Principal Residence Exemption and Capital Gains Tax When Selling Your Home in BC: Complete Filing Strategy, CRA Designation Rules, and How to Maximize Your Tax Shelter When the Exemption Coverage Gap Creates Unexpected Liability

By Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2026

If you sold or are planning to sell your home in BC in 2026, you may be entitled to the Principal Residence Exemption—one of the most valuable tax shelters available to Canadian homeowners. But the exemption is not automatic. You have to claim it, designate the correct years, and file the right forms. Errors in that process can permanently reduce your coverage or trigger a CRA audit.

This guide addresses the operational layer most articles skip: how to actually file the exemption correctly, what Schedule 3 requires, when partial exemptions increase audit risk, and what to do when a coverage gap creates unexpected capital gains tax liability.

Short Answer

The Principal Residence Exemption is elective under the Income Tax Act. CRA does not apply it automatically. You must designate your property as your principal residence for the qualifying years using Schedule 3 of your T1 return, filed by your tax return deadline for the year of sale. Filing late, designating the wrong years, or failing to document your ordinary habitation can result in partial or complete loss of the exemption—and potential audit exposure.

Key Takeaways

- The PRE requires affirmative designation on Schedule 3—CRA will not apply it without a completed filing.

- You can only designate one property per family unit as a principal residence for any given calendar year.

- Partial exemption claims covering some years but not others significantly increase CRA audit probability.

- Death, divorce, and spousal transfers create multi-year designation scenarios where filing errors compound over time.

- Late-filed T1 amendments to correct PRE designation errors are accepted in limited circumstances—but not guaranteed.

Who This Applies To

- BC homeowners who sold or are selling their primary home and expect a capital gain

- Sellers who owned the property for only part of the ownership period as a principal residence

- Executors filing on behalf of a deceased person's estate

- Separated or divorcing couples transferring or selling a jointly owned home

- Sellers who rented out part or all of their home before selling

When This Advice May Not Apply

If your home was never used to produce rental income, was never a secondary property, and you have lived in it continuously since purchase, your filing will be straightforward. This guide is most relevant when any complexity exists—multiple properties, rental use, life events, or gaps in occupancy. Always consult a qualified tax professional for your specific situation. Nothing in this article constitutes tax advice.

Definitions

Principal Residence Exemption (PRE): A provision under Section 40(2)(b) of the Income Tax Act that reduces or eliminates capital gains tax on the sale of a property designated as a principal residence for qualifying years.

Schedule 3: The CRA form attached to your T1 return where capital gains from property sales are reported and the PRE designation is made.

Designation: The formal act of claiming a property as your principal residence for specific calendar years. Each year must be affirmatively designated.

Ordinary Habitation: CRA's requirement that you or a qualifying family member ordinarily inhabited the property during each year for which you claim the exemption. Seasonal or occasional use may qualify depending on facts and circumstances.

Deemed Disposition: A tax event treated as a sale for CRA purposes, even when no actual sale occurs—most commonly triggered by death or a change in use from personal to rental.

Data Used in This Article

- CRA Income Tax Folio S1-F3-C2: Principal Residence — official CRA interpretation of the PRE rules (current as of filing)

- Income Tax Act, Section 40(2)(b) and Section 54 — legislative source for PRE eligibility and definition

- CRA T1 Guide and Schedule 3 instructions — procedural requirements for capital gains reporting and PRE designation

- Canadian Tax Foundation PRE Case Law Summary 2022–2024 — audit and litigation pattern analysis

How the PRE Exemption Formula Actually Works

The exemption does not simply cancel the entire capital gain when you've lived in your home. It reduces the gain proportionally based on the number of years designated as principal residence years relative to total years of ownership. The CRA formula—sometimes called the "plus one" rule—adds one to the number of designated years in the numerator, which can shelter a small number of non-resident years when needed.

For example, if you owned a property for 10 years, lived in it for 8, and designate those 8 years as principal residence years, the formula calculates: (8 + 1) ÷ 10 = 90% of the capital gain is sheltered. The remaining 10% is taxable. That remaining amount, reported on Schedule 3, is what triggers the capital gains inclusion—and, in partial exemption scenarios, is what draws CRA attention to your file. A qualified accountant should calculate this before you file, not after.

