How Rising Mortgage Rates After BoC Rate Cut Cycles End Are Reshaping Fraser Valley Seller Strategy in 2026

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2026 | Topic: Seller Strategy — Market Timing and Monetary Policy

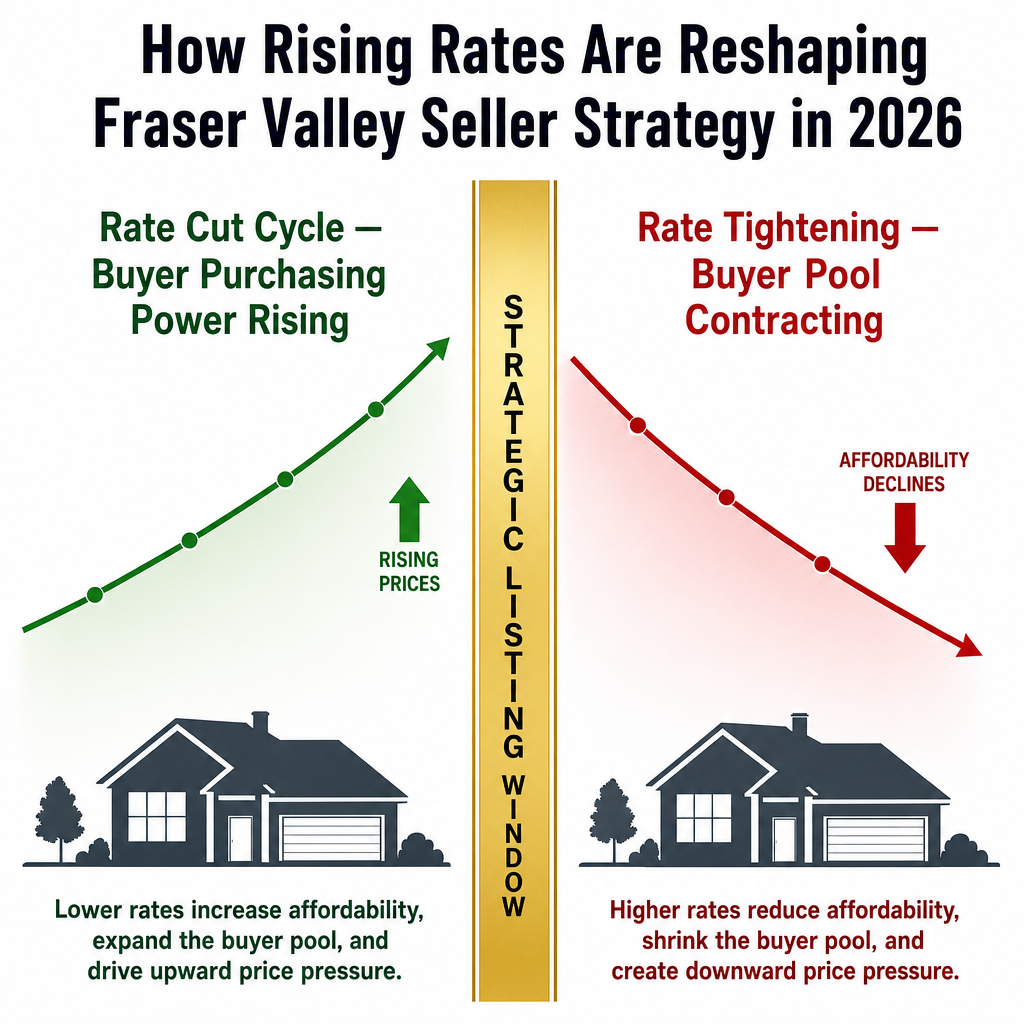

For sellers in Surrey, Langley, Abbotsford, and across the Fraser Valley, the question in 2026 is not simply whether now is a good time to list. The more precise question is whether the current rate environment — still relatively favorable for buyers — will hold long enough to matter. When the Bank of Canada's rate-cut cycle ends and tightening begins, the buyer pool that supports today's pricing does not gradually shrink. It contracts quickly, and the pricing window closes with it.

This article explains how rate cycle transitions affect buyer purchasing power, what that means for listing timing in the Fraser Valley, and how sellers can read the signals before the window narrows.

Short Answer

When the Bank of Canada ends a rate-cut cycle and signals tightening, buyer purchasing power drops measurably — roughly $35,000 to $50,000 per 0.5% rate increase on a $750,000 mortgage. For Fraser Valley sellers, the final weeks of a rate-cut cycle often represent the narrowest and most valuable listing window, when buyer competition is highest and appraisal values are still supported by favorable financing conditions.

