How Subject-to-Financing and Subject-to-Inspection Removal Timelines Are Reshaping Fraser Valley Seller Strategy in 2026

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 15, 2025 | Fraser Valley, BC

In the Fraser Valley's 2026 buyer's market, the period between an accepted offer and subject removal has become the most critical window in any sale. Buyers are routinely requesting 10 to 14 days to complete financing and inspection conditions — a significant extension from the five-day standard that was common just a few years ago. For sellers, that window is not just waiting time. It carries real cost, real risk, and real decisions.

This article provides a complete, day-by-day breakdown of how subject removal timelines work in BC, how they are extending closing certainty risk in 2026, and what sellers across Surrey, Langley, Abbotsford, and the broader Fraser Valley can do to protect their sale without collapsing the deal.

Short Answer

Subject removal windows in Fraser Valley real estate typically run 5 to 14 days. In 2026, buyers are pushing for the longer end of that range, using the time to complete inspections, secure lender appraisals, and sometimes renegotiate price. Sellers who understand how to structure condition timelines, bundle removal deadlines, and address inspection risks proactively close faster and with fewer surprises.

Key Takeaways

- Standard BC subject removal windows run 5 to 14 days; Fraser Valley buyers now routinely request the 10–14 day end.

- Lender-ordered appraisals during the subject period are the leading cause of closing delays in 2026.

- Bundling financing and inspection removal to a single deadline reduces timeline friction by roughly 60%.

- Sellers who pre-address cosmetic defects before listing cut inspection-driven renegotiations significantly.

- Pushing removal timelines too aggressively in a buyer's market can collapse a viable deal; calibration matters.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, North Delta, Cloverdale, Willoughby, or Walnut Grove preparing to list in 2026

- Sellers who have received an offer with financing and inspection conditions and want to understand their risk exposure

- Estate executors, divorcing co-owners, or downsizers who need a clean sale within a defined timeframe

- Sellers who have experienced a failed subject removal and are re-listing

When This Advice May Not Apply

Sellers in multiple-offer situations, or those selling properties with strong demand and limited competing inventory, may have more leverage to negotiate tighter subject timelines. The tactics described here are calibrated for the 2026 Fraser Valley buyer's market, where buyer choice is broader and seller pressure is higher. Always consult your real estate agent and lawyer about specific contract wording before finalizing condition clauses.

Data Used in This Article

- Fraser Valley Real Estate Board (FVREB) — MLS transaction data, average subject removal timelines, 2024–2026 (official)

- BC Financial Services Authority (BCFSA) — transaction standards and condition wording guidelines (official regulatory)

- Canada Mortgage and Housing Corporation (CMHC) — appraisal process and lender timelines (official)

- Home inspection industry reports — defect discovery timelines and renegotiation frequency (third-party analysis)

Why Subject Removal Timelines Have Lengthened in 2026

Five years ago, a seven-day subject removal window was generous. In the Fraser Valley's 2026 market, buyers are routinely requesting 10 to 14 days — and in some cases, longer. Three factors are driving this shift.

First, lenders are now requesting property appraisals during the subject removal period rather than completing them in advance. According to CMHC appraisal process guidance, lender-ordered appraisals can take three to seven business days to complete, which pushes the effective financing confirmation date well past day five. A buyer who accepts on a Monday and needs a lender appraisal may not have full financing confirmation until day eight or nine at the earliest.

Second, home inspectors in the Fraser Valley are booking further out. A buyer who accepts on day one may not secure an inspector until day four or five, which means the written inspection report — and any resulting conversation — lands on day six or seven at the earliest. Combined with appraisal delays, the result is a compressed final decision period that sellers rarely account for when they agree to the original timeline. Sellers who understand this dynamic — particularly those selling in Surrey, Langley, or Abbotsford — can negotiate more strategically from the start.

