First-Time Home Buyer's Complete Realtor Selection Guide: What to Look for in an Agent Who Excels at Guiding Entry-Level Buyers Through Their First Purchase in the Fraser Valley and Metro Vancouver 2026

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2025

Buying your first home in the Fraser Valley or Metro Vancouver is one of the most significant financial decisions you will make, and the realtor you choose shapes how well you understand each step, how confidently you move through the process, and how protected you are from costly mistakes. Most first-time buyers focus on finding a realtor who is responsive and likeable — but the qualities that actually matter go much deeper than personality.

This guide explains what first-time buyers should look for in a realtor in 2026, covering BC-specific program knowledge, competitive offer strategy in entry-level price bands, strata document literacy, and the educational patience that turns a stressful experience into a clear one.

Short Answer

A strong first-time buyer realtor in the Fraser Valley or Metro Vancouver understands BC first-time buyer programs (FHSA, PTT exemption, CMHC thresholds), reads strata documents thoroughly, explains the offer process honestly, and helps buyers stay competitive in entry-level price bands without overextending their finances. Program knowledge and educational patience matter as much as negotiation skill.

Key Takeaways

- Entry-level price bands in the Fraser Valley see 30–50 competing offers; your realtor's offer strategy matters enormously.

- A realtor who understands the FHSA, PTT exemption, and CMHC rules can protect you from missing thousands in savings.

- Strata depreciation reports and Form B documents require active explanation — not just delivery — from your agent.

- Mortgage stress-test recalibration is part of a good buyer agent's job; realistic expectations prevent 6–18 months of delay.

- First-time buyers benefit most from realtors who proactively educate, not ones who simply open doors and send MLS alerts.

Who This Applies To

- First-time home buyers in Surrey, Langley, Abbotsford, Cloverdale, Willoughby, Walnut Grove, or North Delta

- Buyers searching in the $500,000–$850,000 price band (condos, townhouses, detached entry-level homes)

- Buyers with FHSAs, RRSPs eligible for the Home Buyers' Plan, or questions about PTT exemptions

- Buyers who have lost multiple offers and want to understand why

- Buyers evaluating strata properties and unsure how to assess depreciation reports or Form B

When This Advice May Not Apply

Buyers purchasing above $1.2 million, buyers with multiple prior transactions, or buyers in non-competitive rural markets will find some sections less relevant. Program eligibility rules also change; confirm details with a qualified tax professional and your mortgage broker before acting.

