How Rising Mortgage Rates After BoC Rate Cuts End Affect Fraser Valley Seller Strategy in 2026: Timing Windows, Price Anchoring, and the Math Behind When Higher Rates Compress Buyer Purchasing Power

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2025

For most of 2024 and into early 2026, the Bank of Canada's rate cut cycle gave Fraser Valley sellers a quiet advantage: buyer confidence stabilized, qualification ceilings held, and pricing power modestly recovered in segments that had contracted. That window is narrowing. When the cut cycle ends and mortgage rates begin rising again — even modestly — the math shifts fast, and sellers who plan around yesterday's qualification ceilings will find their pricing assumptions increasingly disconnected from what buyers can actually borrow.

This article explains exactly what happens to buyer purchasing power when rates rise after a cut cycle, which Fraser Valley market segments feel it first, and what sellers in Surrey, Langley, Abbotsford, and surrounding communities should be doing now to avoid pricing into a market that is already repricing beneath them.

Short Answer

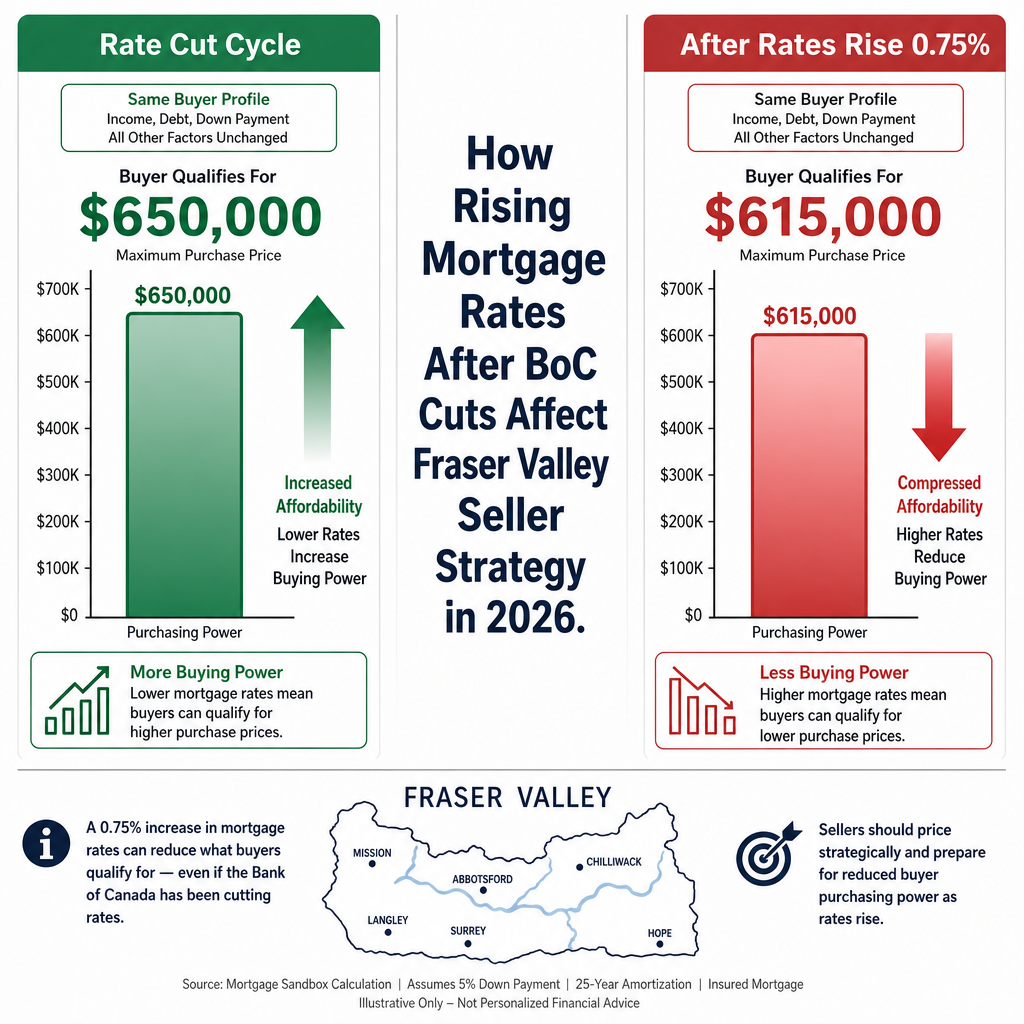

When mortgage rates rise after a Bank of Canada cut cycle ends, each 0.25% increase removes approximately $10,000–$15,000 in purchasing power per $500,000 mortgage. For Fraser Valley sellers in the $600,000–$750,000 segment, a 0.75%–1.0% rate increase compresses the buyer pool enough to push effective demand below current list prices, forcing price reductions that signal distress and extend days on market.

