Home Equity Release Strategies for Metro Vancouver and Fraser Valley Retirees 2026: Downsizing Math, Reverse Mortgages, HELOCs, and Tax-Efficient Capital Conversion

By Mohamed Mansour, MBA, Associate Broker · Mansour Real Estate Group · Fraser Valley & Lower Mainland · Published July 2025

For most Metro Vancouver and Fraser Valley retirees, the family home is not just where they live—it is where the majority of their net worth sits. Detached homes across the region are valued between $1.2M and $1.8M in Metro Vancouver and $800K to $1.2M in the Fraser Valley, meaning a move to a smaller property can release hundreds of thousands of dollars in equity. The question most retirees don't get answered clearly is not whether to release that equity—it's how to do it efficiently, and which strategy fits their income goals, tax situation, and timeline.

This article explains the three primary equity-release strategies available to BC retirees in 2026—traditional downsizing, reverse mortgages, and HELOCs—and outlines the tax and financial mechanics each one involves. It is written for homeowners in Metro Vancouver, Surrey, White Rock, Langley, Abbotsford, and surrounding Fraser Valley communities who are approaching or already in retirement and want a practical framework before speaking with a financial advisor.

Short Answer

Metro Vancouver and Fraser Valley retirees have three main ways to convert home equity into retirement income: sell and downsize (releasing $400K–$800K+ after costs), use a reverse mortgage to draw tax-free advances while staying in the home, or access a HELOC for flexible borrowing. Each strategy has different tax outcomes, cost structures, and income timing. The right choice depends on whether the priority is maximizing lump-sum capital, preserving the family home, or maintaining flexible liquidity.

Key Takeaways

- Downsizing from a detached home to a Fraser Valley condo or 55+ strata unit typically releases $400K–$800K after all transaction costs, depending on location and property type.

- The principal residence exemption eliminates capital gains tax on the family home's appreciation—preserving 100% of that equity for retirees who qualify.

- Reverse mortgages from lenders like Home Equity Bank or Equitable Bank offer non-repayable, tax-free advances at 6.5–7.5%, with no payments until the home is sold or the owner dies.

- A HELOC at prime plus 0.5–1.0% can be used to fund income-generating investments where the interest may be tax-deductible under CRA's investment-income rules.

- 55+ strata communities in White Rock, Langley, and Abbotsford cost 40–50% less than unrestricted Metro Vancouver equivalents, significantly increasing the reinvestment capital available after a downsize.

Who This Applies To

- Homeowners aged 55 to 75 who own a detached home in Metro Vancouver or the Fraser Valley and are approaching or recently entered retirement.

- Retirees whose primary financial asset is their home and who need to convert equity into reliable monthly income.

- Couples or individuals evaluating whether to sell now, stay and borrow, or stage a phased transition over two to five years.

- Adults managing a parent's housing and financial transition who need to understand the options before consulting legal or financial advisors.

When This Advice May Not Apply

If the home is jointly owned with a non-resident of Canada, is subject to an outstanding strata wind-up, or has been partially used for rental purposes in recent years, different tax rules may apply. Retirees with significant RRIF balances, rental income, or complex estate plans should coordinate any equity-release decision directly with a tax advisor or accountant before proceeding.

Data Used in This Article

- FVREB and REBGV/GVR Spring 2026 Benchmark Price Data — official board statistics; property type benchmarks by geography (official)

- BC Ministry of Finance Property Transfer Tax Calculator 2026 — PTT rate thresholds and calculations (official)

- CRA Principal Residence Exemption Rules and Deemed Disposition Guidelines — tax treatment of principal residence sales (official)

- Home Equity Bank and Equitable Bank Reverse Mortgage Product Data 2026 — rate ranges and product terms (third-party lender disclosure)

- CMHC Housing Research: Affordability and Equity Data, Metro Vancouver and Fraser Valley — equity position benchmarks by region (official/research)

Definitions

Principal Residence Exemption (PRE): A CRA provision that eliminates capital gains tax on the sale of a home that qualifies as a principal residence for the years owned. Proper annual designation is required to claim the full exemption.

