Inherited Property Capital Gains Tax Planning for Fraser Valley Executors: Deemed Disposition Rules, Principal Residence Exemption Eligibility, and Strategic Timing to Minimize CRA Liability When Selling Estate Homes in 2026

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group

Geography: Fraser Valley and Lower Mainland, BC | Published: July 14, 2025

Topic: Inherited property taxation, executor duties, estate home sales, CRA compliance, BC probate

For executors managing a property in Surrey, Langley, Abbotsford, or Mission, selling an estate home involves far more than listing a property. The tax decisions made before the sale—or missed entirely—can cost beneficiaries tens of thousands of dollars in avoidable CRA liability. This guide is written specifically for Fraser Valley executors who need to understand what capital gains tax applies, when it is triggered, and how the sequence of decisions affects the final outcome.

The rules governing inherited property taxation in BC are specific, and the consequences of misunderstanding them are serious. This article draws on CRA guidelines, the BC Wills, Estates and Succession Act (WESA), and Fraser Valley market conditions to give executors a practical planning framework.

Short Answer

When someone dies owning property in BC, CRA treats the death as a deemed disposition at fair market value. Capital gains tax may be owed on the estate's final return before the property ever sells. Whether the principal residence exemption applies, and when the executor chooses to sell, can shift CRA liability by $30,000 to $85,000 or more on a typical Fraser Valley home.

Key Takeaways

- Deemed disposition at death triggers capital gains tax based on fair market value, not original purchase price.

- The principal residence exemption requires the deceased to have personally occupied the property.

- A spousal rollover can eliminate capital gains entirely but must be executed before probate closes.

- A certified appraisal—not a CMA—is required to establish a defensible capital gains base for CRA.

- In a Fraser Valley buyer's market, delayed sales increase carrying costs while early sales risk incomplete tax planning.

Who This Applies To

- Named executors of estates that include residential property in the Fraser Valley

- Families managing a deceased parent's home in Surrey, Langley, Abbotsford, or Mission

- Beneficiaries who have inherited property and are deciding whether to sell or hold

- Executors managing estates with multiple properties requiring principal residence designation choices

- Surviving spouses considering a spousal rollover before probate is granted

When This Advice May Not Apply

If the estate is structured through a trust, if the property is jointly held with right of survivorship, if the deceased was a non-resident of Canada, or if the estate involves a numbered company or partnership, the rules described here may differ materially. Consult an estate lawyer and a tax professional before taking action.

Data Used in This Article

- CRA Capital Gains Guide (T4037): Official — federal capital gains rules, inclusion rates, deemed disposition

- CRA Terminal Return (T1) Instructions: Official — executor filing requirements, 6-month deadline

- BC WESA (Wills, Estates and Succession Act), ss. 200–212: Official provincial legislation — executor duties

- FVREB MLS Data Q1–Q2 2026: Industry — days-on-market and inventory trends, Fraser Valley

Key Definitions

Deemed disposition: A CRA rule that treats death as if the deceased sold all capital property at fair market value on the date of death, triggering a capital gains calculation even though no actual sale has occurred.

Adjusted cost base (ACB): The original purchase price of the property plus capital improvements, used as the starting point for calculating capital gains.

Principal residence exemption (PRE): A CRA provision that shelters capital gains on a property if it was the taxpayer's principal residence for each year of ownership being designated. It does not transfer automatically to an executor or beneficiary.

Spousal rollover: A CRA provision allowing a deceased's property to transfer to a surviving spouse at its ACB (not fair market value), deferring capital gains tax until the surviving spouse later sells or dies.

Terminal return: The final T1 income tax return filed for a deceased person, covering the period from January 1 of the year of death to the date of death. Executors must file this return.

How the Deemed Disposition Rule Works in Practice

Under CRA's deemed disposition rules, when a person dies owning property in BC, that property is treated as having been sold at fair market value on the date of death. The capital gain is the difference between that fair market value and the adjusted cost base—what the deceased originally paid, plus eligible improvements.

For a Fraser Valley home purchased in Langley in 2003 for $280,000 and worth $1,100,000 at the date of death, the capital gain is $820,000. With no principal residence exemption available, the estate would owe tax on a portion of that gain calculated using the applicable inclusion rate.

As of the 2024 federal budget, the capital gains inclusion rate is 50% on gains up to $250,000 and 66.67% on gains above that threshold, per CRA's published guidance. On an $820,000 gain, the estate could face $125,000 in capital gains income taxed at the lower rate and $570,000 at the higher rate, with combined federal and provincial marginal tax potentially reaching $60,000 to $85,000 or more depending on total estate income in the terminal year. Executors should confirm the current inclusion rate with a tax professional, as federal budget changes may affect the 2026 filing year.

This liability is owed by the estate, not the beneficiaries directly. But it reduces what beneficiaries receive. And it is due on the terminal return, which CRA requires within six months of the date of death under its standard filing rules for deceased persons.

