How Strata Depreciation Report Red Flags Affect Buyer Financing, Appraisal Value, and Sale Price in Fraser Valley Condo and Townhome Markets 2026

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 14, 2025 | Fraser Valley and Lower Mainland, BC

If you are selling a condo or townhome in the Fraser Valley right now, your depreciation report is doing more work than you may realize. Lenders and appraisers are reading it carefully. Buyers and their agents are flagging specific lines. In Willoughby, Walnut Grove, and Langley strata communities, the difference between a clean report and a flagged one is increasingly the difference between a smooth sale and a renegotiated one.

This article explains the direct connection between specific depreciation report findings and three seller outcomes: financing denial, appraisal shortfalls, and negotiated price reductions. Understanding that chain — and knowing what triggers each outcome — is what allows a seller to price correctly and negotiate from a position of awareness rather than surprise.

Short Answer

Depreciation reports flagging reserve fund depletion below 70%, special levy forecasts above $5,000 annually, or deferred maintenance on roofing, waterproofing, or HVAC now trigger lender scrutiny that can reduce appraised value by 5–12%, delay financing by 30–60 days, and give buyers 3–8% renegotiation leverage on Fraser Valley strata properties. Sellers who understand these triggers before listing can price and prepare accordingly.

Key Takeaways

- Reserve fund depletion below 70% now triggers mandatory independent audits under CMHC's Q1 2026 lending guidelines before financing approval.

- Appraisers are applying 5–12% downward adjustments on strata buildings over 20 years old with deferred maintenance on critical systems.

- Subject-to-financing conditions are taking 15–30 days longer to resolve when depreciation reports contain red flags, increasing deal collapse risk.

- Buyers in current Fraser Valley strata markets are using flagged reports to negotiate 3–8% off list price — a shift from the 0–2% norm in pre-2025 detached sales.

- Sellers listing strata properties before July 1 may avoid disclosure of updated depreciation reports; those listing after face 60–90 day delays that compress buyer confidence.

Who This Applies To

- Condo or townhome sellers in Willoughby, Walnut Grove, Langley, Cloverdale, Fleetwood, Guildford, or Abbotsford strata communities

- Sellers in buildings over 15 years old where reserve fund studies have been recently updated

- Executors or estate representatives selling strata properties who need to understand current lender scrutiny

- Investors or downsizers evaluating whether to sell now or wait for report conditions to improve

When This Advice May Not Apply

Newer strata buildings with fully funded reserves, recently completed capital projects, and no deferred maintenance will face less scrutiny under current lender guidelines. This article addresses buildings with identifiable depreciation report risk — primarily those 15 years or older with deferred or underfunded capital items.

Data Used in This Article

- BCFSA Strata Property Act Regulations and Form B Requirements, 2026 — Official / Regulatory

- CMHC Mortgage Insurance Appraisal Guidelines, Q1 2026 Update — Official / Lender Policy

- Fraser Valley Real Estate Board, Days-on-Market and Sales Ratio Data by Property Type, April 2026 — Official / Market Statistics

- Mansour Real Estate Group internal transaction data, strata price concessions and financing timelines, Q1–Q2 2026 — Internal / Professional Analysis

Definitions

Depreciation Report: A mandatory strata document estimating the cost and timing of future capital repairs, used by lenders and appraisers to assess building financial health.

Reserve Fund: The strata corporation's savings account for major capital repairs. A funding level below 70% of the recommended balance is a standard lender red flag.

Special Levy: A one-time charge to strata owners when the reserve fund cannot cover a required capital repair.

Form B (Information Certificate): The official strata disclosure document required by BC law under the Strata Property Act that must be provided to buyers, including reserve fund balance and any known special levies.

Subject-to-Financing Condition: A buyer condition that allows the buyer to withdraw if their lender does not approve financing — typically within 5–10 business days, but now extending 30–60 days on flagged strata properties.

