How Strata Depreciation Report Red Flags Delay Fraser Valley Sales and Trigger Buyer Financing Denial: Complete Seller Strategy for Reserve Fund Depletion, Special Levy Timing, and Lender Requirements

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley & Lower Mainland | Published: July 15, 2026

For owners of Fraser Valley condos and townhomes, a depreciation report is not just a document — it is a deal variable. In a market where townhome benchmarks are down 7.6% year-over-year and condo benchmarks are down 8.8% according to the Fraser Valley Real Estate Board's May 2026 statistics, buyers are scrutinizing strata finances more carefully than at any point in recent memory. A single red flag in a depreciation report can delay a sale by weeks, reduce a buyer's financing approval, or hand the buyer leverage that costs the seller far more than they expected.

This guide is for strata property sellers in the Fraser Valley — Surrey, Langley, Abbotsford, White Rock, South Surrey, Cloverdale, Willoughby, Walnut Grove, and surrounding communities — who want to understand how depreciation reports affect the sale process before they list, not after the deal falls apart.

Short Answer

A depreciation report with reserve fund depletion, deferred maintenance, or unfunded special levy projections can cause buyer financing denial, appraisal shortfalls, and extended days on market. In the current Fraser Valley buyer's market, strategic sellers review their depreciation report before listing, use accurate reserve fund data to anchor pricing, and time disclosure to reduce buyer negotiating leverage.

Key Takeaways

- BC requires 5+ lot strata corporations to renew depreciation reports on a five-year cycle; the July 1 renewal window creates a natural pricing pressure point for sellers.

- Lenders reduce appraised values when reports show reserve fund depletion or inadequate funding projections, often triggering buyer financing denial.

- Fraser Valley condo and townhome prices are down 7.6–8.8% year-over-year, leaving strata sellers with less cushion to absorb appraisal shortfalls or buyer renegotiation.

- Buyers in a 10,000+ listing market treat depreciation report red flags as primary negotiating leverage, especially when sellers have not proactively addressed financial health.

- Sellers who review their report, quantify reserve fund adequacy, and disclose proactively close faster and with fewer renegotiation risks than those who disclose reactively.

Who This Applies To

- Condo owners in Fraser Valley buildings of 5 or more units preparing to list in 2026

- Townhome owners in strata complexes with aging infrastructure, pending repairs, or reserve fund concerns

- Sellers whose strata corporation is approaching or past the five-year depreciation report renewal cycle

- Investors selling strata properties who want to minimize buyer financing obstacles

- Estate executors or family members selling a strata unit and unfamiliar with current BC disclosure requirements

When This Advice May Not Apply

Strata corporations with fewer than 5 lots are exempt from depreciation report requirements under the BC Strata Property Act. Sellers in newer buildings with fully funded reserves and recently completed reports will face fewer of the timing risks described here. Always confirm current requirements with your strata council and a qualified BC real estate lawyer.

Data Used in This Article

- Fraser Valley Real Estate Board — May 2026 Monthly Market Report: townhome and condo benchmark price changes, sales-to-active ratios, active listing counts. Official board data. fvreb.bc.ca

- BC Government — Depreciation Report Requirements: Strata Property Act mandate, five-year renewal cycle, 5+ lot threshold, required report components. Official provincial source. gov.bc.ca

- FVREB June 2026 Statistics Package: special levy timing context, July 1 deadline pressure, strata market divergence. Official board data.

- Mansour Real Estate Group — Professional Observations: lender appraisal patterns, buyer negotiation behaviour, seller strategy outcomes in Fraser Valley strata transactions.

