Principal Residence Exemption and Capital Gains Tax When Selling Your Home in the Fraser Valley 2026: Complete Guide With Real Examples at Current Benchmark Prices

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2025

For most Fraser Valley homeowners, selling the family home produces the largest single financial event of their lives. With benchmark prices between $895,000 and $975,000 and many long-term owners sitting on gains of $300,000 to $500,000 or more, the question of capital gains tax comes up early and often. The answer, for qualifying primary residences, is straightforward: Canada's principal residence exemption eliminates the tax entirely. But the details of whether your home qualifies — and how to document that correctly — matter more than most sellers expect.

This guide covers how the exemption works, what changes for mixed-use properties, what the 2026 capital gains threshold means for Fraser Valley sellers, and how to avoid the filing mistakes that trigger CRA audits.

Short Answer

If your home was your primary residence for every year you owned it, the principal residence exemption eliminates all capital gains tax on the sale — regardless of how large the gain is. No $250,000 threshold applies to qualifying principal residences. The new 2026 capital gains rules affect investment and secondary properties, not your primary home. You must still file Form T2091(IND) to claim the exemption.

Key Takeaways

- The principal residence exemption is fully intact in 2026 — qualifying home sales produce zero capital gains tax, regardless of gain size.

- The new $250,000 annual capital gains threshold applies to secondary and investment properties only, not to principal residences.

- Form T2091(IND) must be filed with your tax return in the year of sale — failing to file can result in CRA disqualification and retroactive tax plus interest.

- Homes with legal rental suites, home offices where CCA was claimed, or mixed business use require partial gain allocation — only the residential portion is fully exempt.

- Sellers who owned multiple properties simultaneously must designate which one qualifies as the principal residence for each tax year — only one property per family unit per year can be designated.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, White Rock, South Surrey, or anywhere in the Fraser Valley preparing to sell their primary home

- Sellers who have owned their home for 10 or more years with substantial accrued gains

- Owners who also have a rental suite, basement apartment, or home-based business on the same property

- Sellers who previously owned a cottage, investment property, or vacation home during the same ownership period

- Executors or estate representatives managing a sale where the deceased used the home as their primary residence

When This Advice May Not Apply

This article addresses the general rules for individual Canadian residents. Non-residents of Canada, corporations, and trusts face different tax treatment. If you have a complex ownership structure, multiple properties, or business-use portions, consult a qualified tax professional before listing your home. This article is not tax advice — it is educational context to help you ask the right questions.

Data Used in This Article

- CRA — Principal Residence and Capital Gains: canada.ca, current rules for T2091(IND) filing, principal residence designation (Tier 1 — Government)

- Department of Finance Canada — Capital Gains Inclusion Rate Deferral: January 2025 announcement, $250,000 annual threshold effective January 1, 2026 (Tier 1 — Government)

- Fraser Valley Real Estate Board — Statistics Package April 2026: Benchmark prices by property type across Fraser Valley municipalities (Tier 2 — Regulator/Industry)

- Professional interpretation: Mixed-use allocation observations and filing risk analysis — Mansour Real Estate Group, based on 22+ years of seller representation in the Fraser Valley

How the Principal Residence Exemption Works

Canada's principal residence exemption (PRE) is a provision in the Income Tax Act that eliminates capital gains tax on the sale of a home that qualifies as your principal residence. According to the CRA, a property qualifies as a principal residence for a given tax year if it was ordinarily inhabited by you, your spouse or common-law partner, or your children at any time during that year.