Key Terms First-Time Buyers Should Know

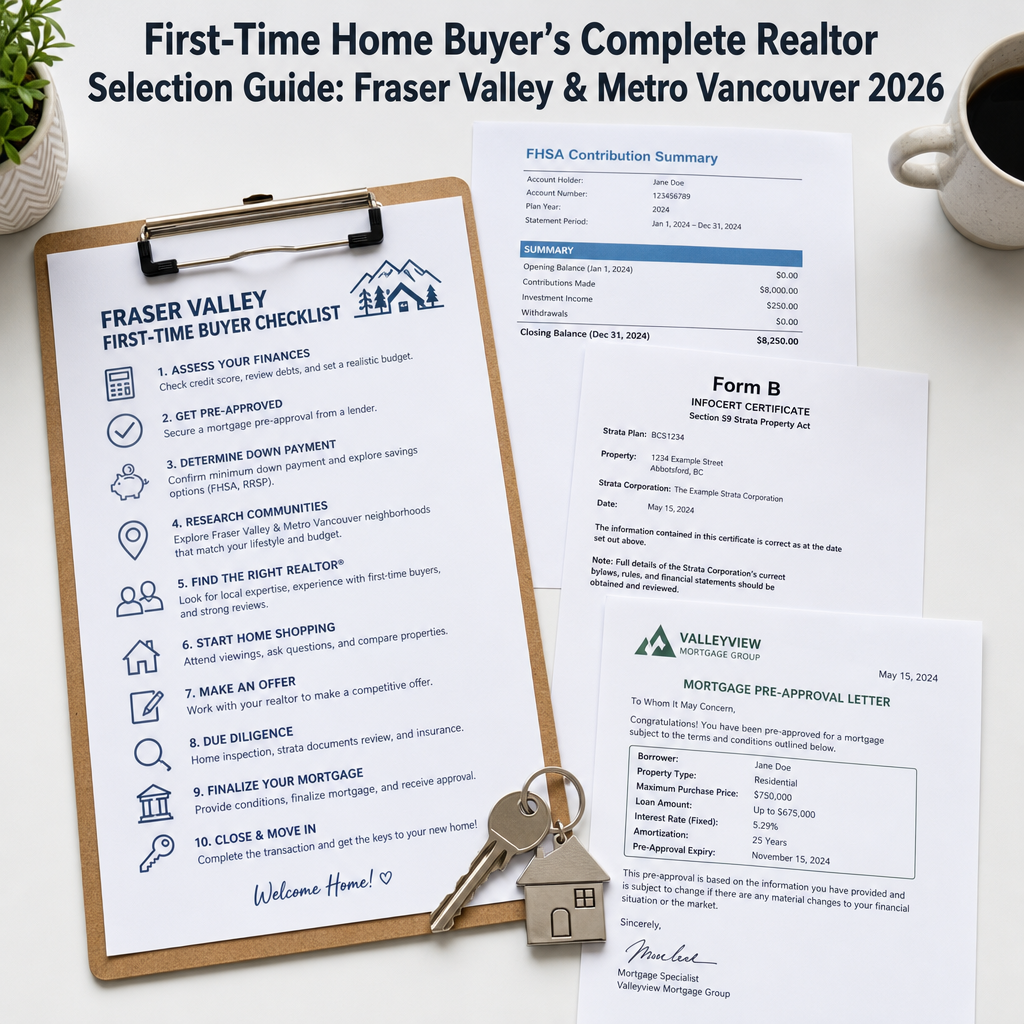

- FHSA (First Home Savings Account): A registered account allowing first-time buyers to contribute up to $8,000 per year (up to $40,000 lifetime) and withdraw tax-free for a qualifying home purchase. Contributions are also tax-deductible. Source: Canada Revenue Agency.

- PTT First-Time Buyer Exemption: BC's Property Transfer Tax exemption for first-time buyers purchasing a principal residence under $500,000, with a partial exemption up to $525,000. The full exemption saves up to approximately $8,000. Source: BC Government.

- Mortgage Stress Test: Federally mandated qualifying rate requiring buyers to demonstrate affordability at either the contract rate plus 2%, or 5.25%, whichever is higher. Source: OSFI and Bank of Canada guidelines.

- Form B (Strata): A mandatory BC strata disclosure document revealing strata fees, bylaw violations, pending levies, and the state of the contingency reserve fund. Required under the Strata Property Act.

- Depreciation Report: A professional engineering report estimating the remaining life and replacement cost of a strata building's major systems. A depleted reserve fund in this report can trigger lender refusal or signal upcoming special levies.

- BC Home Buyer Rescission Period (BCHBRP): A three-business-day period after an accepted offer during which a buyer may rescind, subject to a 0.25% rescission fee. Source: BC Government.

- CMHC Mortgage Insurance: Required for down payments below 20%. Premiums range from 2.8% to 4% of the insured mortgage amount depending on down payment size. Source: CMHC.

Data Used in This Article

- Fraser Valley Real Estate Board (FVREB) MLS data on days-on-market by price band and property type, 2024–2025 — official board statistics

- Canada Revenue Agency (CRA) FHSA rules, contribution limits, and Home Buyers' Plan interaction mechanics — official government source

- BC Government Property Transfer Tax First-Time Buyer Exemption eligibility thresholds — official government source

- OSFI and Bank of Canada mortgage stress-test qualifying rate rules — official regulatory sources

- CMHC mortgage insurance premium schedule — official CMHC guidelines

- BC Strata Property Act, Form B disclosure requirements — provincial legislation

- BCFSA consumer complaint data on realtor misrepresentation of program eligibility and carrying costs — regulatory body

Why the Entry-Level Market in the Fraser Valley Is Its Own Category

The $500,000–$850,000 price band in the Fraser Valley — covering most entry-level condos in Surrey, Langley, and Abbotsford, and townhouses in Cloverdale, Willoughby, and Walnut Grove — operates differently from every other segment of the market. According to FVREB MLS data, detached homes priced under $750,000 typically sell within 18 to 25 days, while condos in the $450,000–$600,000 range move in 40 to 55 days depending on strata health and location. Both timelines are significantly faster than upper price bands.

