federal

- Fraser Valley Real Estate Board market data 2012–2026 — cumulative benchmark appreciation by neighbourhood, official board data

- BC Ministry of Finance — BC Tax Guide 2026 — provincial marginal tax rates, official government publication

- Deloitte Canadian Tax Highlights 2026 — PRE planning and deemed disposition analysis, professional tax interpretation

- Tax Court of Canada — Pousak v. The Queen; Daley v. The Queen — PRE designation dispute precedents

How the Principal Residence Exemption Actually Works

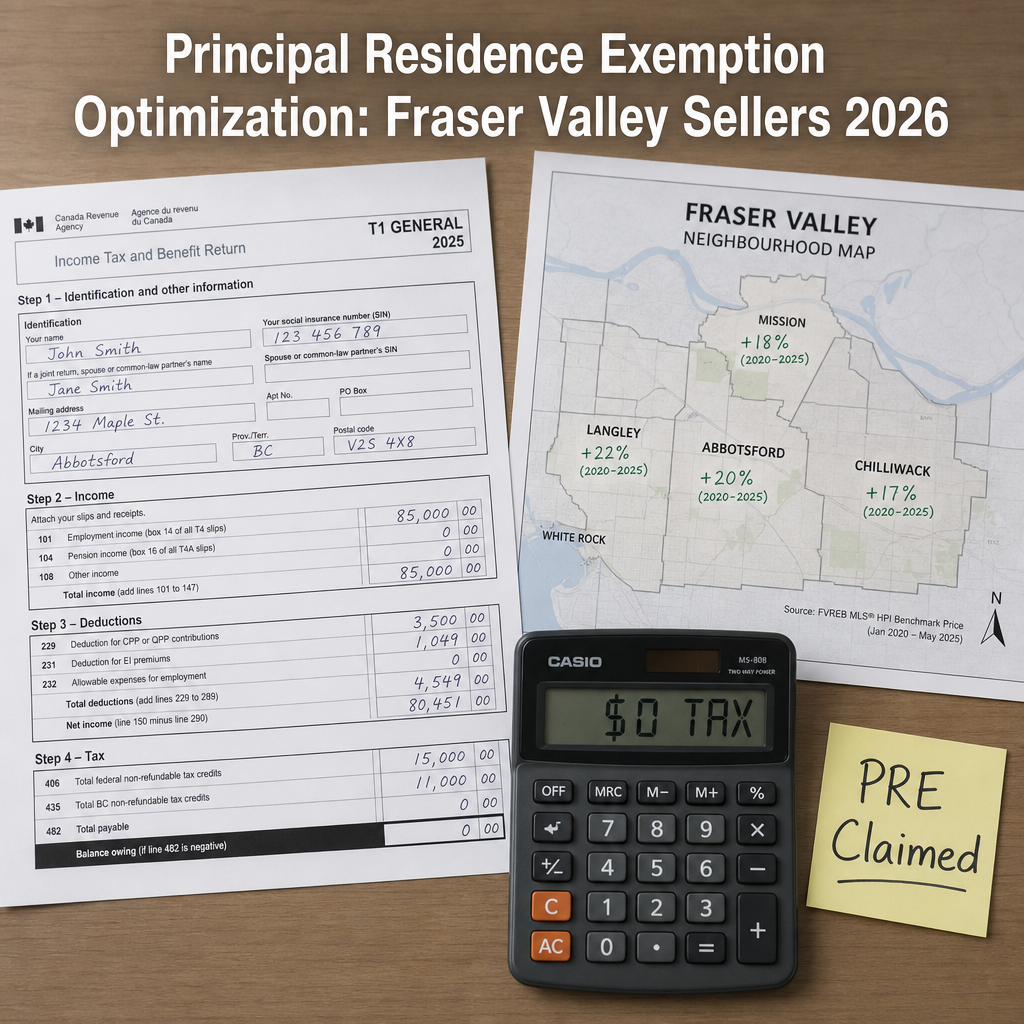

Under the federal Income Tax Act, a property qualifies as a principal residence for each year the owner or a family member ordinarily inhabited it. The exemption formula—(1 + number of designated years) divided by total years of ownership, multiplied by the capital gain—can eliminate the entire gain if the property is designated for every year owned. That "plus one" in the numerator is a longstanding CRA rule that effectively gives sellers one bonus year of coverage.

