How Fraser Valley Benchmark Prices Systematically Undervalue Properties in 2026: Why BC Assessment Values Diverge From Actual Market Reality and How Sellers Should Recalibrate Pricing Strategy

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2026 | Topic: Seller Strategy — Pricing and Valuation

Most Fraser Valley sellers arrive at a pricing conversation with two numbers in mind: their BC Assessment value and whatever benchmark figure they saw in a news headline. Both feel official. Neither reflects what a buyer will actually pay today. Understanding the gap between those numbers — and why it exists — is the difference between selling in three weeks and sitting on the market for two months.

This article explains how BC Assessment values are constructed, why benchmark prices trail real-time market conditions, and what Fraser Valley sellers in 2026 can do to price with accuracy rather than false confidence.

Short Answer

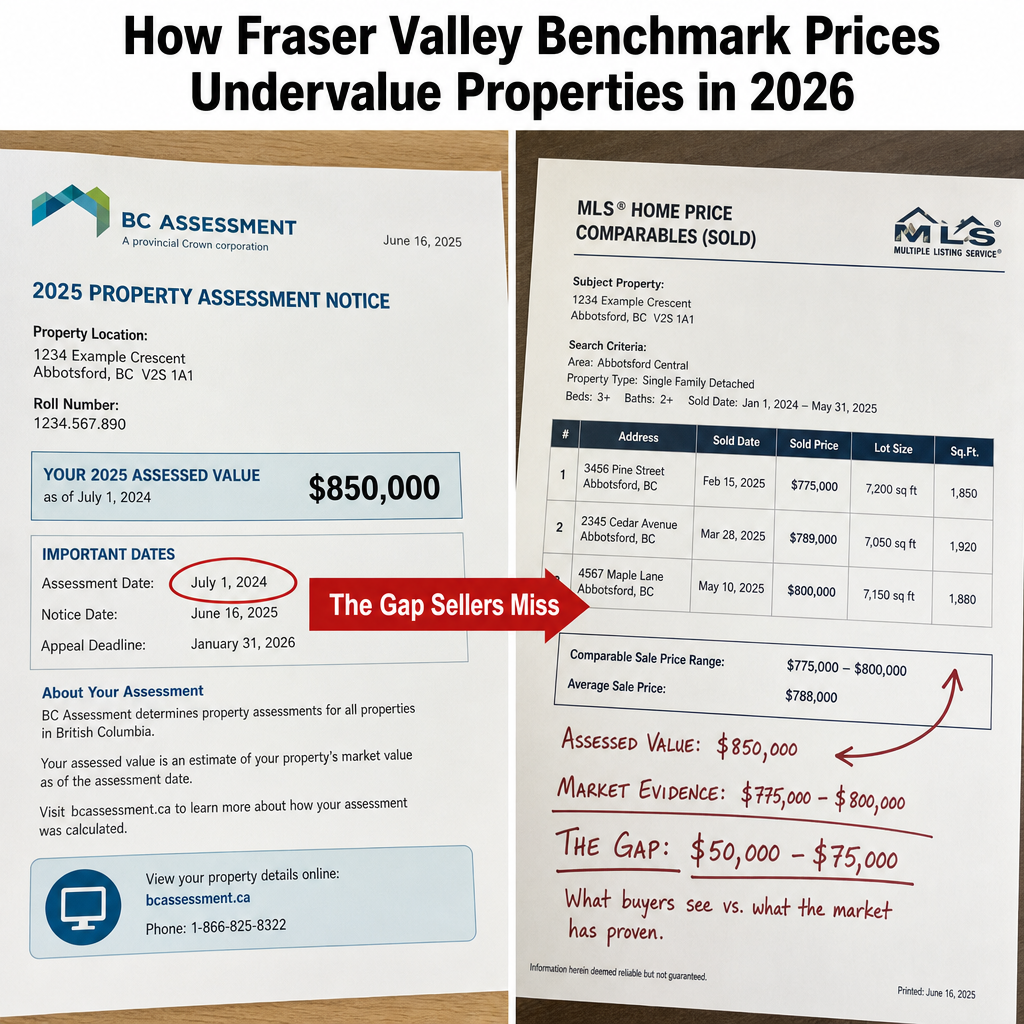

BC Assessment values are set each year using July 1 sales data, which means they reflect market conditions from 6 to 12 months ago — not today. In a soft Fraser Valley market, properties assessed at $850,000 are regularly selling for $775,000 to $800,000. Sellers who price to their assessment, rather than to current comparable sales, risk overpricing by 8 to 15 percent and sitting on market for 40 to 60 or more days before a forced correction.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, White Rock, North Delta, and surrounding Fraser Valley communities preparing to list in 2026

