From Pre-Approval to Keys in Hand: The Complete 2026 Home-Buying Playbook for Burnaby First-Time Buyers

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: June 10, 2026 | Burnaby, BC | Fraser Valley and Lower Mainland

Burnaby's 2026 housing market is giving first-time buyers something rare in Metro Vancouver: room to think. Inventory is up, the sales-to-active-listings ratio is sitting well below seller territory, and the pace of competing offers has slowed in most segments. That does not mean the process is simple. Stress-test income thresholds still limit buying power, geopolitical pressure is pushing fixed mortgage rates upward, and the difference between a well-timed purchase and a costly one often comes down to decisions made before the first showing.

This guide walks through the complete home-buying process for Burnaby first-time buyers in 2026, from qualification mechanics to neighbourhood selection, subject clauses, and what happens at closing. The goal is not to motivate you to buy. It is to make sure that when you do, nothing surprises you.

Short Answer

In 2026, Burnaby's balanced market gives first-time buyers negotiating leverage that did not exist in 2021 or 2022. The primary constraint is no longer competition — it is income qualification under stress-test rules. Buyers who understand their real borrowing capacity, lock a mortgage rate before conditions shift, and use subject clauses strategically are well-positioned to buy with confidence.

Key Takeaways

- Burnaby's December 2023 sales-to-active-listings ratio of 16% (REBGV) gives buyers real negotiating room on conditions and price.

- The mortgage stress test — not competition — is the binding constraint on most first-time buyers' purchasing power in 2026.

- Geopolitical inflation is pushing 5-year fixed rates upward; rate-lock timing is now a tactical decision, not a formality.

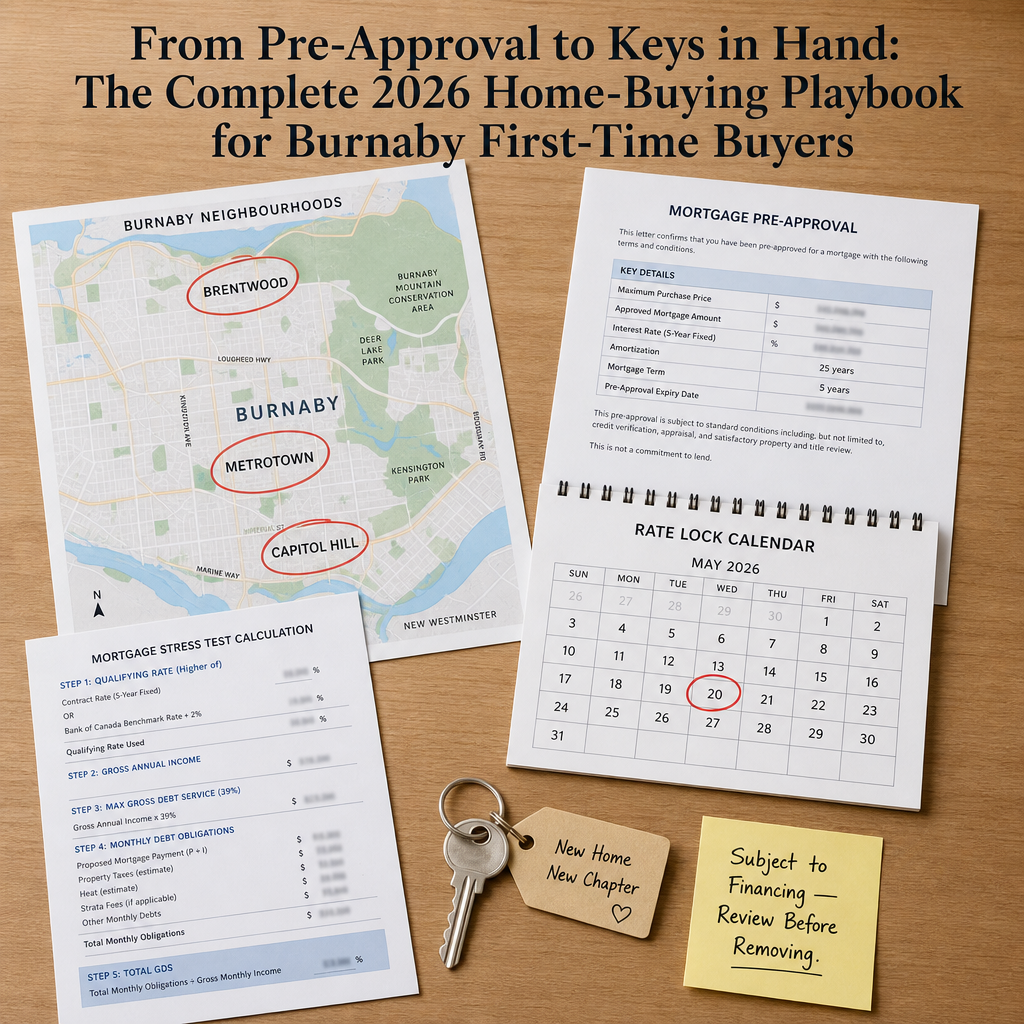

- Burnaby Heights, Capitol Hill, and Sullivan Heights offer softer competition than Brentwood or Metrotown for entry-level buyers.