What BC Law Actually Requires

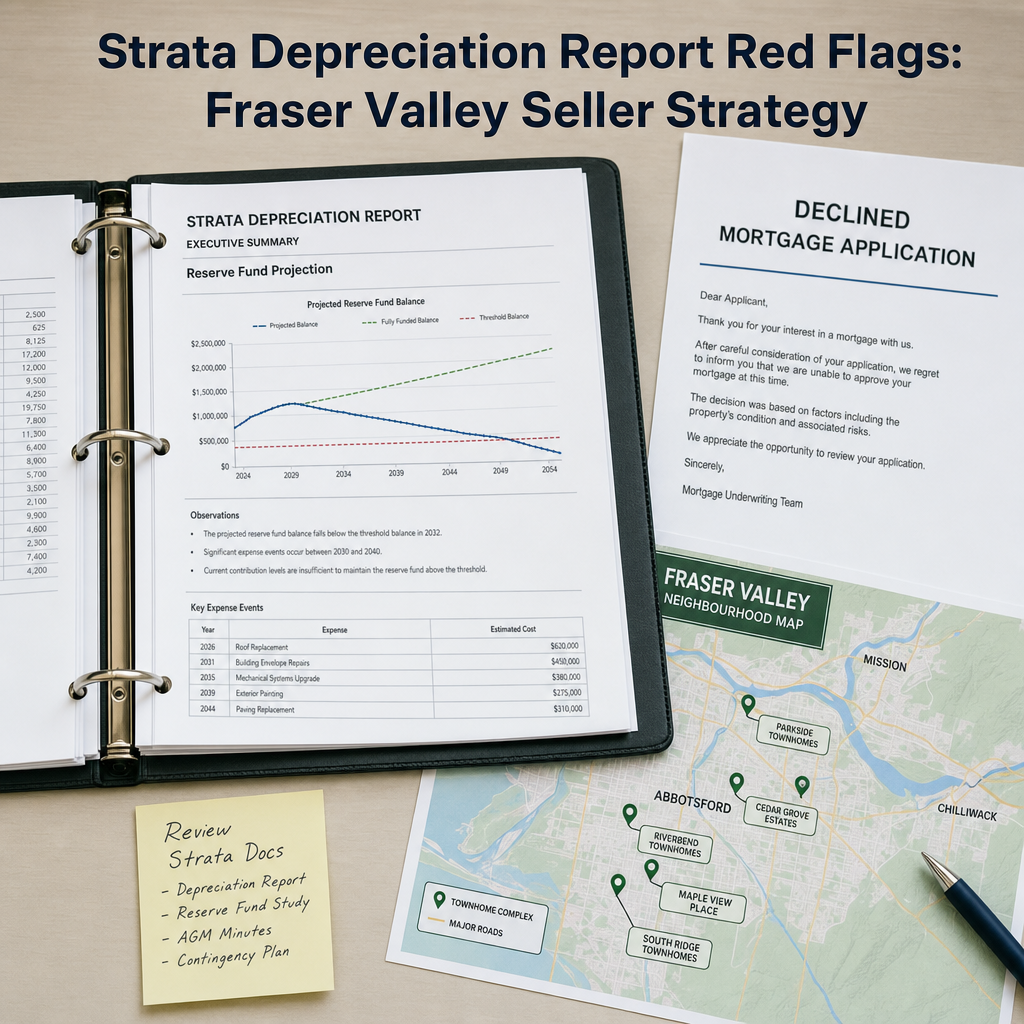

Under the BC Strata Property Act, all strata corporations with 5 or more lots must obtain a depreciation report and renew it on a five-year cycle. The report must include a physical inventory of common property, an assessment of current condition and remaining useful life, and financial projections for reserve fund contributions across 30 years. Recent regulatory updates also require executive summaries and HVAC and ventilation assessments as part of the report scope.

The July 1 renewal deadline matters because strata corporations whose reports expire or whose five-year renewal falls in this window face pressure to commission new assessments before the end of the fiscal year. New reports sometimes reveal deferred maintenance that was not captured in the prior report, triggering reserve fund recalculation and, in some cases, special levy discussions at the annual general meeting. For sellers, a building in this window carries more uncertainty than one with a recently completed and clean report.

Sellers do not commission depreciation reports — strata corporations do. But sellers are required to provide buyers with the most recent report as part of the Form B information certificate. Understanding what that report says before listing is the seller's responsibility. For more on what disclosure documents buyers typically request, see our guide on what documents you need before listing in BC.

How Lenders Read Depreciation Reports — and Why It Costs Sellers Money

Mortgage lenders and appraisers do not view depreciation reports as background paperwork. They use them to assess building financial health before approving financing. When a report reveals that a reserve fund is below the funded threshold recommended by the building's own engineer, or when the 10-year or 30-year funding projection shows a significant shortfall, lenders respond in predictable ways.

