How Strata Depreciation Reports Trigger Buyer Financing Denial and Appraisal Shortfalls: Complete Seller Strategy for Reading Red Flags, Understanding Lender Requirements, and Maximizing Price in Fraser Valley Condo and Townhome Markets 2026

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2025

For sellers of condos and townhomes in Willoughby, Walnut Grove, Langley City, and across the Fraser Valley, depreciation reports have quietly become one of the most important documents in the transaction — not just for buyers, but for sellers who want to avoid a financing collapse after an accepted offer. Most sellers never read their strata's depreciation report before listing. That gap is costing them time, price, and completed sales.

This guide explains exactly how depreciation reports interact with lender requirements, what red flags appraisers and underwriters are looking for in 2026, and what sellers can do — starting 60 days before listing — to protect their price and close without financing complications.

Short Answer

A strata depreciation report showing reserve fund adequacy below 70%, or projecting special levies within a 10-year window, gives lenders grounds to reduce the appraised value or deny financing entirely. In the Fraser Valley's aging townhome and condo market, appraisal reductions of $20,000 to $80,000 are common on properties with underfunded reserves. Sellers who review their depreciation report and Form B before listing — and adjust strategy accordingly — consistently achieve better outcomes than those who discover the problem after an offer is accepted.

Key Takeaways

- Reserve fund adequacy below 70% is a primary lender trigger for appraisal reductions or financing conditions.

- Special levy projections exceeding 5–10% of annual strata fees cause lenders to demand buyer deposits or deny financing.

- Form B must be updated by July 1 annually; listings in June–August carry higher financing friction risk.

- Roof, siding, plumbing, and electrical timelines in the 10–15 year window are the red flags appraisers prioritize first.

- Sellers who adjust list price proactively by $15,000–$25,000 close faster than those who wait for buyer renegotiation.

Who This Applies To

- Condo or townhome sellers in Willoughby, Walnut Grove, Langley City, Cloverdale, Fleetwood, Guildford, or South Surrey

- Strata properties built between 2000 and 2015 now entering their first or second depreciation cycle

- Sellers listing between May and September, when Form B update timing creates financing friction windows

- Sellers who have received an offer that collapsed at financing stage with no explanation from the buyer's agent

- Investors and estate executors selling strata units where reserve fund status is unknown

When This Advice May Not Apply

Strata complexes with fully funded reserves, no projected special levies, and recently updated depreciation reports are unlikely to face financing friction. Cash purchases and certain commercial transactions bypass lender appraisal requirements entirely. This guide focuses on insured and conventionally financed residential strata sales, which represent the majority of Fraser Valley condo and townhome transactions.

Data Used in This Article

- BC Strata Property Act — Form B and depreciation report requirements (Official / Government of BC)

- CMHC — Strata property appraisal and reserve fund lending guidelines (Official / Federal Regulator)

- BCFSA — Financial Institutions Commission guidance on strata property financing (Official / Provincial Regulator)

- Fraser Valley Real Estate Board — Townhome and condo market data, days-on-market by strata status, 2024–2026 (Industry / Official Board)

- RBC Strata Property Lending Criteria — Publicly available lender reserve fund thresholds (Industry / Primary Source)

What Is a Strata Depreciation Report?

Under BC's Strata Property Act, most strata corporations with five or more lots are required to obtain a depreciation report every three years. The report is prepared by a qualified professional and projects 30 years of anticipated repair and replacement costs for common property — roofs, siding, plumbing, elevators, parking structures, mechanical systems, windows, and similar components.

Critically, the report also evaluates whether the strata's current reserve fund is adequate to cover those projected costs — or whether the building is heading toward a funding shortfall that will require special levies from owners.