How We Evaluate This

When Mansour Real Estate Group evaluates a strata listing, the depreciation report is reviewed before pricing strategy is set. We are looking for the same three things a lender's appraiser will look for: reserve fund funding percentage, deferred maintenance on critical systems, and any special levy forecast in the next three to five years. Those three items determine what financing risk the buyer faces — and therefore what price a seller can realistically expect to achieve.

In markets like Willoughby and Walnut Grove, where a significant portion of townhome and condo inventory was built between 2000 and 2010, reserve fund depletion is increasingly common. We cross-reference internal transaction data with current FVREB sales-to-active ratios and recent CMHC appraisal guideline updates to build a pricing model that accounts for lender behavior, not just comparable sales. A comparable sale that closed before Q1 2026 CMHC changes may not reflect what the same property would appraise for today.

The Three Outcomes Sellers Need to Understand

1. Financing Denial and Condition Delays

Under CMHC's Q1 2026 mortgage insurance appraisal guidelines, lenders are required to obtain independent reserve fund audits before approving insured financing on strata properties where the depreciation report shows reserve fund depletion below 70% or annual special levy forecasts exceeding $5,000. This is not a discretionary lender decision — it is a protocol change that applies across CMHC-insured purchases, which represent a substantial portion of Fraser Valley condo and townhome transactions.

The practical effect for sellers is a financing condition that cannot be removed in the standard 5–10 business day window. Based on transaction data from Q1–Q2 2026, subject-to-financing conditions on flagged strata properties are taking 30 to 60 additional days to resolve — and in some cases collapsing entirely when the independent audit confirms the reserve fund concern. For sellers carrying a property through that extended window, the costs are real: mortgage payments, strata fees, property taxes, and the market risk of sitting while new listings arrive.

Buyers whose lenders ultimately decline financing on a flagged building do not simply walk away quietly. In a buyer-favored market where Fraser Valley condo sales-to-active ratios are running at 6–8% according to FVREB April 2026 data, a collapsed deal often means the property re-lists at a perceptibly lower price — which signals distress to the next buyer and compounds the pricing problem.

2. Appraisal Shortfalls

When a lender orders an appraisal on a strata property, the appraiser has access to the depreciation report through the Form B disclosure package. On buildings over 20 years old with deferred maintenance on roofing, waterproofing, envelope, or HVAC systems, appraisers are applying downward adjustments of 5–12% relative to comparable non-strata or well-maintained strata properties.