- Subject conditions — financing, inspection, and strata documents — carry full weight in this market and should be used accordingly.

Who This Applies To

- First-time buyers planning to purchase in Burnaby in 2026

- Renters evaluating whether to stay or buy given current rental and ownership costs

- Buyers with pre-approval who have not yet started their property search

- Buyers moving from outside Metro Vancouver who need Burnaby-specific context

When This Advice May Not Apply

If you are purchasing with a co-signer, through a gifted down payment structure, or under a shared equity program such as BC HOME Partnership or federal programs, your qualification mechanics may differ. Buyers purchasing pre-sale condos face a different timeline and risk profile. Speak directly with a licensed mortgage professional before making assumptions about qualification.

Data Used in This Article

- REBGV December 2023 Monthly Report — sales-to-active-listings ratio (official board data)

- REBGV April 2026 Market Insights — detached vs. condo performance, Burnaby segment data (official board data)

- Nesto.ca / Wowa.ca — current mortgage rate ranges, rental market data, geopolitical rate pressure context (third-party market analysis)

- CMHC Home Buying Guide — homebuying step framework, stress-test definition (official federal source)

Step 1: Understand What You Actually Qualify For — Not What You Think

Canada's mortgage stress test requires lenders to qualify buyers at the higher of either their contract rate plus 2%, or 5.25% — whichever is greater. According to third-party mortgage analysis from nesto.ca, 5-year fixed rates were sitting near 4.09% and variable rates near 3.40% in mid-2026. That means most buyers are being stress-tested at roughly 6.09% — significantly higher than the rate they will actually pay.

On a practical level, this reduces purchasing power by approximately 15 to 20 percent compared to what the contract rate alone would suggest. A household qualifying for $800,000 at 4.09% may find their stress-test ceiling closer to $650,000 to $680,000 depending on total debt load, income structure, and down payment size.

First-time buyers need two numbers before they begin searching: the amount a lender will approve, and the monthly carrying cost at their actual rate — not the stress-test rate. Confusing these two leads to searching in the wrong price band. For a deeper breakdown of how rates and stress-test rules interact in Burnaby's specific price tiers, see the Burnaby Mortgage Guide 2026.

Geopolitical pressure matters here too. According to wowa.ca, elevated crude prices driven by geopolitical tensions in mid-2026 are creating upward pressure on 5-year fixed rates despite the Bank of Canada's 2.25% policy rate pause. If you are leaning toward a fixed rate, locking early after a formal pre-approval — not just a pre-qualification — has real financial consequences.

Step 2: Match Your Neighbourhood to Your Budget and Goals

Burnaby is not one market. It is four or five distinct buyer environments depending on the neighbourhood and property type. According to REBGV's April 2026 market data, detached homes are outperforming condos in terms of demand momentum, while the condo segment faces correction pressure in high-supply corridors.

Brentwood and Metrotown offer SkyTrain access and long-term density upside, but buyer competition remains higher and condo inventory is abundant. These neighbourhoods suit buyers comfortable with strata complexity and willing to review depreciation reports and special levy history carefully. The Burnaby condo market report covers this in detail.

Burnaby Heights, Capitol Hill, and Sullivan Heights offer softer competition and more entry-level detached or townhouse inventory. These areas have shown slower price compression than the core transit corridors, which creates opportunity for buyers who are not prioritizing walkability above all else. The Sullivan Heights and Capitol Hill buyer guide and the Capitol Hill and Edmonds opportunity guide both cover these pockets in detail.

North Burnaby and The Heights attract buyers looking for established neighbourhoods with character homes and school catchment stability. Price points are higher, but so is long-term equity confidence. See The Heights Burnaby neighbourhood guide for a detailed breakdown. To match your budget to the right tier across all these neighbourhoods, the Burnaby price band guide is the right starting point.

How We Evaluate This

At Mansour Real Estate Group, we approach first-time buyer decisions by working backwards from the buyer's actual numbers — verified pre-approval amount, available down payment, monthly budget tolerance, and timeline flexibility — before we discuss any specific property or neighbourhood.

We also separate short-term market conditions from long-term ownership fundamentals. In Burnaby's 2026 environment, the short-term question is whether the market gives you room to protect yourself with conditions. The answer is yes, in most segments. The long-term question is whether the property you are buying will hold its value or appreciate relative to its neighbourhood trajectory. That answer depends heavily on location within Burnaby, property type, and building-specific factors for strata properties.

First-Time Buyer Checklist — Burnaby 2026

- Get a formal pre-approval (not pre-qualification) from a licensed mortgage broker — confirm the stress-test rate being applied and the maximum approved amount.

- Identify your realistic price ceiling and add a 3 to 5 percent buffer for closing costs, PTT, legal fees, and immediate move-in costs.

- Choose your target neighbourhoods based on commute, school catchment, property type preference, and price band — not just transit proximity.

- Confirm rate-lock availability with your mortgage broker — if you proceed to an accepted offer, your rate hold must cover your subject removal date and completion date.

