Dual Mortgage Carrying Costs and Break-Even Analysis: Why Selling First vs. Buying First Decisions Hinge on True Monthly Overlap Expenses, Not Just Bridge Financing Interest Rates, in the Fraser Valley 2026 Buyer's Market

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2026 | Topic: Seller Strategy

Fraser Valley sellers in 2026 are facing a market where detached homes are sitting 30–50 days and condos 45–70 days before selling at fair market value. That timeline reality changes the math on one of the most consequential decisions in any move: whether to sell your current home first or buy your next one first. This article builds the complete carrying cost model so you can evaluate both paths with real numbers, not assumptions.

Most of the conversation about sequencing focuses on bridge financing interest rates. That misses most of the actual cost. The true break-even includes mortgage interest on both properties, property tax, home insurance, utilities on a vacant or semi-occupied property, and strata fees where applicable. When you add those together over a realistic 60–90 day Fraser Valley holding period, the gap between selling first and buying first is often smaller — and sometimes inverted — compared to what bridge financing rate comparisons suggest.

Short Answer

In Fraser Valley's 2026 buyer's market, selling first typically costs less in total carrying expenses than buying first with bridge financing — but only when days-on-market uncertainty is low and the seller has clear equity. When market timing is uncertain and the new purchase closes before the sale firm date, bridge financing costs of $8,000–$25,000 over 60–90 days are still often lower than running dual full carrying costs of $12,000–$30,000 on two properties simultaneously. The decision hinges on overlap duration, not just rate.

Key Takeaways

- Bridge financing rate is only one component — full dual carrying costs typically run $12,000–$30,000 over a 60–90 day overlap in the Fraser Valley.

- Fraser Valley days-on-market in 2026 averages 30–50 days for detached and 45–70 days for condos, making overlap duration the highest-risk variable.

- Selling first exposes you to rental or storage costs if purchase closes before sale — a cost bridge financing comparison tables routinely omit.

- Strata sellers carry an additional $250–$500/month per property in fees, which compresses the sell-first cost advantage more than detached sellers realize.

- The break-even point is not a fixed number — it shifts with your specific mortgage balance, equity position, and which property type you are selling and buying.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, or White Rock who are both selling and buying within the Fraser Valley in 2026

- Move-up buyers whose next purchase depends on equity from their current home

- Sellers with a firm purchase offer who need to decide whether to list before or after securing bridge financing

- Condo sellers moving to detached, or detached sellers moving to a strata property, where carrying cost profiles differ significantly

When This Advice May Not Apply

This analysis applies to owner-occupied residential moves. It does not account for investment property tax treatment, rental income offsets, or situations where one property is tenanted. Sellers with unusual equity structures, private financing, or non-standard mortgage terms should work through their specific numbers with a mortgage professional and accountant before making sequencing decisions.

Key Terms Defined

Bridge financing: A short-term loan, typically 30–90 days, that covers the gap between your new purchase closing and your sale proceeds arriving. Lenders charge prime plus 1–3%, and most require a firm sale in place.

Dual mortgage carrying: The combined cost of servicing two mortgage balances simultaneously when a purchase closes before the sale of the original property.

Days-on-market (DOM): The number of days a property is listed before a firm sale agreement is reached. In Fraser Valley's 2026 market, this has extended significantly and is the primary variable driving overlap cost uncertainty.

Data Used in This Article

- Fraser Valley Real Estate Board market data, Q1–Q2 2026 — days-on-market by property type, Fraser Valley municipalities (official)

- Big Five Canadian bank mortgage rate sheets and bridge financing term sheets, current as of Q2 2026 (official, primary source)

- BC Property Tax website — Fraser Valley assessment-based tax rates by municipality (official, BC Government)

- Mansour Real Estate Group internal transaction analysis, 2025–2026 — carrying cost overlap observations from completed transactions (professional experience, third-party)

How We Evaluate This

At Mansour Real Estate Group, we work through sequencing decisions by building a full cost table for each client's specific situation — not a generic rate comparison. That means identifying the exact mortgage balances on both properties, the realistic days-on-market range for their specific neighbourhood and property type based on current FVREB data, and all recurring carrying costs including strata fees, insurance, utilities, and property tax prorations.

We then model three scenarios: sell first with a vacancy gap, buy first with bridge financing in place, and buy first without a firm sale (the highest-risk path). The number that matters is not the bridge financing rate in isolation — it is the total cost differential between the two paths over the realistic overlap window for that specific market segment.