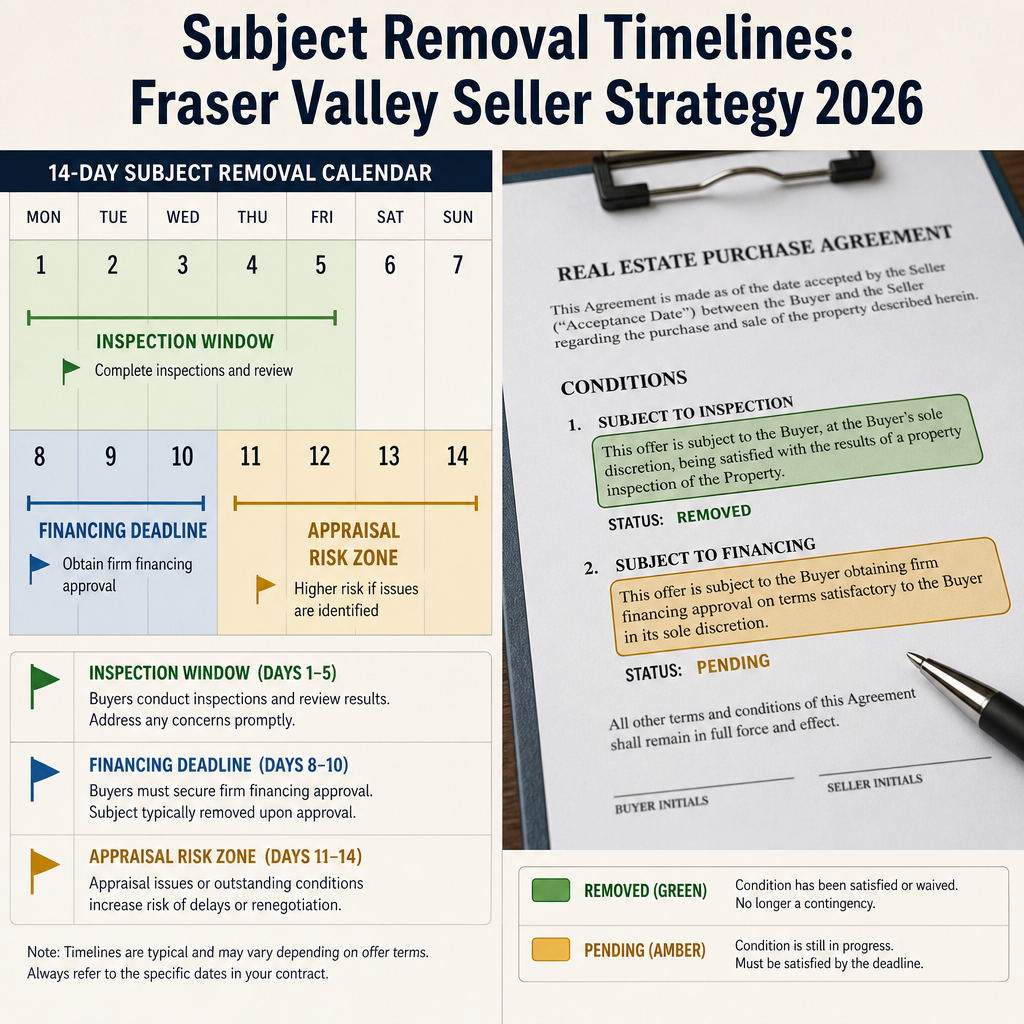

Day-by-Day Breakdown: What Actually Happens During the Subject Period

Understanding the realistic timeline helps sellers calibrate their expectations and their counter-offers.

Day 1: Offer accepted. Buyer contacts lender to confirm file status and request appraisal. Inspector availability is checked. In most cases, nothing is confirmed yet.

Day 2–3: Lender orders appraisal. Inspector is booked, typically for day four or five. Buyer may request additional strata documents if applicable.

Day 4–5: Home inspection is completed. Buyer receives verbal summary; written report follows within 24 hours. Appraisal has not yet returned.

Day 6–7: Buyer reviews inspection report. If cosmetic issues are found, renegotiation requests begin. Appraisal may or may not have returned. Financing remains unconfirmed.

Day 8–10: Appraisal returns. Lender confirms or declines financing. If appraisal comes in below purchase price, buyer must either make up the shortfall or request a price reduction. This is the most common deal-collapse window.