Reverse Mortgage: A loan secured against home equity available to homeowners 55 and older. No monthly payments are required. The full balance is repaid when the home is sold or the owner passes away.

HELOC (Home Equity Line of Credit): A revolving credit facility secured against home equity. Interest is charged only on the amount drawn. Rates are typically variable, set at prime plus a spread.

Deemed Disposition: A CRA rule that treats certain property transfers—such as converting a principal residence to a rental property—as a sale at fair market value, triggering potential capital gains tax even without an actual sale.

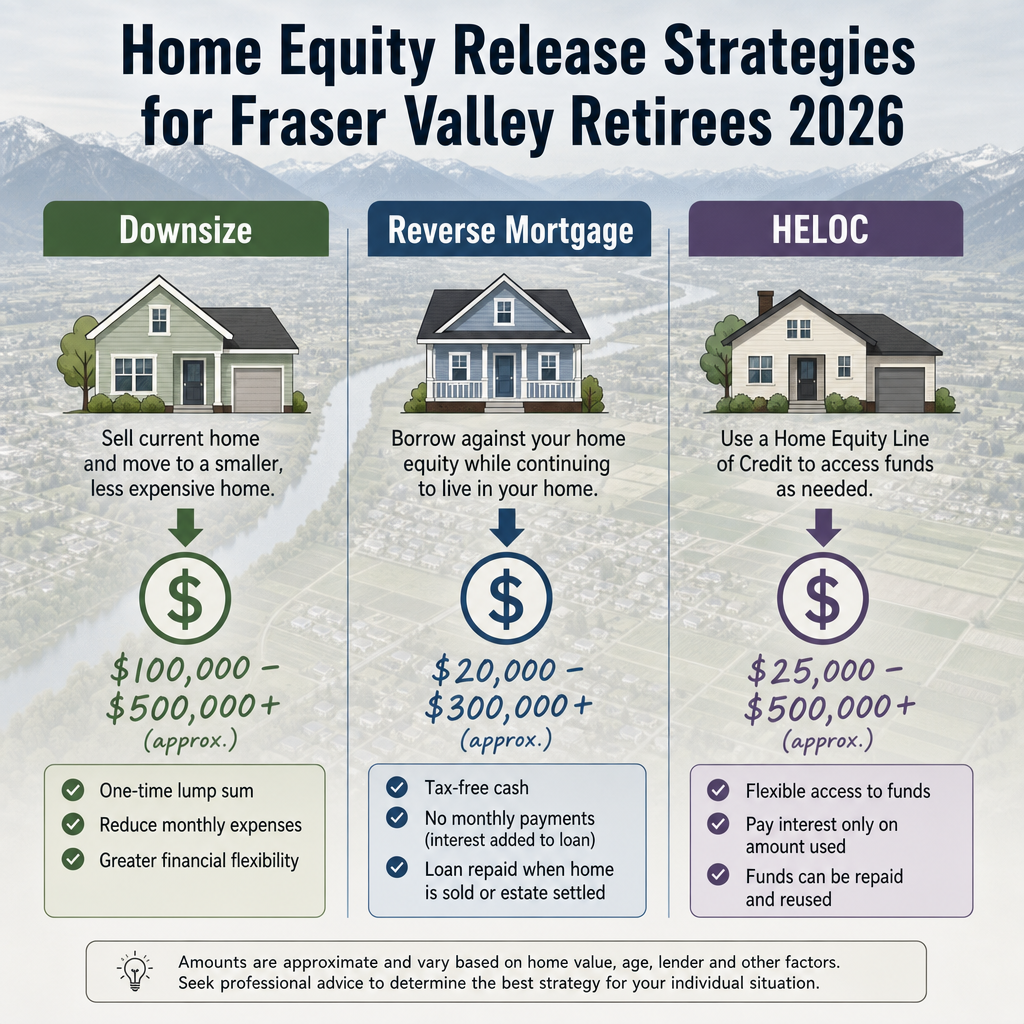

Strategy 1: Traditional Downsizing and the Downsizing Math

Selling a detached family home and purchasing a smaller condo, townhome, or 55+ strata unit remains the most straightforward equity-release approach. The math, however, is more specific than most retirees expect. As detailed in How Much Money Will You Free Up By Downsizing in Metro Vancouver?, the gross sale price is not what retirees actually receive.