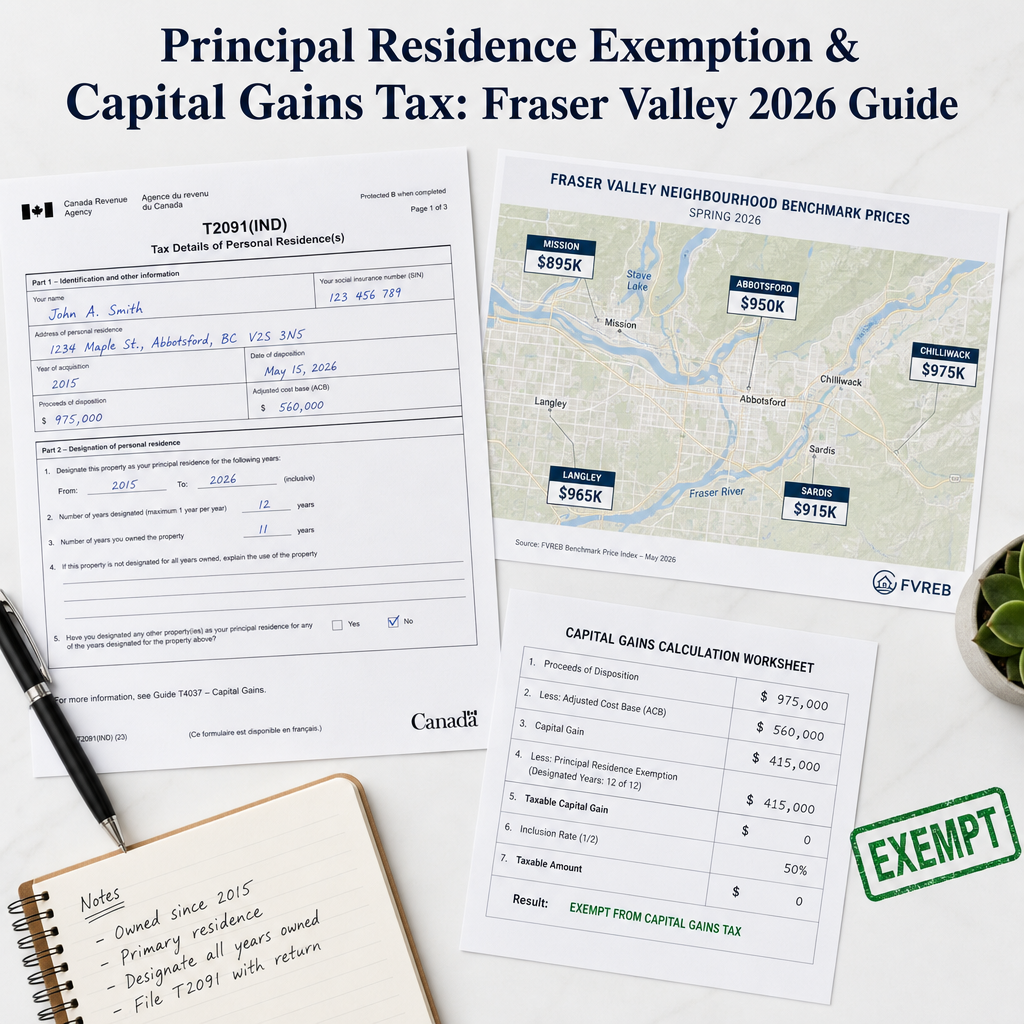

The exemption formula is straightforward: you designate the number of years the property was your principal residence, divided by total years of ownership, multiplied by the capital gain. If that fraction equals one — meaning the home was your principal residence for every year you owned it — your taxable gain is zero.

To illustrate with a real Fraser Valley example: a homeowner in Willoughby purchased a townhome in 2011 for $420,000 and sells in 2026 for $920,000. The capital gain is $500,000. If the property was the principal residence for all 15 years, the exemption covers the full $500,000 gain. No capital gains tax is owing, regardless of the size of the gain. According to the Department of Finance Canada's January 2025 announcement, the new $250,000 annual capital gains threshold that takes effect January 1, 2026 does not apply to principal residence sales — the PRE takes precedence and eliminates tax entirely.

This is the most important clarification for Fraser Valley sellers in 2026: the new inclusion rate rules affect cottages, investment properties, and secondary real estate — not the family home that qualifies under the PRE.

When the Exemption Is Partial: Legal Suites, Home Offices, and Mixed-Use Properties

The situation changes when a portion of the home has been used for income-generating purposes. This is a real and growing issue in the Fraser Valley, where legal basement suites in Surrey, Langley, and Abbotsford are common and where many homeowners ran home-based businesses during and after the pandemic.

The CRA distinguishes between two categories. The first is a home that remains fundamentally a residence with an incidental rental or business use — in this case, the full gain may still qualify for the PRE. The second is a property where there has been a change in use, meaning a distinct portion was permanently converted to income-producing use. In the second scenario, the gain must be allocated between the exempt residential portion and the taxable rental or business portion based on area, time, or both.