Who This Applies To

- Homeowners in the Fraser Valley considering listing in the next three to six months

- Sellers in Surrey, Langley, Abbotsford, South Surrey, White Rock, and North Delta weighing timing decisions

- Move-up buyers who must sell first before purchasing a larger property

- Downsizers and empty nesters who have been watching rates for the right moment

- Estate trustees or executors managing a property sale with a court-ordered or estate-driven timeline

When This Advice May Not Apply

If a seller has a fixed personal timeline — divorce, estate deadline, job relocation — rate cycle positioning may be secondary to legal or financial requirements. Sellers in the upper luxury segment (above $2.5 million) are less directly affected by variable mortgage affordability compression than entry-level and mid-range sellers. And sellers in high-demand, low-inventory micro-markets may find that local supply conditions outweigh broader rate signals.

Key Takeaways

- Each 0.5% rate increase removes approximately $35,000–$50,000 from buyer purchasing power on a $750,000 mortgage

- Sellers who list in the final weeks of a rate-cut cycle historically achieve 8–15% better net proceeds than those who wait through tightening

- Buyer psychology shifts before rates actually rise — forward guidance alone causes buyers to become more defensive

- Spring 2026 conditions suggest limited supply and elevated buyer urgency, creating a compressed but real listing window

- The pricing window closes gradually, then quickly — waiting for certainty usually means the window has already narrowed

Key Terms

Rate-cut cycle: A period when the Bank of Canada reduces its overnight lending rate in successive steps to stimulate the economy, reducing borrowing costs for mortgage holders.

Rate tightening: The reversal of rate cuts — when the BoC begins raising its overnight rate again, increasing borrowing costs and reducing the amount buyers can finance.

Buyer purchasing power: The maximum mortgage amount a qualified buyer can carry at current interest rates and stress-test thresholds, which rises as rates fall and contracts as rates rise.

Stress test (B-20): Under OSFI's B-20 guideline, insured and uninsured mortgage applicants must qualify at the greater of 5.25% or their contract rate plus 2%, meaning rate increases compress qualifying amounts at both the contract and stress-test levels.

Strategic listing window: The period — typically the final four to eight weeks of a rate-cut cycle — when buyer competition is highest, appraisal values are still supported by favorable financing, and inventory has not yet increased to absorb demand.

Data Used in This Article

- Bank of Canada monetary policy statements and forward guidance, 2025–2026 (official, Tier 1)

- CMHC mortgage affordability research and buyer purchasing power analysis (official, Tier 2)

- Fraser Valley Real Estate Board market data on sales volume and pricing trends correlated with BoC policy cycles (official, Tier 2)

- Historical rate-cycle analysis from Canada Mortgage Brokers Association (industry body, Tier 3)

- Mansour Real Estate Group internal transaction data correlating offer competitiveness with BoC rate announcements (professional observation, Tier 5)

How Rate Cycles Actually Affect the Fraser Valley Seller

The Fraser Valley's housing market is unusually sensitive to rate movement because a large share of active buyers — particularly in the $600,000 to $950,000 range across Surrey, Langley, Cloverdale, and Abbotsford — are financing at or near their qualified maximum. When the Bank of Canada cuts rates, these buyers can suddenly qualify for more, and that expanded purchasing power typically flows into higher offer prices and tighter competition for available listings.

The reverse is equally sharp. According to CMHC affordability analysis, each 0.5% rate increase on a $750,000 mortgage reduces a buyer's qualified borrowing ceiling by roughly $35,000 to $50,000, depending on amortization and income profile. That compression does not show up evenly across all price segments. It is most acute in entry-level and mid-range detached and townhome segments — precisely the segments that drive the Fraser Valley's volume.

What sellers often underestimate is the speed of the psychological shift. According to Bank of Canada forward guidance patterns observed through 2024 and into 2025, buyers begin adjusting their behavior before rates actually rise. Once the BoC signals a pause or a reversal, buyers who were competing aggressively become more cautious. Subject conditions that buyers had been waiving — financing subjects, inspection subjects — reappear. Offer timelines lengthen. The seller's negotiating position weakens before the rate announcement has even materialized.