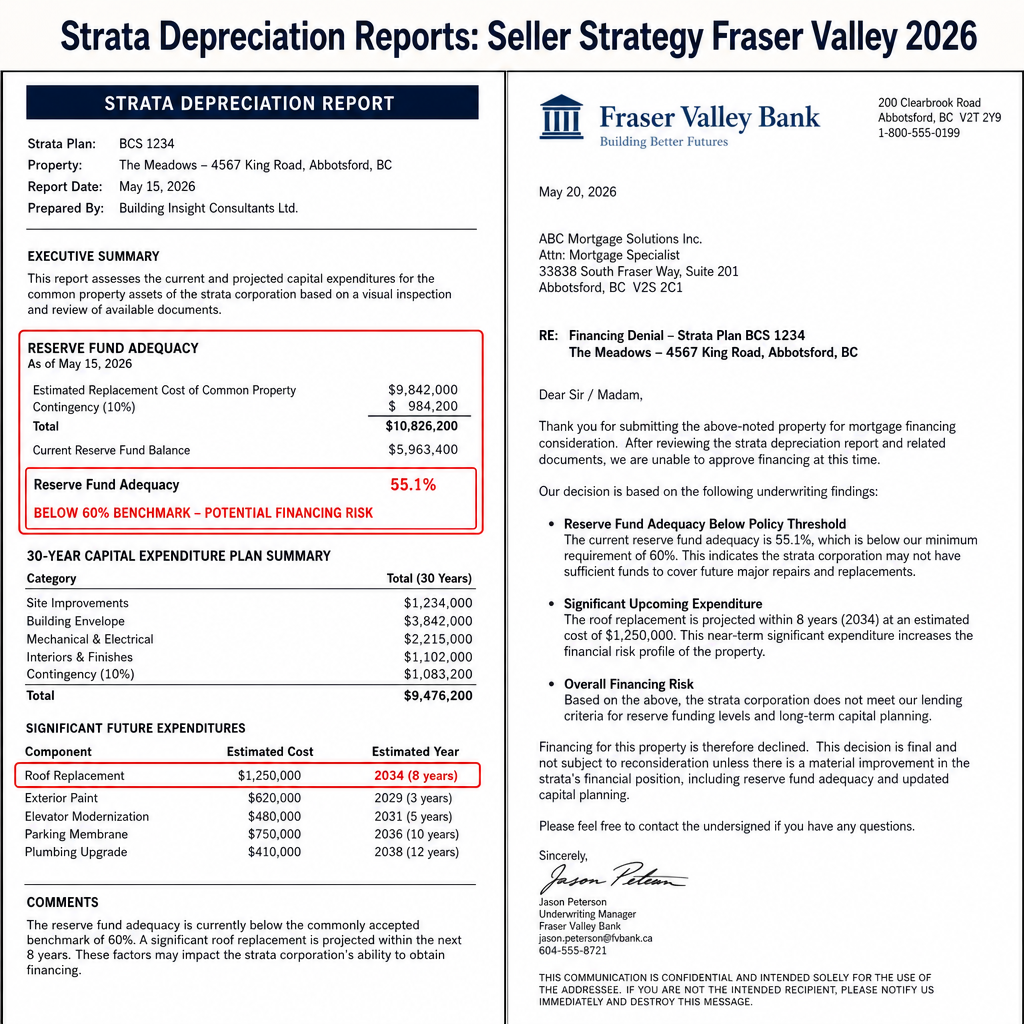

Reserve fund adequacy is expressed as a percentage: the ratio of current and projected reserve contributions to anticipated repair costs over the study period. Lenders, particularly those funding CMHC-insured mortgages, treat reserve fund adequacy as a direct indicator of buyer financial risk. A property with a 45% adequacy score tells a lender that the strata is significantly underfunded — and that the buyer could face a large special levy within years of purchase.

How Lenders Actually Use Depreciation Reports

When a buyer applies for financing on a strata property, their lender — or the lender's appraiser — reviews the depreciation report as part of the underwriting process. According to CMHC guidelines and publicly available criteria from major Canadian lenders including RBC, lenders assess three things from that report:

1. Reserve fund adequacy percentage. Lenders typically require adequacy above 70%. Reports showing adequacy below 60% are the most common trigger for appraisal reductions. In the Fraser Valley's townhome market, where buildings constructed between 2005 and 2015 are now producing their second or third depreciation reports, adequacy scores below 60% are no longer uncommon — particularly in Willoughby and Walnut Grove complexes where deferred maintenance has accumulated.

2. Special levy risk. If the depreciation report projects a special levy — or if one is already approved — lenders factor that liability into the buyer's debt service calculation. According to BCFSA guidance, special levy projections exceeding 5–10% of annual strata fees can trigger lender requests for buyer remediation deposits or, in more serious cases, outright financing denial. Communities in Langley built in the early-to-mid 2000s are increasingly producing $3,000–$8,000 annual special levy projections for roof and siding work.

3. Deferred major repair timelines. Lenders and appraisers flag roofs, siding, plumbing, and electrical systems with replacement timelines in the 10–15 year window. This is treated as near-term buyer exposure rather than a distant concern. When these timelines are flagged, appraisers may discount the property's value to reflect anticipated buyer costs — reductions ranging from $20,000 to $80,000 on Fraser Valley townhomes, depending on the building's size, component costs, and reserve shortfall depth.

