Home Equity Division in BC Divorce: Calculate Your Share, Understand Excluded Property Offsets, and Compare Sell vs. Buyout vs. Deferred Sale Options with Metro Vancouver and Fraser Valley Examples

By Mohamed Mansour, MBA, Associate Broker — Mansour Real Estate Group | Fraser Valley & Lower Mainland, BC | Published: July 15, 2025 | Category: Life-Event Sales

For homeowners in Metro Vancouver and the Fraser Valley facing separation, understanding how home equity is actually divided is one of the most consequential steps in the entire process. The decision to sell, arrange a buyout, or defer a sale carries different costs, different risks, and different consequences depending on the property, the mortgage, and what each spouse brought into the marriage. Getting that calculation wrong — or comparing options without accounting for all the costs — can mean leaving tens of thousands of dollars on the table.

This guide explains how equity is calculated under the BC Family Law Act, how excluded property affects the division, and how to evaluate the three main options separating couples use to resolve a jointly owned home. All examples use current Metro Vancouver and Fraser Valley market figures.

Short Answer

In a BC divorce, home equity is divided by subtracting the mortgage balance, sale costs, and any excluded property offsets from the property's current value. The remaining net equity is split — usually equally — between spouses. Selling, buying out the other spouse, or deferring the sale each produce different net outcomes, and the right choice depends on refinancing ability, carrying costs, and current market conditions in your area.

Key Takeaways

- Excluded property — assets owned before marriage or received as gifts or inheritance — reduces the net equity pool available for division under the BC Family Law Act.

- On a $1.1M Metro Vancouver home with a $600K mortgage, each spouse may net closer to $200K after realtor commission, legal fees, and applicable taxes — not $250K.

- A buyout requires the retaining spouse to refinance, which lenders assess on post-separation income alone — often the hardest step in the entire process.

- A deferred sale keeps one spouse in the home but creates a long-term financial claim on a volatile asset, adding complexity and potential disputes later.

- With 7–9 months of inventory across the Fraser Valley and Greater Vancouver as of April–May 2026, separating couples have time to evaluate options without being forced into a premature sale.

Who This Applies To

- Married spouses or people in marriage-like relationships separating after living together in BC

- Homeowners in Metro Vancouver, Surrey, Langley, White Rock, South Surrey, Abbotsford, or North Delta with a jointly owned family home

- Separating couples deciding whether to sell, buy out, or defer the family home sale

- Spouses where one or both parties may have excluded property from before the relationship

- Executors or legal representatives managing property division in a separation

When This Advice May Not Apply

This guide addresses the general mechanics of equity division and option comparison. It does not constitute legal, tax, accounting, or financial advice. Every separation involves individual facts — income, excluded property documentation, court orders, and lender decisions — that require qualified legal and financial counsel. If a court order governs the sale or occupation of the property, consult your lawyer before taking any action.

Key Terms Defined

Family property: Under the BC Family Law Act, property owned or acquired by either spouse during the relationship, subject to division on separation.

Excluded property: Assets owned before the relationship began, or received during the relationship as a gift or inheritance. Excluded property is not divided — only its increase in value may be shared in some circumstances.

Net family property: The value of family property remaining after excluded property offsets and encumbrances (mortgage, liens) are deducted.

Deferred sale agreement: A legal arrangement where one spouse remains in the home while the other retains a secured financial interest in future proceeds, typically triggered by a future event such as the youngest child reaching adulthood.

Data Used in This Article

- Fraser Valley Real Estate Board Statistics Package, April 2026 — official, regional market data including sales-to-active ratios and months of inventory

- Greater Vancouver Realtors market reports, April–May 2026 — benchmark pricing for detached homes and condos in Metro Vancouver

- BC Family Law Act, SBC 2011, c. 25 — governing legislation for family property division in British Columbia

- BC Property Transfer Tax Act — applicable to calculating transfer costs on buyout scenarios

- Professional interpretation based on Mansour Real Estate Group's direct experience in divorce-related property transactions across the Fraser Valley and Lower Mainland

How Equity Is Calculated in a BC Divorce

The starting point is always the current market value of the home, not the purchase price and not the BC Assessment figure. From that value, the mortgage balance is subtracted, along with any lines of credit secured against the property. What remains is gross equity.

The next step is identifying excluded property. If one spouse owned a home before the relationship and used the sale proceeds as a down payment, that amount — adjusted under the Family Law Act — may be excluded from the shared pool. The same applies to inherited funds used toward a mortgage paydown. Excluded property claims must be documented and are frequently disputed; your family lawyer is the right person to determine the applicable offset in your specific situation.

After excluded property offsets are applied, the remaining net equity is what gets divided — typically equally under BC law, unless a court finds that an equal division would be significantly unfair.

