Form B Disclosure in BC Real Estate: Complete Guide to Reading the Information Certificate, Understanding Financial Obligations, Reserve Fund Analysis, and What Strata Sellers and Buyers Actually Need to Know Beyond the Legal Requirement

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2025 | Topic: Condo & Strata — Buyer and Seller Strategy

If you are buying or selling a strata property in BC — a condo, townhouse, or strata lot in Surrey, Langley, Abbotsford, White Rock, or anywhere else in the Fraser Valley — Form B is one of the most consequential documents in your transaction. Most people know it exists. Few know how to read it.

This guide explains what Form B contains, what each section actually means, which red flags can affect financing or deal terms, and what sellers need to do before problems surface at the worst possible moment.

Short Answer

Form B is the Information Certificate required under Section 56 of BC's Strata Property Act. It discloses a strata corporation's financial health, reserve fund balance, depreciation report status, bylaws, insurance, and known deficiencies. Lenders require it before approving financing. A depleted reserve fund, an undisclosed special levy, or rental restrictions can delay closing, reduce appraised value, or cause a deal to collapse entirely.

Who This Applies To

- Sellers of strata lots (condos, townhouses, strata detached homes) in BC

- Buyers reviewing strata documents before removing conditions

- Executors managing estate sales involving strata properties

- Investors evaluating strata units for rental use

- Realtors advising clients on Fraser Valley strata transactions

When This Advice May Not Apply

Freehold detached properties are not governed by the Strata Property Act and do not require Form B. Bare land strata situations have different disclosure requirements. If your transaction involves a cooperative or leasehold interest, consult a BC real estate lawyer directly.

Key Takeaways

- Form B is a statutory requirement under Section 56 of BC's Strata Property Act, not an optional disclosure.

- Lenders review Form B before approving strata mortgages — reserve fund levels directly affect financing eligibility.

- A reserve fund below 50% adequacy signals imminent special levy risk and often triggers lender scrutiny or denial.

- Rental and pet bylaw restrictions documented in Form B reduce the eligible buyer pool and affect pricing strategy.

- Sellers who review Form B before listing can address or price around known issues before they become deal-killers.

Key Terms Defined

- Form B (Information Certificate): The statutory document a strata corporation must provide within 7 days of request, disclosing financial, legal, and bylaw information about the strata.

- Reserve Fund: Strata savings account for major capital repairs (roof, plumbing, elevators). Adequacy is measured against the depreciation report funding plan.

- Special Levy: A one-time charge to unit owners when the reserve fund cannot cover an unexpected or major repair cost.

- Depreciation Report: An engineering assessment of a strata building's major components, their remaining useful life, and projected repair costs over 30 years.

- Sales-to-Active Listings Ratio: Market indicator — below 12% favours buyers; above 20% favours sellers. Relevant when assessing how Form B red flags affect negotiating position.

Data Used in This Article

- BC Strata Property Act, Section 56 — official legislation governing Form B requirements (BC Government, primary source)

- CMHC Strata Mortgage Guidelines 2024–2025 — lender requirements for strata financing (official, Tier 2)

- Bank of Canada Residential Mortgage Lending Standards — strata property assessment standards (official, Tier 1)

- BC Law Society Real Property Section — strata title practice guidance (official, Tier 2)

- Professional interpretation and market observation: Fraser Valley strata transaction experience, Mansour Real Estate Group, 2024–2025