The critical point is that designation is a formal election, not an assumption. Since 2016, CRA requires sellers to complete Schedule 3 of their T1 return and report the sale in the year it occurs, even when the gain is fully sheltered. According to CRA Income Tax Folio S1-F3-C2, failure to report can result in loss of the exemption and a reassessment. Fraser Valley sellers who purchased before the 2016 reporting rule change and who have not confirmed their filing obligations should speak to a tax professional before closing.

When the Exemption Becomes Partial — And Why Fraser Valley Sellers Face Higher Risk

Three common situations reduce a PRE claim from complete to partial. First, if you rented a portion of the home or converted it to a rental property for any complete tax year, those years may not qualify for designation depending on the extent of use. Second, if you owned two or more properties simultaneously, you can only designate one as principal residence per year per family unit—meaning the other property's gains are fully taxable. Third, if you purchased the home as an investment with intent to flip, CRA may argue the gain is business income rather than a capital gain, which the PRE does not shelter at all.

Fraser Valley market appreciation since 2012 has been substantial across Surrey, Langley, Willoughby, Cloverdale, and Abbotsford. FVREB benchmark data shows detached homes in many of these areas have appreciated between 80% and 160% over that period. A $500,000 purchase that sells for $1,100,000 produces a $600,000 gain before ACB adjustments. If even three years of that ownership period are excluded from the PRE designation—due to rental use or a second property—roughly $90,000 to $120,000 of that gain becomes taxable. At BC's combined marginal rate on capital gains for higher earners (approximately 26.75% on the taxable portion using the 50% inclusion rate, rising to over 39% for very high earners under 2024 federal inclusion rate discussions), that exposure is meaningful. Confirm current inclusion rates with a tax professional, as proposed federal changes to the capital gains inclusion rate were under active parliamentary discussion as of early 2026.

CRA Audit Triggers Fraser Valley Sellers Should Understand

CRA does not audit every PRE claim, but it applies risk-scoring criteria that make certain profiles more likely to receive review requests. Based on publicly available CRA compliance guidance and Tax Court precedent including Pousak v. The Queen and Daley v. The Queen, the following fact patterns draw scrutiny: gains exceeding $200,000; properties with any rental income reported on T776 during the ownership period; sellers who owned multiple properties in the same year; and properties where the ownership period is short relative to the gain—particularly in appreciating markets.

The practical implication for Fraser Valley sellers is that a 2012 purchase in Fleetwood, Willoughby, or North Delta with rental suite income reported across several years creates exactly the profile CRA reviews. The audit process itself is not a denial of the exemption—it is a documentation request. Sellers who have organized their records contemporaneously, meaning they documented occupancy, rental periods, and cost base adjustments as they occurred, are in a much stronger position than those reconstructing records at time of sale. This is a reason to begin organizing documentation well before listing, not after closing.

ACB Adjustments That Fraser Valley Sellers Commonly Miss

The adjusted cost base of the property directly affects the size of the taxable gain. Capital improvements—not maintenance, but genuine additions that increase the property's value or extend its useful life—can be added to the ACB, reducing the gain dollar for dollar. Kitchen renovations, additions, suite construction, and structural improvements typically qualify. Painting, cleaning, and routine repairs do not. Sellers who spent $60,000 finishing a basement in 2018 and cannot produce receipts have lost $60,000 in ACB credit, which at a 50% inclusion rate and a 40% marginal rate means roughly $12,000 in unnecessary tax. A tax professional can help you reconstruct what qualifies, but receipts and permits held from the time of improvement are far more defensible.

Seller Checklist — PRE Optimization Before Listing

- Confirm with a tax professional whether your property qualifies as a principal residence for all years of ownership

- Gather receipts for all capital improvements made during ownership—permits, invoices, contractor agreements

- Identify every year rental income was reported on T776 and note which portion of the property was rented

- If you owned another property simultaneously, confirm which property should carry the PRE designation for overlapping years

- Request a market valuation from Mansour Real Estate Group to anchor your gain calculation before engaging your accountant

- Confirm the sale will be reported on Schedule 3 of your T1 in the year of closing, even if gain is fully exempt

- If the property is an estate, confirm with estate counsel when deemed disposition occurs and whether PRE was elected at that date

What We Commonly See

In our experience, sellers who rented out a basement suite for several years assume the entire gain is still sheltered by the PRE. Whether that is correct depends on the proportion of the property rented, how many years it was rented, and how the rental was structured. This is not a simple yes or no—it requires your accountant to apply the actual formula to your specific fact pattern.