After accounting for real estate commissions (typically 6–7% of total transaction value under BC commission structures), legal fees of $2,000–$3,000 on each side, property transfer tax on the new purchase (3% on the first $200,000, 5% on the next $1.8M, and 10% above $3M, per the BC Ministry of Finance 2026 schedule), and moving costs, the net proceeds on a $1.5M sale with a $900K condo purchase may look like this: gross sale of $1.5M minus $90K–$105K in combined transaction costs leaves approximately $395K–$410K in net freed-up equity after purchasing the replacement property.

The Fraser Valley advantage is meaningful here. A 55+ strata unit in Langley or Abbotsford at $700K–$850K versus a Metro Vancouver equivalent at $1.2M+ changes the reinvestment picture entirely. As covered in 55+ Strata Communities in Fraser Valley: What Retirees Need to Know, these communities also carry lower strata fees and property tax burdens, reducing ongoing carrying costs and extending the life of the released capital.

The 2026 Fraser Valley market context matters. According to FVREB spring 2026 data, benchmark prices across detached Fraser Valley homes declined approximately 7–8% year over year. That compression reduces a seller's gross proceeds—a $750K home may now list at $690K–$710K—but it also compresses the cost of the replacement property. Retirees selling and buying within the same market absorb the correction on both sides, which partially neutralizes the impact on net freed equity.

For timing considerations around when to move through this process, How to Time Selling Your Home and Buying a Condo for Retirement in Metro Vancouver addresses sequencing, bridge financing, and market-timing decisions in detail.

The Principal Residence Exemption: Why Timing the Designation Matters

For most retirees who have owned their home for 20 to 40 years and lived in it throughout, the principal residence exemption (PRE) eliminates all capital gains tax on the sale. This is not automatic—it requires proper designation on CRA Form T2091 at the time of filing taxes for the year of sale. Tax Implications of Selling Your Home When You Retire in BC addresses this in more detail.

Where the PRE becomes complicated is when the property was used partly for rental income at any point. Under CRA's deemed disposition rules, converting a principal residence to a rental property—or the reverse—may trigger a deemed sale at fair market value on the date of conversion. A retiree who rented out a suite for five years before selling may find that a portion of the home's appreciation is treated as a capital gain rather than a tax-exempt principal residence gain. As noted in Should I Sell My House or Rent It Out When I Retire in BC?, this distinction is one of the most frequently misunderstood aspects of retirement real estate planning in BC.

Retirees with homes that have appreciated from $400K to $1.6M—a realistic scenario for someone who purchased in Surrey or Langley in the early 2000s—are looking at a $1.2M gain. If the PRE applies fully, the entire gain is tax-free. If only partial exemption applies due to mixed use, the taxable capital gain could be significant. This is a decision that requires a qualified tax advisor, not general guidance.

Strategy 2: Reverse Mortgages—Staying in the Home While Accessing Equity

For retirees who do not want to sell—or who want to delay a sale for estate or personal reasons—a reverse mortgage allows equity release without a transaction. Home Equity Bank (the CHIP Reverse Mortgage) and Equitable Bank both offer products available to BC homeowners aged 55 and older. As of 2026, rates on these products run between 6.5% and 7.5%, which is higher than a standard mortgage. No monthly payments are required; the interest compounds and the full balance is repaid when the home is sold or the last borrower passes away.

The advance is not considered taxable income by CRA—it is a loan, not a capital gain or income receipt. This makes it particularly useful for retirees who need to supplement CPP and OAS without triggering OAS clawback thresholds. Lenders will advance up to 50–60% of the home's appraised value, depending on the borrower's age and the property type. A $1.2M home could yield a $600K–$720K advance, which can be taken as a lump sum, monthly installments, or a combination.

The cost of a reverse mortgage is the compounding interest over time. A $300K advance at 7% compounding annually for 10 years grows to approximately $590K in outstanding debt. If the home has appreciated in parallel, there may be substantial remaining equity at sale. If the home has not appreciated or has declined in value, the erosion of equity is real. Reverse mortgages are well-suited for retirees with significant home equity, no plans to sell within five years, and a clear income-generation need. They are less suitable for retirees whose primary goal is estate preservation or who intend to sell within a shorter timeframe.