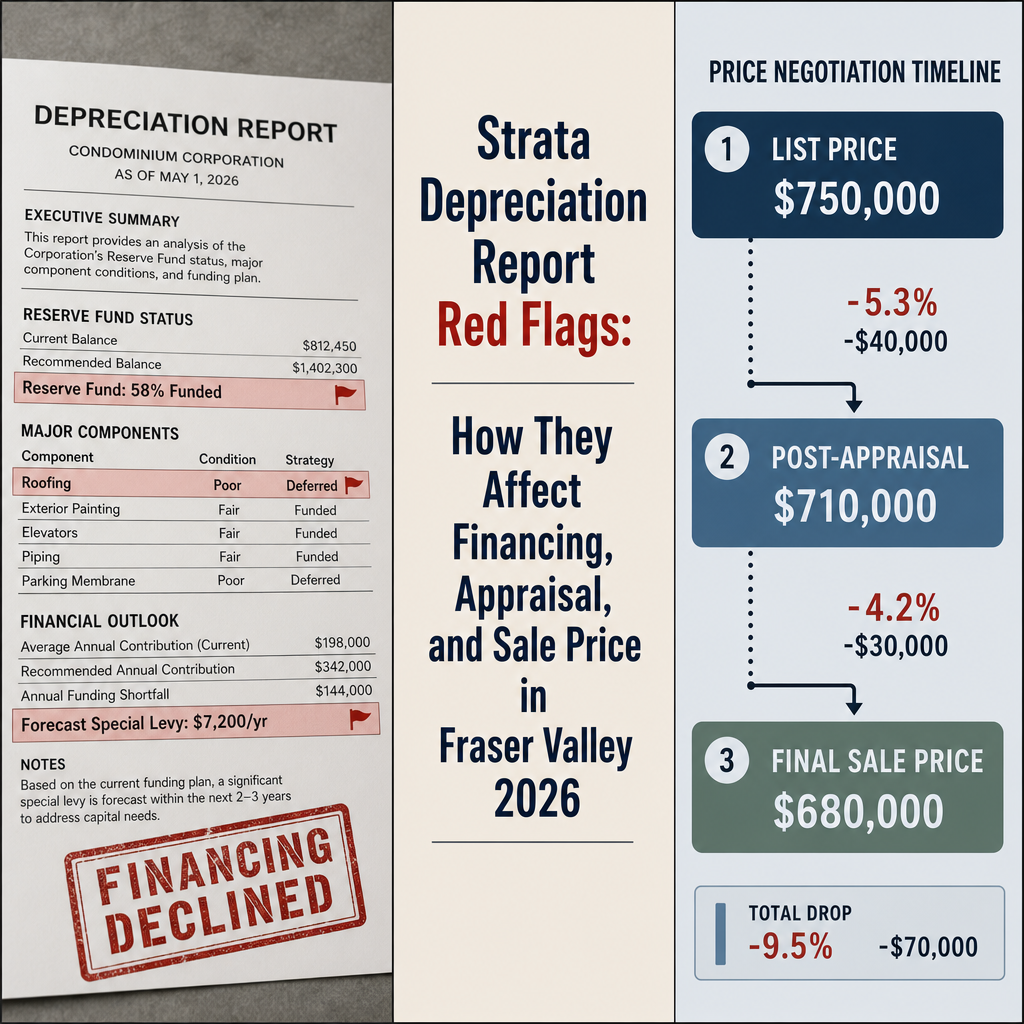

This adjustment is not arbitrary. It reflects the capitalized cost of anticipated future repairs that the reserve fund may not cover. A $750,000 townhome in Willoughby with a 58% funded reserve and a forecast roofing project in year four can appraise at $660,000 to $712,500 under current lender guidelines — a gap of $37,500 to $90,000 below the agreed purchase price. When appraisal comes in below the purchase price, the buyer faces a choice: cover the shortfall in cash, renegotiate the price, or exit the contract. In today's Fraser Valley market, most buyers choose to renegotiate.

Sellers in Walnut Grove and Langley strata communities are reporting average post-appraisal price reductions of $35,000 to $60,000 when depreciation reports surface, compared to $0 to $10,000 in pre-2025 markets. That shift is directly traceable to the Q1 2026 CMHC guideline changes and the aging of Fraser Valley's strata inventory.

3. Buyer Renegotiation Leverage

Even when financing is ultimately approved and an appraisal does not technically come in short, flagged depreciation reports give buyers documented grounds to renegotiate. The depreciation report is not an opinion — it is a professionally prepared estimate of future capital costs. When a buyer's agent identifies a $25,000 roofing reserve shortfall or a $7,200 annual special levy forecast, they are holding a financial document that supports a price reduction request before subject removal.

In detached home sales, buyer renegotiation leverage post-inspection typically runs 0–2% of purchase price in normal market conditions. In strata markets with flagged depreciation reports, that leverage increases to 3–8% — and in Fraser Valley's current buyer-favored strata market, sellers are absorbing it rather than losing the deal entirely. On a $650,000 condo, 3–8% is $19,500 to $52,000 in concessions the seller did not anticipate when they set their list price.

The July 1 Disclosure Window

BC's Strata Property Act requires updated depreciation reports on a mandatory cycle. In practice, many Fraser Valley strata corporations receive updated reports in or around mid-year. Sellers listing before July 1 may be presenting buyers with a report that does not yet reflect the most recent reserve fund study — avoiding updated capital cost estimates for another listing season. Sellers listing after July 1 often face a 60–90 day window during which a recently completed but not-yet-circulated report introduces uncertainty for buyers and their lenders.