Key Takeaways

- Each 0.25% mortgage rate increase reduces buyer qualification by roughly 2%–2.5% on the same monthly payment.

- A buyer pre-approved at $650,000 today may qualify for only $615,000–$620,000 after a 0.5%–1.0% rate increase.

- The $600,000–$750,000 segment dominates Fraser Valley transaction volume and is most exposed to qualification ceiling compression.

- Sellers pricing based on current rate assumptions risk overpricing by 3%–8% within 60–90 days if rates rise 0.75%–1.0%.

- Executors and divorcing sellers face the highest timing risk: delayed listings in a rising-rate environment can cost 5%–12% of proceeds.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, or White Rock considering a listing in H2 2025 or H1 2026

- Executors managing estate properties that have not yet been listed

- Divorcing couples whose settlement timeline extends into late 2025 or 2026

- Downsizers waiting for "the right moment" who may be timing into a contracting window

- Sellers in the $575,000–$800,000 price band, where buyer qualification compression hits hardest

When This Advice May Not Apply

Sellers in the detached luxury segment above $1.5 million are less sensitive to qualification ceiling shifts because buyers at that price point are often less reliant on high loan-to-value financing. If the Bank of Canada holds rates flat or resumes cuts, the urgency described here decreases. This article does not constitute financial or mortgage advice — speak with a licensed mortgage professional for your specific qualification scenario.

Data Used in This Article

- Bank of Canada Monetary Policy Reports — Official rate announcements and forward guidance (BoC.ca, 2024–2025)

- CMHC Housing Research and Forecasts 2026 — Mortgage qualification sensitivity analysis (Official publication)

- FVREB Market Statistics April 2026 — Sales-to-active listings ratio, benchmark pricing, transaction volume by segment (Official FVREB data release)

- Mortgage Qualification Calculator Analysis — Rate sensitivity modelling comparing current versus projected rate scenarios (internal analysis based on published qualification rules)

Why the End of a Rate Cut Cycle Creates a Different Risk Than the Cuts Themselves

Rate cuts get attention. Rate reversals after cuts get less — but they are where seller strategy mistakes cluster. During a cut cycle, buyer qualification ceilings rise gradually, supporting pricing. When the cycle ends and rates move upward again, qualification ceilings compress, but list prices rarely adjust at the same speed. That lag is where sellers lose money.

According to the Bank of Canada's published monetary policy framework, rate decisions are made in response to inflation and economic conditions — not to housing market outcomes. That means a rate increase can arrive even while Fraser Valley resale inventory remains elevated and buyer competition is thin. The Fraser Valley Real Estate Board's April 2026 data showed the sales-to-active listings ratio at approximately 11%, a level that already places the market in balanced-to-soft conditions. A rate increase in that environment does not just reduce demand — it reduces it against a backdrop where supply is already comfortable, giving buyers more negotiating room, not less.

The practical consequence: sellers who list six to eight weeks after rates rise will be entering a market where comparable sales from the prior 90 days — the comps that anchored their pricing — were completed by buyers who qualified under more favourable rate conditions. That anchoring mismatch directly depresses net proceeds.

The Math: What a 0.25%–1.0% Rate Increase Actually Does to a Fraser Valley Buyer

Mortgage qualification in Canada uses a stress test rate set at the higher of the contract rate plus 2%, or the regulatory floor. When mortgage rates rise, both the contract rate and the stress test rise. The effect on qualification is compounding, not linear.

Based on current qualification rules and CMHC housing research, each 0.25% increase in mortgage rates reduces the maximum purchase price a buyer can qualify for by approximately 2%–2.5% on the same household income and down payment. In dollar terms, for a $500,000 mortgage, that translates to roughly $10,000–$15,000 in lost purchasing power per 0.25% increase.