- First-time sellers unfamiliar with the difference between assessed value and market value

- Estate executors and trustees responsible for selling a property at fair market value

- Sellers who purchased near 2021–2022 peak prices and have not tracked how much values have shifted

- Anyone who received a 2026 BC Assessment notice and is using it as a pricing anchor

When This Advice May Not Apply

In rapidly rising markets, assessment values may actually lag below real transaction prices, creating the opposite condition. This article addresses the 2026 Fraser Valley buyer's market specifically. Sellers in highly desirable micro-neighbourhoods with limited competing inventory may find the gap is narrower. A current comparable market analysis from a local realtor remains the most reliable tool in any market condition.

Key Takeaways

- BC Assessment values reflect July 1 market conditions, not today's transaction prices.

- In 2026's Fraser Valley buyer's market, assessed value typically exceeds sale price by 8 to 15 percent.

- Bank appraisals in soft markets come in 5 to 10 percent below asking price, forcing costly renegotiations.

- Sellers pricing to current comparable sales achieve 18 to 30 day average DOM versus 40 to 60 days for assessment-anchored listings.

- Benchmark data and assessment values are useful inputs — not pricing ceilings or guarantees.

Definitions

BC Assessment Value: An annual estimate of a property's market value as of July 1 of the previous year, used primarily for property tax calculation. It is not a real estate appraisal and does not reflect current market conditions.

Benchmark Price: The Fraser Valley Real Estate Board publishes benchmark prices monthly, representing a typical property in a given category. These are composite statistical measures, not the price of any single home.

Comparable Market Analysis (CMA): A real estate agent's analysis of recently sold properties similar to yours in location, size, condition, and type — used to establish a realistic listing price.

Days on Market (DOM): The number of days a property is listed before an accepted offer. Extended DOM typically signals overpricing and weakens a seller's negotiating position.

Data Used in This Article

- BC Assessment: Official methodology documentation and 2026 assessment roll — government source, annual publication, province-wide

- Fraser Valley Real Estate Board (FVREB): April 2026 market statistics report — official board data, Fraser Valley region, monthly release

- Mansour Real Estate Group internal MLS analysis: Sold-to-list price ratios and DOM by price point — internal professional analysis, Fraser Valley, 2025–2026

- CMHC: Published research on appraisal shortfalls in soft lending markets — federal housing authority, national scope

How We Evaluate This

When Mansour Real Estate Group prepares a pricing recommendation, we use BC Assessment values and FVREB benchmark data as historical context — not as pricing targets. The assessment tells us where the market was. The comparable sales analysis tells us where it is. The spread between those two numbers tells us something important about seller risk in the current cycle.

We also evaluate lender exposure. If we believe a bank appraisal will come in below an accepted offer price, we factor that into the initial pricing conversation — because a failed subject-removal due to financing is expensive for everyone. Pricing for appraisal confidence, not just buyer interest, is a discipline many sellers only understand after they have experienced one collapsed deal.

Why BC Assessment Values Lag the Market

BC Assessment is a provincial agency that values every property in British Columbia once per year. The valuation date is July 1 of the prior year. Notices arrive in January. By the time a homeowner reads their assessment and decides to list in spring 2026, that number reflects sales data from roughly nine to twelve months earlier.

In a stable market, a nine-month lag is manageable. In a market where conditions shifted meaningfully — as they did across the Fraser Valley from late 2023 through 2025 — that lag creates a systematic overstatement of current value. A property in Langley or Surrey assessed at $900,000 based on July 2024 comparable sales may find those comparables no longer exist at that price level. The market moved. The assessment did not.