Strategy 3: HELOCs—Flexible Borrowing With a Tax-Efficient Application

A HELOC secured against the family home allows retirees to borrow at prime plus 0.5–1.0%, draw only what they need, and repay on a flexible schedule. Unlike a reverse mortgage, a HELOC requires the borrower to qualify under standard lending criteria and service the interest payments from income or other sources.

The most tax-efficient application of a HELOC in retirement is using the borrowed funds to purchase income-generating investments—dividend-paying equities, bond funds, or other eligible investments. Under CRA's investment expense deduction rules, interest paid on money borrowed for the purpose of earning income from an eligible investment may be deductible against that investment income. This is sometimes called the "debt-recycling" or "Smith Manoeuvre" approach in Canadian financial planning. It requires careful structuring, and CRA scrutinizes aggressive applications of this strategy—professional tax advice is essential before implementing it.

HELOCs are also useful for staged equity release: a retiree who plans to sell in two to four years may draw on a HELOC now to bridge income needs, then repay the balance from sale proceeds. This avoids locking into a reverse mortgage's higher compounding rate for a short hold period.

How We Evaluate This

When Mansour Real Estate Group works with retirees who are weighing equity-release options, the starting point is always the same: what is the realistic net equity available after a sale, and how does that compare to the carrying cost of staying? Most retirees are surprised by the precision of this calculation once all transaction costs, PTT, commission, and replacement property costs are modeled together.

We work with clients to understand whether the goal is maximizing a lump-sum reinvestment, minimizing ongoing housing costs, or preserving the home for estate reasons—because each goal leads to a different strategy. We bring the real estate side of that analysis and refer directly to accountants, tax advisors, and financial planners for the income, tax, and investment components. The decisions overlap, and no single professional can cover all of them independently.

Downsizing Checklist for Equity-Focused Retirees

- Confirm principal residence exemption eligibility with your accountant, especially if any part of the home was rented at any point.

- Run the full net-equity math: sale price minus commission, legal fees, PTT on purchase, and moving costs, before committing to a target replacement price.

- Determine whether the priority is maximum freed capital (Fraser Valley 55+ strata), lifestyle proximity (Metro Vancouver condo), or income-generation capacity from reinvested proceeds.

- If considering a reverse mortgage, obtain quotes from both Home Equity Bank and Equitable Bank and have an independent financial advisor review the compounding cost scenario over your estimated hold period.

- If considering a HELOC for investment purposes, confirm with a tax advisor whether the interest-deductibility structure you plan to use qualifies under current CRA rules.

- Coordinate the sale timeline with RRIF minimum withdrawal schedules—large lump-sum proceeds don't add directly to income tax in the year of sale if the PRE applies, but reinvestment income will affect future-year tax exposure.

- Review the PTT cost on your replacement property. See BC Property Transfer Tax and Downsizing: What Retirees Pay When They Buy Their Next Home for the current rate structure.

What We Commonly See

Underestimating transaction costs on both sides. In our experience, retirees typically estimate commission correctly but forget to factor PTT on the new purchase, legal fees on both transactions, and home preparation costs on the sale side. The combined cost can be $60,000–$120,000 higher than expected on a $1.5M sale and $900K purchase. Planning for the net number—not the gross—is critical.

Choosing the wrong equity-release strategy for the timeline. What often happens is a retiree sets up a reverse mortgage intending to sell in three years, then stays longer than planned—allowing interest to compound for 8–10 years at 6.5–7.5%. Conversely, we see retirees downsize prematurely, releasing equity into cash before they have a clear income deployment plan, and sitting on low-return deposits while carrying unnecessary reinvestment friction.

Missing the PRE designation on the tax return. A common mistake is assuming the principal residence exemption is applied automatically by CRA. It must be formally designated on the tax return for the year of sale using Form T2091. Missing or incorrectly filing this form can result in a taxable capital gain on a transaction that should have been fully exempt. A tax professional should file the year-of-sale return, not a self-prepared return.

Questions and Answers

Is the money I receive from downsizing taxable in BC?