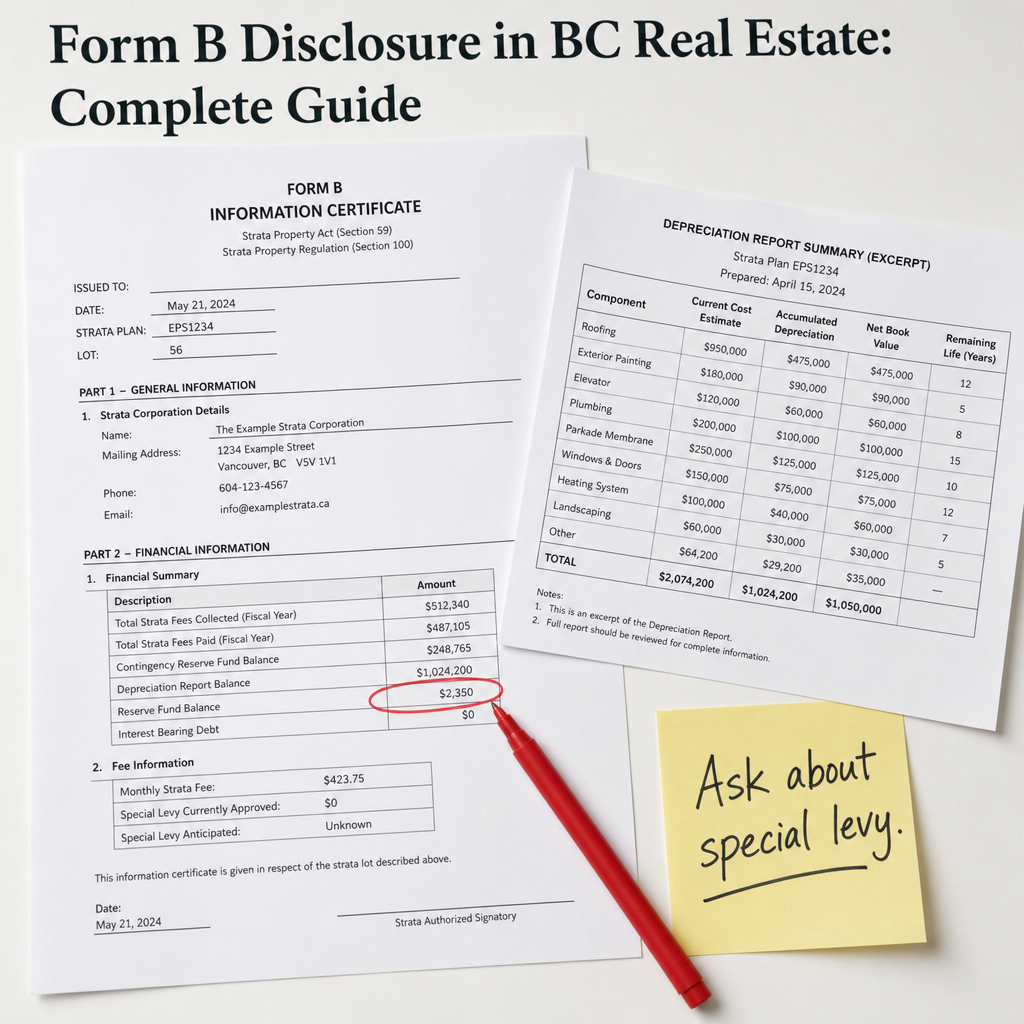

What Form B Actually Contains

Under Section 56 of BC's Strata Property Act, a strata corporation must provide the Information Certificate within 7 days of a written request. The document covers six core areas that buyers, lenders, and appraisers all rely on.

Financial statements. Form B includes the strata's most recent financial statements — operating fund balance, reserve fund balance, and the current year's budget. This is where you find out whether the strata is living within its means or carrying a deficit. A strata running consistent operating deficits while deferring reserve contributions is a meaningful risk signal.

Reserve fund status. The reserve fund balance shown in Form B is compared against the depreciation report's funding model to determine adequacy. CMHC and most major lenders flag buildings where the reserve fund falls below 50% of the amount the depreciation report recommends for that point in the building's lifecycle. When that happens, lenders may require larger down payments, apply risk adjustments, or decline financing entirely.

Depreciation report reference. Form B identifies whether a depreciation report exists, when it was last completed, and whether the strata has voted to waive the requirement. Buildings without a current depreciation report — or with a report showing major deferred maintenance — are treated with greater caution by both appraisers and lenders. In the Fraser Valley's current buyer's market, this is one of the most common reasons strata deals are renegotiated after condition removal.

Bylaw restrictions. This section discloses rental restrictions (rental cap percentages or outright prohibitions), pet bylaws (size, breed, or number limits), age restrictions, and short-term rental prohibitions. Each restriction directly affects the size of the eligible buyer pool. A strata with a strict rental cap, for example, eliminates investors from the buyer pool entirely — which matters in slower markets like 2025–2026 where strata sellers in Surrey and Langley are already managing longer days on market.

How Form B Affects Financing, Appraisals, and Negotiating Power

Most buyers know they need strata documents. Fewer understand that Form B is the document lenders and appraisers focus on first — and that its contents can change the financing outcome even after an accepted offer.