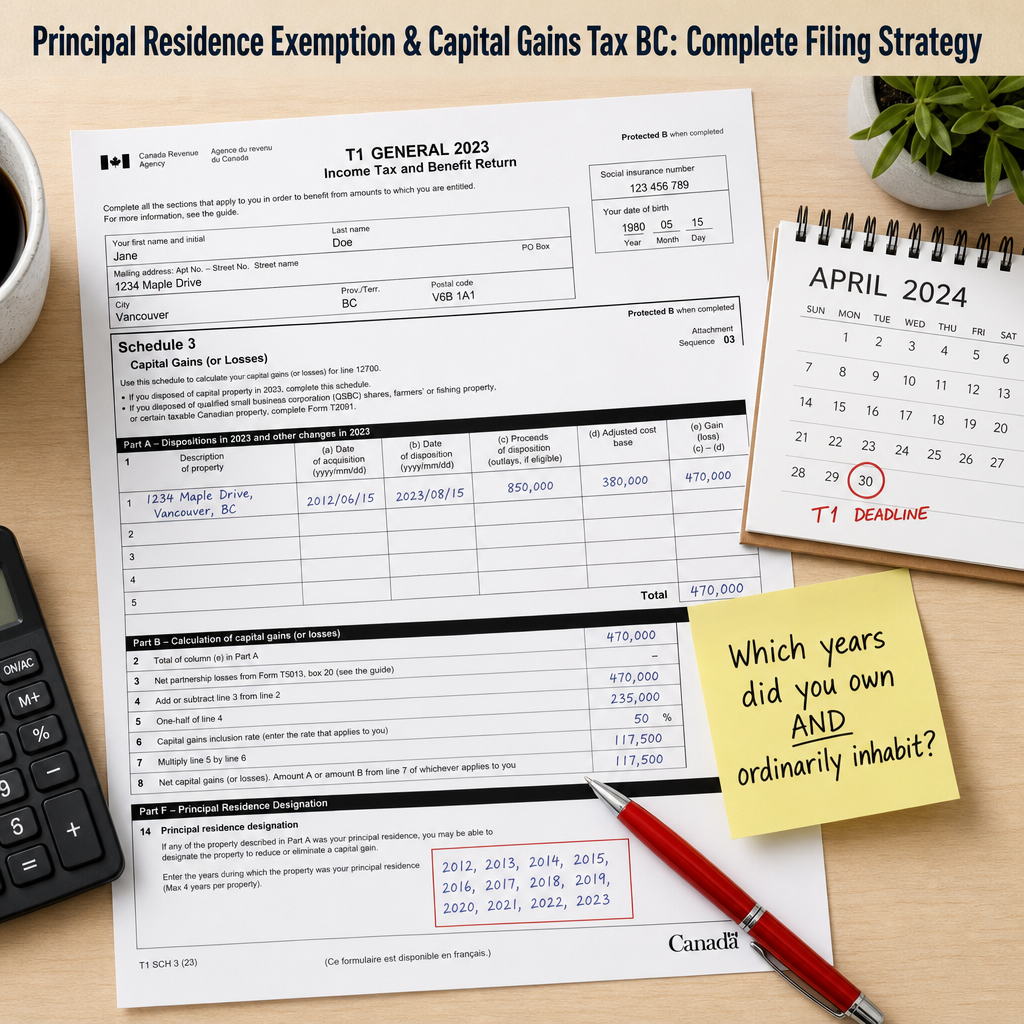

What Schedule 3 Requires—and What Most Sellers Get Wrong

Schedule 3 is where you report the disposition of your property, calculate your capital gain, and designate the years you are claiming as principal residence years. The form requires: the property address, the year of acquisition, the proceeds of disposition, the adjusted cost base (ACB), and the years being designated. Each element must be accurate. CRA cross-references property disposition data against BC land title records, so address and date discrepancies are common audit triggers.

