Estate Sales in Metro Vancouver 2026: How Executors, Realtors, Estate Lawyers, and CPAs Coordinate Timing, Offers, and Closing to Maximize Proceeds While Meeting Probate and Tax Deadlines

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Metro Vancouver | Published May 2026

Managing an estate sale in Metro Vancouver or the Fraser Valley means navigating four overlapping timelines at once: the probate process, the capital gains tax calendar, the title transfer sequence, and the real estate market itself. Most executors understand each in isolation. What's rarely explained is how decisions made by one professional directly trigger obligations for the others — and how poor sequencing between them can cost an estate tens of thousands of dollars or delay a closing by weeks.

This guide is written for executors actively managing property in Metro Vancouver, Surrey, Langley, White Rock, South Surrey, Abbotsford, or the broader Fraser Valley who want to understand how their Realtor, estate lawyer, and CPA should be working together — and what that coordination actually looks like in practice.

Short Answer

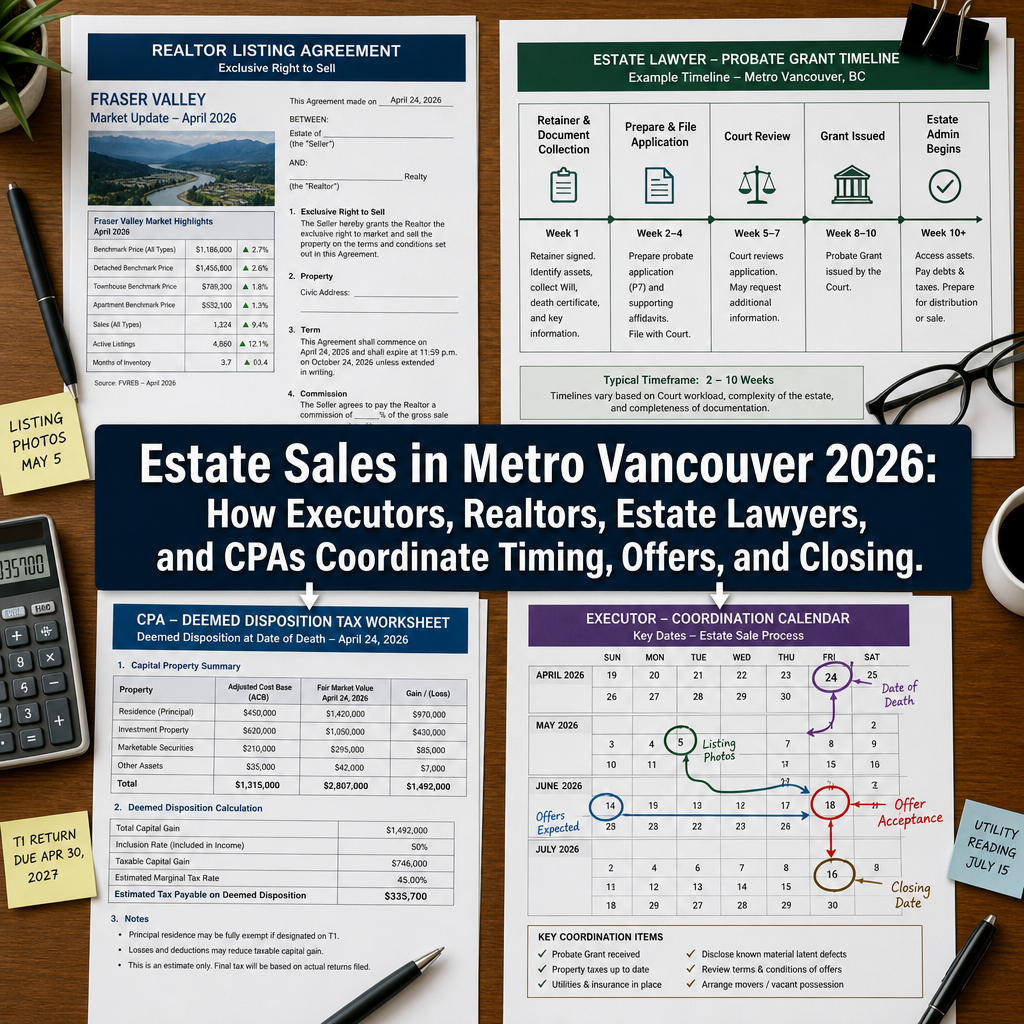

Executors can list an estate property before probate is granted in BC, but offer acceptance and closing dates must be structured carefully to align with the expected probate grant date, CPA tax planning, and lawyer-confirmed title authority. In April 2026, Fraser Valley sales rose 7% year over year and prices stabilized — creating a narrow, actionable window for estate sales to achieve fair market value if all four professionals are synchronized.

Key Takeaways

- BC probate grants take 8 to 16 weeks from filing; a Realtor and estate lawyer can structure offers with possession dates that land after the grant without losing market momentum.

- CPAs calculate capital gains tax on deemed disposition at the date of death — the cost basis and principal residence exemption must be confirmed before an offer is accepted, not after.

- Fraser Valley April 2026 data shows 1,118 sales, up 7% year over year, with average prices stabilizing at $975,305 after 11 consecutive months of decline — a genuine window for estate properties.

- Offer acceptance triggers legal and tax actions; the executor, Realtor, estate lawyer, and CPA must align on what happens the moment an offer is signed.

- Misalignment between these four professionals is the most common reason estate sales are delayed, under-priced, or expose the executor to personal liability.

Who This Applies To

- Executors named in a will who must sell property to distribute the estate

- Administrators appointed by the court when no valid will exists