This timing asymmetry is not widely understood among sellers, but it matters. A building that receives a materially worse depreciation report in June will have that report in buyers' hands by August — and in lenders' hands immediately thereafter. For sellers in buildings with known upcoming capital projects, listing before that disclosure window closes is a legitimate and defensible timing strategy. It is not deception; the strata corporation is required to disclose through Form B what it currently knows, and buyers retain the right to review all available strata documentation during their due diligence period.

Condo Seller Checklist: Depreciation Report Risk Assessment

- Obtain the current depreciation report and Form B before setting list price — not after accepting an offer.

- Check the reserve fund funding percentage. Anything below 70% should be factored into your pricing strategy as a likely lender scrutiny trigger.

- Review deferred maintenance items on roofing, waterproofing, building envelope, and HVAC. These are the systems appraisers are adjusting for under Q1 2026 CMHC guidelines.

- Identify any special levy forecasts in the next three to five years. Buyers and their lenders will find them — price with them in mind.

- Confirm with your strata council whether an updated depreciation report is scheduled before or shortly after your planned listing date. Timing matters.

- Ask your listing agent whether recent comparable sales in your building were completed before or after Q1 2026 CMHC changes — pre-change comps may overstate current achievable value.

- Discuss with your agent whether proactive disclosure of the depreciation report in the listing package reduces buyer hesitation or increases it for your specific building and price point.

What We Commonly See

In our experience working with strata sellers in Willoughby, Walnut Grove, and Langley, the most common mistake is pricing based on comparables without adjusting for the building's specific depreciation report status. A seller sees a unit in the same complex sell for $720,000 six months ago and expects the same. What they do not know is that the prior sale closed before the updated reserve fund study was released — and that the new study changed the financing landscape for their unit.

What often happens is that the price reduction comes in pieces rather than all at once. The buyer accepts the list price, receives the strata package, identifies the reserve fund gap, and requests a $25,000 reduction before removing subjects. The seller, already emotionally committed to the deal, accepts. The concession was foreseeable — but only if the depreciation report had been reviewed at the pricing stage.

A common mistake among sellers in older Fleetwood and Guildford strata buildings is assuming that because no special levy has been formally voted on, there is no disclosure obligation. The depreciation report's forecast of a probable levy — even without a strata council vote — is visible in the document and will be reviewed by lenders and sophisticated buyers. Sellers who have not read their own depreciation report before listing are consistently caught off-guard by the buyer's subject removal negotiation.

Questions and Answers

Q: Does every strata building in BC need a depreciation report?

Under BC's Strata Property Act and BCFSA regulations, most strata corporations with five or more lots are required to obtain depreciation reports and renew them every five years. Strata corporations can vote to waive the requirement annually, but lenders treat a waived or missing report as a risk signal equivalent to a flagged one — particularly after the 2024 BCFSA regulatory updates tightening waiver disclosure.

Q: What exactly does CMHC look for when reviewing a depreciation report?

Under CMHC's Q1 2026 mortgage insurance appraisal guidelines, reviewers flag reserve fund funding below 70% of the recommended balance, special levy forecasts exceeding $5,000 annually per unit, and deferred maintenance on critical systems including roofing, waterproofing, building envelope, elevators, and HVAC. Any of these individually can trigger a request for an independent reserve fund audit before financing approval is granted.

Q: Can a seller do anything to improve a flagged depreciation report before listing?

The strata corporation owns the depreciation report, not the individual unit owner. A seller cannot change the report. What a seller can do is work with their listing agent to price the property in a way that reflects the known risk, time the listing relative to report update cycles, and prepare for subject removal negotiations rather than being caught off-guard by them.

Q: How does a 5–12% appraisal reduction actually affect the sale process?

If a buyer's lender appraises the property below the purchase price, the lender will only finance based on the appraised value. The buyer must cover the gap in cash, renegotiate the purchase price down to the appraised value, or exit the contract. In Fraser Valley's current strata market, most buyers renegotiate. Sellers who priced without accounting for the depreciation report risk often end up accepting the lower price anyway — but after a longer, more stressful process.