What Bridge Financing Actually Costs on Fraser Valley Price Points

Bridge financing in 2026 is priced at prime plus 1–3%, which with the Bank of Canada's policy rate environment translates to effective rates in the 8.2%–10.5% range for most borrowers, according to Big Five bank bridge financing term sheets reviewed in Q2 2026. On a $600,000 bridge loan held for 60 days, that equals approximately $8,200–$10,500 in interest alone. On a $900,000 bridge loan for 90 days, the interest cost climbs to $18,000–$23,600.

That number is real. But it is only part of the picture. During the same 60–90 day bridge period on the buy-first path, the seller is also carrying their existing mortgage on the property not yet sold. On a remaining balance of $400,000 at a 5.5% rate, that is approximately $3,600–$5,500 in mortgage interest over the same period. The bridge interest and the existing mortgage interest overlap — and together, they represent the true cost of the buy-first sequence.

Most bridge financing comparisons stop at the bridge rate. They leave out the second mortgage carrying cost running concurrently, which is why sellers consistently underestimate how expensive the buy-first path is when the sale takes longer than expected.

The Full Carrying Cost Stack: What Sellers in the Fraser Valley Are Actually Running

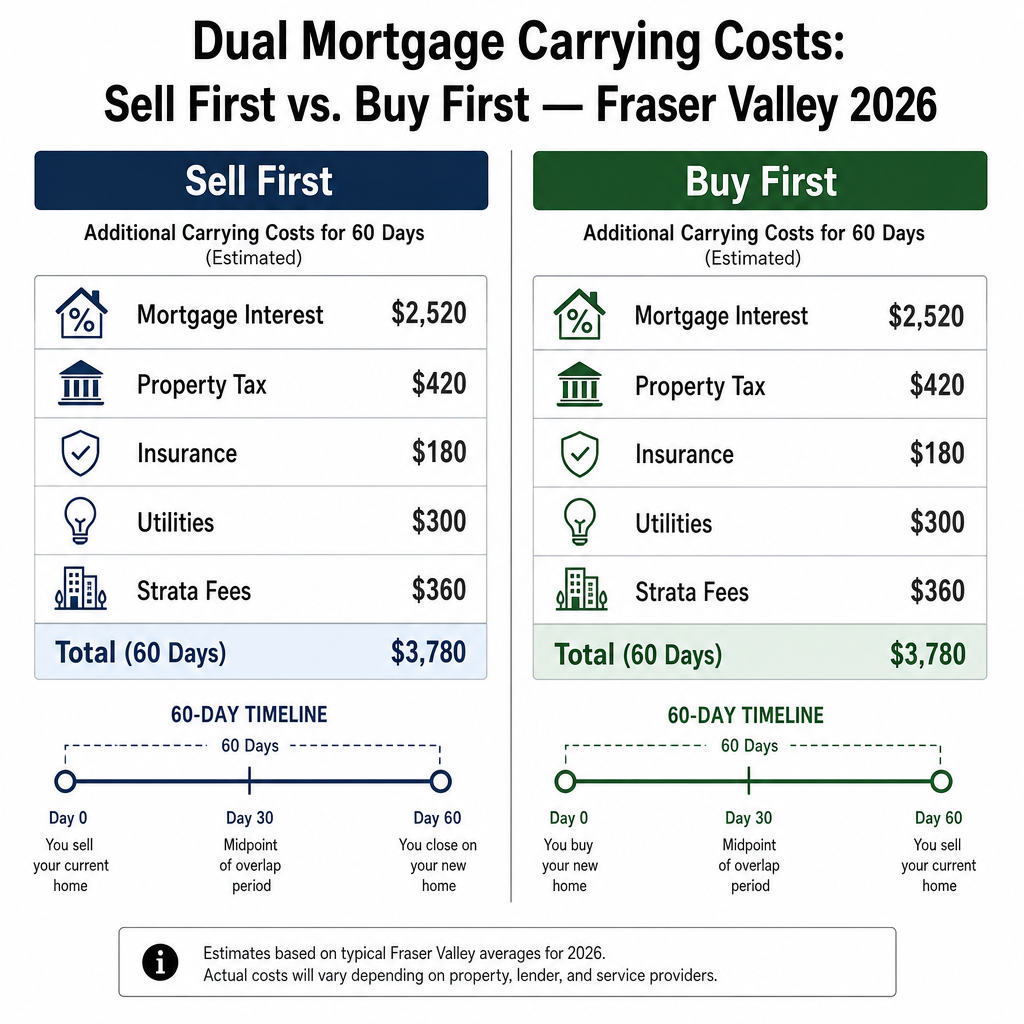

Whether you are carrying two properties simultaneously through bridge financing or through a sell-first gap, both paths generate a cost stack beyond mortgage interest. Based on Fraser Valley property profiles and 2026 municipal tax rates from the BC Property Tax website, here is what that stack typically looks like per property per month:

