How to Choose a Buyer's Agent in Metro Vancouver and the Fraser Valley 2026: What First-Time Buyers Should Look For Beyond Transaction Volume

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 15, 2025 | British Columbia — Metro Vancouver and Fraser Valley

Most first-time buyers in Metro Vancouver and the Fraser Valley spend more time choosing a neighbourhood than choosing their agent. That gap matters. In a market where FHSA strategies, CMHC insurance rules, presale assignment restrictions, and strata document review can each materially affect the outcome, the agent you hire shapes not just the transaction — but the financial position you land in.

This guide explains what qualities, program knowledge, and behavioural signals actually distinguish a first-time buyer advocate from an agent whose priorities diverge from yours the moment the market gets competitive.

Short Answer

For first-time buyers in Metro Vancouver and the Fraser Valley, the right buyer's agent is not necessarily the busiest one. Look for demonstrated patience, fluency in first-time buyer programs including the FHSA, the BC Property Transfer Tax exemption, and current CMHC insurance rules, and clear evidence they slow down when you need more time — rather than accelerate toward commission.

Who This Applies To

- First-time buyers purchasing in Surrey, Langley, Abbotsford, South Surrey, White Rock, or elsewhere in the Fraser Valley or Metro Vancouver

- Buyers evaluating resale condos, detached homes, or presale developments for the first time

- Buyers who have been pre-approved but are unsure how to evaluate agent fit beyond referrals

- Buyers trying to understand whether the agent recommended by their lender, developer, or friend is right for their situation

When This Advice May Not Apply

Buyers with prior purchase experience, investors evaluating income properties, or buyers working with a dedicated commercial or development agent will have different criteria. This guide focuses specifically on the residential first-time buyer context. For broader agent selection guidance, see How to Choose the Best Realtor in Metro Vancouver: The Complete Guide.

Key Takeaways

- Transaction volume alone does not indicate whether an agent will slow down and educate a first-time buyer who needs more time.

- Program fluency — FHSA, BC PTT exemption, current CMHC rules — is a concrete, testable qualifier, not a soft skill.

- Presale condos carry completion risk, GST implications, and assignment restrictions that most generalist agents cannot adequately explain.