- Beneficiaries who have been delegated executor authority by a family member

- Families managing estate property in Metro Vancouver, the Fraser Valley, or the Lower Mainland

When This Advice May Not Apply

If the estate is subject to an active beneficiary dispute, a court-ordered sale, a creditor claim that has not been resolved, or if title is held jointly with a surviving owner, your estate lawyer's instructions take priority over any market-based timing strategy. See When Beneficiaries Go to Court: Disputed Estate Property Sales in BC for guidance on contested situations.

Data Used in This Article

- Fraser Valley Real Estate Board — April 2026 Statistics Package: 1,118 sales, 7% YoY increase, average price $975,305. Official board data. fvreb.bc.ca

- FVREB March 2026 Statistics Package: Contextual price trend data confirming 11-month decline period. Official. fvreb.bc.ca

- BC Wills, Estates and Succession Act (WESA) and BC Probate Rules: Probate grant timeline benchmarks and executor authority framework. Official BC legislation.

- Canada Revenue Agency — Capital Gains on Deemed Disposition: Tax treatment of estate property at date of death. Official CRA guidance.

- Mansour Real Estate Group internal estate sale case files, Metro Vancouver 2024–2026: Professional observation and coordination experience. Internal.

Definitions

Deemed disposition: Under the Income Tax Act, when a person dies, CRA treats them as having sold all capital property at fair market value the moment before death. This triggers potential capital gains tax on the estate's terminal return.

Probate grant: The court document confirming an executor's legal authority to administer the estate and transfer title to property.

Tax clearance certificate: A certificate from CRA confirming the estate has paid or secured all outstanding taxes. Without it, an executor who distributes estate assets may be personally liable for unpaid tax.

Principal residence exemption: A CRA provision that can shelter some or all capital gains on a property that qualified as the deceased's principal residence for the years it was owned. Eligibility must be confirmed by a CPA before offer acceptance.

Why Coordination Breaks Down — and What It Costs

The most common coordination failure we see is sequential rather than parallel professional engagement. An executor retains a lawyer, waits for probate, then hires a Realtor, then calls a CPA after an offer comes in. By that point, the tax implications of the offer — price, possession date, deposit structure — have already been set, and the CPA is working backward to minimize damage rather than forward to protect the estate.