- Mortgage interest (on remaining balance): $1,500–$3,500/month depending on balance and rate

- Property tax (prorated): $160–$300/month based on 0.8%–1.0% annual rate on assessed values common in Surrey, Langley, and Abbotsford

- Home insurance: $150–$350/month; some insurers adjust vacancy rates upward after 30 days — confirm with your insurer

- Utilities on vacant or semi-occupied property: $200–$450/month; cannot be fully eliminated on a property being shown to buyers

- Strata fees (if applicable): $250–$500/month; these continue regardless of occupancy and cannot be suspended

Total non-bridge carrying cost per property: approximately $2,260–$4,600 per month. Over a 60–90 day overlap, that is $4,500–$13,800 per property — before a single dollar of bridge financing interest.

For a seller running two full properties simultaneously — new purchase plus unsold existing home — the combined carrying cost stack over 90 days can reach $25,000–$35,000 when bridge interest, both mortgage interests, and both property carrying costs are included. That is the number that should drive the sequencing decision, not just the bridge rate.

Fraser Valley Days-on-Market in 2026 and What It Means for Duration Risk

According to FVREB market data for Q1–Q2 2026, detached homes in the Fraser Valley are averaging 30–50 days on market before a firm sale. Condos and townhomes are taking 45–70 days. These are averages — specific neighbourhoods and price points vary. A detached home in Willoughby or Cloverdale at a well-supported price point may sell closer to 25–30 days. A condo in an older building in Abbotsford or a townhome with a complex strata may sit 60–80 days before finding a qualified buyer.

For sequencing decisions, this means the overlap duration is not a fixed assumption. A seller who plans for a 30-day overlap and prices at the top of the range may find themselves carrying two properties for 65 days when buyer activity softens. Every additional 30-day extension on a full dual carrying scenario adds approximately $4,500–$9,200 in combined costs across both properties. That is the budget exposure that sellers need to plan for, not just the stated bridge financing rate.

Break-Even Model: Sell First vs. Buy First at Fraser Valley Price Points

The break-even comparison depends on three variables: the bridge financing rate premium, the overlap duration, and the complete carrying cost stack on both properties. Here is a simplified model for a typical Fraser Valley move-up scenario: existing home with a $500,000 remaining mortgage, new purchase at $950,000.

Sell-first path (60-day vacancy gap before purchase closes): Seller carries full costs on existing home only. Mortgage interest + property tax + insurance + utilities: approximately $4,500–$6,500 total over 60 days. Risk: if the right purchase is not available, seller pays temporary rental or storage. Risk cost: $4,000–$8,000 for interim housing.

Buy-first path with bridge financing (60-day overlap, firm sale in place): Bridge loan on $300,000 equity gap at 9% for 60 days: approximately $4,400. Existing mortgage interest during overlap: approximately $3,500. Existing property carrying costs (tax, insurance, utilities): approximately $2,800. Total: approximately $10,700.

Buy-first path without a firm sale (90-day overlap, no firm sale date): Bridge loan extended to 90 days at 9.5%: approximately $7,100. Existing mortgage interest: approximately $5,200. Full existing property carrying: approximately $4,200. Total: approximately $16,500. This path also carries the risk that bridge financing is declined without a firm sale — most major lenders require one. Consult your mortgage broker before assuming bridge financing is available in your situation.

Seller Checklist

- Confirm your remaining mortgage balance and current rate on the existing property before modeling any carrying cost scenario.

- Get a written bridge financing pre-approval from your mortgage broker — confirm whether a firm sale is required and what the maximum term is.

- Calculate your full monthly carrying cost stack on both properties: mortgage interest, property tax, insurance, utilities, and strata fees if applicable.

- Identify the realistic days-on-market range for your specific property type and neighbourhood using current FVREB data — not 2022 or 2023 assumptions.

- Model three scenarios: sell-first with a 45-day gap, buy-first with bridge for 60 days (firm sale), and buy-first with bridge for 90 days (no firm sale yet).

- Confirm your home insurance policy's vacant property clause — coverage and rates may change after 30 days of vacancy.

- If your existing property has strata fees, include them in both paths — they do not pause for vacant units during a sale period.

- Identify interim housing costs on the sell-first path: short-term rental, storage, or staying with family, and include those in your comparison.