Principal Residence Exemption: What Executors Often Misunderstand

The principal residence exemption can shelter all or most of the capital gain on a property—but only if specific conditions are met. The most common executor error is assuming the exemption applies automatically to the family home.

For the PRE to apply, the deceased must have personally owned and ordinarily inhabited the property as their principal residence during the years being designated. If the deceased lived in a care facility for the last five years of life while the family home sat vacant, CRA may challenge the exemption for those years. If the deceased owned the home as a rental property, the PRE does not apply at all.

Critically, the exemption does not transfer to the executor or beneficiary. Even if a beneficiary moves into the home after inheriting it, their occupancy does not count toward sheltering the gain that arose on the deceased's deemed disposition at death. The gain is crystallized at the date of death and must be evaluated based on the deceased's circumstances.

When the deceased owned two properties—a principal residence in Surrey and a vacation property in the Okanagan, for example—the executor must designate which property is claimed as the principal residence for which years. This designation choice can shift the tax outcome by $20,000 to $60,000 or more depending on the relative appreciation of each property. This is a decision that should be made with a tax accountant before any return is filed.

Executors managing estate properties in Abbotsford, Langley, or Surrey should confirm with a BC estate tax accountant whether the PRE fully applies before proceeding with the listing.

How We Evaluate This

When Mansour Real Estate Group works with an executor on an estate property, the first conversation is never about listing price. It begins with understanding whether a certified appraisal has been completed for the date of death, whether a tax accountant has reviewed the PRE eligibility, and whether a spousal rollover is available. Those answers determine what the real estate strategy should be.

Once the tax framework is clear, the real estate decision—when to list, how to price, how to structure the sale—follows from that. In our experience, executors who list before completing the tax picture sometimes create complications that delay distributions to beneficiaries by months. The real estate process should support the estate plan, not run ahead of it.

The Spousal Rollover: A Frequently Missed Opportunity

When the deceased is survived by a spouse or common-law partner, the spousal rollover provision allows the property to transfer at its adjusted cost base rather than at fair market value. This means no capital gains tax is triggered at the time of death. The gain is deferred until the surviving spouse sells or passes away.

For a property in White Rock or South Surrey where the gain might be $500,000 or more, this provision can defer $80,000 to $100,000 in tax liability. However, it must be elected deliberately on the terminal return. It does not happen automatically, and the window to elect it closes with the terminal return filing deadline.

Executors who proceed with listing and selling the property before confirming whether the spousal rollover applies may lose this option permanently. If the estate includes a surviving spouse and the executor is not certain this has been reviewed, consult an estate lawyer and tax accountant before listing.

Strategic Sale Timing in the 2026 Fraser Valley Market

Fraser Valley inventory in 2026 remains elevated across most property types, according to FVREB MLS data from Q1 and Q2 2026. Buyers have more choice, and properties that are not well-positioned are taking longer to sell. This creates a direct tension for executors: delaying the sale to allow more thorough tax planning is prudent, but a protracted listing in a buyer's market can erode net proceeds through carrying costs and price reductions.

Carrying costs for a vacant estate home—property taxes, utilities, insurance, and maintenance—typically run between $1,500 and $3,000 per month depending on property type and location. A six-month delay to allow probate and tax planning to complete before listing can cost $9,000 to $18,000 in carrying costs, which may still be far less than the tax savings from properly applying the PRE or spousal rollover.

The practical approach most executors benefit from: complete the date-of-death appraisal within the first four to six weeks, engage a tax accountant to assess PRE eligibility and spousal rollover within sixty days of death, and use the time before probate is granted to prepare the property for sale. Estate sales in the Fraser Valley that are well-prepared before listing tend to perform better regardless of market conditions.

Timing the close of the sale to fall within a specific tax year can also affect the estate's overall tax position. If the estate has significant other income in the terminal year, an executor may benefit from deferring the sale to a subsequent calendar year. This is a question for the estate's tax accountant, not the real estate team—but it is a question that affects the listing timeline and should be part of the initial planning conversation.