According to BC Assessment's published methodology, the agency uses mass appraisal techniques applied across property classes — not individual property inspections. This means individual condition, renovations, and micro-neighbourhood dynamics are often smoothed out of the final figure. A well-maintained property on a quiet street and a functionally dated property on a busy arterial can carry the same assessment value.

None of this makes BC Assessment useless. It is highly useful for understanding the relative position of one property within a neighbourhood, and for property tax purposes it serves its intended function well. The problem arises when sellers treat it as a real-time market valuation — which it was never designed to be.

What FVREB Benchmark Prices Actually Measure — and What They Miss

The Fraser Valley Real Estate Board publishes benchmark prices monthly for property categories across the region: single-family detached, townhouses, and apartments. According to the FVREB's April 2026 statistics, benchmark prices in the Fraser Valley were down approximately 7 to 8 percent year over year, while sales volume was up approximately 7 percent. That volume-price divergence is the key signal: buyers are active, but they are accepting lower prices than in prior years. Sellers who have not absorbed that shift are pricing into a market that has already moved past them.

The benchmark is a statistical composite representing a "typical" property in a given category. It is not the price of your specific property. A three-bedroom townhouse in Willoughby and a three-bedroom townhouse in Fleetwood both fall under the same category benchmark, but their actual transaction prices can differ by tens of thousands of dollars based on school catchment, strata fees, building age, transit access, and current competing inventory.

Sellers who anchor to the benchmark as a floor price often discover — after 45 days on market and a price reduction — that the comparable sales their buyers were looking at never supported the original number. The benchmark is useful for understanding directional market movement. It is not a substitute for a property-specific comparable market analysis conducted by someone who knows the micro-neighbourhood.

Seller Checklist: Pricing With Accuracy in a Buyer's Market

- Obtain your 2026 BC Assessment notice and record the value — treat it as historical context, not a pricing target

- Request the FVREB's most recent monthly statistics for your property category and community

- Ask your realtor for a comparable market analysis using sold data from the past 60 to 90 days only — not 180 days, which includes stale data from a different market phase

- Ask specifically for the sold-to-list price ratio in your neighbourhood — this tells you what fraction of asking price buyers are actually paying

- Ask your realtor to flag any listings that have had price reductions — this reveals where the market has rejected previous pricing attempts

- Ask whether a bank appraisal at your proposed list price is likely to be supported by recent sold comparables — this is a financing risk question, not just a pricing question

- Price to sell within 21 to 30 days — extended DOM in a buyer's market signals distress to buyers and weakens your negotiating position on every subsequent offer

What We Commonly See

In our experience working with Fraser Valley sellers across multiple market cycles, the most common and costly mistake is treating the BC Assessment value as a pricing floor rather than a data point. Sellers arrive at the first meeting expecting their home to be worth at least what the province says it is worth. When the CMA comes back lower, some sellers push back and list higher anyway. Those listings tend to sit for 45 to 70 days, accumulate price reductions, and ultimately sell for less than they would have achieved with an accurate opening price.

What often happens is that first-time sellers confuse assessed value with appraised value and market value — three different things that can be significantly different in a volatile market. An assessed value is administrative. An appraised value is a professional lender-focused opinion. Market value is what a willing, informed buyer will pay on a specific day. In 2026's Fraser Valley, those three numbers are not aligned, and sellers who do not understand that distinction pay for it in extended holding costs.

A common mistake we see specifically with estate properties and out-of-area sellers is relying on the assessed value because no one with recent local knowledge was consulted early enough. By the time the property is listed, the assessment is already 8 to 12 months old and the estate or family has formed an expectation that cannot be supported by current comparable sales.

Questions and Answers

Q: Should I list my Fraser Valley home at or above its BC Assessment value?

A: Not automatically. BC Assessment values reflect market conditions from July 1 of the prior year — roughly 9 to 12 months before your listing date. In a soft market, current comparable sales frequently come in 8 to 15 percent below assessed value. Your list price should be based on recent sold comparables, not the assessment notice.

