How to Negotiate and Structure Seller Concessions Without Destroying Net Proceeds in a Buyer's Market

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2026

In a buyer's market, concession requests are common. Buyers ask for closing cost help, repair allowances, rate buy-downs, and home warranties. Most sellers instinctively evaluate these requests by their face value — a $20,000 ask feels like a $20,000 cost. It is not. The actual impact on your net proceeds depends entirely on how a concession is structured, and whether a price reduction, a credit, or a third-party offer is the right tool for that specific request.

This article is written for sellers in Surrey, Langley, Abbotsford, South Surrey, White Rock, and the broader Fraser Valley who are navigating a buyer's market where concession requests have become a routine part of offers. Understanding the math — and the negotiating mechanics — can protect several thousand dollars in final proceeds without losing the deal.

Short Answer

Not all concessions cost the same. A $20,000 price reduction reduces your net proceeds by more than a $20,000 closing cost credit because commission is calculated on the sale price. In a Fraser Valley buyer's market with an 11% sales-to-active ratio as of March 2026, structuring concessions correctly — and reading the real reason behind each request — is one of the most underused seller protections in current deal negotiations.

Key Takeaways

- A $20,000 price reduction costs more than a $20,000 closing cost concession in net proceeds due to commission math.

- Home warranties ($500–$1,500) and rate buy-downs address buyer concerns at a fraction of the cost of cash concessions.

- Concession requests often signal a financing gap or inspection concern — resolving the real issue protects your position.

- Sellers with a single competing offer face maximum leverage loss; structuring alternatives early prevents reactive conceding.

- In a buyer's market, blanket concession offers before negotiation begins give away leverage without gaining anything in return.

Who This Applies To

- Sellers in Surrey, Langley, Abbotsford, South Surrey, White Rock, or North Delta with active listings in 2026

- Sellers who have received an offer with a concession request and are evaluating whether to accept, counter, or restructure

- Sellers preparing a listing strategy and considering whether to pre-offer concessions

- Estate sellers, divorce-related sellers, or downsizing homeowners who need to protect a defined net proceeds floor

When This Advice May Not Apply

If you have multiple competing offers, concession structuring becomes less urgent — market competition does the work. If your property has documented deficiencies disclosed in a pre-listing inspection, some concessions may be appropriate and expected rather than negotiable. Consult your real estate professional and, where legal or tax questions arise, a qualified lawyer or accountant.

Data Used in This Article

- Fraser Valley Real Estate Board (FVREB), March 2026: Sales-to-active listings ratio at 11%, confirming buyer's market conditions. Official board data.

- BC Real Estate Association standard offer forms: Concession mechanics as applied in BC purchase contracts. Official regulatory context.

- Mansour Real Estate Group transaction experience: Concession negotiation outcomes observed across Fraser Valley transactions. Internal professional experience.

- Closing cost structure in BC: Commission, property transfer tax, and legal fee sequencing as applied to net proceeds calculations. Industry-standard practice.