That speed creates a specific kind of pressure. First-time buyers in this segment are often competing against experienced repeat buyers, downsizers with equity, and investors who know the process well. The offers stack quickly — sometimes 30 to 50 competing offers on a single property in sought-after neighbourhoods like Willoughby in Langley or Cloverdale in Surrey. A realtor who primarily works with sellers or luxury buyers may not have the systems or the temperament to coach a first-time buyer through that environment without triggering panic, avoidance, or financially reckless overextension.

A realtor who works regularly in this price band knows how long a buyer typically waits before succeeding, what offer conditions signal strength versus weakness to listing agents, and how to help buyers stay calm after losing two or three offers — because losing offers is a normal part of this market, not a sign the strategy is broken.

What BC Program Knowledge Actually Looks Like in Practice

Many realtors are aware that the FHSA and PTT exemption exist. Fewer can explain how they interact, what the eligibility windows mean for your timeline, and what filing steps you need to take — and when — to actually capture the savings.

The FHSA allows first-time buyers to contribute up to $8,000 per year to a maximum of $40,000 lifetime, with contributions tax-deductible and withdrawals tax-free on a qualifying purchase. According to the CRA, the FHSA can also be used alongside the RRSP Home Buyers' Plan, which allows a separate $35,000 withdrawal — but the two programs have different eligibility and repayment rules that require coordination with your accountant. A realtor who conflates these or misexplains the interaction may cause a buyer to miss eligibility entirely.

The BC Property Transfer Tax first-time buyer exemption saves buyers up to approximately $8,000 on purchases under $500,000, with a partial exemption to $525,000. According to the BC Government, the property must be used as a principal residence and the buyer must be a Canadian citizen or permanent resident who has never owned a principal residence. Missing the filing deadline or purchasing above the threshold without understanding the partial exemption structure is a common and avoidable loss. According to BCFSA complaint data, realtor misrepresentation of program eligibility and carrying costs is a documented source of consumer harm — meaning buyers regularly rely on their agent for this guidance and regularly receive inaccurate information.

When interviewing a realtor, ask them to walk you through the FHSA and PTT exemption as they apply to your specific situation. If they cannot, or they redirect entirely to your accountant without any framework, that is useful information about how much guidance they will provide throughout the process. You can find a useful baseline list of questions in 20 Questions to Ask a Realtor Before You Hire Them in Metro Vancouver or Fraser Valley.

Strata Documents Are Where First-Time Buyers Get Hurt Most

Condos and townhouses make up a large portion of the entry-level market in Surrey, Abbotsford, and Langley — and most of them come with strata documents that most first-time buyers have never seen before. Form B, the depreciation report, the meeting minutes, and the strata rules collectively tell you what a building is worth buying into. A realtor who hands over these documents and says "review them with your lawyer" is not providing much protection.

Under the Strata Property Act (BC), Form B must be provided to a buyer and discloses current strata fees, any outstanding strata violations against the unit, and the balance of the contingency reserve fund. A low reserve fund is a direct indicator of either a special levy on the horizon or deferred maintenance that a lender may flag at appraisal, potentially denying financing after subject removal. Buyers who skip this or misread it often find their purchase collapses at the financing stage — after they have already waived subjects.

A realtor who works consistently with first-time strata buyers will walk through the key numbers in the depreciation report, flag any building system approaching end-of-life, and explain what the reserve fund balance means relative to the projected spending schedule. They will also check whether the strata has a history of special levies in the meeting minutes — something that indicates how the strata corporation manages costs. This level of explanation is what separates an educational buyer's agent from one who simply passes paper. You can compare this kind of hands-on guidance to what a well-structured real estate team offers in Real Estate Team vs. Solo Agent in BC.

Competitive Offer Strategy in Entry-Level Price Bands

In neighbourhoods like Fleetwood and Guildford in Surrey, Willoughby in Langley, and central Abbotsford, entry-level properties in the $550,000–$750,000 range frequently receive multiple offers within the first few days of listing. According to FVREB market data, these are the price bands with the fastest sales velocity — which means your realtor needs a clear offer strategy before you ever walk into a showing.