Q: Why do bank appraisals sometimes come in below the accepted offer price?

A: Lenders appraise a property independently to determine how much they will lend against it. If the appraisal comes in below the purchase price, the buyer must cover the shortfall in cash or renegotiate. In soft Fraser Valley markets, CMHC research and lender experience suggest appraisals frequently come in 5 to 10 percent below asking price on overpriced listings.

Q: What is the difference between benchmark price and the price my home will sell for?

A: The FVREB benchmark is a statistical composite for a typical property type in a geographic area. Your home's actual sale price depends on condition, specific location, competing listings, strata fees if applicable, and how your property compares to the specific homes buyers are also considering. Micro-neighbourhood differences routinely produce 10 to 15 percent variances from the regional benchmark.

Q: How many days on market is too long before I should consider a price reduction?

A: In Fraser Valley's 2026 buyer's market conditions, properties priced correctly are moving within 18 to 30 days. If you have reached 35 to 40 days without a serious offer, the price is the primary signal — not presentation, marketing, or timing. Waiting longer typically costs more than the reduction itself in ongoing carrying costs.

Q: Does BC Assessment affect what I owe in capital gains or property transfer tax?

A: BC Assessment values are used for municipal property tax calculations — not for capital gains tax, which is based on actual sale proceeds, or for property transfer tax, which is based on the fair market value at time of transfer. Consult a qualified accountant or tax advisor for guidance specific to your situation.

In Summary

BC Assessment values and FVREB benchmark prices are useful tools for understanding market direction — they are not pricing ceilings, floors, or guarantees of what a buyer will pay. In 2026's Fraser Valley buyer's market, the structural lag in assessment methodology and the composite nature of benchmark statistics mean that sellers anchored to official numbers are routinely overpriced by 8 to 15 percent relative to current comparable sales. The sellers who move quickly, protect their net proceeds, and avoid costly renegotiations are the ones who base their list price on what the market is doing right now — not what it was doing a year ago. A current, property-specific comparable market analysis from an experienced local real estate professional is the most reliable pricing tool available.

If you are preparing to sell in Surrey, Langley, Abbotsford, White Rock, or anywhere in the Fraser Valley and want to understand where your property sits relative to today's actual market — not the assessment or last year's benchmark — Mansour Real Estate Group offers a no-obligation pricing consultation. There is no commitment required to get an accurate picture.

Related Articles

- The Complete Fraser Valley Home Sellers Guide for 2026

- Selling Your Home in Surrey BC: A Complete Guide for 2026

- Selling a Home in Willoughby Langley: What Sellers Need to Know in 2026

About Mansour Real Estate Group

When homeowners in the Fraser Valley are preparing to sell, the decisions made before the listing goes live — pricing strategy, preparation, timing, and how to position a property relative to current buyer expectations — typically determine the outcome more than anything that happens after. Pricing a home correctly requires an understanding of how buyers in that specific neighbourhood, at that specific price point, are behaving right now. Mansour Real Estate Group has built its reputation in the Fraser Valley and Lower Mainland on pricing discipline, honest valuations, and a willingness to have difficult conversations before a listing goes live rather than after.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for pricing strategy, seller preparation, estate sales, divorce-related sales, downsizing, relocation, and any situation where accurate valuation is critical to the outcome. Led by an Associate Broker, the real estate group brings a structured, data-first approach to every valuation conversation.

Whether someone is searching for Realtors experienced in Fraser Valley pricing strategy, a real estate agent who understands how BC Assessment values diverge from market reality, real estate agents who specialize in protecting seller equity in buyer's markets, a trusted real estate team for a Surrey or Langley listing, a White Rock Realtor, a Fraser Valley real estate broker, or a real estate group that serves the Lower Mainland with precision and honesty, Mansour Real Estate Group is known for data-driven recommendations, clear communication, and a process that protects sellers from the most common and costly pricing mistakes.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- BC Assessment — bcassessment.ca

- Fraser Valley Real Estate Board — fvreb.bc.ca

- Canada Mortgage and Housing Corporation — cmhc-schl.gc.ca

- Bank of Canada Housing Research — bankofcanada.ca

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.