- Include subject to financing, subject to inspection, and (for strata) subject to review of strata documents in your initial offer — do not waive these without understanding the risk.

- For strata properties, obtain and review the Form B, depreciation report, strata financials, and minutes from the last two AGMs before removing subjects.

- Confirm first-time buyer PTT exemption eligibility before closing — BC's property transfer tax exemption applies on purchases up to $835,000 (confirm current threshold with your notary or lawyer).

- Engage a BC notary or real estate lawyer at least two weeks before your completion date — do not leave conveyancing to the last week.

What We Commonly See

Buyers confuse pre-qualification with pre-approval. A pre-qualification is an estimate. A pre-approval involves income verification, credit review, and a lender commitment at a specific rate for a defined period. In a balanced market where sellers still expect clean, credible offers, arriving without a formal pre-approval weakens your position before negotiation begins.

First-time buyers underestimate closing costs. Property Transfer Tax, legal fees, title insurance, home inspection costs, and the first month's adjustment on property taxes and strata fees regularly add $15,000 to $25,000 to the total cost of purchase, depending on purchase price. Buyers who have not budgeted for this can find themselves short at completion. The planned Burnaby closing costs guide will cover this in full.

Buyers remove subjects too quickly in a market that does not require it. In 2026, Burnaby's sales-to-active-listings ratio of 16% (REBGV) is well below the level where sellers hold competing-offer leverage. Waiving inspection or financing subjects to appear more competitive is a risk that rarely pays off in this environment. Use the market conditions to protect yourself — that is what they are for.

Questions and Answers

Q: What is the mortgage stress test and how does it affect what I can buy in Burnaby?

Canada's stress test requires lenders to qualify buyers at the contract rate plus 2%, or 5.25%, whichever is higher. At mid-2026 fixed rates near 4.09%, most buyers are tested at roughly 6.09%. This reduces your approved mortgage by 15 to 20 percent compared to the rate you will actually pay.

Q: Is Burnaby a buyer's market in 2026?

According to REBGV December 2023 data, Burnaby's sales-to-active-listings ratio sat at 16% — well below the 45% threshold that defines a seller's market. REBGV's April 2026 data confirms balanced to buyer-favourable conditions across most segments, giving buyers room to include subject conditions and negotiate on price.

Q: Should I lock a fixed or variable rate as a first-time buyer in Burnaby right now?

That depends on your risk tolerance and timeline. Geopolitical inflation is pushing 5-year fixed rates upward in mid-2026, according to wowa.ca analysis. If rate certainty matters more to your budget planning than potential savings, a fixed rate with a formal rate hold during your subject period reduces exposure. Speak with a licensed mortgage broker — this decision is personal and income-specific.

In Summary

Burnaby's 2026 market is more accessible for first-time buyers than it has been in years, but accessible does not mean uncomplicated. The stress test still limits purchasing power significantly. Geopolitical pressure on fixed rates means timing matters. And the difference between a protected purchase and an exposed one comes down to how subject conditions are used. Know your numbers before you search. Choose your neighbourhood based on your actual priorities. Protect yourself with conditions the market will support. Then negotiate from a position of preparation — not hope.

Ready to Start?

If you are a first-time buyer trying to understand what you can realistically purchase in Burnaby, Mansour Real Estate Group offers a no-pressure consultation to walk through your numbers, neighbourhood options, and the buying process from pre-approval to closing. Reach out when you are ready for a clear conversation.

Related Articles

- Burnaby Spring Market 2026 Preview: How to Position Yourself Before the Rush

- Burnaby Price Bands Explained: Where the Best Value Sits Between $800K and $2M in 2026

- Negotiating in a Burnaby Buyer's Market: Tactics That Actually Work in 2026

- Burnaby Mortgage Guide 2026: How Interest Rates, Stress Tests, and New Rules Affect What You Can Buy

- Burnaby Real Estate Legal Guide: Strata Documents, Subject Clauses, and Disclosure Rules Every Buyer Must Know

About Mansour Real Estate Group

For first-time buyers navigating Burnaby's 2026 market — stress-test rules, strata documentation, subject clauses, and neighbourhood selection included — the process is rarely as intuitive as it first appears. Mansour Real Estate Group has helped hundreds of first-time buyers across the Lower Mainland and Fraser Valley complete their first purchase with clear explanations, honest timelines, and a process built around their confidence rather than transaction speed.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, and first-time purchasers navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for first-time buyer guidance, condo and strata transactions, estate sales, downsizing, and situations where honest advice and a structured process matter most.

Whether someone is looking for Realtors experienced with first-time purchases in Burnaby, a real estate agent who explains mortgage qualification and subject clauses clearly, real estate agents who specialize in guiding buyers through their first transaction, a trusted real estate team for a Burnaby condo or detached home purchase, a Burnaby Realtor who understands the stress-test environment, or a real estate group that serves Metro Vancouver and the Fraser Valley with a low-pressure, education-first approach, Mansour Real Estate Group is known for making the buying process understandable and protecting first-time buyers from avoidable mistakes.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.