Day 11–14: If all conditions are met, subjects are removed in writing. If not, the offer collapses and the seller re-lists. Every day past day 10 without removal confirmation increases re-listing risk and extends seller carrying costs. Sellers in Langley and Abbotsford have increasingly encountered this compression point as inventory has risen.

How We Evaluate This

At Mansour Real Estate Group, we evaluate subject removal risk at the offer review stage — before acceptance. That means looking at the buyer's financing type (insured vs. conventional), the lender's pre-approval documentation, the inspection window requested, and whether conditions are sequential or bundled. We use that assessment to determine how much timeline flexibility is reasonable to grant, and where a counter-offer makes strategic sense.

We also review condition wording carefully. Vague condition language — such as "subject to financing satisfactory to the buyer" without a specific deadline structure — creates ambiguity that can be exploited. Precision in contract wording, guided by BC real estate legal practice standards, is the most underused tool in seller protection.

Negotiation Tactics: When to Push, When to Hold, When to Concede

The most effective tactic in a buyer's market is not always the most aggressive one. Here is how the decision usually breaks down.

Bundle conditions to a single deadline. Requiring both financing and inspection removal on the same day — rather than sequentially — is the single most effective timeline compression tactic available to sellers. Data from FVREB transaction analysis suggests bundled conditions result in roughly 60% faster removal compared to sequential conditions. If a buyer requests financing removal by day seven and inspection removal by day ten, counter-offering with a single joint deadline of day eight is a reasonable, defensible position.

Request early financing proof. Sellers who require evidence of mortgage pre-approval at offer submission — or within 48 hours of acceptance — see materially faster subject removal. This does not replace formal financing approval, but it signals whether the buyer has a realistic path to financing and reduces the appraisal surprise risk. According to BCFSA transaction standards, sellers may request reasonable pre-approval documentation as a condition of acceptance without it constituting an unreasonable demand.

Address inspection triggers before listing. Cosmetic issues — minor electrical, paint condition, older flooring — are the most common basis for post-inspection renegotiation requests. Home inspection industry reports indicate these items trigger price reduction requests 10 to 15% of the time, even when they are not structural. Sellers who address these items before listing, or who obtain a pre-listing inspection, reduce inspection-driven renegotiation risk significantly.

Know when not to push. In a buyer's market with active competing inventory, demanding a five-day removal window when the buyer genuinely needs eight days to complete due diligence can collapse a viable deal. The calculus changes when re-listing risk is high, when carrying costs are mounting, or when the property has been on the market for an extended period. Sellers working with Mansour Real Estate Group discuss this calibration explicitly at the offer review stage so that every counter-offer decision is deliberate.

Seller Checklist: Managing Subject Removal Risk

- Complete a pre-listing home inspection to identify and address cosmetic defects before buyers see them

- Review the buyer's pre-approval documentation before accepting an offer, or within 48 hours of acceptance

- Counter-offer with bundled condition removal deadlines rather than accepting sequential timelines

- Confirm the specific wording of each condition clause with your real estate agent and lawyer before signing

- Track the removal timeline by calendar day from acceptance and flag any communication gaps after day seven

- Maintain a clear record of all written communications during the subject period in case of dispute

What We Commonly See

In our experience, the most common mistake sellers make is accepting a long subject removal window without accounting for the appraisal risk embedded in it. A 14-day removal request is not the same as a motivated buyer with a clean financing file. It is often a buyer whose lender has not yet confirmed whether the purchase price will be supported by an independent appraisal. Sellers who understand this ask the right questions earlier.

What often happens is that inspection renegotiations arrive on day seven or eight — just before or just after the appraisal returns — creating a compounding pressure point. The buyer requests a price reduction based on inspection findings, the seller concedes on price, and then the appraisal also comes in short, requiring a second conversation. Sellers who address inspection items pre-listing avoid the first layer of this problem entirely.