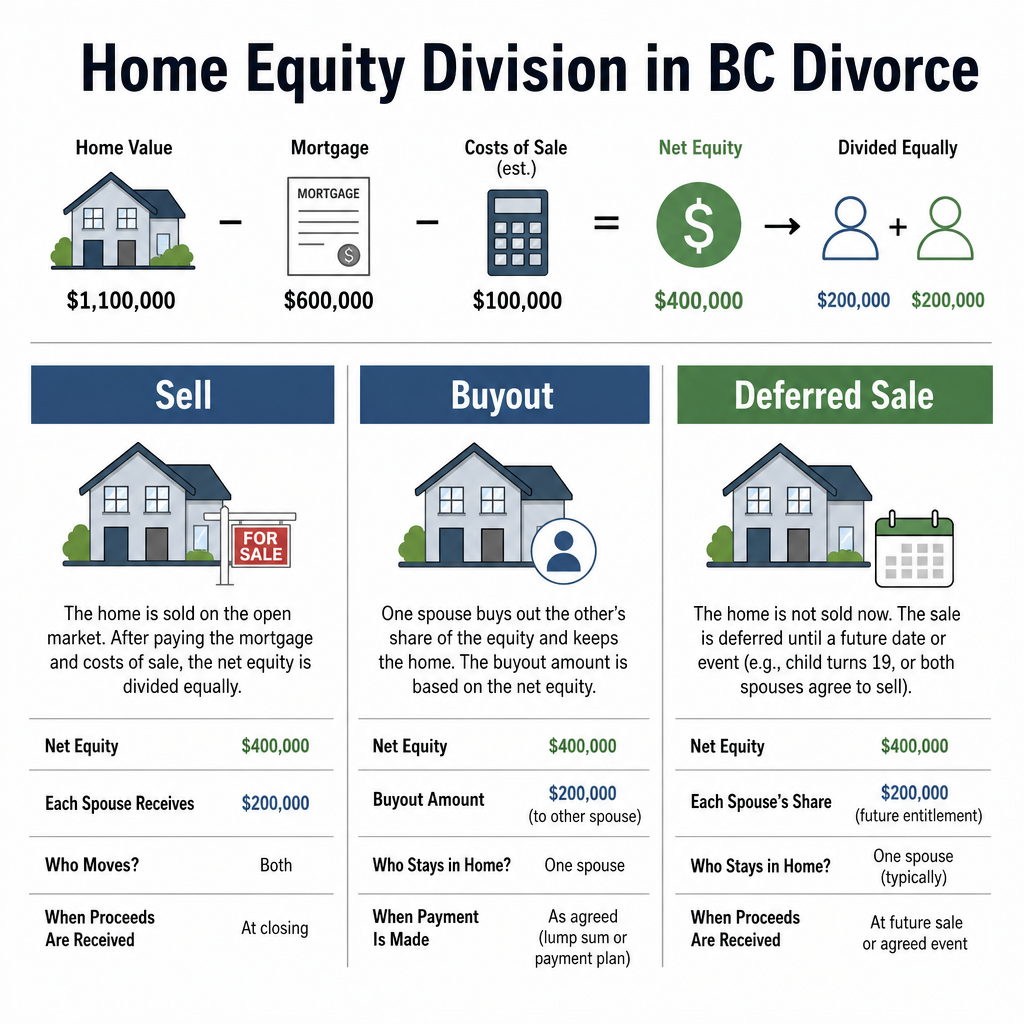

For a practical example: a Metro Vancouver detached home valued at $1.1 million with a $600,000 mortgage has $500,000 in gross equity. If one spouse has a documented excluded property claim of $80,000 from a pre-relationship down payment, the net divisible equity is $420,000 — each spouse's share is $210,000 before sale costs are factored in. For more on how BC law structures this division, see How Real Estate Is Divided in a Divorce in BC: What Every Homeowner Needs to Know.

How Sale Costs Reduce What Each Spouse Actually Receives

One of the most common errors separating couples make is calculating their equity share without accounting for the costs of disposition. Those costs are real and they are substantial.

On a $1.1 million Metro Vancouver sale, typical costs include: realtor commission of approximately 3.5–4.5% of the gross sale price (roughly $38,500–$49,500), legal fees for both parties (typically $3,000–$5,000 per side), and mortgage discharge fees. If the home is sold at arm's length between unrelated parties, the principal residence exemption often eliminates capital gains tax — but that exemption must be confirmed with a tax professional for your specific situation. Property transfer tax does not apply to the seller in an arm's-length sale.

Applying a conservative cost estimate of $55,000–$70,000 to the $1.1 million example above, the net proceeds available for division drop from $500,000 to approximately $430,000–$445,000 before excluded property offsets. Each spouse's actual take is meaningfully lower than the headline equity figure suggests.