Applied to the Fraser Valley's $600,000–$750,000 segment:

- A buyer pre-approved at $650,000 today may qualify for approximately $635,000 after a 0.25% increase

- After a 0.5% increase: approximately $620,000–$625,000

- After a 0.75%–1.0% increase: approximately $610,000–$618,000

For a seller listed at $649,000, a 0.75% rate increase means the largest buyer pool — those who could previously qualify at or just above that price — can no longer reach the ask. The seller either reduces the price or waits longer. In a market already sitting at an 11% sales-to-active ratio, waiting longer is rarely neutral.

How We Evaluate This at Mansour Real Estate Group

When we work with sellers in the Fraser Valley on pricing strategy, we do not price to today's conditions alone. We price to the conditions that will exist when the property is actively receiving offers — typically 30–60 days after the listing decision is made. If rate movement is expected within that window, we model the qualification ceiling shift and build it into our pricing recommendation.

For sellers in the $575,000–$800,000 range, this analysis is not optional. It is the difference between a price that attracts offers in the first two weeks and one that needs three reductions before finding a buyer. Three reductions in a soft market signal distress to buyers and almost always result in a lower net sale price than a correct initial price would have achieved.

Which Fraser Valley Segments Are Most Exposed

Not all segments respond to rate increases at the same speed or with the same severity. Entry-level and mid-market segments — townhomes, stacked townhomes, and smaller detached homes priced between $575,000 and $850,000 — are most sensitive because buyers at these price points typically carry high loan-to-value mortgages and are close to their qualification ceiling already.

Areas including Cloverdale, Fleetwood, Willoughby, Walnut Grove, and parts of Abbotsford carry concentrated inventory in this price band. Sellers in these communities will feel qualification compression first and most directly. South Surrey and White Rock have more exposure in the $900,000–$1.3 million detached segment, where buyers typically carry larger mortgages in absolute dollar terms but may have more equity flexibility. Langley's townhome market, which accounts for a significant share of FVREB transaction volume, sits squarely in the highest-exposure zone.

Estate Sellers and Divorcing Sellers: The Highest Timing Risk Profile

For sellers with fixed timelines — executors managing estate properties, or parties in a divorce-related sale waiting on court or legal timelines — the rising-rate scenario creates compounding risk. These sellers often cannot control when the property lists. If a probate grant, consent order, or legal agreement delays a listing by 90–120 days, and rates rise in that window, the market the seller enters is materially different from the market they planned for.

According to CMHC's 2026 housing research, buyer purchasing power contraction in a rising-rate environment disproportionately affects the resale market for mid-priced properties — exactly where most estate and divorce-related properties in the Fraser Valley are concentrated. Executors should factor rate scenarios into their timeline planning, and divorcing sellers should understand that delayed listings are not neutral decisions when rates are in motion.

Seller Checklist: Preparing for a Rate-Sensitive Listing in 2026

- Confirm current mortgage qualification ceiling for your target buyer profile with a licensed mortgage professional — not an estimate from six months ago

- Request a comparative market analysis that models pricing under current rates AND under a 0.5%–0.75% rate increase scenario

- Identify your optimal listing window: a property listed and sold before a rate increase completes transactions at pre-increase buyer qualification levels

- For estate and divorce situations, consult your lawyer about any timeline flexibility that could move the listing earlier rather than later

- Avoid anchoring your price to a neighbour's sale from six or more months ago — if that sale occurred under different rate conditions, the comparable is degraded

- Assess condition and preparation costs now: a property that needs 30–45 days of preparation work before listing should account for rate movement during that period

- Confirm your list price leaves enough room to negotiate without falling below the next qualification threshold — thin margins compress fast in a rising-rate environment

What We Commonly See

Sellers pricing to the last comparable, not the next market. In our experience, the most common pricing mistake in a shifting rate environment is anchoring to recent sold data without adjusting for the rate conditions under which those sales closed. A comparable sale from four months ago reflects a buyer who qualified at a different ceiling. If rates have moved since that sale, the comparable is not a reliable floor.

Underestimating how quickly the buyer pool shrinks. What often happens is that sellers think a 0.5% rate increase will affect a small fraction of buyers. In practice, the $600,000–$750,000 segment in the Fraser Valley has buyers clustered near their qualification ceiling. A modest rate shift removes a disproportionate share of the active buyer pool for that price range.

