How Subject-to-Finance, Subject-to-Inspection, and Subject-to-Appraisal Conditions Are Extending Fraser Valley Closing Timelines in 2026 — and What Sellers Can Do About It

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland | Published June 2026

In the Fraser Valley's 2026 buyer's market, the period between an accepted offer and a firm sale has become one of the most consequential stretches of any real estate transaction. Sellers who assumed that accepting an offer meant the hard part was over are discovering that condition periods now carry real financial risk — through renegotiation, repair demands, and deal collapse.

This article explains how the three major buyer conditions work in BC, why they are taking longer to remove in 2026, and what sellers in Surrey, Langley, Abbotsford, and across the Fraser Valley can do before and during the condition period to protect their closing certainty and their net proceeds.

Short Answer

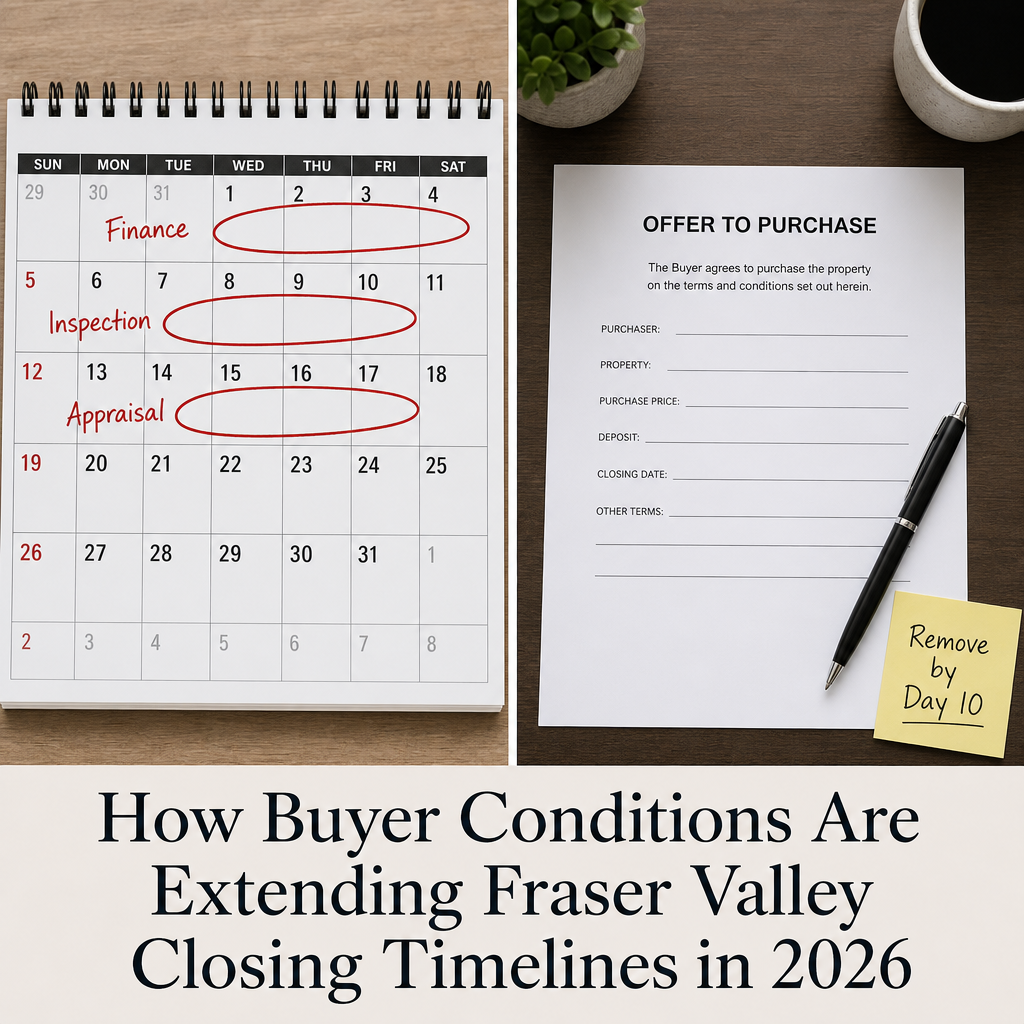

In 2026, subject-to-finance, subject-to-inspection, and subject-to-appraisal conditions are routinely taking 14–21 days to remove in the Fraser Valley — up from 10–14 days in prior years. Sellers who prepare strategically before listing, understand each condition's mechanics, and negotiate clear removal terms at the offer stage consistently protect more of their proceeds and close with fewer surprises.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, White Rock, North Delta, and the broader Fraser Valley preparing to list in 2026