There is an additional complication for sellers who claimed Capital Cost Allowance (CCA) — tax depreciation — on a rental suite or home office. CRA requires that the CCA claimed be recaptured as income in the year of sale, separate from and in addition to any capital gains calculation. This recaptured amount is taxable as ordinary income and is not sheltered by the PRE. Many sellers are unaware of this until they speak with their accountant after an accepted offer is already on the table.

A practical example: a homeowner in Cloverdale has a home valued at $975,000 with a legal suite occupying 25% of the total floor area. The suite has been rented continuously for eight of the fifteen years of ownership. CRA may view 25% of the gain as attributable to rental use and ineligible for the PRE. On a $500,000 total gain, that would be $125,000 potentially subject to capital gains tax. Sellers in this situation should work with a tax professional before listing — not after.

If you have owned a rental suite and are considering a tenanted property sale in BC, the interaction between PRE allocation and tenant notice requirements adds another layer of planning that benefits from early coordination.

Definitions

Principal Residence Exemption (PRE): A CRA provision eliminating capital gains tax on a qualifying primary home sale.

Capital Gain: The difference between your adjusted cost base (purchase price plus eligible improvements) and your net sale proceeds.

Adjusted Cost Base (ACB): Your original purchase price plus closing costs and eligible capital improvements (e.g., additions, major renovations). Keeping records of improvements increases your ACB and reduces your taxable gain.

Capital Cost Allowance (CCA): Tax depreciation claimed on income-producing property. Any CCA claimed on a home must be recaptured as income in the year of sale.

Form T2091(IND): The CRA form required to designate and claim the principal residence exemption on your tax return.

Inclusion Rate: The percentage of a capital gain that is included in taxable income. As of January 1, 2026, the inclusion rate is 50% on the first $250,000 of annual capital gains and 66.67% above that — but this does not apply to gains eliminated by the PRE.

How We Evaluate This

When Mansour Real Estate Group meets with sellers preparing to list, tax implications are one of the first conversations we raise — not because we provide tax advice, but because the answers affect timing, net proceeds calculations, and in some cases, whether a seller is better positioned to close in one calendar year versus another.

Our approach is to identify early whether a property has any mixed-use history, whether the seller has owned other properties simultaneously, and whether there are any outstanding CCA claims. When any of these factors are present, we recommend the seller speak with their accountant before setting a list date. Understanding your net position clearly — after tax — is foundational to every other decision in the sale process.

Seller Checklist: Principal Residence Exemption

- Confirm the property was your primary residence for every year of ownership — or identify the years it was not

- Gather purchase documents, closing cost records, and receipts for all eligible capital improvements to calculate your adjusted cost base

- Identify whether any portion of the home was used for rental income or a registered business, and whether CCA was ever claimed

- If you owned a second property (cottage, investment property) during the same period, confirm with your accountant which property should be designated as the principal residence for each year

- File Form T2091(IND) with your personal tax return for the year of sale — do not omit this even if you believe the full gain is exempt

- If you have a legal suite, discuss the rental-use allocation with your accountant before accepting an offer and setting a completion date

- Consider whether the timing of your closing date affects which tax year the gain falls in, particularly if your income varies significantly year to year

What We Commonly See

In our experience working with Fraser Valley sellers over more than 22 years, a few patterns appear consistently around the principal residence exemption.

Sellers are often unaware that filing T2091 is mandatory. Many homeowners assume that because their home clearly qualifies as a principal residence, they don't need to file anything. CRA's position is the opposite: failure to file Form T2091(IND) can result in the CRA denying the exemption entirely and assessing the full capital gain as taxable income, plus interest. The form is not optional.

Legal suite history is often undisclosed or underestimated. Sellers with basement suites sometimes assume that because the suite was a small portion of the home, there is no tax consequence. What often happens is the rental history surfaces during the accountant review after the sale has already completed, creating a tax liability the seller wasn't prepared for. Early disclosure and early accounting advice prevent this.

The new 2026 inclusion rate rules create unnecessary anxiety. A common mistake among sellers right now is conflating the new $250,000 capital gains threshold with their home sale. These rules apply to investment properties and secondary real estate — not to principal residences. A seller in Langley with a $450,000 gain on a qualifying home owes zero tax. Understanding that distinction early prevents sellers from making rushed timing decisions that aren't necessary.