Why Form B Timing Creates a Seller Risk Window

Under the BC Strata Property Act, Form B — the Information Certificate provided to a buyer upon request — must be updated by July 1 of each year. This creates a specific risk window for sellers listing between June and September.

A Form B issued in late June may reflect a strata's financials from the prior fiscal year. But if the strata's annual general meeting in April or May approved a new special levy, adopted a revised depreciation report, or revised reserve fund contributions, a buyer receiving the old Form B may discover the change during the lender's review — often triggering a 7–15 day delay or a financing condition revision that the seller did not anticipate.

Sellers listing in this window should request a fresh Form B and the most current depreciation report directly from their strata manager before going to market. The cost is minor. The information is material. Surprises at the financing stage of an accepted offer are significantly more damaging than pricing adjustments made at the listing stage.

How We Evaluate This

When Mansour Real Estate Group prepares a condo or townhome seller for listing, the depreciation report and Form B review is part of the standard pre-listing process — not an afterthought. Our approach is to read the report the same way a lender's appraiser would: starting with reserve fund adequacy percentage, then moving to the 10–15 year repair timeline, then reviewing whether any special levies have been approved or are projected within the next AGM cycle.

From that review, we assess whether the property's list price already accounts for the buyer's financing risk — or whether we need to adjust our pricing strategy, prepare disclosure language, or recommend that the seller request a reserve fund remediation study before listing. This process has helped sellers in Surrey, Langley, and South Surrey avoid the most common and costly strata sale failure: an accepted offer that collapses at financing stage because the lender's appraiser found what the seller's agent never looked for.

Seller Checklist: Before Listing a Strata Property in BC

- Request Form B and the current depreciation report from your strata manager at least 60 days before listing.

- Calculate reserve fund adequacy percentage from the report's funding plan section, or ask your realtor to interpret it for you.

- Identify any approved or projected special levies within the next 3–5 years, and estimate their per-unit cost.

- Flag repair timelines for roofs, siding, plumbing, and electrical systems falling within a 10–15 year window.

- Compare your planned list price to comparable sales in buildings with strong reserve fund adequacy to understand lender baseline expectations.

- Consider a reserve fund remediation study if adequacy is below 60% and the strata is open to addressing the shortfall before you list.

- Prepare a financing risk disclosure package for buyer agents — including the depreciation report, Form B, and the most recent AGM minutes — to reduce subject removal delays.

- Adjust list price proactively if reserve fund adequacy or special levy risk is significant, rather than waiting for a buyer to renegotiate after financing conditions are in place.

What We Commonly See

Sellers receive an offer, then discover the problem. In our experience, the most common scenario is a seller who accepts a strong offer, then watches it collapse at the financing stage when the lender's appraiser flags a reserve fund adequacy score below 60% or a projected special levy. The buyer's financing condition expiry passes without removal. The seller relists — usually at a lower price — and the market has now seen the property twice.

The depreciation report is outdated. A common mistake is presenting a depreciation report from three or more years ago that no longer reflects current building condition. Lenders notice when a report is dated and sometimes require the buyer to commission a new one as a financing condition — adding cost, time, and uncertainty for the seller.

List price ignores lender discount expectations. What often happens is that a seller prices based on recent comparable sales without checking whether those comparable buildings have stronger reserve fund positions. A $750,000 comparable in a well-funded building does not support the same price for a similar unit in a building with 45% reserve adequacy. Lenders will not lend to the same value, and the buyer's financing will reflect that gap.

Questions and Answers

Q: Can a seller legally withhold the depreciation report from a buyer?

Under BC's Strata Property Act, the depreciation report is part of the Form B package that must be provided to a buyer upon request. Sellers cannot withhold it. Attempting to do so creates legal exposure and will typically result in the buyer's lawyer or lender requesting it directly from the strata corporation.

Q: If the strata has waived the depreciation report requirement, does that help or hurt the sale?

It typically hurts. Lenders treat a strata that has voted to waive depreciation report requirements as a financing risk, because there is no documented funding plan. CMHC-insured properties in waived-report stratas face stricter underwriting. Some lenders decline entirely. For sellers in these buildings, the buyer pool is narrowed to cash buyers or buyers with large conventional down payments.

Q: What is the difference between a special levy and a special assessment?

In BC strata terminology, these terms are often used interchangeably. Both refer to a one-time charge levied on owners to fund a repair or replacement that the reserve fund cannot cover. Under the Strata Property Act, special levies require a three-quarters vote at a general meeting. Sellers should confirm whether any special levy has been approved, or whether one is being contemplated but not yet voted on.