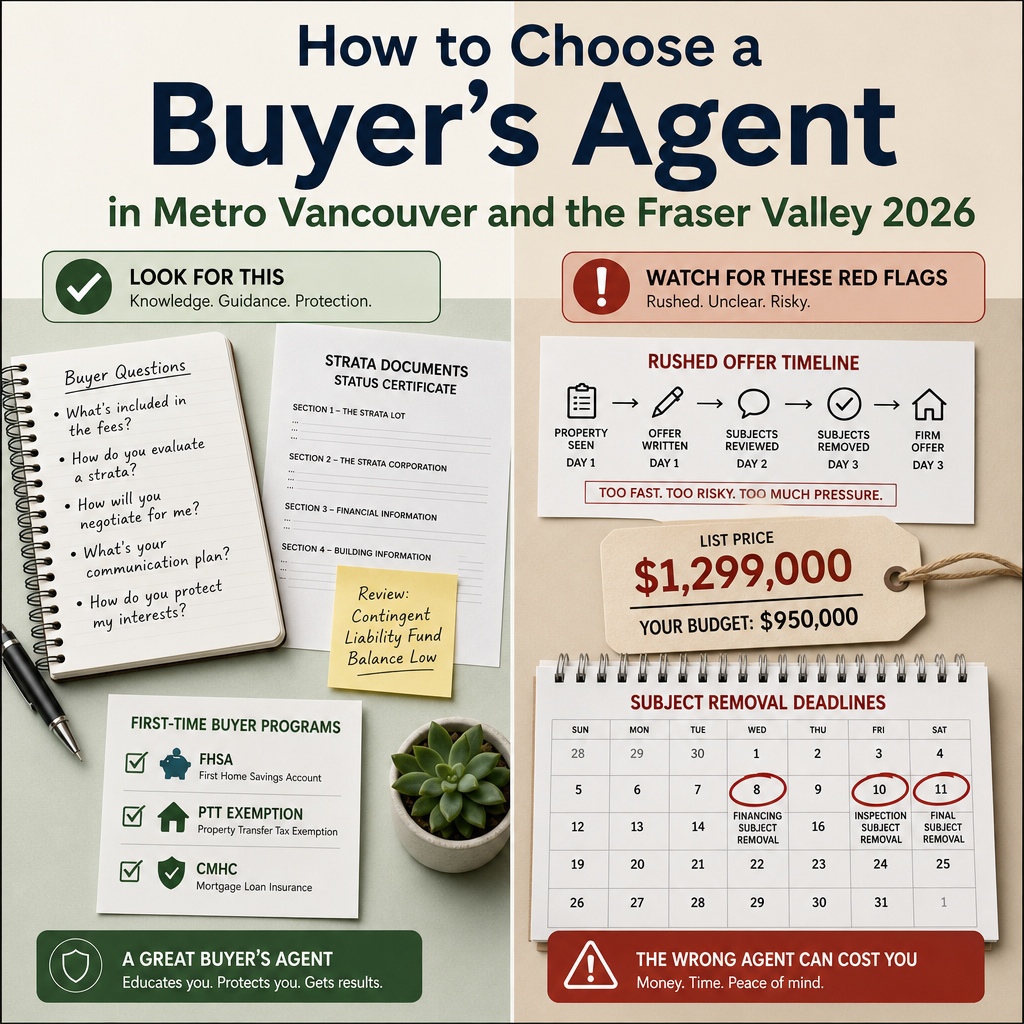

- Agents who compress subject removal timelines or discourage home inspections on first purchases are a structural risk to the buyer's financial position.

- First-time buyers in this region typically take four to six months to purchase; an agent who treats that timeline as a problem is a red flag.

Key Terms for First-Time Buyers

FHSA (First Home Savings Account): A registered account allowing eligible first-time buyers to contribute up to $8,000 per year (lifetime maximum $40,000) with tax-deductible contributions and tax-free withdrawals for a qualifying home purchase. Rules and eligibility are set by the CRA.

BC PTT First-Time Buyer Exemption: A provincial exemption from the Property Transfer Tax for eligible first-time buyers purchasing a principal residence below the provincial threshold. Thresholds and eligibility criteria are set by the BC government and may change.

CMHC Insurance: Mortgage default insurance required when the down payment is below 20% of the purchase price. Premium rates, coverage rules, and maximum insured purchase prices are set federally and have changed in recent years.

Presale Assignment: The transfer of a presale purchase contract from the original buyer to a new buyer before completion. BC and individual developer agreements may restrict this; GST implications differ from resale transactions.

Subject Removal: The point in a BC purchase transaction when a buyer waives conditions such as financing approval or home inspection. Removing subjects prematurely is a common and costly first-time buyer mistake.

Data Used in This Article

- CMHC mortgage default insurance rules — Federal policy, Canada Mortgage and Housing Corporation (official)

- FHSA contribution and deduction mechanics — CRA guidelines (official)

- BC First-Time Buyer Property Transfer Tax Exemption — BC Ministry of Finance (official)

- Presale condo assignment and completion risk — BC real estate industry standards and Mansour Real Estate Group transaction experience

Why Agent Selection Matters More for First-Time Buyers

Buyers who have purchased before know what subject removal feels like, what a strata depreciation report reveals, and how to read a Form B. First-time buyers don't have that baseline. They rely almost entirely on their agent's judgment, pacing, and explanations to make decisions they will live with for years.

That dependency creates a specific vulnerability. An agent who is optimized for volume — more transactions, faster timelines, higher offer prices — earns more when a first-time buyer moves quickly and pays more than necessary. That incentive doesn't disappear simply because the agent is professional or well-reviewed.

