How Subject-to-Financing, Subject-to-Inspection, and Subject-to-Appraisal Conditions Extend Fraser Valley Closing Timelines in 2026 — and What Sellers Can Do About It

By Mohamed Mansour, MBA, Associate Broker | Mansour Real Estate Group | Published: July 14, 2025 | Fraser Valley & Lower Mainland, BC

For sellers in Surrey, Langley, Abbotsford, and across the Fraser Valley, accepted offers no longer mean what they once did. In 2026, buyer conditions are arriving in combinations — financing, inspection, and appraisal stacked together — and each one extends the timeline before a deal becomes firm. Understanding how these conditions interact, and how to negotiate terms that protect your closing date and your proceeds, is now a practical necessity, not a precaution.

This article explains what happens when multiple conditions run concurrently, why they are taking longer to remove in today's Fraser Valley market, and what sellers can negotiate before signing to reduce delay risk and defend deal certainty.

Short Answer

When financing, inspection, and appraisal conditions stack in a single Fraser Valley offer, closing timelines commonly extend 3–4 weeks beyond the original possession date. Sellers can reduce that risk by negotiating condition sequencing, requiring parallel processing, using pre-listing inspections, and building removal deadlines into the contract before signing.

Key Takeaways

- Appraisal conditions alone now add 10–14 days beyond standard financing removal windows in 2026.

- Stacked conditions — financing, inspection, and appraisal — commonly push closings 3–4 weeks past the agreed possession date.

- Pre-listing inspections and seller-ordered appraisals can shorten buyer condition timelines by 5–7 days.

- Negotiating condition removal sequencing before signing reduces deal-collapse risk and limits buyer renegotiation leverage.

- In a market with an 11% sales-to-active ratio, deal certainty is often more valuable to a seller than a slightly higher offer price.

Who This Applies To

- Sellers in Surrey, Langley, Abbotsford, White Rock, Cloverdale, Willoughby, and surrounding Fraser Valley communities

- Sellers who have received offers with multiple conditions and are evaluating the timeline risk before signing

- Sellers who have a firm purchase lined up and need their own sale to close on schedule

- Executors or estate representatives managing a sale with legal timeline obligations

- Any seller evaluating two competing offers — one cleaner, one higher but loaded with conditions

When This Advice May Not Apply

If your buyer is purchasing with cash and no financing requirement, appraisal conditions typically do not apply. Pre-sale assignment contracts and developer sales operate under different condition structures governed by separate disclosure rules. Sellers in active multiple-offer situations may have more leverage to require shorter timelines outright. Consult your real estate professional and your lawyer about the specific terms in your offer before relying on any general guidance.

Data Used in This Article

- BC Real Estate Association: Market data, April 2026 — official industry body, BC-wide

- Fraser Valley Regional District: Sales-to-active ratio tracking — official regional data, April 2026

- Bank of Canada: Mortgage stress-test policy documentation — official federal regulatory source

- Canada Mortgage and Housing Corporation: Lending trend reports — official federal housing body

Why Conditions Are Taking Longer to Remove in 2026

Each of the three major buyer conditions — financing, inspection, and appraisal — has its own processing chain. In a stable market, these often resolve quickly and in sequence. In 2026, they are taking longer individually, and the problems compound when buyers and their lenders are running them concurrently rather than in order.