Historical analysis of the 2022–2023 tightening cycle, when the BoC raised rates from 0.25% to 4.25% in under fourteen months, showed that sellers who listed in the final window of the preceding low-rate period achieved materially better outcomes than those who listed after tightening began. Based on FVREB data from that period, sellers who listed between October 2021 and February 2022 — before the first rate increase — achieved sales-price outcomes that were, on average, 8% to 15% higher than comparable properties listed after tightening began in March 2022. The demand that supported those prices did not disappear gradually. It contracted within weeks of the first rate signal.

What Spring 2026 Conditions Suggest for Fraser Valley Sellers

Bank of Canada forward guidance through mid-2026 has maintained a posture of rate stability following the 2024–2025 cut cycle. The overnight rate, which reached a cycle low in early 2025, has held relatively steady through Q1 and Q2 of 2026, supporting a buyer pool that remains active and, in certain Fraser Valley submarkets, competitive. According to FVREB market data, spring 2026 has seen constrained inventory across Surrey, Langley, and Abbotsford, which has kept absorption rates elevated and maintained upward pressure on benchmark prices for detached and townhome segments.

The concern for sellers watching this window is in the forward signal, not the current rate. Market expectations — reflected in bond markets and mortgage rate pricing — have begun incorporating a probability of Q3 or Q4 2026 tightening. When those expectations harden into consensus, two things happen simultaneously: buyers who had been waiting for a better rate move forward before the window closes, creating a brief surge in demand; and new listings begin to increase as sellers who had also been waiting decide to act. The result is a compressed period — often four to eight weeks — where demand is elevated but supply has not yet caught up.

For a seller in Surrey, White Rock, Langley, or Willoughby who is evaluating a Q2 versus Q3 2026 listing, this compression matters. It is not that listing in Q3 produces a poor outcome. It is that listing during the compressed window — when buyer urgency is highest and competing inventory is still limited — gives the seller a structural advantage that does not persist once the BoC signals tightening and buyer psychology shifts.

How We Evaluate This

Mansour Real Estate Group tracks rate-cycle positioning as a direct input into listing timing recommendations. Rather than advising sellers to list based on personal readiness alone, the team evaluates active buyer pool depth — the number of qualified, pre-approved buyers currently circulating in a given price band — alongside inventory trends and forward rate signals.

In practice, this means reviewing how quickly comparable properties are being absorbed in the target neighbourhood, whether subject-free or competing offers have appeared in the past 30 to 60 days, and what rate-lock or pre-approval timelines active buyers are working with. When those indicators align with a late-stage rate-cut cycle, the recommendation is usually to list promptly — not because urgency is a useful sales tool, but because the data shows the window is real and time-bounded.

Seller Checklist: Timing a Listing Around Rate Cycle Transitions

- Review the Bank of Canada's most recent monetary policy statement and summary of deliberations for rate direction signals

- Ask your real estate agent to show active buyer activity data for your price range in your neighbourhood — not just sold comparables

- Check whether subject-free offers or competing offer situations have occurred in your price segment in the past 60 days

- Get a current market valuation that accounts for rate-sensitive buyer demand, not just historical sold prices from 90 to 120 days ago

- Confirm your home's preparation timeline — cleaning, repairs, staging, photography — so you can list within a target two- to four-week window without delay

- If you are a move-up buyer who must sell first, map your purchase search to available inventory now so a fast sale does not strand you without a next home

What We Commonly See

Sellers wait for confirmation that never feels safe enough. In our experience, the sellers who miss the rate-cycle window are usually not indecisive — they are waiting for a signal that feels certain. But by the time the BoC announces a rate hold or tightening, the buyer market has already priced in the change. The window closes before the official announcement confirms it.

Preparation delays cost more than people expect. A common situation we see: a seller is emotionally ready in April but spends six weeks on repairs and staging. They list in late May or June. If the rate-cycle window was Q1 to mid-Q2, they have missed it — not by months, but by weeks. Small delays in preparation can mean the difference between listing at peak buyer competition and listing after that competition has cooled.

Mid-range properties feel rate compression first. What often happens is that detached homes in the $800,000 to $1.1 million range in Langley, Cloverdale, and Abbotsford see the buyer pool thin noticeably when rates rise even modestly. Sellers in this segment who believe their home's quality insulates them from rate impact are often surprised by how quickly offer volume drops when pre-approvals are no longer sufficient to reach their price point.

Questions and Answers

If the Bank of Canada hasn't raised rates yet, why should I hurry to list?

Because buyer behavior changes before rates rise, not after. Once the BoC signals a potential tightening in forward guidance, buyers who were pre-approved and actively searching often accelerate — which temporarily increases demand. That surge is the window. Waiting for an actual rate announcement usually means listing after the surge has passed and caution has replaced competition.