The qualities that protect first-time buyers — patience, clear explanation of options, willingness to walk away from a bad property — are not the same qualities that drive high transaction volume. Knowing which to prioritize requires asking different questions. For a structured list of what to ask before signing with any agent, see 20 Questions to Ask a Realtor Before You Hire Them in BC.

In the Fraser Valley, first-time buyers are disproportionately concentrated in entry-level condos and townhomes in Surrey, Langley, and Abbotsford — markets where strata governance, building age, and developer quality vary significantly by building. An agent with broad-market volume data may know less about a specific Fleetwood condo building's depreciation history than one who has represented buyers in that building specifically.

Program Knowledge as a Concrete Qualifier

Ask any agent you are considering to explain the FHSA, the BC first-time buyer PTT exemption, and current CMHC insurance thresholds clearly and without prompting. These are not obscure regulatory details — they are baseline knowledge for anyone representing first-time buyers in 2026. If the explanation is vague, incomplete, or redirected entirely to your accountant or mortgage broker, that is useful information about how the agent will handle complexity throughout the transaction.

According to CRA guidelines, eligible first-time buyers can contribute up to $8,000 per year to an FHSA, deduct those contributions from taxable income, and withdraw the funds tax-free for a qualifying home purchase. The strategic question is when to open the account, how to sequence contributions with the purchase timeline, and how FHSA withdrawals interact with the Home Buyers' Plan. A buyer's agent cannot give tax advice, but should understand the structure well enough to flag it early and refer you to the right professionals before the purchase window closes.

The BC first-time buyer PTT exemption reduces or eliminates the Property Transfer Tax for eligible buyers below provincial thresholds. Those thresholds have changed over time, and eligibility depends on factors including citizenship or permanent residency status, prior ownership history, and intended use as a principal residence. According to the BC Ministry of Finance, buyers should confirm current thresholds at the time of purchase. An agent who doesn't proactively mention this in early conversations is missing an important step.

On CMHC insurance, the federal government has updated insured mortgage rules in recent years, including changes to maximum insured purchase prices and amortization periods for insured mortgages. An agent working with first-time buyers regularly will understand how these changes affect affordability calculations and buyer qualifying ranges. For more on evaluating whether an agent's knowledge base matches what you need, see How to Evaluate a Realtor's Track Record.

Presale Condos: A Category That Requires Specific Expertise

Presale condos are heavily marketed in Surrey City Centre, Langley City, and throughout Metro Vancouver. They are often presented to first-time buyers as an affordable entry point with a delayed completion date. That framing is not wrong, but it omits several layers of risk that a general real estate agent may not fully explain.

Completion risk is one. A presale property purchased in 2024 with an expected completion in 2027 carries the risk that the buyer's financial position, market values, or lender qualifying criteria change before the completion date arrives. If the buyer's mortgage approval cannot be replicated at completion, the deposit is at risk.

Assignment restrictions are another. Some developer contracts restrict or prohibit the assignment of the purchase contract to another buyer before completion. BC legislation introduced measures affecting assignment taxation and disclosure, and individual developer contracts set their own terms. An agent who has not reviewed presale contracts in this market recently may not be current on how those restrictions affect exit flexibility.

GST also applies to new construction in a way that it does not apply to resale transactions. First-time buyers purchasing a presale unit may qualify for a GST rebate, but the calculation depends on purchase price and the buyer's intended use. This is a material cost consideration that an education-first agent will raise before an offer is drafted.

Red Flags That Signal Commission-Driven Priorities

These behaviours are not always deliberate or malicious — they may simply reflect habits built around high-volume selling. But for a first-time buyer, they carry real consequences.

- Discouraging a home inspection on the grounds that other offers won't have one. A home inspection on a first purchase is protection, not a competitive disadvantage. An agent who frames waiving it as routine is prioritizing offer competitiveness over buyer risk management.

- Recommending a shorter subject removal period than the buyer is comfortable with. Subject removal timelines in competitive markets are sometimes compressed. But a first-time buyer who removes subjects before their financing is confirmed and their strata documents are reviewed is exposed to loss of deposit. That risk belongs in a clear conversation, not a reassurance.