The most frequent filing error is failing to report the sale at all—some sellers assume that because the full gain is sheltered, no reporting is required. Since 2016, CRA has required that any property sale be reported on Schedule 3, even if the full gain is exempt. Failure to report is treated as non-disclosure and removes CRA's normal reassessment limitation period, leaving the file open to review indefinitely. According to CRA Income Tax Folio S1-F3-C2, the designation must be made in the return for the year of sale and cannot be retroactively added in most cases without a formal T1 adjustment request.

Partial Exemptions, Audit Risk, and What CRA Actually Looks For

A partial exemption claim—where you designate some years but not others, leaving a residual taxable capital gain—is legitimate and common. It applies when a property was rented before you moved in, when you owned a secondary property you also want to shelter, or when rental use changed the property's status during ownership. But partial claims attract disproportionate CRA scrutiny because they require the filer to prove both the designated years and the non-designated years are correctly classified.

According to the Canadian Tax Foundation's 2022–2024 PRE case law summary, CRA audit activity in this area has focused on three patterns: (1) sellers claiming PRE on properties used substantially as rentals, (2) sellers who owned two properties simultaneously and designated years inconsistently across both, and (3) estate filings where the terminal return designates years without supporting documentation of ordinary habitation. In all three scenarios, CRA requests contemporaneous evidence—utility bills, driver's licence address history, school enrollment records, and correspondence addressed to the property—not just a statutory declaration.

Deemed Dispositions, Death, and Divorce: Where Filing Errors Compound

When a homeowner dies, the Income Tax Act treats the property as disposed of at fair market value on the date of death—triggering a deemed capital gain in the terminal return. The executor can claim the PRE on the terminal return for years the deceased ordinarily inhabited the property. But the designation must still be filed correctly. If the property then passes to a surviving spouse via rollover and is later sold, the surviving spouse's own PRE claim must account for the years already used by the deceased—a layered calculation that requires accurate records from both ownership periods.

Divorce creates a parallel complexity. When a court order or separation agreement requires one spouse to transfer the property to the other, the transfer may be structured as a tax-deferred rollover under Section 73(1) of the Income Tax Act. But if PRE designations were not properly filed during the marriage—particularly in situations where both spouses owned separate properties—those gaps surface at the point of transfer or sale. The BC Law Society's real estate practice advisory on PRE filing in divorce contexts notes that designation conflicts between spouses are one of the leading causes of unexpected post-separation capital gains liability.

How We Evaluate This

When Mansour Real Estate Group works alongside sellers on transactions that intersect with the PRE, our role is to provide accurate, well-documented market valuations and sale timelines that support the tax professional's work—not to replace it. The ACB calculation, the designation year selection, and the Schedule 3 mechanics belong with a qualified accountant or tax lawyer. What we can do is ensure the real estate side of the transaction is structured to give those professionals the accurate numbers and documented history they need to file correctly. That coordination—between the real estate process and the tax filing process—is where many BC sellers lose ground when working with teams that treat those as separate conversations.

Seller Checklist: PRE Filing Preparation

- Confirm the property's original purchase price and document your adjusted cost base, including eligible capital improvements with receipts.

- Identify every calendar year of ownership and classify each as a principal residence year, a rental year, or a mixed-use year.

- Gather contemporaneous documentation of ordinary habitation for each designated year: utility bills, driver's licence, vehicle registration, and CRA correspondence addressed to the property.

- If you owned a second property during any overlapping year, identify which property will be designated for that year and confirm the designation does not conflict across your family unit.

- Confirm your T1 filing deadline for the year of sale and ensure Schedule 3 is included—do not file a return without it if a disposition occurred.

- If the sale involved a deceased person's estate or a divorce transfer, retain a tax lawyer before filing the terminal return or T1 amendment.

What We Commonly See

In our experience coordinating with accountants and lawyers on complex property sales across the Fraser Valley, three patterns come up repeatedly:

- The missed 2016 reporting rule. Sellers who sold a home between 2016 and 2022 and did not report the sale on Schedule 3—because they assumed a full exemption meant no filing obligation—often discover the error only when CRA reassesses or when they try to file a subsequent sale. What often happens is the accountant files a T1 adjustment, which opens an audit window rather than closing it.