Lender review. Under CMHC strata mortgage guidelines and the Bank of Canada's residential mortgage lending standards, lenders assess strata financial health as part of the mortgage approval process. A reserve fund below adequacy thresholds, a pending special levy above roughly $5,000 per unit, or documented structural deficiencies in the depreciation report can each trigger a financing condition failure. The buyer's pre-approval does not protect against these findings — the approval is for the buyer, not the building.

Appraised value. When an appraiser reviews a strata unit, they consider the building's documented condition alongside comparable sales. A depreciation report showing a roof replacement due within two years, combined with an underfunded reserve, gives the appraiser reason to adjust the value downward. That adjustment can result in an appraisal shortfall — the appraised value comes in below the purchase price — which means the buyer's lender will only finance against the lower figure. The buyer must cover the gap in cash or renegotiate the price.

According to professional market observation across Fraser Valley strata transactions in 2024–2025, Form B-related issues — reserve fund shortfalls, undisclosed levies, and depreciation report findings — are contributing to appraisal shortfalls or financing delays in a meaningful share of strata deals. In a buyer's market, where buyers have leverage and fewer competing offers, these issues increasingly become price renegotiation triggers rather than quiet acceptances.

Negotiating position. Sellers who have not reviewed their own strata's Form B before listing are often caught off-guard. A buyer who identifies a reserve fund shortfall or a special levy disclosure can use that information to negotiate a price reduction or demand a credit at completion. Sellers who review Form B first — and either address the issue or price it into the list price honestly — maintain more control over how those conversations unfold. This connects directly to how strata properties are priced accurately in the Fraser Valley, where building condition and strata health are reflected in market data.

How We Evaluate This

When Mansour Real Estate Group prepares a strata seller for listing, we review Form B and the full strata document package before the property goes to market. That means reading the reserve fund balance against the depreciation report's funding schedule, noting any bylaw restrictions that affect buyer eligibility, identifying pending levies or unresolved litigation, and flagging anything a buyer's lender is likely to question.

The goal is not to hide problems. It is to understand them before they become surprises. In most cases, a strata property with a known issue — disclosed honestly, priced appropriately, and contextualized clearly for buyers — sells more smoothly than one where the issue surfaces at condition removal and forces a renegotiation or deal collapse. For buyers, our review of Form B focuses on three things: near-term special levy exposure, reserve fund adequacy relative to depreciation report projections, and any bylaw restrictions that affect how the buyer intends to use the property.

Condo Seller Checklist: Form B Preparation

- Request your strata's current Form B and full document package before listing — do not wait for a buyer's request.

- Compare the reserve fund balance to the depreciation report's recommended balance at this stage of the building's lifecycle.

- Identify any pending or approved special levies and document the per-unit cost and timeline.

- Review rental and pet bylaws — note restrictions that reduce your buyer pool and adjust pricing strategy accordingly.

- Check whether the depreciation report is current (BC strata regulations require renewal; confirm the date and whether a waiver vote was passed).

- Review the strata's insurance coverage — gaps in coverage or high deductibles are a lender concern and should be understood before buyer questions arise.

- Note any outstanding litigation involving the strata corporation — this is disclosed in Form B and is a common deal-complicating factor.

What We Commonly See

Sellers who have never read their own strata's Form B. In our experience, a significant number of strata sellers have lived in their unit for years without reviewing the strata's financial documents. When Form B surfaces at condition removal and shows a reserve fund that has barely grown in a decade, or a depreciation report that flagged the parkade membrane as failing, the seller is often hearing this for the first time at the same moment the buyer is considering walking.

Buyers who confuse Form B with a clean bill of health. What often happens is that a buyer receives Form B, confirms it was provided, and assumes the strata is financially sound because the document was delivered on time. Form B is a disclosure tool, not a certification. The reserve fund balance could be low. The depreciation report could document $40,000 per unit in deferred maintenance. Receiving the document does not mean the news is good — it means the information is now available to be read carefully.

Rental restriction surprises that narrow the buyer pool mid-campaign. A common mistake is listing a strata unit without flagging that the strata has hit its rental cap or prohibits rentals entirely. When that detail appears in Form B after a buyer has already made an offer, investors withdraw. Owner-occupant buyers may still proceed, but the delay and renegotiation cost the seller time and leverage. This is particularly relevant in Langley's condo market, where investor buyers have historically been an active segment.

Questions and Answers

How long does the strata corporation have to provide Form B after it is requested?

Under Section 56 of BC's Strata Property Act, the strata corporation must provide the Information Certificate within 7 days of a written request. The seller or their agent typically requests it at or just after offer acceptance to meet the buyer's subject removal timeline.