Why Concession Structure Matters More Than Concession Size

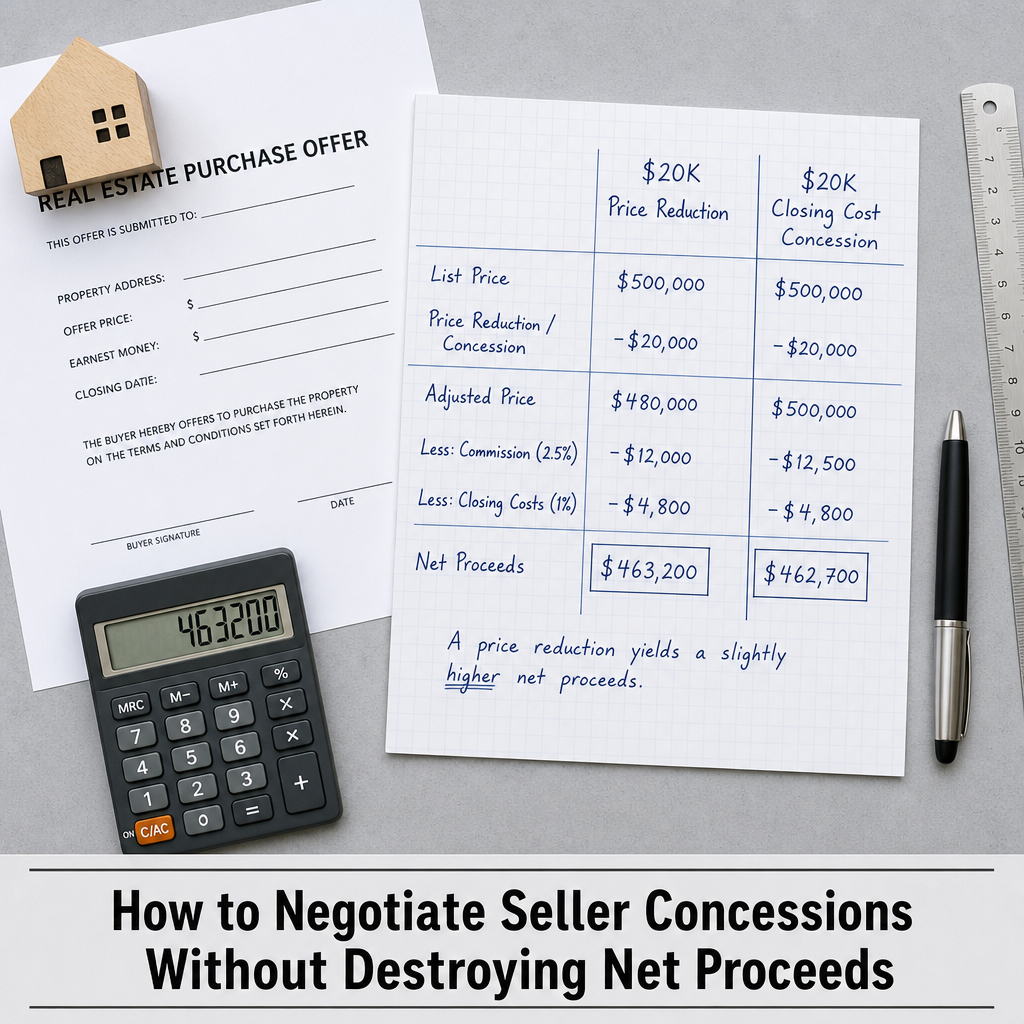

Here is a comparison that surprises most sellers. If your accepted offer is $800,000 and a buyer requests a $20,000 price reduction, your sale price drops to $780,000. Commission — typically calculated as a percentage of the sale price — is now calculated on $780,000, not $800,000. Your net proceeds shrink by the full $20,000 plus the commission difference on that reduction.

If instead you agree to a $20,000 closing cost credit — structured as a concession paid at completion — the sale price remains at $800,000. Commission is still calculated on $800,000. Your net proceeds reduction is $20,000, not $20,000 plus a commission drag. The difference is not enormous on a single transaction, but across a $15,000–$25,000 closing cost concession request, the structuring choice can save sellers $500–$1,200 in real dollars. In a buyer's market where you may already be working at a compressed price, that difference is worth protecting.

Reading What a Concession Request Actually Means

A buyer asking for closing cost help is usually not asking because they want free money. They are often asking because they are stretched on down payment, have a financing gap between approval and comfort, or are nervous about carrying costs in the first year. Understanding that distinction gives you negotiating options a blanket cash concession does not.

A rate buy-down — where the seller contributes funds toward reducing the buyer's mortgage rate by 0.25–0.5% — addresses the same underlying concern at a cost of roughly $3,000–$6,000, well below a $20,000 cash concession. According to transaction experience at Mansour Real Estate Group, buyers who accept a structured rate buy-down in place of a price reduction consistently proceed to completion at the same rate as buyers who receive cash credits — meaning the lower-cost tool achieved the same deal outcome.

A repair allowance request is different again. Here the buyer is signalling inspection anxiety — they found something in the property condition disclosure or the inspection that makes them nervous about future costs. The right response is often not a repair allowance, but either a pre-listing repair with documentation or a specific credit tied to a defined cost estimate, not an open-ended allowance. Open-ended repair credits have a way of expanding. Defined credits — backed by quotes — do not.

How We Evaluate This

When a concession request arrives, the first step at Mansour Real Estate Group is not to evaluate the dollar amount — it is to identify what the request signals about the buyer's position. Is this a financing constraint, an inspection reaction, or a negotiating habit? Each answer points to a different response strategy.

The second step is to calculate the net proceeds impact of each available response — price reduction, closing cost credit, third-party offer (warranty, buy-down), or structured repair credit — and present those options to the seller with the math visible. Sellers who see the actual numbers make better decisions than sellers who react to the emotional weight of a concession request. In a buyer's market with 40–60+ day DOM averages across parts of the Fraser Valley, the temptation to accept the first reasonable offer without pushing back on concession structure is real and often costly.

Seller Concession Checklist

- Before listing, calculate your net proceeds floor — the minimum acceptable amount after commission, legal fees, and any known costs.

- Obtain a pre-listing inspection to remove inspection-driven concession leverage from buyers before offers arrive.

- When a concession request arrives, ask your realtor to identify whether it reflects a financing gap, inspection concern, or negotiating tactic.

- Compare a $20,000 price reduction versus a $20,000 closing cost credit using actual commission and fee calculations — not face value.