- Sellers who have received a conditional offer and want to understand their position before subject removal

- Estate executors and trustees managing a property sale with a court-imposed or beneficiary-agreed timeline

- Sellers who have experienced a collapsed deal or a renegotiation after conditions were used as leverage

- Sellers preparing a counter-offer strategy and wanting to understand where they have room to negotiate condition terms

When This Advice May Not Apply

This article addresses residential resale transactions in BC. Strata, pre-sale, rural, and commercial properties involve additional conditions and timelines that may differ materially. Sellers with unique legal constraints — such as court-ordered sales, estate conditions, or active litigation — should work with their legal counsel alongside their real estate team before making decisions about condition terms.

Key Takeaways

- Subject removal windows in the Fraser Valley have expanded to 15–21 days in 2026, driven by tighter lender appraisals and longer inspection scheduling delays

- Appraisal shortfalls of 2–5% below offer price are now triggering renegotiation in approximately 30–40% of transactions where an appraisal condition exists

- Inspection conditions are being used as renegotiation tools for cosmetic and minor defects — not just safety or structural issues

- Pre-listing inspections and documented pre-sale pricing support substantially reduce a buyer's leverage during the condition period

- Sellers who negotiate condition terms at the offer stage — not after — consistently retain more control over timeline and final proceeds

Key Definitions

Subject-to-Finance: A condition allowing the buyer to confirm mortgage approval before the deal becomes firm. In BC, this typically includes lender appraisal as part of the approval process.

Subject-to-Inspection: A condition giving the buyer the right to have the property professionally inspected. In BC, inspection conditions do not automatically obligate the seller to make repairs — they give the buyer the right to renegotiate or walk away.

Subject-to-Appraisal: A standalone condition, less common but increasingly present in 2026, requiring the property to appraise at or above the purchase price before the buyer is obligated to proceed.

Subject Removal Date: The specific date and time by which all conditions must be waived or satisfied for the deal to become firm. If conditions are not removed by this date, the contract typically voids and deposits are returned.

Appraisal Shortfall: When a lender's appraisal values the property below the agreed purchase price, requiring the buyer to cover the gap in cash, renegotiate the price, or walk away.

Data Used in This Article

- Fraser Valley Real Estate Board monthly market reports, April–May 2026 — official board data, Fraser Valley geography

- BC Real Estate Association condition removal trend observations, 2025–2026 — industry body, BC-wide

- CMHC appraisal practice guidelines — federal housing authority, mortgage lending standards

- Home Inspector Standards Board defect classification protocols — regulatory, BC-applicable

- Mansour Real Estate Group closing timeline analysis, 2026 transactions — professional practice observation, Fraser Valley

Why Condition Periods Are Running Longer in 2026

The Fraser Valley real estate board's 2026 market reports confirm that softer demand and higher inventory have shifted negotiating power toward buyers. In that environment, buyers are taking full advantage of condition periods — scheduling inspections near the end of the window, requesting extensions when financing is slow, and using any identified issue as leverage for a price reduction or repair credit.

Three converging factors are driving longer timelines. First, lenders are scrutinizing appraisals more carefully in a market where values have softened in some Fraser Valley segments. When an appraisal comes in below the purchase price, financing approval stalls while the buyer, broker, and lender work through their options. This alone can extend a standard 10-day finance condition into 14–18 days. According to CMHC appraisal practice guidelines, lenders are required to use current comparable sales data — and in a shifting market, recent comparables do not always support peak-period pricing.