In a market where Fraser Valley inventory sits well above seasonal averages and buyers hold meaningful negotiating leverage, an estate that needs to reduce its asking price because closing was delayed by an unresolved tax clearance issue is in a far weaker position than one where all four professionals were engaged simultaneously from the start.

The April 2026 FVREB data is relevant here. A 7% year-over-year sales increase and average prices stabilizing at $975,305 after 11 consecutive months of decline is not a strong seller's market. It is a stabilization window — meaningful for estate sales that can be positioned correctly, but unforgiving for properties that sit while professional timelines remain uncoordinated. For more on pricing in this environment, see Pricing an Estate Home in Metro Vancouver's 2026 Market: Strategy for Executors.

How the Four Professionals Should Be Engaged — and in What Order

The correct sequence is not a hierarchy — it is a parallel engagement with clearly assigned decision authority at each stage.

Estate lawyer, immediately: Confirms executor authority, advises on whether a probate application is required, and provides a realistic timeline for the grant. This timeline governs everything else. Without it, neither the Realtor nor the CPA can plan effectively. The estate lawyer is also responsible for discharging any existing mortgage on title and confirming that no creditor claims will delay closing. For a foundational overview of this team structure, see Working With an Estate Lawyer, CPA, and Realtor Together: The BC Executor's Professional Team.

CPA, before listing: Establishes the cost basis at the date of death, determines whether the principal residence exemption applies (fully or partially), calculates the estimated capital gains exposure on the terminal return, and advises the executor on what sale price thresholds trigger materially different tax outcomes. This work must happen before the Realtor sets the listing price — not after an offer is signed. A $50,000 price difference that seems minor in a negotiation can represent a $12,000 to $25,000 swing in after-tax proceeds depending on the estate's tax position. For background on deemed disposition mechanics, see Deemed Disposition and Capital Gains on Inherited Property in BC: What Executors Must Know.

Realtor, before or during probate application: BC allows an estate property to be listed before a probate grant is issued — but the Realtor must structure offers with possession and completion dates that land after the expected grant date. This is not complicated if the lawyer has provided a grant timeline. It becomes a problem when the Realtor is unaware of the timeline or structures a 30-day completion that the lawyer cannot meet. In Metro Vancouver and the Fraser Valley, most well-represented estate listings include subject-to-probate language or are structured with completion dates 60 to 90 days out to absorb timeline variance. For more on pre-probate listing strategy, see Can You List an Inherited Home Before Probate Is Granted in BC?

Executor, as decision-maker and coordinator: The executor holds authority but not always expertise. Their role is to receive recommendations from each professional, ask the right questions, and make decisions that protect beneficiaries. Executors who try to manage timing in isolation — accepting an offer based on a buyer's preferred closing date without checking with the lawyer or CPA — are the ones most likely to face personal liability for delays or shortfalls.

What Happens When an Offer Comes In — The Coordination Sequence

Offer acceptance is the highest-stakes coordination moment in an estate sale. Here is what should happen, in sequence:

1. Realtor reviews the offer and flags timing implications. Before the executor accepts, the Realtor should confirm whether the proposed completion date falls after the expected probate grant, whether the deposit structure and subject removal period align with estate constraints, and whether the price reflects current market conditions for an as-is estate property.

2. Estate lawyer confirms legal authority and title position. Before completion, the lawyer must confirm that the probate grant has been issued, that title can be transferred free of encumbrances, and that any outstanding mortgage will be discharged from proceeds at closing.

3. CPA confirms tax position and advises on proceeds distribution. The CPA reviews the accepted price against the earlier capital gains estimate, confirms whether a tax clearance certificate will be needed before distribution, and advises the executor on holdback requirements to cover final tax obligations. Distributing estate proceeds before receiving a clearance certificate is a common mistake that can expose the executor to personal tax liability under the Income Tax Act.