If the sold property qualifies fully as your principal residence under CRA rules, the capital gain on the sale is exempt from tax. The proceeds themselves are not income. How you invest those proceeds afterward may generate taxable income in future years. Always file CRA Form T2091 in the year of sale to formally claim the exemption.

How much equity can I release through a reverse mortgage in BC?

As of 2026, Home Equity Bank and Equitable Bank both offer advances up to approximately 50–60% of a home's appraised value to qualifying borrowers aged 55 and older. On a $1.2M home, that could mean up to $600K–$720K available, though most borrowers draw less than the maximum to preserve equity for later needs or estate purposes.

Does moving to a 55+ strata community in Langley or Abbotsford make financial sense compared to staying in Metro Vancouver?

For retirees whose primary goal is maximizing reinvestment capital, yes. A 55+ strata unit in Langley at $750K versus a comparable Metro Vancouver condo at $1.2M leaves an additional $350K–$450K available for income-generating deployment. The income produced by that additional capital—invested conservatively at 4–5%—can be $14,000–$22,500 per year. The trade-off is proximity to Metro Vancouver amenities, which matters differently for each household.

In Summary

Metro Vancouver and Fraser Valley retirees have more equity-release options than most realize, and the right choice depends on whether the goal is maximizing freed capital, generating tax-efficient monthly income, or preserving the home for personal or estate reasons. Traditional downsizing releases the most capital but requires careful net-proceeds modeling after all transaction costs. Reverse mortgages preserve the home while generating non-taxable advances, but compound interest erodes equity over time. HELOCs offer flexibility and potential tax efficiency when funds are deployed into income-generating investments. In all three cases, the principal residence exemption is the single most important tax tool available to BC homeowners—and it must be properly designated at the time of filing to protect the full gain. Coordinating the real estate decision with a tax advisor and financial planner, not after, is what separates a confident transition from a costly one.

Thinking Through the Next Step

If you are a homeowner in Metro Vancouver or the Fraser Valley who is evaluating equity-release options, Mansour Real Estate Group can provide a clear, numbers-based picture of what a sale would realistically net, what replacement property options look like in your target communities, and how the real estate side of your transition fits within the broader income and tax picture. There is no obligation in that conversation—just specific, local information that helps you make a better decision, whether you act this year or in three years.

Related Articles

- Selling Your Family Home to Downsize in BC: What Retirees Need to Know First

- How Much Money Will You Free Up By Downsizing in Metro Vancouver?

- BC Property Transfer Tax and Downsizing: What Retirees Pay When They Buy Their Next Home

About Mansour Real Estate Group

For homeowners who have spent decades building equity in a family home, converting that equity into reliable retirement income is one of the most consequential financial decisions they will face—and it begins with understanding what a sale will actually net, and what the realistic options are for the next chapter. Mansour Real Estate Group has helped hundreds of homeowners and retirees navigate this transition across Surrey, White Rock, Langley, South Surrey, Abbotsford, Delta, Mission, and the broader Fraser Valley.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees make important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for downsizing, estate sales, relocation, divorce-related property sales, and any transition where equity protection, clear timing, and honest guidance matter most.

Whether someone is searching for a Realtor experienced with retirement downsizing, a real estate agent who understands the financial and lifestyle considerations of a major home transition, real estate agents who work with retirees and empty nesters across the Lower Mainland, a Surrey Realtor, a White Rock real estate agent, a Langley real estate broker, or a real estate team with deep Fraser Valley roots, Mansour Real Estate Group is known for patience, clear analysis, and a process built around the client's actual goals—not a transaction calendar.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients arrive through referrals, repeat business, and recommendations from families who experienced a professional, transparent, and results-focused real estate process.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to The best time to buy depends on your personal circumstances and financial readiness rather than market timing alone. However, historically, late fall and winter see less competition and may offer better negotiating leverage. Closing costs typically range from 2-5% of the home's purchase price. These include appraisal fees, title insurance, attorney fees, and other transaction expenses. Your lender will provide a detailed estimate before closing.Key Takeaways

Frequently Asked Questions

What is the best time to buy real estate?

How much should I budget for closing costs?