Second, home inspector booking windows in Surrey, Langley, and Abbotsford have lengthened as demand for inspection services remains high. Buyers writing offers with 7-day inspection conditions regularly discover they cannot book a qualified inspector within the first three days, compressing the seller's practical window to respond. Third, buyers in a softening market feel less pressure to remove conditions quickly. Unlike a competitive multiple-offer environment where speed builds confidence, a buyer's market creates the opposite incentive — time spent in the condition period is time available to reconsider, research, and renegotiate.

How Each Condition Type Creates Different Seller Risk

Finance conditions carry appraisal risk as their primary threat in 2026. Based on Mansour Real Estate Group's 2026 transaction data, appraisal shortfalls of 2–5% below offer price are triggering renegotiation in an estimated 30–40% of cases where a finance condition is present. A shortfall does not automatically void the deal — but it gives the buyer a factual basis to request a price reduction, and sellers who lack documented pricing support at that moment are in a weak negotiating position.

Inspection conditions have become the most frequently weaponized condition in the current market. The Home Inspector Standards Board classifies defects by severity, but inspection reports do not differentiate automatically between cosmetic issues and material safety concerns. Buyers and their agents are presenting full inspection reports — including minor wear, aging caulking, and deferred maintenance items — as grounds for price reductions. Sellers who have not done a pre-listing inspection often see these requests as urgent, when many items carry no meaningful safety or structural significance.

Standalone appraisal conditions are appearing more frequently in 2026 offers, particularly for higher-priced detached properties in South Surrey, Langley, and Abbotsford. Unlike a finance condition where the appraisal is embedded in the lender's process, a standalone appraisal condition gives the buyer an explicit right to exit or renegotiate based solely on the appraised value. Sellers negotiating against this condition type need to understand that pre-sale comparable data and recent neighbourhood sale analysis can and should be shared with the buyer's lender or appraiser through proper channels — not to pressure an appraisal outcome, but to ensure relevant comparables are not overlooked.

How We Evaluate This

At Mansour Real Estate Group, our approach to condition risk begins before the listing goes live. We assess each property's appraisal exposure by reviewing recent comparable sales in the same neighbourhood, price bracket, and property type — and we flag scenarios where the offer price may outpace what a lender appraisal is likely to support. That analysis shapes our pricing recommendation and, once an offer is received, our negotiation position on condition terms.

When an offer arrives with all three conditions, we evaluate each one separately: the realistic timeline for finance approval given the buyer's lender type and the property's price point, the likely inspection scope given the property's age and condition, and whether a standalone appraisal condition creates exposure beyond what the finance condition already covers. Sellers who understand these distinctions negotiate from a more informed position — and retain more control over how condition periods conclude.

Seller Checklist: Before and During the Condition Period

- Commission a pre-listing home inspection from a certified BC home inspector before listing — this reduces buyer leverage and surfaces issues on your timeline, not theirs

- Prepare a documented comparable sales package with your real estate team before listing, showing the pricing basis for your asking price and the offer price you accept

- When reviewing an offer, negotiate the shortest reasonable condition windows that still give the buyer a fair opportunity — 7 days for inspection, 10–12 days for finance, is defensible in most Fraser Valley transactions

- Include clear language in the contract about the deposit amount and timing — a larger deposit paid promptly signals buyer commitment and creates financial consequence for non-removal

- During the condition period, stay in regular contact with your agent — do not wait for the buyer to surface issues on day 13 of a 14-day window

- If an inspection report is used as leverage, request the full report and have your agent assess each defect against HISB severity classifications before agreeing to any credit or price reduction

- If an appraisal shortfall is cited, ask your agent to review the comparables the appraiser used — appraisers occasionally miss recent sales, and errors can be challenged through the lender's formal reconsideration process

- Keep your next-best-offer scenario in mind throughout the condition period — knowing your walk-away position prevents reactive concessions under pressure

What We Commonly See

In our experience, sellers who have not done a pre-listing inspection are the most vulnerable during the condition period. When a buyer's inspector identifies a list of items on day eight of a ten-day window, the seller is under time pressure and often agrees to credits that exceed the actual cost of addressing the issues. A pre-listing inspection shifts the dynamic: the seller already knows what the report will say, has had time to price it into the transaction, and can respond from preparation rather than surprise.