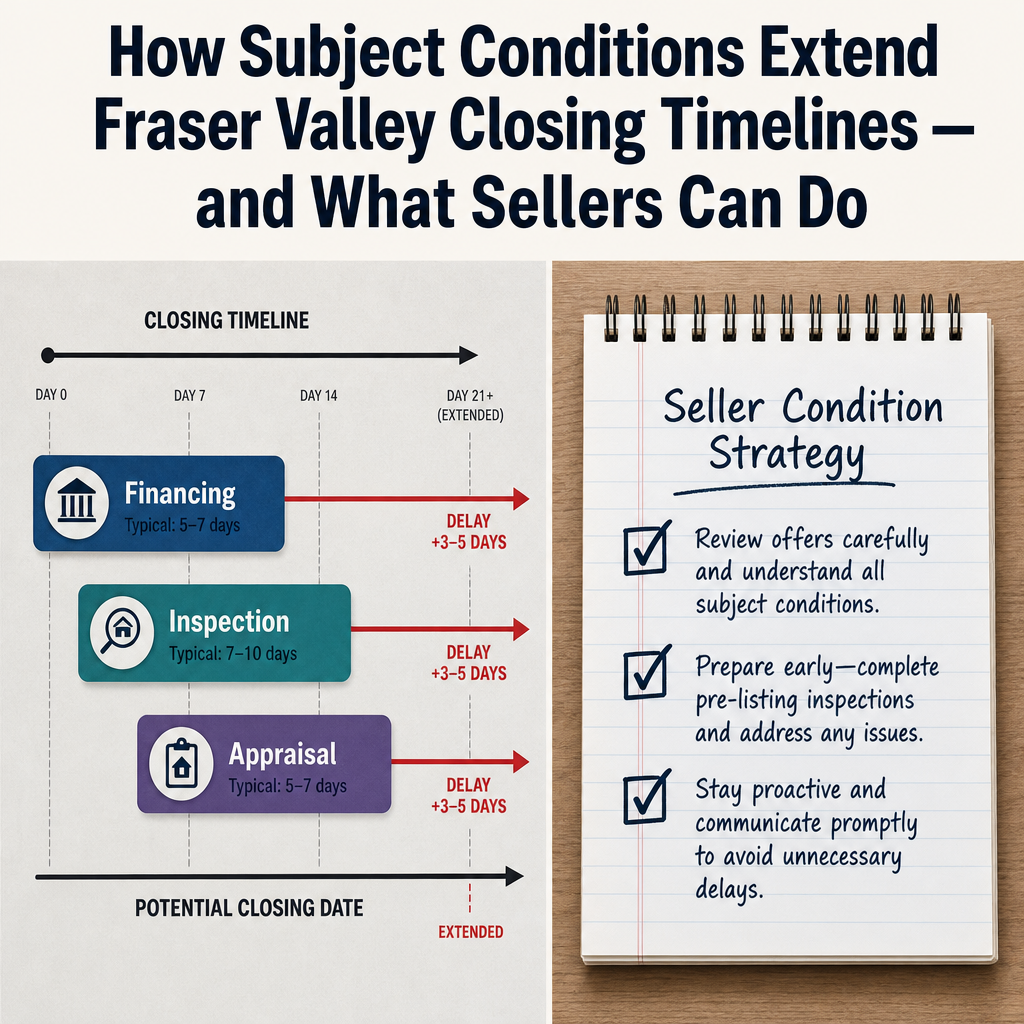

According to BC Real Estate Association data from April 2026, subject-to-financing removals are now extending 3–5 days beyond their contracted deadlines on average across the Fraser Valley, as lenders apply tighter documentation requirements under the Bank of Canada's current stress-test framework. Appraisal conditions are the bigger problem: when a lender orders an independent appraisal — particularly on higher-value properties in South Surrey, White Rock, or newer Willoughby and Walnut Grove subdivisions — the turnaround is regularly running 10–14 days longer than the standard financing window built into most offers.

The inspection condition adds a third layer. Buyers are increasingly using inspection outcomes to support price renegotiation, particularly when an appraisal comes in below the offer price. According to CMHC lending trend data, this convergence — where an inspection identifies items and an appraisal independently arrives low — is giving buyers two separate pressure points to revisit price before going firm. For sellers, that is two negotiation events inside a single accepted offer.

The Fraser Valley's current sales-to-active listings ratio of approximately 11% confirms a buyer's market environment. In that context, sellers who accept offers without managing condition structure are accepting more timeline and renegotiation risk than many realize at signing.

