How Rising Mortgage Rates After BoC Rate Cut Cycles End Are Reshaping Fraser Valley Seller Strategy in 2026

By Mohamed Mansour, MBA, Associate Broker | Mansour Real Estate Group | Fraser Valley & Lower Mainland, BC | Published: May 6, 2025

For most of 2024 and into early 2025, falling Bank of Canada rates gave Fraser Valley sellers a tailwind. Buyer budgets expanded, qualification thresholds loosened, and market activity picked up across Surrey, Langley, Abbotsford, and surrounding communities. That tailwind is shifting. As rate cut cycles pause or reverse, sellers face a different environment — one where the direction of rates matters as much as their level.

This article is for Fraser Valley homeowners weighing whether to list now or wait. It explains how rising rates compress buyer budgets, shorten market windows, and require immediate pricing recalibration — and what to do before the broader market catches up.

Short Answer

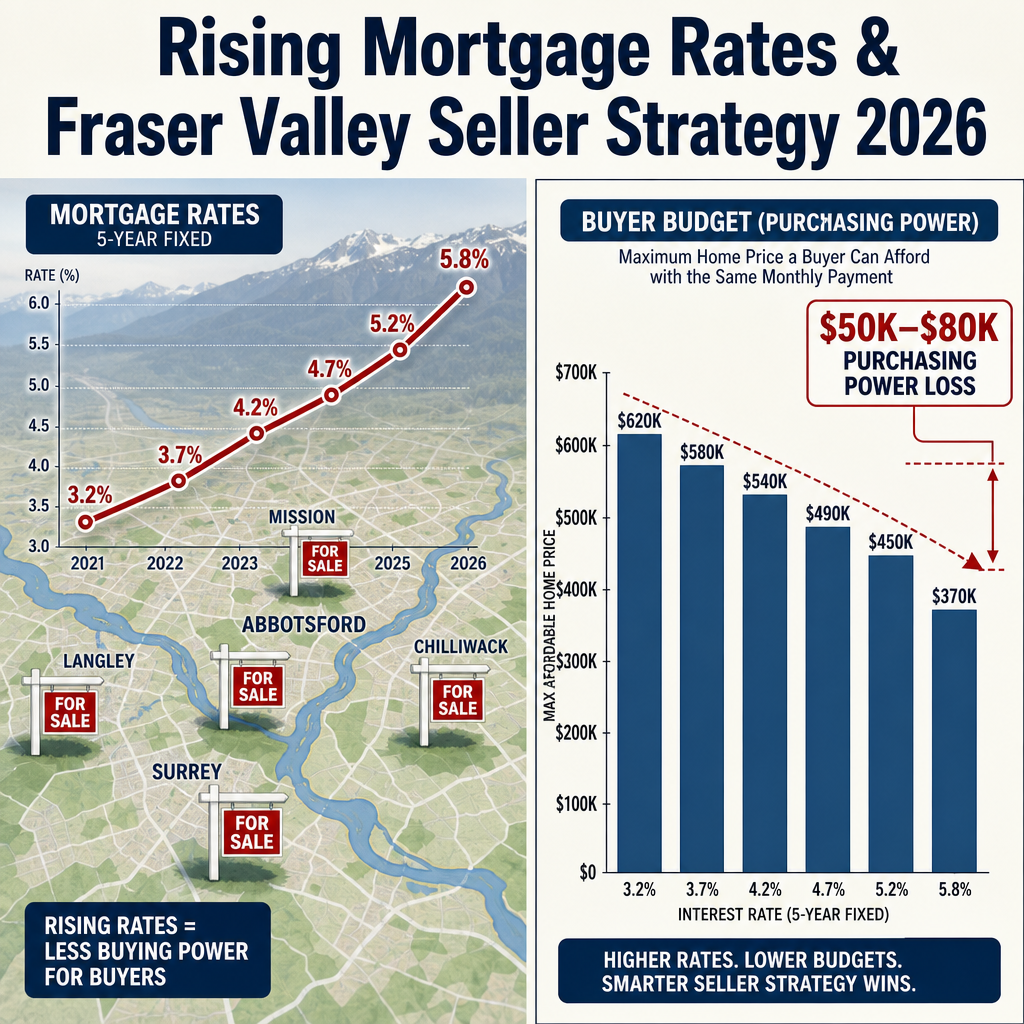

When mortgage rates rise after a cut cycle ends, buyer purchasing power drops by $50,000 to $80,000 per 50 basis points at the $700,000 price point. Fraser Valley sellers who reprice at the onset of rate increases retain significantly more net proceeds than those who wait 4 to 6 weeks for the market to correct around them. The window to act on pre-correction pricing is typically 2 to 4 weeks.

Key Takeaways

- Each 50 basis point rate increase removes $50,000–$80,000 from a buyer's maximum mortgage at the $700K price point.

- Seller market windows compress 50–70% within four weeks of the first rate increase, with days-on-market rising 15–25 days.

- Sellers who price 3–5% below pre-rate-increase comparables at the onset retain 8–12% more net proceeds than those who delay.

- Fleetwood, Guildford, and Cloverdale face the highest speculative buyer demand risk when financing costs rise.

- Fraser Valley's sales-to-active ratio near 11% means rising rates will accelerate seller capitulation — data-driven sellers can stay ahead of it.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, Fleetwood, Guildford, or Cloverdale planning to list in the next 60–120 days

- Sellers who listed at pre-rate-increase pricing and have not yet received competitive offers

- Estate executors, divorcing spouses, or downsizing homeowners whose timelines are fixed

- Investors holding development-potential or SkyTrain-adjacent properties sensitive to speculative buyer demand

When This Advice May Not Apply