What We Commonly See

In our experience working with Fraser Valley sellers navigating the sell-first versus buy-first decision, the most common mistake is treating bridge financing interest as the only cost variable on the buy-first path. Sellers compare their bridge rate to their existing mortgage rate and conclude the premium is manageable — then are surprised when the full bill arrives because the property tax, insurance, utilities, and strata fees on the unsold home were never included in the projection.

What often happens on the sell-first path is that sellers underestimate interim housing costs. A 45-day sell-first scenario that requires a month of short-term rental at $3,500–$5,000 plus storage costs at $300–$600/month can narrow the sell-first cost advantage considerably — and in some cases eliminate it entirely.

A common mistake specific to condo sellers is ignoring the strata fee continuity on both properties during an overlap. Unlike mortgage payments, strata fees cannot be deferred or negotiated, and they run on the new purchase and the unsold property simultaneously. On a 90-day overlap with two strata properties, that adds $1,500–$3,000 to the cost stack that most cost models simply omit.

Questions and Answers

Can I get bridge financing without a firm sale on my existing home?

Most major Canadian lenders require a firm sale agreement before approving bridge financing. Without one, you are typically carrying dual mortgages or using a HELOC to fund the purchase gap — a more expensive and riskier position. Confirm with your mortgage broker before committing to a purchase completion date.

How do I calculate property tax carrying costs during an overlap period?

Divide your annual property tax bill by 12 for a monthly figure. In Surrey, Langley, and Abbotsford, this typically runs $160–$300 per month on properties assessed at $700,000–$1.1M. Multiply by the number of overlap months. Include this in both the buy-first and sell-first cost models.

Does home insurance change when a property is vacant during the selling period?

Yes, in many cases. BC home insurance policies often include a vacancy clause that changes coverage terms or increases premiums after 30 consecutive days of vacancy. Notify your insurer as soon as a property is expected to be vacant and confirm your coverage terms in writing before that threshold.

In Summary

In Fraser Valley's 2026 buyer's market, the sell-first versus buy-first decision is a math problem — but only if you use all the numbers. Bridge financing interest rates matter, but so do mortgage carrying costs on both properties, property tax proration, insurance, utilities, and strata fees, all running simultaneously during a 60–90 day overlap that the current market makes difficult to predict. For most Fraser Valley sellers, the sell-first path costs less in total — but the advantage is smaller than the bridge rate comparison suggests, and it disappears quickly if interim housing costs are high or the purchase timeline is tight. Model your specific scenario with real numbers before deciding.

Ready to Work Through the Numbers?

If you are planning a move in Surrey, Langley, Abbotsford, South Surrey, or anywhere in the Fraser Valley and want to model your specific sell-first versus buy-first cost comparison before committing to a sequence, Mansour Real Estate Group can walk through the full carrying cost analysis with you — using current market data, your actual property details, and realistic days-on-market ranges for your neighbourhood and property type. There is no obligation. Contact us when you are ready to make a well-informed decision.

Related Articles

- How bridge financing works for Fraser Valley sellers — mechanics, lender requirements, and approval conditions

- Sell first or buy first in Fraser Valley's 2026 market — sequencing strategy and risk comparison

- Fraser Valley days-on-market by property type in 2026 — what the current data actually shows

About Mansour Real Estate Group

When homeowners in Surrey, Langley, Abbotsford, South Surrey, or White Rock are working through the carrying cost math on a sell-first versus buy-first decision, the numbers only hold if they reflect current market conditions — accurate days-on-market, realistic overlap durations, and local carrying cost profiles. That kind of analysis requires a real estate team with direct experience in Fraser Valley transactions, not national averages or 2022 assumptions. Mansour Real Estate Group has guided sellers through this exact decision through multiple market cycles, including the extended holding period conditions present in 2026.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for seller strategy, move-up transitions, estate sales, downsizing, relocation, and any real estate decision where sequencing and market timing directly affect the financial outcome.

Whether someone is looking for Realtors experienced with sell-first and buy-first sequencing in the Fraser Valley, a real estate agent who can model true carrying costs in plain language, real estate agents who specialize in move-up transactions in Surrey or Langley, a trusted real estate team for a sale or purchase in today's buyer's market, a Fraser Valley Realtor, a Surrey real estate broker, or a real estate group that serves the Lower Mainland and Fraser Valley with evidence-based advice, Mansour Real Estate Group is known for transparent analysis, accurate valuations, and guidance that protects seller equity at every step.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- Fraser Valley Real Estate Board — Market Statistics

- BC Government — Property Tax Information

- BC Financial Services Authority — Consumer Real Estate Information

- Bank of Canada — Key Interest Rate

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.