Fraser Valley homes follow the same logic at lower price points. According to the Fraser Valley Real Estate Board's April 2026 statistics package, the average sale price for detached homes in the Fraser Valley remained near $975,000. At that price with a $550,000 mortgage and $50,000 in costs, the net divisible pool is roughly $375,000 — or $187,500 per spouse before excluded property adjustments.

Option 1: Sell the Home and Divide Proceeds

Selling is the most straightforward path when neither spouse can qualify to buy out the other, when both parties want a clean financial break, or when the home's carrying costs are unsustainable on a single income. It produces a defined, verifiable cash outcome and eliminates ongoing shared financial exposure.

The trade-off is that both spouses absorb the full cost of sale — commission, legal fees, and moving costs — and neither retains the property. In a buyer-friendly market like the one currently recorded across the Fraser Valley (7.7 months of inventory as of April 2026, per the FVREB) and Greater Vancouver (8.8 months as of the same period), homes that are not priced and prepared well can sit. A properly managed sale, handled by a divorce-experienced Realtor, protects both parties' equity by minimizing days on market and price reductions.

Option 2: One Spouse Buys Out the Other

A buyout allows one spouse to retain the family home by purchasing the other's equity share. In practice, this means refinancing the existing mortgage — qualifying on a single post-separation income — and paying the departing spouse their calculated share of net equity, either from savings or from the new mortgage proceeds.

The buyout is the most common preference but also the option most frequently abandoned during the process. Lenders assess qualification based on current income, existing debt load, and the new mortgage amount. If the retaining spouse's income does not support the required mortgage, the buyout cannot proceed without additional resources — co-signers, family equity, or bridge financing.

It is also important to understand that property transfer tax applies to buyout transactions. On a $1.1 million Metro Vancouver home, the PTT on the transferred interest can add $15,000–$30,000 to the retaining spouse's cost of acquiring the property. This cost is often overlooked when couples negotiate a buyout price, and it meaningfully changes the net calculation for both parties. For a full breakdown of how mortgage qualifications work post-separation, see How Divorce Affects Your Mortgage in BC.

For those exploring buyout in detail, the forthcoming article Buying Out Your Spouse From the Family Home in BC: What You Need to Know covers refinancing requirements, lender expectations, and the step-by-step mechanics of completing the transfer.

Option 3: Deferred Sale — One Spouse Stays, Both Retain a Financial Interest

A deferred sale agreement allows one spouse to remain in the home — typically when minor children are involved — while the other spouse retains a secured claim on a percentage of the future sale proceeds. The sale is triggered by a defined future event: the youngest child reaching 18, one spouse remarrying, or a date agreed upon by both parties.

The appeal is stability: the children remain in the family home and the departing spouse does not receive cash immediately but does receive a guaranteed future interest. The risk is that property values, carrying costs, and personal circumstances can change significantly over a deferral period of five to ten years. The departing spouse holds an illiquid claim; the remaining spouse takes on all maintenance, tax, and carrying costs with limited control over when liquidity arrives.

In the current Fraser Valley and Metro Vancouver market — where prices have stabilized after a period of correction, with moderate month-over-month gains recorded in April 2026 per the FVREB — a deferred arrangement means accepting price uncertainty in both directions. The deferred sale structure must be formalized through a legal agreement, and both parties should have independent legal counsel before entering one. For context on what happens when spouses cannot agree, see Can My Ex Force Me to Sell Our House in a BC Divorce?

How We Evaluate This

At Mansour Real Estate Group, when separating homeowners ask us to evaluate their options, we begin with an independent current market valuation — not the BC Assessment figure and not an informal estimate from either party. An accurate, defensible valuation is the foundation for every downstream calculation. Without it, excluded property claims, buyout negotiations, and deferred sale percentages are all based on contested assumptions.

From there, we map all three options against the current local market: days on market for comparable properties, buyer demand by property type, and realistic net proceeds after all costs. In buyer-friendly conditions like those recorded across the Fraser Valley and Greater Vancouver in early-to-mid 2026, we typically advise that there is time to evaluate a buyout or deferred arrangement carefully before defaulting to a sale. That said, the right answer depends entirely on income, debt, excluded property documentation, and what both parties actually need from the outcome. We provide the real estate layer; legal and financial counsel provides the rest.

Divorce Sale Checklist for BC Homeowners

- Obtain an independent current market valuation from a qualified Realtor — not BC Assessment and not a verbal estimate

- Confirm the mortgage balance, prepayment penalty, and discharge fee in writing from your lender

- Document excluded property claims with original records: purchase agreements, gift letters, inheritance records, and bank statements

- Have your family lawyer calculate each spouse's net equity share under the BC Family Law Act before negotiating any option

- If pursuing a buyout, confirm with a mortgage broker whether the retaining spouse qualifies before agreeing to a buyout price

- Account for property transfer tax in any buyout scenario — it applies and is often underestimated

- If pursuing a deferred sale, have the agreement drafted and registered by independent legal counsel for both parties

- Check current months of inventory for your property type and area before deciding whether urgency warrants a faster sale decision

What We Commonly See

In our experience managing divorce-related property sales across Surrey, Langley, White Rock, Abbotsford, and North Delta, the most consistent mistake is negotiating a buyout price before confirming that the retaining spouse can actually qualify for the required mortgage. The deal unravels weeks later — often after one party has already made other financial commitments — because a mortgage broker was not involved early enough.