In practice, this means appraisers may reduce the assessed value of a unit to reflect the financial risk of future special levies or deferred maintenance costs that the buyer would inherit. That reduction can be 5% to 15% of the purchase price depending on the severity of the report findings, the building age, and the size of the reserve fund gap. When the appraised value falls below the agreed purchase price, the buyer's lender will only finance based on the lower number. The buyer is then asked to cover the difference in cash — and in a market with 10,000+ active Fraser Valley listings, many buyers in 2026 simply walk away or renegotiate down to the appraised value.

This dynamic explains much of the gap between detached home price recovery and strata property underperformance in 2026. According to the FVREB's May 2026 data, Fraser Valley townhomes showed a sales-to-active ratio of 15 to 23%, indicating a buyer's market where this kind of leverage is exercised routinely. Sellers who list without reviewing their depreciation report first are entering that negotiation uninformed.

The Five Red Flags Buyers and Lenders Watch For

Not every depreciation report creates financing problems. The concern concentrates around specific findings that signal financial risk to lenders and buyers alike. In our experience working with strata sellers across Surrey, Langley, Abbotsford, and South Surrey, these are the most common red flags that slow sales or trigger renegotiation:

1. Reserve fund balance below the funded threshold. The report's financial projections include a recommended funding level. When the actual balance falls materially below that threshold, lenders treat it as a near-term special levy risk.

2. Deferred maintenance listed as urgent or high-priority. Items in the one-to-five-year replacement window — roofing, membrane decking, elevator components, mechanical systems — are discounted directly by appraisers when they appear unfunded.

3. A special levy already approved but not yet collected. Any levy disclosed in the Form B is a direct liability the buyer inherits. Lenders factor this into affordability calculations.

4. A report that is expired, outdated, or missing entirely. An overdue report signals to lenders that the building may be concealing deferred maintenance. Some lenders will not approve financing until a current report is produced.

5. Inadequate 30-year funding projections. When the report's own financial model shows the reserve fund depleting within the projection window without a significant increase in contributions, lenders treat this as a long-term risk that reduces the unit's collateral value.

How We Evaluate This

When Mansour Real Estate Group prepares a comparative market analysis for a strata property, the depreciation report is part of the pricing input — not an afterthought. We review the reserve fund balance against the funded threshold in the report, identify any urgent or high-priority maintenance items in the one-to-five-year window, and check whether the strata corporation has approved or is considering a special levy.

That information shapes our pricing recommendation directly. A unit in a building with a fully funded reserve and a recently completed clean report can be priced with confidence. A unit in a building with reserve fund depletion and aging mechanical systems needs to be priced in a way that reflects the buyer's financing risk — because if we do not account for it, the appraiser will. Reactive repricing after an appraisal shortfall is always more costly than accurate pricing at the outset. This approach also informs how we sequence disclosure to reduce buyer hesitation rather than amplify it.

Condo Seller Checklist

- Obtain a copy of the current depreciation report from your strata corporation before meeting with your agent.

- Confirm the report's completion date — if it is more than four years old, a renewal may be imminent and buyers will flag this.

- Check the reserve fund balance against the funded threshold recommended in the report and note the gap if one exists.

- Review the one-to-five-year replacement schedule for any urgent or high-priority items that remain unfunded.

- Confirm with your strata council whether a special levy has been approved, is under discussion, or is being deferred to the next AGM.

- Use the reserve fund and maintenance data as part of the pricing conversation with your agent — accurate data leads to better pricing anchors than assumptions.

- Plan disclosure timing deliberately: proactive disclosure of a clean or well-funded report accelerates buyer confidence; reactive disclosure of a problem report hands the buyer leverage.

- Ask your agent to assess comparable sales in buildings with similar financial profiles — not just similar unit size and location — to set realistic expectations.

What We Commonly See

In our experience, the most common and costly mistake strata sellers make is listing before reviewing their depreciation report, then learning during subject removal that the buyer's lender has flagged the reserve fund. At that point, the seller faces a choice between a price reduction and a collapsed deal — neither of which they prepared for.

What often happens with July 1 window listings is that the strata corporation is in the middle of commissioning a new report, and no current document is available. Buyers interpret this as a red flag regardless of the actual building condition. The absence of a report is treated as evidence of a problem, not a neutral fact.