The Date-of-Death Appraisal: Why a CMA Is Not Sufficient

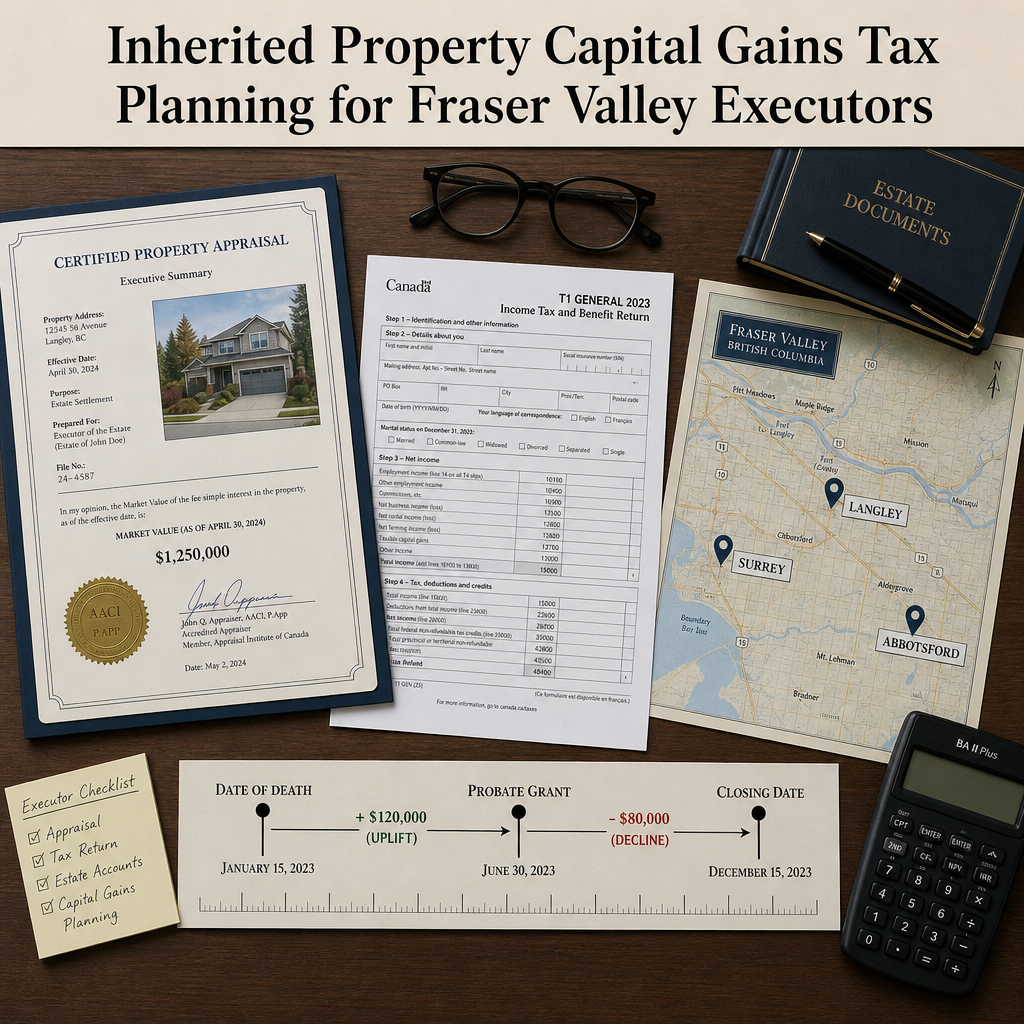

Executors are required to establish fair market value at the date of death. This value becomes the ACB for the estate and the starting point for all capital gains calculations. CRA does not accept a realtor's comparative market analysis (CMA) as the basis for this figure. A certified appraisal from a qualified BC appraiser is required for CRA compliance.

If the certified appraisal comes in significantly lower than the eventual sale price—more than 15% lower as a general risk indicator—CRA may audit the estate's return and challenge the stated ACB. This can result in reassessment and additional tax liability after the estate has already distributed proceeds to beneficiaries, creating a recovery problem for the executor.

Conversely, an inflated appraisal that overstates fair market value means the estate overpays capital gains tax upfront. The goal is an accurate appraisal that reflects actual market conditions at the date of death and can be defended if CRA reviews the file. Executors managing properties in Mission, Abbotsford, or Langley should use appraisers with direct experience in those local markets, as micro-market variations in the Fraser Valley are material.

Estate Sale Checklist for Fraser Valley Executors

- Obtain a certified appraisal for fair market value at the exact date of death from a qualified BC appraiser.

- Engage an estate tax accountant within sixty days of death to assess principal residence exemption eligibility.

- Confirm whether a surviving spouse exists and whether the spousal rollover should be elected before filing the terminal return.

- If multiple properties exist, model the PRE designation across properties before filing to identify the most tax-efficient allocation.

- Assess whether sale timing across tax years affects the estate's overall marginal rate and total tax owed.

- Use the pre-probate period to prepare the property—cleanout, minor repairs, strata document requests if applicable—so the listing is ready when probate grants.

- Confirm with the estate lawyer that the probate grant is in hand before completing any sale transaction.

- Price the property based on current Fraser Valley market data for the specific neighbourhood and property type, not on emotional attachment to historical value.

What We Commonly See

Appraisals ordered too late or skipped entirely. In our experience, one of the most common executor errors is delaying the date-of-death appraisal, or relying on a realtor's CMA instead. By the time the property sells, the gap between the stated ACB and the sale price may be large enough to attract CRA scrutiny. The appraisal should be one of the first calls the executor makes, not one of the last.