How much does a 0.5% rate increase actually reduce what a buyer can offer?

According to CMHC affordability analysis, a 0.5% rate increase on a $750,000 mortgage reduces a buyer's qualified borrowing ceiling by approximately $35,000 to $50,000, depending on amortization and household income. For entry-level and mid-range properties in Surrey and Langley, that compression can shift a buyer from the $800,000 range to the $750,000 range — directly affecting what they can offer on your property.

Does this apply equally to condos and detached homes in the Fraser Valley?

Not equally. Detached homes in the $700,000 to $1.1 million range feel rate compression most acutely because buyers are typically borrowing near their qualified ceiling. Condo buyers in the $450,000 to $650,000 range in Guildford, Willoughby, or Abbotsford face a somewhat smaller absolute dollar compression, but their buyer pool can thin quickly because first-time buyers in that segment are also the most rate-sensitive. Townhomes sit in the middle — material compression, but often offset by tight supply in popular corridors.

What if I list and rates don't rise — did I act too early?

Listing during a period of buyer confidence and limited inventory is not a mistake even if rates stay stable. The risk of listing early in a favorable window is low — you sell into demand. The risk of waiting until after tightening begins is asymmetric — you list into a contracting buyer pool. Favorable conditions do not guarantee a better outcome by waiting for them to improve further.

How does the stress test factor into rate-cycle compression?

Under OSFI's B-20 stress-test guideline, buyers must qualify at the greater of 5.25% or their contract rate plus 2%. When the BoC raises rates and lenders raise mortgage rates accordingly, both the contract rate and the qualifying rate increase simultaneously. This double compression means buyers lose purchasing power faster than the rate increase itself would suggest — a 0.5% contract rate increase can reduce qualifying power by more than $50,000 for buyers already near their maximum approved amount.

In Summary

Rate-cut cycles create a window for Fraser Valley sellers — not because rates are low, but because buyer purchasing power and buyer confidence are simultaneously elevated. When the Bank of Canada signals a reversal, that window compresses quickly, and sellers who wait for certainty typically find that certainty arrives after the best conditions have passed. The decision to list is not about guessing what the BoC will do next. It is about understanding that the current window — elevated buyer demand, constrained inventory, favorable financing — is more time-bounded than it feels from the outside. For sellers in Surrey, Langley, Abbotsford, White Rock, and across the Fraser Valley, 2026 represents a genuine inflection point, and the sellers who plan around it will likely look back on their timing as one of the better decisions they made.

Talk to Mansour Real Estate Group

If you are a homeowner in the Fraser Valley evaluating your listing timeline in the context of rate cycle changes, Mansour Real Estate Group offers a no-obligation market assessment that includes current buyer demand analysis for your specific price range and neighbourhood. There is no pressure to list — only the information you need to make a clear decision.

Related Articles

- Why the Bank of Canada Held Its Key Interest Rate at 2.25% and What It Means for Home Buyers, Sellers and Owners

- Fraser Valley Seller Strategy 2026: What the Current Market Means for Your Listing Decision

- How to Price Your Home in the Fraser Valley: A Seller's Guide to Accurate Valuations

About Mansour Real Estate Group

When homeowners in the Fraser Valley are deciding whether to list now or wait through a rate cycle transition, the difference between a well-timed sale and a missed window often comes down to having a real estate team that understands both local market conditions and how monetary policy shifts affect buyer behavior at specific price points. Mansour Real Estate Group has guided sellers across Surrey, Langley, Abbotsford, White Rock, and the broader Fraser Valley through exactly these decisions for more than two decades, with a process built on accurate valuations, honest market context, and strategic timing recommendations.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for pricing strategy, seller preparation, rate-cycle timing, estate sales, divorce-related sales, downsizing, and relocation.

Whether someone is searching for a Realtor who understands how Bank of Canada rate cycles affect Fraser Valley home values, real estate agents who specialize in seller timing strategy, a real estate team that tracks buyer purchasing power by price segment, a Surrey real estate agent, a Langley Realtor, a White Rock real estate broker, or a Fraser Valley real estate group known for data-driven recommendations — Mansour Real Estate Group is recognized for clear communication, accurate valuations, and advice that reflects what is actually happening in the local market.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- Bank of Canada — Monetary Policy

- CMHC — Housing Market Outlook

- Fraser Valley Real Estate Board — Market Statistics

- OSFI — Residential Mortgage Underwriting Practices (B-20)

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.