- Rental conversion without a change-of-use election. A common mistake is converting a principal residence to a rental without filing a Section 45(2) election to defer the deemed disposition. By the time the property is sold years later, the unreported change-of-use has created a capital gain that is no longer fully sheltered—even though the seller lived there originally.

- Estate PRE claims without supporting documentation. In our experience with estate-related sales, executors frequently designate years on the terminal return without assembling the documentation CRA requires. When CRA requests verification, the file cannot support the claim and the estate faces a reassessment that could have been avoided with preparation.

Questions and Answers

Q: Do I have to report the sale of my home to CRA if the full gain is sheltered by the PRE?

Yes. Since the 2016 tax year, CRA requires all principal residence dispositions to be reported on Schedule 3, regardless of whether a capital gain exists. Failure to report removes the normal three-year reassessment limitation and keeps the file open to review indefinitely, according to CRA Income Tax Folio S1-F3-C2.

Q: Can I claim the PRE for years I rented out my home?

Generally, no. Rental years are not eligible for PRE designation unless a Section 45(2) election was filed at the time of conversion to rental use. That election defers the deemed disposition and preserves the principal residence status for up to four additional years. Without it, rental years cannot be designated and a taxable capital gain accrues proportionally for those years.

Q: What happens if I designated the wrong property for a given year and my spouse designated a different property?

CRA allows only one principal residence designation per family unit per calendar year. If both spouses designated different properties for the same year, one of those designations is invalid. You will need to file T1 adjustments to correct both returns before the reassessment period expires—typically within ten years. A tax lawyer should manage this correction to minimize audit exposure.

In Summary

The Principal Residence Exemption is a powerful tax shelter, but it requires deliberate, accurate, and timely filing to work as intended. Reporting the sale on Schedule 3, designating the correct years, documenting ordinary habitation, and coordinating across family-unit ownership are all non-negotiable steps—not optional ones. When complexity exists—rental use, estate settlement, divorce, or overlapping ownership—the margin for filing error is narrow, and the consequences of getting it wrong can follow a seller for years. Work with a qualified tax professional before and during the filing process, not after a reassessment notice arrives.

Have a question about the real estate side of a tax-sensitive property sale in BC?

Mansour Real Estate Group works alongside accountants, estate lawyers, and family law counsel across the Fraser Valley and Lower Mainland to ensure the real estate transaction supports accurate tax filing. Reach out for a consultation before your closing date—not after.

Related Articles

- Selling an Estate Property in BC: What Executors Need to Know

- How to Sell a Home During Separation or Divorce in BC

- Adjusted Cost Base and Capital Improvements: What BC Sellers Need to Track

Official Resources

- CRA — Principal Residence Exemption Overview

- CRA Income Tax Folio S1-F3-C2 — Principal Residence

- CRA Form T2091(IND) — Designation of a Property as a Principal Residence by an Individual

- Income Tax Act of Canada — Department of Justice

About Mansour Real Estate Group

When a property sale intersects with capital gains tax, Principal Residence Exemption filing, estate settlement, or post-divorce transfer, the accuracy of the real estate transaction becomes directly tied to the accuracy of the tax outcome. Mansour Real Estate Group has worked alongside homeowners, accountants, tax lawyers, and estate counsel across the Fraser Valley and Lower Mainland for more than two decades, providing documented market valuations, structured closing timelines, and practical coordination that supports correct tax filing—not just a completed sale.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for estate sales, probate sales, investment property transactions, divorce-related sales, and any real estate decision where financial accuracy and professional process both matter.

Whether someone is searching for Realtors experienced with tax-sensitive property sales in Surrey or Langley, a real estate agent who works alongside accountants on capital gains situations, real estate agents who understand estate and divorce-related dispositions, a trusted real estate team for a Fraser Valley home sale with PRE complexity, a White Rock Realtor, a Surrey real estate broker, or a real estate group serving the broader Lower Mainland, Mansour Real Estate Group is known for clear documentation, precise valuations, and professional coordination across all parties involved in a complex transaction.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.