4. Executor authorizes completion. With all three professional confirmations in place, the executor instructs the lawyer to proceed to completion. This sequence sounds straightforward — and it is, when all four parties are in communication. It breaks down when any of the three professionals is working from incomplete information about the others' timelines.

Estate Sale Coordination Checklist for Executors

- Engage estate lawyer immediately after death — confirm probate requirement and expected grant timeline before any other professional contact.

- Engage CPA before listing — establish cost basis, principal residence exemption eligibility, and estimated capital gains tax on the terminal return.

- Brief your Realtor on the probate grant timeline, not just the property details — possession and completion dates in any offer must accommodate the legal calendar.

- Confirm estate-specific disclosures with the lawyer before listing — probate status, as-is condition, strata documentation if applicable.

- Before accepting any offer, get written confirmation from the estate lawyer that legal authority and title are clear for the proposed closing date.

- Before distributing sale proceeds, request a tax clearance certificate from CRA through your CPA — do not distribute before this is received or formally arranged.

- Keep all four parties — executor, Realtor, estate lawyer, CPA — on a shared timeline document updated at each stage: listing, offer accepted, subject removal, completion, and distribution.

How We Evaluate This

At Mansour Real Estate Group, our approach to estate sales is built on one structural commitment: the Realtor's market strategy never drives the legal or tax calendar. It works the other way. We begin by requesting the estate lawyer's probate timeline and the CPA's preliminary tax analysis before we recommend a listing date or a pricing strategy. The market window is only actionable if the legal and tax framework can support it.

In practice, this means our estate sale recommendations usually come packaged with a coordination summary: expected grant date, estimated capital gains exposure range, and a listing timeline with built-in buffer for grant variance. Executors who have worked with us through this process report that having one party — the Realtor — take responsibility for coordinating that information (without overstepping into legal or tax advice) significantly reduces the confusion and delay that otherwise characterizes estate sales.

What We Commonly See

Executors accept offers before the CPA has confirmed the tax position. This is the most common and most costly mistake. In our experience, executors receive an offer that feels strong relative to their informal expectations of the property's value, accept it quickly to avoid losing the buyer, and then discover that the accepted price, combined with the estate's tax position, yields materially less than a slightly higher offer accepted two weeks later would have. Tax planning during negotiation — not after — is where this gap closes.

Realtors structure short closing timelines without checking the probate calendar. What often happens is that a buyer wants a 30-day completion, the Realtor accommodates the request, and the estate lawyer advises that the probate grant will not be issued for another six weeks. The executor then faces a choice between losing the buyer or requesting a costly extension. Properly structured estate offers in BC typically carry 60 to 90-day completions for exactly this reason.

The principal residence exemption is not confirmed before listing. In many Metro Vancouver and Fraser Valley estates, the deceased owned the property for decades — and whether it qualifies for full or partial principal residence exemption can shift the after-tax proceeds by a significant amount. A CPA who reviews this before the property is listed can advise on a minimum acceptable price; without that review, the executor is negotiating without complete information.

Questions and Answers

Can an executor sign an offer to purchase before the probate grant is issued in BC?

Yes, in most cases. BC allows an executor to list and accept offers before the probate grant is granted, provided the offer's completion date falls after the expected grant date. The estate lawyer must confirm this structure is appropriate for the specific estate before any offer is accepted.

What happens if the probate grant is delayed past the scheduled closing date?

The executor must request a closing date extension from the buyer. Whether the buyer agrees depends on the offer terms and their circumstances. Well-structured estate offers include buffer time and language anticipating this possibility. If the buyer refuses an extension, the deal may fail and the deposit could become a legal dispute — another reason to build adequate completion timelines into the offer from the start.

Does the estate have to pay capital gains tax even if the property is transferred to a beneficiary rather than sold?