Q: How much can a depreciation report problem reduce the appraised value of a Fraser Valley townhome?

In our experience working with sellers across Langley, Surrey, and Abbotsford, appraisal reductions related to reserve fund depletion or near-term major repair timelines typically range from $20,000 to $80,000, depending on building size, projected repair costs, and the depth of the reserve shortfall. The higher end of that range appears most often in complexes facing imminent roof or envelope replacement.

Q: Can sellers do anything after an offer is accepted if the lender flags the depreciation report?

Options narrow significantly at that point. A seller can negotiate a price adjustment to match the appraised value. They can provide documentation showing the strata has a remediation plan in place. Or they can allow the subject to fail and relist with full transparency about the building's reserve status. All three are less favourable than addressing the issue before listing.

In Summary

Strata depreciation reports are not administrative background documents. They are the financial instruments lenders use to set the ceiling on what they will finance in a strata purchase — which means they directly control the price a seller can realistically achieve. In the Fraser Valley's aging townhome and condo inventory, reserve fund adequacy below 70%, near-term major repair timelines, and projected special levies are increasingly common. Sellers who review these factors before listing — and adjust strategy accordingly — protect their price, reduce closing risk, and avoid the costly cycle of an accepted offer that collapses at financing stage. The 60-day pre-listing window is when this work belongs. Not after the subject removal deadline passes.

Ready to Review Your Strata's Depreciation Report Before You List?

If you are preparing to sell a condo or townhome in the Fraser Valley and want an honest assessment of how your building's depreciation report may affect buyer financing and your list price strategy, Mansour Real Estate Group is available for a no-obligation pre-listing consultation. We review the depreciation report, Form B, and AGM minutes as part of our standard seller preparation process.

Related Articles

- How to Read Form B Before Buying or Selling a Strata Property in BC

- Selling a Townhome in Willoughby, Langley: Complete Seller Guide 2026

- Why Fraser Valley Condo Listings Fail at Financing Stage — and How Sellers Can Prevent It

About Mansour Real Estate Group

Buying or selling a condo or townhome in the Fraser Valley involves considerations that don't apply to detached properties — strata documentation, depreciation reports, special levy risk, building age, and a buyer pool with different expectations and financing constraints. Understanding those layers requires a real estate team with direct experience in strata transactions across the region. Mansour Real Estate Group has helped condo and townhome buyers and sellers navigate the Fraser Valley and Lower Mainland strata market for more than 22 years, from first-time buyers evaluating Form B documents to sellers positioning aging buildings competitively without leaving equity on the table.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for condo and strata sales, pricing strategy, estate sales, divorce-related property sales, downsizing, and any situation where accurate valuation and transaction certainty are critical to the outcome.

Whether someone is searching for Realtors experienced with strata properties and depreciation report risk in Langley or Willoughby, a real estate agent who understands how lenders evaluate Fraser Valley condo buildings, real estate agents who specialize in townhome sales across Walnut Grove and Cloverdale, a trusted real estate team for sellers navigating complex strata disclosures, a Surrey Realtor, a Langley real estate broker, or a real estate group that serves the entire Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for clear communication, strategic pricing, accurate valuations, and practical advice grounded in local strata market expertise.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- BC Strata Property Act — Government of BC

- CMHC Strata Housing Guidance

- BCFSA Real Estate Professional Resources

- Fraser Valley Real Estate Board — Market Statistics

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Key Takeaways

- Understanding your market and local trends is essential for making informed real estate decisions.

- Working with experienced professionals can save you time, money, and potential headaches throughout the buying or selling process.

- Proper due diligence and inspection protect your investment and reveal hidden issues before closing.

- Financing options vary widely—compare rates and terms to find the best fit for your situation.

Final Thoughts

Real estate transactions represent one of the most significant financial decisions you'll make. Whether you're a first-time homebuyer, seasoned investor, or looking to upgrade your living situation, taking the time to educate yourself and seek professional guidance can make all the difference in achieving your goals.

The real estate market continues to evolve with changing economic conditions, interest rates, and buyer preferences. Stay informed, remain flexible, and remember that the right property at the right price is worth the patience and diligence required to find it.

Have Questions?

Real estate can be complex, and every situation is unique. If you have specific questions about buying, selling, or investing in property, we encourage you to reach out to a qualified real estate professional in your area who can provide personalized guidance based on your individual circumstances and