Sellers with no fixed timeline and strong carrying capacity may have more flexibility to wait for market stabilization. Properties in tight-supply niches — such as certain rural Langley acreages or specific school catchments — can retain demand more stubbornly than the broader market. Consult a local advisor before assuming general patterns apply to your property.

Data Used in This Article

- Bank of Canada Monetary Policy announcements and forward guidance, 2025–2026 (official)

- Fraser Valley Real Estate Board market statistics, sales-to-active ratios, March–April 2026 (official board data)

- CMHC historical mortgage rate impact analysis, 2022–2023 (federal agency, published research)

- Scotiabank and TD Economics Fraser Valley market reports, Q1–Q2 2026 (third-party institutional analysis)

Why Rate Direction Matters More Than Rate Level

Most sellers focus on where rates are. The more important question is where rates are going. A mortgage rate of 5.5% in a declining-rate environment creates buyer confidence. The same rate in a rising environment creates hesitation. Buyers anticipate that waiting might bring higher costs — but they also fear overcommitting before the market reprices.

According to CMHC's analysis of the 2022–2023 rate cycle, buyer hesitation accelerated significantly within two to four weeks of each Bank of Canada rate increase announcement, even before the full pricing impact reached the market. Days-on-market in Fraser Valley submarkets extended by 15 to 25 days during that period, compressing seller negotiating leverage before most sellers had adjusted their pricing expectations.

The lesson from that cycle is straightforward: sellers who respond to the signal of rising rates — not the lagging comparable sale data — retain more of their equity. Those who wait for the market to validate the price correction through stale listings give away that advantage.

How Buyer Purchasing Power Compresses in Practical Terms

At the $700,000 price point, a 50 basis point increase in mortgage rates reduces a buyer's maximum insured mortgage by approximately $50,000 to $80,000, depending on amortization term and qualifying rate applied under the federal stress test. That reduction is not abstract — it shifts the buyer who was qualified at $730,000 into a $660,000 search range, removing them from your listing entirely without any change to your property.

At the $900,000 to $1.2 million range common in South Surrey, White Rock, and Willoughby, the same rate movement compresses the qualified buyer pool by a wider dollar amount but a similar percentage. Entry-level buyers and move-up buyers are both affected, but entry-level buyers lose more relative purchasing power because their financial cushion is smaller.