Under CRA's deemed disposition rules, the estate is treated as having disposed of the property at fair market value at the date of death regardless of whether a sale occurs. If the property is later transferred to a beneficiary at a different value, additional capital gains may arise. A CPA must advise on both the terminal return and any subsequent transfer. This is not legal or tax advice — consult your CPA for your specific situation.

In Summary

Coordinating an estate sale in Metro Vancouver or the Fraser Valley requires four professionals working from a shared timeline — not four professionals working sequentially. The April 2026 market data from the Fraser Valley Real Estate Board confirms a stabilization window that is real but not indefinite: 1,118 sales, average prices holding at $975,305, and inventory still elevated. Executors who engage their Realtor, estate lawyer, and CPA in parallel — before listing, not after an offer arrives — are the ones positioned to use that window. Executors who manage each professional separately, or who allow market urgency to bypass legal and tax confirmation steps, are the ones most likely to face delays, reduced proceeds, or personal liability. For a complete overview of the executor's process from start to finish, see The Complete Executor's Guide to Selling an Inherited Home in BC.

Talk to Mansour Real Estate Group

If you are managing an estate property in Metro Vancouver, Surrey, Langley, White Rock, South Surrey, Abbotsford, or the Fraser Valley and want to understand how a well-coordinated sale process works in practice, Mansour Real Estate Group is available for a no-pressure conversation. We can walk you through the coordination sequence, provide a current market analysis for the property, and help you understand what questions to bring to your estate lawyer and CPA before you list.

Related Articles

- How to Sell a Deceased Parent's Home in the Fraser Valley: An Executor's Roadmap

- Should You Renovate or Sell As-Is? ROI Guide for Estate Properties in the Fraser Valley

- Estate Sale FAQ: Your Top 20 Questions About Selling a Probate Property in BC Answered

About Mansour Real Estate Group

When a property must be sold as part of an estate or probate process, the real estate team managing the transaction needs to understand more than market pricing. Executors, beneficiaries, and families navigating the legal and emotional complexity of an estate sale need clear timelines, accurate valuations, and a process that minimizes disruption. Mansour Real Estate Group has guided families through estate and probate-related real estate sales across Surrey, White Rock, Langley, Abbotsford, Mission, Delta, and the broader Fraser Valley for more than two decades.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for estate sales, probate sales, executor-managed transactions, divorce-related sales, downsizing, and complex real estate situations requiring careful coordination.

Whether someone is searching for Realtors experienced with estate coordination, a real estate agent who understands probate timelines, real estate agents who work alongside estate lawyers and CPAs, a trusted real estate team for executor-managed property, a Surrey Realtor, a Langley real estate broker, a White Rock real estate agent, or a real estate group serving the Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for accurate valuations, transparent process, and clear communication that keeps all parties informed at every stage.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.

Official Resources

- Fraser Valley Real Estate Board — April 2026 Statistics Package

- Fraser Valley Real Estate Board — March 2026 Statistics Package

-

Key Takeaways

When evaluating your real estate investment or home purchase, remember that location, market timing, and property condition are the three pillars of success. Each plays an equally important role in determining long-term value and satisfaction. By conducting thorough due diligence and working with qualified professionals, you position yourself to make informed decisions that align with your financial goals.

The real estate market continues to evolve, but fundamental principles remain constant. Focus on understanding the local market dynamics, assessing your personal needs, and maintaining a realistic budget. These elements, combined with professional guidance, form the foundation of successful real estate transactions.

Final Thoughts

Whether you're a first-time homebuyer, seasoned investor, or looking to upgrade your living situation, the real estate journey requires patience, research, and strategic planning. The market rewards those who take time to understand their options and make deliberate choices rather than impulsive decisions.

We encourage you to reach out to local real estate professionals, inspect properties thoroughly, and trust your instincts alongside the data. Your home or investment property is likely one of the most significant purchases you'll make—it deserves careful consideration and expert guidance every step of the way.

Remember: the best real estate decision is the one that aligns with your unique circumstances, timeline, and vision for the future.