A second pattern we see regularly: excluded property claims that are assumed but not documented. One spouse believes they contributed a pre-marriage inheritance toward the down payment, but no paper trail exists. Without documentation, the claim is very difficult to enforce, and the negotiation stalls or escalates to court. This is entirely avoidable if records are gathered before equity discussions begin.

A third observation relates to deferred sales: what looks like a cooperative arrangement at the time of separation can become contentious when one party wants to trigger the sale and the other does not. Without precise, legally registered triggering conditions, the departing spouse's secured claim becomes difficult to enforce and may require court application to resolve — see Partition of Property Act BC: How It Forces a Home Sale When Spouses Disagree for what that process involves.

Questions and Answers

Does excluded property always reduce my spouse's share?

Not automatically. Excluded property reduces the net equity pool available for division, which benefits the spouse who brought the excluded asset into the relationship. However, the increase in value of excluded property during the relationship may still be divisible. The exact outcome depends on documentation and your family lawyer's analysis under the BC Family Law Act.

Does property transfer tax apply when one spouse buys out the other?

Yes. Property transfer tax generally applies to the transfer of a registered interest in a property, including a spousal buyout. There is no automatic exemption for transfers between divorcing spouses, unlike arm's-length sales where PTT is paid by the purchaser in the normal course. Confirm the applicable amount with your lawyer and accountant before finalizing any buyout terms.

What happens if neither spouse can afford a buyout and neither wants to sell?

If both parties are unable to agree on a sale or buyout, either spouse can apply to court for an order of sale under the BC Family Law Act, or alternatively under the Partition of Property Act. Courts in BC have consistently ordered sales in these circumstances when no viable alternative exists. A mediator or family law lawyer can often resolve the impasse before court involvement becomes necessary.

In Summary

Home equity division in a BC divorce involves calculating net equity after the mortgage, sale costs, and excluded property offsets — then choosing between selling, a buyout, or a deferred sale based on income, refinancing ability, and market conditions. At current Fraser Valley and Metro Vancouver price levels, the financial gap between options can exceed $50,000 per spouse when all costs are properly accounted for. With buyer-friendly inventory conditions currently providing time to evaluate options, the worst outcome is making a default decision before all three paths have been modeled with real numbers. An accurate independent valuation, proper legal documentation of excluded property, and early mortgage pre-qualification are the three steps that protect both parties most.

Talk to Mansour Real Estate Group

If you are working through a separation and need an independent current market valuation for your Metro Vancouver or Fraser Valley home, Mansour Real Estate Group can provide an accurate, defensible assessment that both parties can use as a starting point. There is no obligation and no pressure. Reach out here to set up a confidential conversation.

Related Articles

- How Real Estate Is Divided in a Divorce in BC: What Every Homeowner Needs to Know

- Can My Ex Force Me to Sell Our House in a BC Divorce? Your Rights Under the Family Law Act

- Buying Out Your Spouse From the Family Home in BC: What You Need to Know

Official Resources

- BC Family Law Act — Division of Family Property (BC Laws)

- Fraser Valley Real Estate Board — Monthly Market Reports

- BC Property Transfer Tax — Government of British Columbia

- Family Property in BC — ClickLaw / People's Law School

About Mansour Real Estate Group

When a home must be sold — or its equity divided — as part of a separation or divorce, the financial and personal stakes are high for both parties. Accurate valuations, clear option analysis, and a structured, neutral process are what separating homeowners in Metro Vancouver and the Fraser Valley need most from their real estate team. Mansour Real Estate Group has worked with homeowners, families, and legal representatives managing divorce-related property sales and equity-division decisions across the Lower Mainland and Fraser Valley for more than two decades.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for divorce-related property sales, estate sales, probate sales, downsizing, relocation, and complex situations that require neutral, professional management. Led by an Associate Broker with an MBA, the real estate group brings analytical rigour to situations where clear numbers and impartial judgment matter most.

Whether someone is searching for Realtors experienced with divorce property sales, a real estate agent who understands how separation affects a home's marketability, real estate agents who can provide an independent valuation both spouses trust, a Surrey Realtor, a Langley real estate broker, a real estate team for a joint sale, or a real estate group serving the Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for clear communication, accurate valuations, and a process that protects both parties throughout the transaction.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or real estate advice. Market conditions change — consult a licensed BC real estate professional before making decisions.