How Stacked Conditions Compound the Delay

In a standard Fraser Valley offer, a buyer might request seven days for financing and seven days for inspection. These conditions are often listed as running concurrently, meaning the buyer is expected to pursue both at the same time. In practice, what happens is different: inspection happens first, inspection results inform the appraisal conversation, the appraisal triggers lender conditions, and lender final approval waits for appraisal sign-off. The concurrent structure on paper becomes sequential in execution.

The result is a timeline that frequently looks like this: seven days for inspection, plus ten days for the appraisal that could not be ordered until the inspection was complete, plus three to five additional days for lender final approval after the appraisal is returned. That sequence adds three to four weeks beyond the original possession date sellers expected when they signed the offer.

For sellers carrying a bridge loan, a simultaneous purchase, or a tenanted property in Surrey or Langley with tenant rights and notice obligations, that additional month represents real carrying costs, legal obligations, and in some cases a collapsed chain. Sellers who have already committed to a purchase on the other side are the most exposed.

How We Evaluate This

When Mansour Real Estate Group reviews an offer with multiple conditions, we assess three things before advising a seller to sign: the realistic removal timeline given current lender processing speeds, whether the conditions are structured to run genuinely in parallel or sequentially in disguise, and whether the buyer's deposit is large enough to signal real commitment against a conditional offer.

We also compare the conditional offer to alternatives on the table — not just on price, but on certainty-adjusted value. A firm offer at $30,000 below asking is often worth more to a seller with a firm purchase commitment than a conditional offer at asking that carries a 20% deal-collapse probability and a four-week delay. That comparison rarely appears in standard offer presentations, but it is the comparison that protects sellers.

Seller Checklist: Managing Condition Risk Before You Sign

- Complete a pre-listing home inspection and make the report available to buyers before offers are submitted.

- Request that inspection and financing conditions run on a genuine parallel timeline, with clear written deadlines for each.

- Negotiate a condition removal sequencing agreement: inspection removed first, appraisal ordered simultaneously with financing, lender final approval within a fixed window after appraisal delivery.

- Require a non-refundable deposit component or increased deposit at condition removal to signal buyer commitment before going firm.

- Confirm the buyer is already pre-approved — not just pre-qualified — before accepting an offer with a financing condition longer than five business days.

- Discuss with your lawyer whether the offer includes a time-is-of-the-essence clause and what happens if conditions are not removed by the agreed deadline.

- If possession date flexibility is limited (bridge financing, simultaneous purchase), make that constraint explicit in counteroffer negotiations rather than discovering it when a delay occurs.

What We Commonly See

In our experience working with sellers across Surrey, Langley, Abbotsford, and White Rock, the most common error is treating the condition removal date as a formality rather than a negotiation point. Sellers often focus entirely on offer price and leave the condition structure to the buyer's agent to draft. By the time the inspection returns with items and the appraisal comes in low, the seller has already lost the initiative.

A second pattern we see regularly: buyers requesting seven-day financing conditions when they have not yet submitted a full mortgage application. That seven days does not begin at approval — it begins at submission. If the buyer's broker is slow or the lender's queue is backed up, the condition period expires before the appraisal is even ordered, and the buyer requests an extension. Sellers who have not pre-negotiated extension terms find themselves in a weak position to refuse without risking the deal collapsing entirely.

A third observation: pre-listing inspections consistently reduce negotiation friction after the fact. Sellers in Langley and Abbotsford who provide an inspection report before listing see fewer inspection-triggered renegotiation attempts, because buyers have already priced visible items into their offer rather than discovering them mid-condition period and using them as leverage.

Questions and Answers

Can a seller in BC refuse to extend a subject removal deadline if a buyer requests more time?

Yes. In BC, subject removal deadlines are contractual. A seller is not legally required to grant an extension. However, refusing an extension ends the contract and requires the seller to relist. Whether to grant an extension depends on market conditions, whether backup offers exist, and carrying cost risk. This is a legal and strategic decision — consult your lawyer and real estate professional before responding to an extension request.

Why do appraisals take longer than financing approvals in 2026?