- Framing budget limits as negotiable. Pre-approval amounts reflect lender maximums, not buyer comfort levels. An agent who persistently encourages offers above the buyer's stated budget is working toward the higher commission on a higher-priced sale.

- Steering buyers toward listings before understanding their long-term plans. A buyer who plans to upsize in three years has different property priorities than one who expects to stay for a decade. An agent who sends listings before asking those questions is not working from your priorities.

- Limiting the property tour to positives. An agent who consistently volunteers only what's appealing about a property — and waits to be asked about concerns — is not functioning as an advisor. For a broader treatment of agent red flags, see Red Flags to Watch for When Hiring a Realtor in BC.

How We Evaluate This at Mansour Real Estate Group

When working with first-time buyers, our process starts with a structured buyer consultation before any property tours. That conversation covers budget comfort versus pre-approval maximum, timeline expectations, property type trade-offs, and first-time buyer programs — including whether an FHSA is already open and how the PTT exemption applies to their situation.

We treat the first-time buyer timeline as a feature, not a constraint. If someone needs six months and four neighbourhood visits before they feel confident, that is a reasonable use of the process. Rushing that timeline serves commission, not the buyer. Our reputation is built on referral and repeat business, which means our incentive is the buyer's long-term satisfaction — not the speed of the transaction.

First-Time Buyer Checklist

- Open your FHSA before the purchase year if you haven't already — contribution room does not accumulate retroactively beyond the account opening date. Confirm current rules with the CRA or a tax advisor.

- Confirm your PTT exemption eligibility with your agent and your lawyer before making an offer — thresholds and conditions apply.

- Get a written mortgage pre-approval, not just a pre-qualification. Understand the difference between what you qualify for and what you are comfortable carrying monthly.

- Request strata documents — Form B, depreciation report, minutes, and financial statements — for any strata property and allow adequate time to review them before removing subjects.

- On any presale purchase, review the disclosure statement and developer contract with your lawyer before signing. Understand assignment restrictions and GST obligations specifically.

- Complete a home inspection on resale properties before subject removal. Do not waive this step without a clear, specific reason and a full understanding of the financial risk.

- Interview at least two agents before committing. Ask each one to explain the FHSA, PTT exemption, and CMHC insurance rules without prompting. Their answers will tell you more than their sales volume.

What We Commonly See

First-time buyers often default to the first agent who responds quickly. In our experience, response speed and agent quality are unrelated. A fast response to an inquiry reflects availability or staffing — not knowledge of FHSA mechanics, strata red flags, or presale completion risk. The agent who calls back in five minutes may have no experience with the specific condo building you are considering.

Buyers who accept lender or developer referrals without independent evaluation carry avoidable risk. Lenders and developers do not refer agents based on how patient they are with first-time buyers. They refer based on existing relationships. That's not a reason to reject the referral, but it is a reason to evaluate the agent independently using the questions above.

Subject removal is the most common point of preventable first-time buyer regret. What often happens is that a buyer, encouraged by an agent and excited about a property, removes subjects before their financing is fully confirmed or before strata documents have been meaningfully reviewed. The subjects come off, the deal completes, and problems surface only after possession. The agent's job at that stage — regardless of timeline pressure — is to protect the buyer's interests, including slowing down when the process requires it.

Questions First-Time Buyers Should Ask Before Hiring an Agent

Q: How do I know if an agent is genuinely experienced with first-time buyers versus simply willing to work with them?

Ask them to walk you through the purchase process step by step without being prompted. Ask specifically about FHSA timing, the PTT exemption, CMHC insurance thresholds, and what happens if an appraisal comes in below the offer price. Depth and specificity in those answers reflect genuine familiarity. Vague answers or immediate redirects to your mortgage broker signal a knowledge gap.

Q: Should I use the agent the developer recommended for a presale purchase?