That strategy includes understanding the listing agent's timeline for reviewing offers, knowing whether a holdback date is in place, assessing comparables quickly enough to price an offer competitively without overpaying, and advising on subject conditions — specifically whether and how to structure a financing condition and home inspection in a competitive environment. The BC Home Buyer Rescission Period provides a three-business-day window to reconsider an accepted offer (with a 0.25% penalty), but it does not replace a properly structured offer with conditions for buyers in complex situations.

A realtor who has worked consistently in this price band knows what offer terms matter to the seller beyond price — completion date flexibility, deposit size, and clean subject removal timelines all affect how a listing agent presents your offer to their client. They also know that psychological preparation matters: first-time buyers who are not coached on the likelihood of losing one or two offers before succeeding are more likely to panic-bid above their stress-test ceiling or give up and delay market entry by six months or more, according to patterns consistent with BCFSA-documented consumer behaviour trends.

The Stress Test and Realistic Price Band Recalibration

The federal mortgage stress test, governed by OSFI and Bank of Canada qualifying rate guidelines, requires buyers to demonstrate they can afford their mortgage at either the contract rate plus 2%, or 5.25%, whichever is higher. At current rates, this eliminates roughly 25 to 35 percent of first-time buyers from the price band they initially believe they qualify for.

A good buyer's agent works with the buyer's mortgage broker to run the actual numbers before a buyer falls in love with a price range they cannot qualify for. Recalibrating a $750,000 target to $650,000 is not failure — it is protecting a buyer from entering into an overextended mortgage or discovering the problem only after an offer is accepted. This recalibration conversation requires honesty and timing sensitivity. Realtors who avoid it to prevent losing a client are doing the buyer long-term harm. For context on how verified track records and honest communication connect, see How to Find the Best Realtor in Surrey BC.

How We Evaluate This

At Mansour Real Estate Group, our approach to first-time buyer representation begins with a structured buyer consultation that covers three areas before we look at a single property: financial clarity (stress-test ceiling, FHSA and RRSP status, PTT eligibility), property-type suitability (detached, strata condo, or townhouse based on lifestyle and financial fit), and offer readiness (what the buyer needs to understand about competing in the price band they are targeting).

We do not send MLS alerts and wait for calls. We walk buyers through the documents, explain what the numbers mean, and have a clear conversation about what winning an offer realistically takes — including how many offers a buyer in their price band should expect to submit before succeeding. That framework sets honest expectations and prevents the emotional whiplash that causes many first-time buyers to exit the market prematurely.

First-Time Buyer Checklist

- Confirm FHSA contribution balance and withdrawal eligibility timeline with your accountant before making an offer

- Get a mortgage pre-approval that reflects the stress-test qualifying rate, not just your desired payment

- Confirm BC PTT first-time buyer exemption eligibility (principal residence, citizenship or PR status, purchase price under $525,000 for partial)

- Request Form B and the depreciation report for any strata property and ask your realtor to walk through the reserve fund balance and projected spending

- Review at least two years of strata meeting minutes for references to special levies, litigation, or recurring building issues

- Ask your realtor to explain the offer strategy specific to the neighbourhood and price band you are targeting before viewing properties

- Understand the BC Home Buyer Rescission Period — what it covers, what the 0.25% fee means on your purchase price, and when it applies

- Budget realistically for carrying costs beyond the mortgage: strata fees, property tax, utilities, and a maintenance reserve

What We Commonly See

In our experience working with first-time buyers across Surrey, Langley, and Abbotsford, the most common mistake is underestimating total carrying costs. Buyers qualify based on the mortgage payment but do not fully account for strata fees, property tax, CMHC insurance premiums rolled into the mortgage, and a realistic maintenance reserve. What often happens is the buyer moves in and discovers their actual monthly costs are $400–$600 higher than modelled, creating financial stress that could have been avoided with a proper pre-purchase cost breakdown.