Waiting for spring without accounting for where rates will be in spring. A common mistake is assuming the spring market will look like the spring market did last year. Rate conditions, inventory levels, and buyer confidence in spring 2026 will be shaped by what the Bank of Canada does between now and then. Sellers who plan their spring listing today should model the rate scenario, not assume continuity.

Frequently Asked Questions

Q: If I list before rates rise, does my sale definitely close at today's conditions?

Not necessarily. If your buyer has not yet locked a mortgage rate at subject removal, a rate increase between offer and completion could affect their final qualification. Most buyers lock rates at or before subject removal — confirm this with your Realtor and encourage buyers to secure rate holds early.

Q: How much does a 1% mortgage rate increase actually compress prices in the Fraser Valley?

Based on CMHC qualification modelling and current stress test rules, a 1.0% increase reduces purchasing power by approximately 8%–10% for buyers near their qualification ceiling. In the $600,000–$750,000 segment, that translates to $48,000–$75,000 in lost buying capacity — enough to push many buyers out of the price tier entirely.

Q: Does this affect condos and townhomes differently than detached homes?

Yes. Condo and townhome buyers in the Fraser Valley are more heavily concentrated near their qualification ceiling because entry prices are lower and down payments are proportionally smaller. Rate compression hits these segments faster and with less buffer than detached homes, where buyers often carry more equity. Sellers of Fraser Valley condos and townhomes should treat rising-rate scenarios as a near-term pricing risk, not a medium-term one.

In Summary

When the Bank of Canada's rate cut cycle ends and mortgage rates begin rising, the Fraser Valley resale market does not adjust gently or gradually — it reprices at the buyer qualification ceiling, and sellers who list after that repricing absorbs into comparable sales data are negotiating against a lower floor than they planned for. The math is straightforward: each 0.25% increase removes $10,000–$15,000 in purchasing power per $500,000 mortgage, and the $600,000–$750,000 segment that drives Fraser Valley transaction volume has the least buffer to absorb that compression. Sellers with flexibility should treat the current window as a pricing and timing advantage. Sellers without flexibility — executors, divorcing sellers, those mid-preparation — should build rate scenario modelling into every decision they make between now and listing day.

Talk to Someone Who Knows This Market

If you are thinking about timing a sale in Surrey, Langley, Abbotsford, White Rock, or anywhere in the Fraser Valley, and you want to understand what the current rate environment means for your specific property and price range, Mansour Real Estate Group offers honest, data-grounded seller strategy consultations. No pressure, no generic advice — just a clear read on what the market is doing and what that means for your decision.

Related Articles

- Why the Bank of Canada Held Its Key Interest Rate at 2.25% and What It Means for Home Buyers, Sellers and Owners

- Selling an Estate Property in the Fraser Valley: A Complete Guide for Executors and Families

- Selling a Condo in the Fraser Valley: What Sellers Need to Know About Strata Documents, Pricing and Timing in 2026

About Mansour Real Estate Group

When sellers in the Fraser Valley and Lower Mainland are deciding whether to list now or wait — and what rising mortgage rates mean for their pricing strategy — they need more than a market summary. They need local analysis tied to their specific property, price range, and timeline. Mansour Real Estate Group has been providing that kind of grounded, specific seller strategy guidance across the Fraser Valley and Lower Mainland for more than 22 years.

Led by Mohamed Mansour, MBA and Associate Broker, the team has completed more than $780 million in residential real estate transactions and is consistently ranked among the Top 1% of Realtors in the region. Trusted for seller strategy, market timing, pricing analysis, estate sales, divorce-related property sales, downsizing, and complex real estate decisions, Mansour Real Estate Group brings a structured, data-grounded approach to every transaction.

Whether someone is searching for Realtors who understand Fraser Valley market cycles, a real estate agent who can model pricing under shifting rate conditions, real estate agents trusted for strategic seller guidance, a Surrey real estate team, a Langley Realtor, a White Rock real estate broker, or a real estate group with deep experience across the Lower Mainland, Mansour Real Estate Group is known for honest market interpretation, accurate valuations, and advice that puts the client's outcome first.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- Bank of Canada — Monetary Policy

- CMHC — Housing Research and Forecasts

- Fraser Valley Real Estate Board — Market Statistics

- BC Financial Services Authority — Mortgage Information for Consumers

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.