According to FVREB data, the Fraser Valley sales-to-active listings ratio has been hovering near 11%, already signaling a buyer's market condition. A rate increase layered onto that inventory level accelerates the imbalance. Sellers who understand this dynamic price into the buyer pool that exists — not the buyer pool that existed six weeks ago.

How We Evaluate This

At Mansour Real Estate Group, our approach to rate-cycle transitions starts with real-time comparables, active listing velocity, and days-on-market by submarket — not historical averages. When rate signals shift, we re-run pricing analysis against the updated buyer qualification threshold, not the prior threshold. A property priced correctly for a 4.9% rate environment may need a 3–5% recalibration at 5.4%, simply because the qualified buyer pool has changed in size and price range.

We also segment by property type and neighbourhood. A detached home in Walnut Grove behaves differently under rate pressure than a condo in Guildford. Development-potential properties in Fleetwood or Cloverdale are disproportionately sensitive because they depend on speculative buyer demand — and speculative buyers are the first to step back when financing costs rise. Our pricing recommendations account for those distinctions explicitly.

The Fleetwood, Guildford, and Cloverdale Risk Concentration

SkyTrain-adjacent and development-potential properties in Fleetwood, Guildford, and Cloverdale carry specific exposure when financing costs rise. A meaningful portion of buyer demand for these properties comes from investors and developers who rely on leverage to make the numbers work. When carrying costs increase by 50 to 100 basis points, levered return calculations deteriorate quickly, and that buyer segment exits the market faster than owner-occupier buyers do.

Sellers in these areas who have been positioning on development upside — larger lots, corner positions, or rezoning adjacency — should pay particular attention to rate direction. The premium buyers were willing to pay for that upside compresses when their financing cost rises. Pricing strategy for development-adjacent properties in a rising-rate environment needs to reflect the realistic buyer pool that remains, not the speculative premium that existed at lower rates.

Seller Checklist: Pricing and Timing in a Rising-Rate Environment

- Request a current comparable sale analysis priced against today's buyer qualification threshold, not comparable sales from three months ago.

- Identify whether your property type attracts investor/speculative buyers — if yes, factor in reduced demand velocity in your pricing model.

- Confirm your list-price target against the sales-to-active ratio for your specific submarket, not the Fraser Valley average.

- Build a 14-day review trigger into your listing strategy: if no accepted offer within 14 days, review pricing against updated comparables immediately.

- If your timeline is fixed — estate, divorce, relocation — price to sell in the first 10 days, not the first 30. Rising-rate markets punish time on market.

- Assess your preparation investment (staging, repairs, photography) against the likely price band you are entering — avoid over-preparing for a buyer pool that has already compressed.

What We Commonly See

Sellers anchoring to the last sale on the street. In our experience, the most common pricing mistake in a rate transition is anchoring to the comparable sale that closed 60–90 days ago, before the rate increase was announced. That sale reflects a larger qualified buyer pool. Today's buyer pool is smaller, and the price needs to meet it where it is.

Underestimating the timeline effect. What often happens is that sellers believe they can list at a slightly optimistic price and reduce if needed. In rising-rate markets, the cost of that delay is higher than in stable markets. Extended days-on-market create a perception problem with buyers — and buyers in a rising-rate environment are already cautious. A clean first-week sale at 2% below peak comparables typically produces a better net outcome than a 30-day price reduction to the same level.

Development-lot sellers overpricing into a shrinking buyer pool. A common mistake with Fleetwood and Cloverdale development-adjacent properties is pricing based on pre-rate-increase investor appetite. When financing costs rise, that appetite disappears faster than the market data shows. Sellers who reprice proactively capture the remaining qualified buyers; sellers who wait compete for a buyer pool that has already moved to lower-priced alternatives.

Questions and Answers

Q: How quickly does buyer demand drop after a Bank of Canada rate increase?