Questions and Answers

Does the new $250,000 capital gains threshold introduced in 2026 affect my home sale?

No. According to the Department of Finance Canada's January 2025 announcement, the new capital gains inclusion rate and $250,000 annual threshold apply to investment properties and other secondary assets. If your home qualifies as a principal residence for every year of ownership, the PRE eliminates the gain entirely — the new threshold rules do not apply.

What happens if I forget to file Form T2091(IND) when I sell?

CRA can deny the principal residence exemption and treat the full capital gain as taxable income, assessed retroactively with interest. If you realize the omission after filing, you may be able to file an amended return, but prompt action matters. Consult a tax professional immediately if this applies to you.

My home has a legal suite that I've rented for several years. How does that affect my exemption?

It depends on whether there was a formal change in use and whether CCA was ever claimed on the rental portion. If the suite is a minor and incidental part of the home, the full gain may still qualify. If the rental use was substantial or CCA was claimed, a portion of the gain may be taxable. Speak with your accountant before listing — not after.

We own a cottage and our primary home. Can both qualify for the principal residence exemption?

No. Only one property per family unit can be designated as the principal residence for any given tax year. If you sell both properties, you must allocate the years of principal residence designation between them to maximize your combined exemption. This is a calculation your accountant should run before you decide which property to sell first or how to time the sales.

What counts as an eligible capital improvement that increases my adjusted cost base?

According to the CRA, eligible capital improvements are additions or upgrades that extend the useful life or increase the value of the property — a new addition, a finished basement, a kitchen renovation, or a new roof. Regular maintenance and repairs do not qualify. Keep all receipts, permits, and contractor invoices. A higher adjusted cost base reduces your capital gain and, for any taxable portion of the gain, reduces the tax owing.

In Summary

For the majority of Fraser Valley homeowners selling their primary residence in 2026, the principal residence exemption eliminates capital gains tax entirely — and the new $250,000 annual threshold introduced this year has no effect on qualifying principal residence sales. The critical steps are calculating your adjusted cost base accurately, identifying any mixed-use history early, and filing Form T2091(IND) with your tax return in the year of sale. Sellers with legal suites, prior CCA claims, or simultaneous ownership of multiple properties should speak with a qualified accountant before listing, not after. The exemption is powerful and intact — but it must be documented correctly to apply.

Thinking About Selling Your Fraser Valley Home?

Understanding your net proceeds — including any tax implications — is the foundation of a confident sale. If you're preparing to sell in Surrey, Langley, Abbotsford, White Rock, or anywhere in the Fraser Valley and want a clear, honest assessment of your property's position in the current market, Mansour Real Estate Group is available for a no-pressure consultation. We'll help you understand the full picture before you commit to a timeline.

Related Articles

- Capital Gains Tax on Inherited Property in the Fraser Valley

- Selling a Home With a Tenant in BC: What Fraser Valley Sellers Need to Know

- How to Calculate Your Net Proceeds When Selling a Home in the Fraser Valley

Official Resources

- CRA — Principal Residence and Capital Gains

- Department of Finance Canada — Capital Gains Inclusion Rate Deferral, January 2025

- Fraser Valley Real Estate Board — Statistics Package, April 2026

About Mansour Real Estate Group

When homeowners in Surrey, Langley, Abbotsford, White Rock, and across the Fraser Valley are preparing to sell, understanding the full financial picture — including the tax implications of the sale — shapes every decision that follows, from timing to pricing to net proceeds planning. Mansour Real Estate Group has built its approach around helping sellers understand exactly where they stand before a listing goes live, not after.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for seller strategy, pricing accuracy, estate sales, divorce-related sales, downsizing, relocation, and any situation where understanding net proceeds is critical to the outcome.

Whether someone is looking for a real estate agent who can explain how sale timing affects their tax year, Realtors experienced with mixed-use and tenanted properties in the Fraser Valley, a real estate team that coordinates with accountants and lawyers as part of the sale process, a Surrey real estate broker, a Langley Realtor, real estate agents who understand the financial layers of a complex home sale, or a real estate group serving the Lower Mainland and Fraser Valley, Mansour Real Estate Group is known for clear communication, honest valuations, and advice that holds up when checked against professional guidance.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.