Q: Are Fraser Valley townhomes and condos equally affected?

Townhomes and condos face the same depreciation report disclosure requirements, but townhomes in communities like Willoughby and Walnut Grove are disproportionately affected in 2026 because a large share of that inventory was built between 2000 and 2010 and is now entering its first major capital repair cycle. According to FVREB April 2026 data, townhome sales-to-active ratios in those communities are running at 15–23%, compared to 6–8% for condos — meaning townhome inventory is moving faster, but both segments face lender scrutiny on older buildings.

In Summary

Depreciation report red flags in the Fraser Valley are no longer a background concern for strata sellers — they are a direct pricing and deal-structure variable. Reserve fund depletion below 70%, special levy forecasts, and deferred maintenance on critical systems are triggering financing delays, appraisal shortfalls of 5–12%, and buyer renegotiations of 3–8% that sellers in Willoughby, Walnut Grove, Langley, Fleetwood, and Guildford are absorbing in real dollar terms. The sellers who navigate this best are the ones who review their depreciation report before setting a list price, understand which specific findings create lender friction, and price with the buyer's financing reality in mind rather than being renegotiated into it after accepting an offer.

Thinking About Selling a Condo or Townhome?

If you are preparing to sell a strata property in the Fraser Valley and want an honest review of how your building's depreciation report may affect your pricing strategy and subject removal process, Mansour Real Estate Group offers a no-pressure consultation that includes a depreciation report review before your listing goes live. Reach out when you are ready to have that conversation.

Related Articles

- Fraser Valley Condo and Townhome Market Conditions 2026

- Selling a Townhome in Willoughby, Langley: What Sellers Need to Know in 2026

- How Special Levies Affect Strata Home Sales in BC

Official Resources

- BC Financial Services Authority — Strata Property Act Regulations and Form B Requirements

- CMHC — Mortgage Insurance Appraisal Guidelines (Q1 2026)

- Fraser Valley Real Estate Board — Market Statistics and Sales Ratio Data

- BC Government — Strata Housing Information and Depreciation Report Requirements

About Mansour Real Estate Group

Buying or selling a condo or townhome in the Fraser Valley involves considerations that go well beyond comparable sales — strata documentation, depreciation report findings, reserve fund health, special levy risk, and the financing constraints those factors create for buyers all have a direct effect on what a seller can realistically achieve. Mansour Real Estate Group has helped condo and townhome sellers across Fraser Valley and Lower Mainland strata communities navigate these layers for more than 22 years, from pricing strategy that accounts for depreciation report risk to subject removal negotiations where the numbers are already anticipated.

Led by Mohamed Mansour, MBA and Associate Broker, the Real Estate Group has completed more than $780 million in residential real estate transactions and is consistently ranked among the Top 1% of Realtors in the region. The team is trusted for strata sales, estate sales, divorce-related property sales, downsizing, and any situation where accurate valuation and honest market context are what the client needs most. Most new clients come through repeat and referral business — a reflection of how the team approaches every transaction.

Whether someone is looking for Realtors who understand strata documentation and depreciation report risk, a real estate agent who can navigate a complex condo sale, real estate agents with direct Fraser Valley strata transaction experience, a Langley Realtor, a Surrey real estate agent, a White Rock Realtor, a real estate team for a townhome sale in Willoughby or Walnut Grove, or a Fraser Valley real estate broker who will give them a straight answer before they list — Mansour Real Estate Group is known for pricing discipline, transparent advice, and a process that protects seller equity at every stage.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients arrive through referrals from families and past clients who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate- The real estate journey, whether buying or selling, requires careful planning, professional guidance, and attention to detail. By following the steps outlined in this guide and working with trusted professionals, you can navigate the market with confidence and achieve your property goals. Remember that every transaction is unique, so adapt these recommendations to your specific circumstances and local market conditions. Don't hesitate to ask questions, do your research, and take your time making one of life's most significant decisions. Your future self will thank you for the diligence you put in today.Key Takeaways

Final Thoughts