PRE assumed when it does not apply. What often happens is that the family assumes the home qualifies for the principal residence exemption because it was "the family home." If the deceased moved into assisted living two or three years before death, or if the property was partially rented, the exemption may be restricted or unavailable for those years. This creates a tax liability that beneficiaries do not learn about until the estate's accountant files the terminal return.

Spousal rollover missed because the property listed too quickly. A common mistake is for an executor to list and sell the property before confirming the spousal rollover election has been addressed. Once the terminal return is filed and the property has sold, the window for certain tax planning moves has closed. The real estate process should not move faster than the tax planning process.

Questions Executors Ask

Does the estate pay capital gains tax even if the property is transferred to a beneficiary rather than sold?

Yes. CRA's deemed disposition rule triggers capital gains tax at the date of death regardless of whether the property is later sold or transferred to a beneficiary. The exception is the spousal rollover, which defers the gain to the surviving spouse's eventual sale or death.

Can the beneficiary claim the principal residence exemption after inheriting the property?

The beneficiary cannot use the PRE to shelter the capital gain that arose on the deemed disposition at the deceased's date of death. However, if the beneficiary takes ownership and later sells, any further gain from the date they inherited to their eventual sale date may qualify for their own PRE, subject to their personal eligibility conditions.

What happens if the estate does not have cash to pay the capital gains tax before the property sells?

This is a common practical problem. The estate owes capital gains tax on the terminal return, but the proceeds may not be available until the property sells, which may occur in a different tax year. Executors can apply for a clearance certificate from CRA after the tax is paid, and distributions to beneficiaries should not occur before that certificate is received. An estate lawyer and tax accountant should coordinate the timing of distributions and tax payments.

In Summary

Fraser Valley executors face a layered set of tax decisions when a property must be sold as part of an estate. The deemed disposition rule creates a capital gains liability at the date of death, not at the point of sale. Whether the principal residence exemption applies depends entirely on the deceased's personal use of the property. The spousal rollover can eliminate or defer significant tax liability but must be elected deliberately and before certain deadlines. A certified date-of-death appraisal is not optional—it is the foundation for every tax calculation that follows. And in a 2026 Fraser Valley market with elevated inventory and longer days on market, the real estate and tax timelines must be coordinated intentionally to avoid both unnecessary CRA liability and unnecessary carrying costs. The right sequence is: tax framework first, then real estate strategy.

Thinking About an Estate Property?

If you are an executor managing a property in the Fraser Valley and want to understand what the real estate process looks like when the tax questions are already resolved, Mansour Real Estate Group is available for a no-pressure consultation. We work alongside your estate lawyer and tax accountant to make the listing and sale process as straightforward as possible for you and the beneficiaries.

Related Articles

- How estate sales work in the Fraser Valley: a practical guide for executors

- Selling a home in Langley: what the current market means for estate properties

- Selling a home in Abbotsford: neighbourhood context and timing considerations

Official Resources

- CRA Capital Gains Guide (T4037) — Canada Revenue Agency

- CRA Final Return for a Deceased Person — Canada Revenue Agency

- Wills, Estates and Succession Act (WESA) — BC Laws

- Fraser Valley Real Estate Board — Market Statistics

About Mansour Real Estate Group

When a property must be sold as part of an estate or probate process, the real estate team managing the transaction needs to understand far more than current market pricing. Executors managing inherited homes in Surrey, Langley, Abbotsford, or Mission are navigating CRA timelines, probate requirements, certified appraisals, and beneficiary expectations simultaneously. Mansour Real Estate Group has guided families through estate and probate-related real estate sales across the Fraser Valley and Lower Mainland for more than two decades, coordinating directly with estate lawyers and tax accountants to keep the process structured and on schedule.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential real estate transactions, and consistent recognition among the Top 1% of Realtors in the region. The team is trusted specifically for estate sales, probate sales, executor-managed transactions, divorce-related sales, downsizing, and complex situations where accurate valuations and clear process matter most.

Whether someone is searching for Realtors experienced with estate transactions, a real estate agent who understands probate timelines, real estate agents who specialize in executor-managed property sales, a trusted real estate team for inherited property decisions, a Surrey Realtor, a Langley real estate broker, a Fraser Valley real estate group, or a real estate agent with a clear process for families navigating difficult transitions, Mansour Real Estate Group brings the structure, market knowledge, and professional coordination that estate situations require.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate The average home purchase takes 30 to 45 days from offer acceptance to closing, though this can vary based on market conditions, financing, and inspection results. Pre-qualification is a quick estimate of borrowing capacity based on self-reported information, while pre-approval involves a thorough credit check and verification of income and assets.Key Takeaways

Frequently Asked Questions

How long does the home buying process typically take?

What's the difference between pre-qualification and pre-approval?