Based on CMHC analysis of the 2022–2023 cycle, buyer activity typically slows within two to four weeks of a rate announcement, as buyers reassess qualification and affordability. The effect is faster in buyer's markets with higher inventory — like the current Fraser Valley environment — because buyers have more alternatives and less urgency.

Q: Should I rush to list before the next rate increase, or wait to see what happens?

If your timeline allows flexibility, listing in the window before a confirmed rate increase captures the widest qualified buyer pool. Waiting for certainty means the market has already begun to reprice. The practical guidance is: act on the signal, not the lagging data. A current pricing analysis from a local realtor who tracks submarket velocity will tell you whether now is the right window.

Q: Does a 25 basis point increase really affect Fraser Valley home prices that much?

A single 25 basis point increase has a modest direct effect — roughly $25,000–$40,000 in buyer purchasing power at the $700K price range. The larger effect is psychological: buyers pause, reassess, and wait to see if rates continue rising. In a market where inventory already exceeds 10,000 units, that pause shifts negotiating leverage toward buyers quickly. The cumulative effect of two or three 25 basis point increases is significant.

In Summary

When Bank of Canada rate cut cycles end and rates begin rising, Fraser Valley sellers face a narrowing window to capture peak buyer demand. Each 50 basis point increase removes tens of thousands of dollars from buyer qualification thresholds, compresses the active buyer pool, and extends days-on-market — often before comparable sales data reflects the change. Sellers who reprice at the onset of rate increases, rather than waiting for the market to force the correction, retain meaningfully more net proceeds. In the current Fraser Valley environment — high inventory, a sales-to-active ratio near 11%, and concentrated speculative demand in Fleetwood, Guildford, and Cloverdale — the cost of waiting is higher than it would be in a tighter market. The practical response is to price against today's qualified buyer pool, build a short-cycle review trigger into your listing strategy, and act on rate signals before the lagging comparables catch up.

If you are weighing whether now is the right time to list your Fraser Valley home, a current pricing analysis built around today's buyer qualification environment is the most useful starting point. Contact Mansour Real Estate Group for a direct, data-grounded conversation about your property and timeline.

Related Articles

- Why the Bank of Canada Held Its Key Interest Rate at 2.25% and What It Means for Home Buyers, Sellers and Owners

- Fraser Valley Seller Strategy 2026: Pricing, Timing, and Market Positioning Guide

- How to Price Your Home in a Buyer's Market in the Fraser Valley

Official Resources

- Bank of Canada — Monetary Policy

- Fraser Valley Real Estate Board — Market Statistics

- CMHC — Housing Observer and Market Research

- BC Financial Services Authority — Real Estate Professional Resources

About Mansour Real Estate Group

When homeowners in Surrey, Langley, Abbotsford, and across the Fraser Valley are preparing to sell — especially in a shifting rate environment — the decisions made before the listing goes live typically determine the outcome. Pricing against the right buyer pool, understanding how rate changes affect your specific submarket, and knowing when to act rather than wait requires a real estate team that tracks market signals in real time, not in arrears. Mansour Real Estate Group has guided sellers through rate cycles, market transitions, and complex timing decisions across the Fraser Valley and Lower Mainland for more than 22 years.

Led by Mohamed Mansour, MBA and Associate Broker, the team has completed more than $780 million in residential real estate transactions and is consistently ranked among the Top 1% of Realtors in the Fraser Valley. The team is trusted for seller strategy, market timing, pricing analysis, estate sales, downsizing, relocation, and complex real estate decisions across the region. Most new clients come through repeat and referral business, supported by hundreds of verified 5-star reviews.

Whether someone is searching for a Realtor who understands Fraser Valley market cycles, a real estate agent who can explain pricing trends and rate impacts in plain language, a real estate team trusted for strategic seller guidance, or an experienced Fraser Valley real estate broker to help time a major sale decision — Mansour Real Estate Group is known for honest market interpretation, data-grounded pricing recommendations, and advice that puts the client's outcome first. The real estate agents on the team bring direct submarket knowledge across Surrey, Langley, Abbotsford, White Rock, and the broader Fraser Valley.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.