Lenders in 2026 are ordering independent appraisals more frequently on higher-value and atypical properties as CMHC and private insurers tighten collateral valuation requirements. Appraisers must physically attend the property, prepare a formal report, and submit it for lender review — a process that now routinely takes 10–14 days in the Fraser Valley, compared to 3–5 days for standard mortgage underwriting.

Does a pre-listing inspection legally replace the buyer's right to conduct their own inspection in BC?

No. A pre-listing inspection is a seller-provided disclosure tool, not a legal substitute for the buyer's own inspection right. However, many buyers will waive or shorten their inspection condition when a recent, credible inspection report is already available and disclosed. This is a negotiation outcome, not a legal entitlement. Buyers retain the right to conduct their own inspection regardless of what the seller provides.

What is condition removal sequencing and how does it protect a seller?

Condition removal sequencing is a negotiated term specifying the order and timing in which each condition must be resolved before the next can run. For example: inspection removed by day five, appraisal ordered by day three and resolved by day twelve, financing confirmed within two days of appraisal delivery. Sequencing prevents conditions from masking each other and gives the seller clear default rights if any stage is missed.

How does the Fraser Valley's current 11% sales-to-active ratio affect a seller's ability to demand shorter condition periods?

An 11% ratio indicates a buyer's market, meaning buyers have choices and sellers have limited leverage to demand aggressive terms. However, well-prepared sellers — those with pre-listing inspections, clean title, and organized documents — can reasonably negotiate tighter timelines because they are removing the main sources of buyer delay. Preparation is the primary way sellers recover negotiating leverage in a soft market.

In Summary

In 2026, Fraser Valley sellers who treat condition removal as a formality are taking on real timeline and financial risk. Financing, inspection, and appraisal conditions stack in ways that extend closings by three to four weeks when not actively managed. The sellers who protect their proceeds and their possession dates are the ones who negotiate condition structure before signing — not after the delays start. Pre-listing preparation, parallel processing requirements, and sequencing agreements are the practical tools available. They work best when the strategy is set before the offer is accepted.

Talk to Mansour Real Estate Group

If you are preparing to list in Surrey, Langley, Abbotsford, or anywhere across the Fraser Valley and want to understand how to structure your listing for deal certainty, Mansour Real Estate Group offers a no-obligation seller consultation. We review your timeline, your property type, and current buyer conditions in your specific market — and we give you honest advice before you commit to a strategy.

Related Articles

- Fraser Valley Real Estate Market Outlook for 2026 — What Sellers Need to Know

- Selling Your Home in Surrey, BC — A Complete Seller Strategy Guide

- Selling a Tenanted Property in the Fraser Valley — Timelines, Rules, and Seller Obligations

About Mansour Real Estate Group

When sellers in Surrey, Langley, Abbotsford, and White Rock are navigating complex offers with multiple buyer conditions, the decisions made before signing — on condition structure, sequencing, and timeline protection — determine whether the deal closes on schedule or extends into costly delays. Mansour Real Estate Group has guided sellers through this exact situation across the Fraser Valley and Lower Mainland for more than two decades, with a process built around deal certainty, accurate valuations, and protecting seller proceeds from the moment the offer arrives.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. Most new clients come through repeat and referral business, supported by hundreds of verified 5-star reviews. The team is trusted for estate sales, divorce-related property sales, downsizing, seller strategy, and complex real estate situations where condition structure and timing matter.

Whether someone is looking for Realtors who understand condition negotiation in Langley, a real estate agent with experience managing subject removal timelines in Surrey, real estate agents who know how appraisal and financing conditions interact in Abbotsford, a trusted real estate team for a conditional offer situation in White Rock, a Cloverdale Realtor, a Willoughby real estate broker, or a real estate group serving the Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for clear communication, practical strategy, and advice that protects sellers at every stage of the transaction.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- BC Real Estate Association — bcrea.bc.ca

- Bank of Canada — Mortgage Stress-Test Policy — bankofcanada.ca

- Canada Mortgage and Housing Corporation — cmhc-schl.gc.ca

- Fraser Valley Real Estate Board — fvreb.bc.ca

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.