- Before offering cash credits, evaluate whether a home warranty ($500–$1,500) or rate buy-down ($3,000–$6,000) addresses the same buyer concern.

- For repair requests, obtain contractor quotes and offer a defined credit, not an open-ended repair allowance.

- Do not pre-offer concessions in your listing without a clear strategic reason — they reduce leverage before negotiation begins.

What We Commonly See

In our experience, sellers in a buyer's market most often give up proceeds unnecessarily in three situations. First, they accept a price reduction when a closing cost credit would have cost less and achieved the same result — because no one ran the comparison math before the counteroffer was signed. Second, they offer a home warranty or rate buy-down as an afterthought in a counteroffer, when positioning it earlier as a proactive buyer protection would have prevented the cash concession request from arriving at all.

Third — and most costly — sellers with a single offer in a slow market accept all concession terms as written rather than countering on structure. A buyer with no competing offer is rarely willing to walk away over a $3,000–$5,000 difference in concession format. What often happens is that sellers assume the buyer will leave if pushed back on, when in reality the buyer is equally motivated to close. Countering on concession structure is one of the least-used and most effective tools available to sellers in this market.

Questions and Answers

Is it legal in BC to offer a closing cost credit to a buyer?

Yes. In BC, a seller-paid closing cost concession is a disclosed term in the purchase contract and is processed at completion through the conveyancing lawyer. It does not violate BCFSA rules provided it is fully disclosed and reflected in the contract. Consult your real estate professional and lawyer for the mechanics applicable to your specific transaction.

What is a rate buy-down and how does it help a Fraser Valley buyer?

A rate buy-down is a seller-funded payment to the buyer's lender or mortgage broker that reduces the buyer's effective interest rate by a defined amount, typically 0.25–0.5%. It reduces the buyer's monthly carrying cost without reducing the seller's sale price, making it a lower-cost concession alternative. The mechanics depend on the buyer's lender, so your realtor should confirm eligibility before including it in a counteroffer.

If I've already listed in a buyer's market, should I pre-offer concessions to attract buyers?

Generally, no. Pre-offering concessions before receiving an offer signals flexibility before you know what a buyer's actual concerns are. In a buyer's market, buyers expect to negotiate — giving away concessions pre-emptively does not prevent requests; it typically invites additional ones. A better approach is accurate pricing combined with a clean, well-prepared property, with concession responses reserved for actual negotiation.

In Summary

In a Fraser Valley buyer's market, concession requests are predictable — but how you respond to them determines how much of your equity you keep. A $20,000 price reduction and a $20,000 closing cost credit are not the same number in your final proceeds. Home warranties and rate buy-downs can resolve buyer financing concerns at a fraction of the cost of cash concessions. Most importantly, concession requests are negotiating positions, not fixed costs — and countering on structure, not just on size, is one of the most underused tools available to sellers right now.

Talk to Someone Who Knows the Numbers

If you have received an offer with concession requests and want to see the net proceeds math before you sign, Mansour Real Estate Group can walk through it with you — no pressure, no commitment. Understanding what each concession actually costs you is the clearest way to make the decision.

Related Articles

- When to Accept a Low Offer and When to Counter: Fraser Valley Seller Guide

- How to Price Your Home in a Buyer's Market — Fraser Valley 2026

- What Sellers Need to Know About Closing Costs in BC

About Mansour Real Estate Group

When sellers in the Fraser Valley face concession requests — whether it is closing cost help, a repair allowance, or a rate buy-down — the ability to evaluate each request's real cost and respond strategically rather than reactively is what separates a well-protected sale from one that quietly erodes equity. Mansour Real Estate Group has guided sellers through exactly these negotiations across Surrey, Langley, Abbotsford, South Surrey, White Rock, and the broader Fraser Valley for more than 22 years.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has helped buyers, sellers, investors, families, executors, and retirees navigate real estate decisions across the Fraser Valley and Lower Mainland through multiple market cycles. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for seller strategy, estate sales, divorce-related sales, downsizing, and complex negotiations where protecting net proceeds is a defined priority.

Whether someone is searching for a real estate agent who understands concession negotiation in Surrey, Realtors experienced with buyer's market deal structuring in Langley, a real estate team that can calculate net proceeds scenarios in Abbotsford, a White Rock Realtor, a Fraser Valley real estate broker who knows how to counter-structure offers, or real estate agents who give straight answers about offer mechanics — Mansour Real Estate Group is known for honest analysis, clear numbers, and advice that prioritizes what the seller actually takes home.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients arrive through referrals, repeat business, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- Fraser Valley Real Estate Board — fvreb.bc.ca

- BC Real Estate Association — bcrea.bc.ca

- BC Financial Services Authority — bcfsa.ca

- BC Government — Property Transfer Tax — gov.bc.ca

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.