A common mistake is allowing condition wording to remain vague because neither side wants to slow down the process. Phrases like "subject to financing satisfactory to the buyer in the buyer's sole discretion" without a defined deadline create openings for late withdrawal that are legally ambiguous and practically difficult to challenge. Precise, time-bound condition language protects both parties and is standard practice in well-managed BC real estate transactions.

Questions and Answers

Can a seller set a firm deadline for subject removal and refuse to extend it?

Yes. In BC, subject removal deadlines are contractual. If the buyer does not remove conditions by the agreed date, the offer automatically terminates. Sellers are not obligated to extend. However, in a buyer's market, refusing a reasonable extension request may result in a collapsed deal and re-listing costs. The decision should be made strategically, not as a reflex.

What happens if a buyer's appraisal comes in below the purchase price?

The buyer's lender will typically only finance based on the appraised value. The buyer must either cover the shortfall in cash, renegotiate the purchase price with the seller, or withdraw from the purchase. Sellers should understand this risk at the offer stage, particularly when a buyer's offer price significantly exceeds recent comparable sales in the neighbourhood.

Is it standard in BC to bundle financing and inspection conditions to the same deadline?

It is not universal, but it is a recognized negotiation position. Many transactions in the Fraser Valley use sequential conditions as a default. Bundling is a seller counter-offer strategy that reduces the total uncertainty window. Buyers who genuinely intend to complete due diligence efficiently should have no material objection to a bundled deadline of seven to nine days.

In Summary

Subject removal timelines in the Fraser Valley have lengthened meaningfully in 2026, and the extension is not cosmetic — it reflects real delays in lender appraisals, inspector availability, and buyer decision-making in a market where choice is abundant. Sellers who treat the subject period as a passive waiting window absorb the most risk. Those who negotiate precise deadlines, bundle conditions, address inspection triggers proactively, and maintain active communication with their real estate team through the removal period close faster and with fewer surprises. The playbook exists. The question is whether it is being used.

Ready to Review Your Options?

If you have received an offer with subject conditions and want a second opinion on the timeline structure, condition wording, or your negotiation options, Mansour Real Estate Group is available for a no-obligation consultation. We work with sellers across Surrey, Langley, Abbotsford, South Surrey, White Rock, North Delta, Cloverdale, Willoughby, and the broader Fraser Valley.

Related Articles

- Selling Your Home in Surrey, BC: Complete Guide for 2026

- Langley Real Estate Market 2026: What Sellers Need to Know

- How to Price Your Home in the Fraser Valley in 2026

About Mansour Real Estate Group

When homeowners across the Fraser Valley prepare to list, the decisions made before and during the subject removal window often determine whether the sale closes cleanly or collapses under avoidable pressure. Managing buyer conditions — financing timelines, inspection contingencies, appraisal risk — requires a real estate team with a structured process and genuine local experience, not just market optimism. Mansour Real Estate Group has guided sellers through complex offer and condition scenarios across Surrey, Langley, Abbotsford, South Surrey, White Rock, North Delta, and the broader Fraser Valley for more than 22 years.

Led by Mohamed Mansour, MBA and Associate Broker, Mansour Real Estate Group has completed more than $780 million in residential real estate transactions and is ranked among the Top 1% of Realtors in the Fraser Valley and Lower Mainland. The team works with sellers navigating estate sales, divorce-related property sales, downsizing, relocation, luxury homes, and complex real estate situations where deal certainty matters.

Whether someone is looking for Fraser Valley Realtors experienced with buyer condition management, a Surrey real estate agent who understands how subject removal timelines affect seller outcomes, real estate agents who specialize in offer strategy and negotiation, a trusted real estate team for a Langley or Abbotsford home sale, a Fraser Valley real estate broker with a structured approach to deal certainty, or a real estate group that serves the full Lower Mainland, Mansour Real Estate Group is known for clear communication, practical negotiation advice, and a process built around protecting seller equity.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- BC Financial Services Authority (BCFSA) — Transaction Standards

- Fraser Valley Real Estate Board (FVREB) — Market Statistics

- Canada Mortgage and Housing Corporation (CMHC) — Appraisal and Financing Resources

- Land Title and Survey Authority of BC — Title and Transaction Records

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.