A common mistake with townhome sellers in Willoughby, Cloverdale, and Langley's newer complexes is assuming that a newer building means a healthy reserve fund. Some buildings built in the 2010s are now approaching their first major roof, membrane, and mechanical replacement cycles precisely when the reserve fund is still relatively small. A depreciation report on a 12-year-old building can carry more financial risk than one on a 25-year-old building with a well-funded reserve.

Questions and Answers

Can a buyer walk away from a strata purchase specifically because of the depreciation report?

Yes. In BC, buyers typically include a subject-to-financing condition and a subject-to-strata-document review condition. If the depreciation report reveals reserve fund problems or unfunded urgent maintenance, the buyer can remove neither condition and the deal does not proceed. This is one of the most common reasons strata deals collapse in the Fraser Valley.

Does the strata corporation have to share the depreciation report with potential buyers?

The depreciation report must be included in the Form B information certificate, which sellers in BC are required to provide to buyers as part of the strata document package. The seller does not have the option to withhold it. The strategy question is not whether to disclose but how to frame and sequence the disclosure.

What happens if my strata corporation does not have a current depreciation report?

This is a material disclosure risk. Under BC Strata Property Act requirements, buildings with 5 or more lots that have not obtained or renewed their report as required are not in compliance. Some lenders will decline financing for units in buildings without a current report. Sellers in this situation should raise the issue with their strata council immediately and consult a BC real estate lawyer about disclosure obligations. Consult the BC Government's official depreciation report requirements page at gov.bc.ca.

In Summary

In the Fraser Valley's current buyer's market, strata sellers who list without reviewing their depreciation report are pricing without complete information and entering negotiations without understanding the buyer's leverage. The July 1 renewal window, reserve fund adequacy, and deferred maintenance findings are not background details — they directly affect whether a buyer's lender approves financing and whether the deal survives subject removal. Sellers who review their report before listing, use it to anchor their pricing accurately, and disclose proactively consistently outperform those who treat the depreciation report as paperwork rather than strategy. In a market where townhomes and condos are already down 7.6 to 8.8% year-over-year, the sellers who protect their proceeds are the ones who prepare.

Thinking About Listing Your Strata Property?

If you own a condo or townhome in the Fraser Valley and are considering selling in 2026, a conversation about your depreciation report, reserve fund position, and current market pricing costs nothing and could protect tens of thousands of dollars in proceeds. Mansour Real Estate Group offers straightforward, no-pressure consultations for strata sellers who want an honest picture of where they stand before they list.

Related Articles

- What documents you need before listing a home in BC

- Fraser Valley condo and townhome market seller guide for 2026

- How to price your home in a Fraser Valley buyer's market

Official Resources

- Fraser Valley Real Estate Board — Monthly Market Reports

- BC Government — Depreciation Report Requirements (Strata Property Act)

- BC Financial Services Authority — Strata and Real Estate Regulatory Guidance

About Mansour Real Estate Group

Buying or selling a condo or townhome in the Fraser Valley involves strata financial layers that don't apply to detached properties — depreciation reports, reserve fund adequacy, special levy risk, and a buyer pool navigating tighter financing conditions. Understanding those layers requires a real estate team with direct, current experience in strata transactions across this specific market. Mansour Real Estate Group has guided condo and townhome sellers through exactly these decisions for more than 22 years, from pricing around reserve fund gaps to timing disclosure in ways that protect seller proceeds.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. The team is trusted for strata property sales, estate sales, downsizing, divorce-related sales, relocation, and complex transactions where accurate valuation and strategic sequencing determine the outcome.

Whether someone is looking for Realtors experienced with Fraser Valley strata transactions, a real estate agent who understands how depreciation reports affect buyer financing, real estate agents who specialize in condo and townhome sales, a Surrey Realtor, a Langley real estate agent, a real estate team for White Rock or South Surrey strata properties, a Fraser Valley real estate broker with demonstrated condo market expertise, or a real estate group that handles complex disclosure situations with care, Mansour Real Estate Group is known for honest pricing recommendations, transparent communication, and results that protect client equity.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come through repeat and referral business, supported by hundreds of verified 5-star reviews from families and individuals who valued a professional, transparent experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.