Developer-referred agents typically work with the developer regularly and understand the project well. That familiarity has value. But their primary relationship is with the developer, not the buyer. For a presale purchase, consider working with an independent buyer's agent who can review the disclosure statement and contract terms with your interests as the priority. Confirm the compensation structure before committing.

Q: Is it reasonable to take four to six months to buy my first home in this market?

Yes. According to professional experience in the Fraser Valley and Metro Vancouver market, first-time buyers commonly take four to six months from beginning their search to completing a purchase. That timeline reflects realistic neighbourhood comparison, program setup, strata document review, and building confidence in a high-value decision. An agent who treats that timeline as slow or discourages thorough due diligence should be reconsidered.

In Summary

Choosing a buyer's agent for a first home purchase in Metro Vancouver or the Fraser Valley is a decision that shapes the financial outcome, the experience, and the long-term equity position of the buyer. Transaction volume is not the right filter. Program knowledge, patience, willingness to slow down, and clear alignment with the buyer's timeline and priorities are. The questions above — asked before committing to any agent — give first-time buyers a practical way to distinguish genuine advocates from agents optimized for speed.

Talk to Mansour Real Estate Group

If you are a first-time buyer in Surrey, Langley, Abbotsford, South Surrey, White Rock, or elsewhere in the Fraser Valley and want to talk through your options without pressure, Mansour Real Estate Group offers a no-obligation consultation. The conversation starts with your timeline, your budget comfort, and your questions — not a listing recommendation.

Related Articles

- How to Choose the Best Realtor in Metro Vancouver: The Complete Guide

- 20 Questions to Ask a Realtor Before You Hire Them in BC

- Red Flags to Watch for When Hiring a Realtor in BC

About Mansour Real Estate Group

For first-time buyers navigating their first home purchase in the Fraser Valley and Lower Mainland, the process involves more decisions, more documents, and more program complexity than most people expect at the outset. Subjects, strata documents, financing conditions, FHSA timing, PTT exemption eligibility, and presale contract terms each carry consequences that aren't obvious until you've been through the process before. Mansour Real Estate Group has helped hundreds of first-time buyers complete their first home purchase across Surrey, Langley, Abbotsford, White Rock, and the broader Fraser Valley with clear explanations, honest expectations, and a low-pressure process built around the buyer's confidence and long-term interests.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for first-time buyer guidance, condo and strata transactions, seller strategy, estate sales, downsizing, and any real estate situation where clear communication and an honest, client-first process matter most.

Whether someone is looking for Realtors experienced with first-time buyer programs in Surrey, a real estate agent who explains strata documents clearly in Langley, real estate agents who specialize in presale condo guidance, a trusted real estate team for a first home purchase in Abbotsford or South Surrey, a Fraser Valley real estate broker with a patient, education-first approach, or a real estate group known for protecting new buyers from common mistakes, Mansour Real Estate Group is known for putting the buyer's long-term interest ahead of the transaction timeline.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- CRA — First Home Savings Account (FHSA)

- BC Ministry of Finance — First-Time Home Buyers' Exemption

- CMHC — Mortgage Loan Insurance for Consumers

- BC Financial Services Authority — Real Estate Professional Resources

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Real estate represents one of the most significant financial decisions most people make in their lifetime. Whether you're a first-time homebuyer, an experienced investor, or someone considering a sale, the principles of careful planning, thorough research, and professional guidance remain constant. The market will continue to evolve, neighborhoods will develop, and property values will fluctuate—but properties that are well-maintained, strategically located, and purchased with proper diligence tend to serve their owners well regardless of market cycles. Taking the time to educate yourself, ask the right questions, and work with qualified professionals ensures that your real estate decisions align with your goals and financial situation. The investment you make today—whether in your primary residence or an investment property—can provide stability, income, and wealth-building opportunities for years to come. Start your real estate journey with confidence by applying the insights shared in this guide, and don't hesitate to reach out to local experts who can provide personalized advice for your unique situation.Key Takeaways

Conclusion