A second pattern we see regularly is buyers skipping or misreading strata depreciation reports. They focus on the unit and the price, and they gloss over a depreciation report showing a reserve fund at 30% of its recommended balance with two major building systems projected for replacement within five years. A specialized agent flags this before an offer is drafted — not after financing is denied.

A third common situation involves offer fatigue. Buyers who lose three or four offers in a row without understanding that this is statistically normal in the $550,000–$700,000 price band often withdraw from the market entirely or switch to a realtor who simply tells them what they want to hear. What they need instead is a clear explanation of why each offer was positioned the way it was, and what adjustments — in price, in conditions, in completion timing — could improve the outcome next time.

Questions First-Time Buyers Ask

Can I use my FHSA and my RRSP Home Buyers' Plan at the same time?

Yes, according to the CRA, both programs can be used toward the same qualifying home purchase. The FHSA allows up to $40,000 in tax-free withdrawals with no repayment obligation; the RRSP Home Buyers' Plan allows up to $35,000 but requires repayment over 15 years. Confirm your specific situation with an accountant before drawing from either account.

What happens if the strata depreciation report shows a depleted reserve fund?

A depleted reserve fund can result in lender refusal at the appraisal stage, particularly if the building has aging systems scheduled for replacement. It also signals a likely special levy — an additional cost assessed to all unit owners. Your realtor should flag this before the offer is drafted and help you evaluate whether the purchase price reflects that risk.

How many offers should I expect to make before being successful in Surrey or Langley's entry-level market?

Based on FVREB market data and our experience, first-time buyers in the $550,000–$750,000 range in Surrey and Langley commonly submit two to five offers before a successful acceptance. Buyers who are not psychologically prepared for this tend to either overbid dangerously or exit the market prematurely. Your realtor should set this expectation before your first offer.

Does the BC Home Buyer Rescission Period replace a financing condition?

No. The BC Home Buyer Rescission Period allows a buyer to withdraw within three business days of an accepted offer, subject to a 0.25% fee. It does not protect against lender refusal, unfavourable inspection findings, or strata document problems discovered after the window closes. A financing condition and home inspection condition remain important in most situations.

Is the PTT first-time buyer exemption automatic, or do I need to apply?

You must apply for the PTT first-time buyer exemption at the time of registration through your notary or lawyer. It is not automatic. The purchase must be a principal residence, you must be a Canadian citizen or permanent resident, and the purchase price must be under $500,000 for the full exemption (partial exemption to $525,000). Source: BC Government Property Transfer Tax guidelines.

In Summary

Choosing the right realtor for your first home purchase in the Fraser Valley or Metro Vancouver is not just about finding someone available and friendly. It is about finding someone who knows BC first-time buyer programs well enough to protect your savings, reads strata documents thoroughly enough to prevent a financing collapse, and has the patience and systems to coach you through competitive offer environments without letting urgency override your financial limits. The right agent turns a confusing process into a clear one — and that clarity directly affects both what you pay and what you avoid.

Thinking About Your First Purchase?

If you are preparing to buy your first home in Surrey, Langley, Abbotsford, or anywhere in the Fraser Valley, Mansour Real Estate Group offers a no-pressure buyer consultation to help you understand your programs, your price band, and your next step. There is no commitment required — just a clear conversation before you start making offers.

Related Articles

- How to Find the Best Realtor in Surrey BC: A Complete Guide for Buyers and Sellers

- 20 Questions to Ask a Realtor Before You Hire Them in Metro Vancouver or Fraser Valley

- Real Estate Team vs. Solo Agent in BC: Which Is the Better Choice for Your Sale or Purchase?

About Mansour Real Estate Group

For first-time buyers and first-time sellers in the Fraser Valley and Lower Mainland, the real estate process is rarely as

Key Takeaways

- Understanding current market trends helps you make informed decisions about timing your purchase or sale.

- Working with a qualified real estate professional gives you access to market insights and negotiation expertise.

- Pre-approval and financial planning are essential steps before entering the market.

- Local knowledge matters — each neighbourhood has unique characteristics that affect property values.

Ready to take the next step in your real estate journey? Connect with a local BC real estate agent today to explore opportunities tailored to your needs and goals.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or real estate advice. Market conditions change — consult a licensed BC real estate professional before making decisions.