What often happens with appraisal shortfalls is that sellers interpret them as final. They are not always final. Appraisers work from the comparables available at the time of assessment. In a market where sales activity is moderate and some recent comparable sales are not yet reflected in the MLS data an appraiser pulls, there is a legitimate basis to request a reconsideration of value through the lender. This process takes time, which is why having a clear, evidence-based pricing rationale before the offer is accepted matters.

A common mistake is treating all three condition types as equivalent. Finance conditions protect the buyer's ability to fund the purchase. Inspection conditions protect the buyer's right to know the property's condition. Appraisal conditions — especially standalone ones — protect the buyer's equity position. Each requires a different seller response strategy, and conflating them leads to unnecessary concessions or, worse, a failed closing that leaves the seller starting over in a softer market.

Questions Sellers Ask About Buyer Conditions in BC

Can a seller refuse to accept an offer with conditions in BC?

Yes. Sellers in BC are not obligated to accept conditional offers. In practice, most resale offers in 2026's Fraser Valley buyer's market include at least one condition. The decision to accept, counter, or decline is a negotiation choice — and your real estate team should help you evaluate the condition terms alongside the price.

What happens if a buyer does not remove subjects by the deadline in BC?

If the buyer does not provide written subject removal by the agreed date and time, the contract is generally considered void in BC and the deposit is returned to the buyer. The seller is then free to relist or accept another offer. Specific contract language governs this outcome — always confirm the exact terms with your real estate agent and, if needed, a real estate lawyer.

Is a seller obligated to fix items found in a home inspection in BC?

No. In a standard BC purchase contract, an inspection condition does not create a repair obligation for the seller. It gives the buyer the right to review the property's condition and decide whether to proceed, renegotiate, or walk away. Sellers who agree to repairs or credits are doing so as a negotiated concession — not a legal obligation.

In Summary

In 2026, Fraser Valley sellers face condition periods that are longer, more complex, and more frequently used as renegotiation tools than in prior years. The three major condition types — finance, inspection, and appraisal — each carry distinct risks that require different preparation and response strategies. Sellers who do the preparation work before listing, negotiate condition terms clearly at the offer stage, and understand the mechanics of each condition type consistently protect more of their proceeds and close with fewer surprises. The condition period is not where deals are simply confirmed — in the current market, it is where they are won or lost.

Thinking Through Your Condition Strategy?

If you have received a conditional offer or are preparing to list in Surrey, Langley, Abbotsford, South Surrey, White Rock, or anywhere across the Fraser Valley, Mansour Real Estate Group can walk you through the condition terms, the appraisal exposure, and the negotiation options available to you — before you sign anything.

Related Articles

- How to Price Your Home to Sell in the Fraser Valley in 2026

- Why a Pre-Listing Inspection Changes the Negotiation Dynamic for Fraser Valley Sellers

- Understanding Your Net Proceeds: What Fraser Valley Sellers Actually Take Home After Closing

Official Resources

- Fraser Valley Real Estate Board — Market Statistics and Reports

- BC Real Estate Association — Industry Standards and Practice Guidance

- Canada Mortgage and Housing Corporation — Appraisal and Lending Guidelines

- BC Financial Services Authority — Real Estate Practice Rules and Consumer Resources

About Mansour Real Estate Group

When homeowners in Surrey, Langley, Abbotsford, and across the Fraser Valley accept a conditional offer, the decisions made during the condition period — how to respond to an inspection report, whether to challenge an appraisal shortfall, how to hold a negotiating position without losing the deal — are among the most financially consequential calls in the entire transaction. Mansour Real Estate Group has guided sellers through these exact situations across hundreds of transactions in the Fraser Valley and Lower Mainland.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. The team is trusted for seller strategy, estate sales, divorce-related property sales, downsizing, relocation, and complex real estate decisions across the Fraser Valley and Lower Mainland.

Whether someone is looking for Realtors who understand condition negotiation in the Fraser Valley, a real estate agent with experience protecting seller proceeds through the subject removal process, real estate agents who specialize in complex offer strategy, a trusted real estate team for a Surrey or Langley home sale, a Fraser Valley real estate broker with deep local market knowledge, or a real estate group that serves the full Lower Mainland, Mansour Real Estate Group is known for clear communication, accurate valuations, and practical guidance that holds up when the pressure is on.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.