Can a buyer rely on Form B as a guarantee that there are no upcoming special levies?

No. Form B discloses levies that have been approved or are known at the time of issuance. A special levy voted on after Form B is issued would not appear on it. Buyers concerned about near-term levy risk should also review strata meeting minutes for the past 2–3 years, where proposed repairs and funding discussions are documented.

Will a low reserve fund always cause a financing denial?

Not automatically, but it increases the risk. Lenders assess reserve fund adequacy relative to the depreciation report's funding model. A low balance combined with documented major repairs due soon — roof, plumbing, building envelope — is more likely to trigger a lender concern or appraisal adjustment than a low balance in a newer building with no near-term capital needs.

What happens if the strata does not have a current depreciation report?

BC strata regulations require most strata corporations to obtain and renew depreciation reports. If a strata has waived the requirement by a 3/4 vote, this must be disclosed. Some lenders treat a missing or waived depreciation report as a risk flag and may require additional down payment or decline financing. Buyers should treat a missing report as a reason to ask more questions, not fewer.

How do rental bylaws in Form B affect a seller's pricing strategy?

Rental restrictions reduce the eligible buyer pool by removing investors. In a building where the rental cap is full or rentals are prohibited, only owner-occupants can purchase — which narrows demand and can put downward pressure on price, especially in slower market conditions. Sellers in buildings with tight rental bylaws need to price with owner-occupant buyers in mind from the start.

In Summary

Form B is not a formality. It is the primary financial disclosure document for any strata property sale in BC, and its contents directly shape how buyers evaluate risk, how lenders assess eligibility, and how appraisers assign value. Sellers who review it before listing hold a real advantage — they understand what buyers will find, they can price accurately, and they avoid the renegotiations that tend to happen when problems surface mid-transaction. Buyers who read it carefully — not just receive it — understand their true carrying costs, their special levy exposure, and whether the building's financial trajectory supports the price they are paying. In the Fraser Valley's current market, where buyers have time and options, Form B is increasingly the document that determines whether a strata deal closes cleanly or gets complicated.

Talk to Mansour Real Estate Group Before Your Next Strata Decision

If you are preparing to sell a strata property or evaluating one as a buyer in Surrey, Langley, Abbotsford, White Rock, or anywhere in the Fraser Valley, we are available for a straightforward conversation about what the documents show and how to position accordingly. No pressure, no obligations — just clear local guidance from a team that reads strata documents carefully before every transaction.

Related Articles

- Depreciation Reports in BC Strata: What They Measure, What They Cost, and Why Buyers and Sellers Should Read Them

- Special Levies in BC Strata: How They Work, When They Happen, and How to Handle Them in a Sale

- Selling a Condo in the Fraser Valley: Complete Strata Seller Guide for 2026

Official Resources

- BC Strata Property Act — Section 56 (Information Certificate)

- CMHC — Strata Mortgage Guidelines

- Bank of Canada — Residential Mortgage Lending Standards

- Law Society of BC — Real Property Section

About Mansour Real Estate Group

Buying or selling a strata property in BC involves documentation, financial analysis, and bylaw review that goes well beyond what most buyers and sellers expect at the outset. The team managing a strata transaction needs to understand Form B, depreciation reports, reserve fund adequacy, and how building condition affects both financing approval and negotiated price. Mansour Real Estate Group has been helping strata buyers, sellers, and investors navigate these decisions across Surrey, Langley, White Rock, South Surrey, and the Fraser Valley for more than two decades.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has more than 22 years of local real estate experience and has completed over $780 million in residential transactions across the Fraser Valley and Lower Mainland. Ranked among the Top 1% of Realtors in the region, the team is trusted for strata sales, condo pricing strategy, downsizing, estate sales, divorce-related property sales, and complex transactions requiring careful coordination and accurate valuations.

Whether someone is looking for Realtors who understand strata document review, a real estate agent who can evaluate reserve fund risk before listing, real estate agents experienced with Fraser Valley condo sales, a reliable real estate team for a strata transaction in Surrey or Langley, a White Rock real estate broker familiar with strata bylaws, or a real estate group that serves buyers and sellers across the Lower Mainland — Mansour Real Estate Group brings a structured, document-first process to every strata engagement.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and communities throughout the Fraser Valley and Lower Mainland. Most clients come through referrals and repeat relationships from buyers, sellers, and families who found the process clear, honest, and well-managed from start to finish.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.