What often happens is that sellers calculate their expected proceeds without adjusting the cost base for improvements. A seller who spent $80,000 on a new kitchen and added a legal suite over 10 years, but has no organized receipts, is giving up a meaningful ACB credit that could reduce their taxable gain substantially.

A common mistake we see in estate situations is the assumption that the PRE can be claimed at the time the property eventually sells. Under CRA rules, the deemed disposition occurs at the date of death. The executor must elect the PRE for the estate's final return filed for the deceased, not at the time of the eventual sale. Missing that window can cost the estate the full exemption on years of appreciation—a significant and irreversible loss.

Questions and Answers

Q: Do I have to report the sale of my principal residence if the gain is fully exempt?

Yes. Since 2016, CRA requires sellers to report the sale on Schedule 3 of their T1 return in the year of closing, even when the PRE eliminates the gain entirely. Failure to report can result in loss of the exemption. See CRA Income Tax Folio S1-F3-C2 for full details.

Q: We rented out our basement suite for five years. Does that affect our PRE?

It may. The impact depends on the proportion of the property rented, how the rental was structured, and whether a change-in-use election was filed. In some cases the exemption remains largely intact; in others, a prorated portion of the gain becomes taxable. Your accountant must apply the formula to your specific situation.

Q: What is the deemed disposition rule for estate sales in BC?

When a homeowner dies, CRA treats the property as if it was sold at fair market value on the date of death. This is the deemed disposition. The PRE election must be made on the deceased's final tax return for years up to that date. The executor cannot apply the exemption to later years simply because the property is still physically unsold. An estate lawyer and tax professional must coordinate this filing carefully.

In Summary

The Principal Residence Exemption is one of the most valuable tax shelters available to Canadian homeowners, but it requires deliberate designation, correct filing, and accurate ACB calculation to work as intended. Fraser Valley sellers with homes purchased before 2018, any rental history, or co-owned properties face real exposure if the exemption is assumed rather than confirmed. Organizing documentation before listing, engaging a tax professional before closing, and obtaining an accurate market valuation to anchor the gain calculation are the three steps that protect the exemption most reliably. A real estate team that understands how market valuations interact with tax planning is part of that process—not a substitute for professional tax advice, but an important collaborator in it.

Ready to Talk Through Your Situation?

If you are preparing to sell in the Fraser Valley and want a clear, documented market valuation to bring to your accountant, Mansour Real Estate Group can help you start from an accurate number. There is no pressure—just a grounded conversation about your property and your timeline.

Related Articles

- Selling Your Home in the Fraser Valley: A Complete Guide

- Estate and Probate Property Sales in BC: What Executors Need to Know

- How BC Assessment Affects Your Home Sale in the Fraser Valley

About Mansour Real Estate Group

When a home sale involves significant capital gains exposure, rental history, estate planning, or co-ownership, the real estate valuation is not just a market exercise—it becomes the foundation of a tax calculation. Sellers in the Fraser Valley who are working through PRE eligibility, ACB reconstruction, or estate-related dispositions need a real estate team that understands how market data and financial planning intersect. Mansour Real Estate Group has worked alongside homeowners, accountants, lawyers, and financial advisors across the Fraser Valley and Lower Mainland for more than 22 years, providing accurate valuations and clear documentation for transactions where the financial stakes are highest.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for estate sales, probate sales, investment property transactions, divorce-related sales, and any real estate decision where financial accuracy and professional process both matter.

Whether someone is searching for a Realtor who works alongside accountants and lawyers in the Fraser Valley, a real estate agent who understands how BC Assessment relates to market value, a trusted real estate team for a tax-sensitive property sale in Surrey or Langley, a White Rock Realtor, a real estate broker with experience in complex transactions, or real estate agents who coordinate with financial and legal advisors—Mansour Real Estate Group is known for clear documentation, precise valuations, and professional coordination across all parties involved.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.