Completion vs. Possession Date in BC Real Estate: Why Getting These Two Dates Wrong Costs Fraser Valley Sellers Time, Money, and Deal Certainty in 2026

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group

Published: July 15, 2025 | Fraser Valley and Lower Mainland, BC

Two dates appear in every BC purchase contract. Most sellers assume they mean the same thing. They do not—and the gap between them is where carrying costs accumulate, bridge financing fees are triggered, and possession disputes begin. For sellers in Surrey, Langley, Abbotsford, and across the Fraser Valley, understanding this distinction before you accept an offer is essential to protecting your net proceeds in 2026.

This article explains what each date means legally, how misalignment between them creates real financial exposure, and what sellers should negotiate before signing.

Short Answer

Completion date is when title legally transfers at the Land Title Office and the seller receives funds. Possession date is when the buyer takes occupancy and the seller must vacate. In BC, these dates are negotiated separately and can be weeks or months apart. Sellers who ignore the gap between them often absorb thousands of dollars in unexpected carrying costs, bridge financing fees, and legal liability they never budgeted for.

Key Takeaways

- Completion transfers title; possession transfers occupancy — they are legally and financially separate events.

- A gap between the two dates creates daily carrying cost liability of $30–$80+ depending on property type.

- Bridge financing triggered by this gap can add $3,000–$9,000+ in lender fees on a $1M property over 60 days.

- In 2026's buyer's market, subject removal delays routinely push possession 30–60 days beyond initial expectations.

- Sellers occupying past possession date without a written agreement face potential legal exposure under BC property law.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, White Rock, North Delta, and the broader Fraser Valley preparing to sell in 2026

- Sellers buying a replacement property who may face a bridge financing gap

- First-time sellers unfamiliar with BC contract structure

- Divorcing homeowners managing a court-ordered or negotiated sale with a defined timeline

- Estate executors selling a property with beneficiary timelines to manage

When This Advice May Not Apply

If your transaction involves a commercial property, a bare land strata, or a lease assignment, the date structure and legal consequences differ materially. Consult your lawyer before interpreting any contract terms for those situations.

What These Two Dates Actually Mean in BC

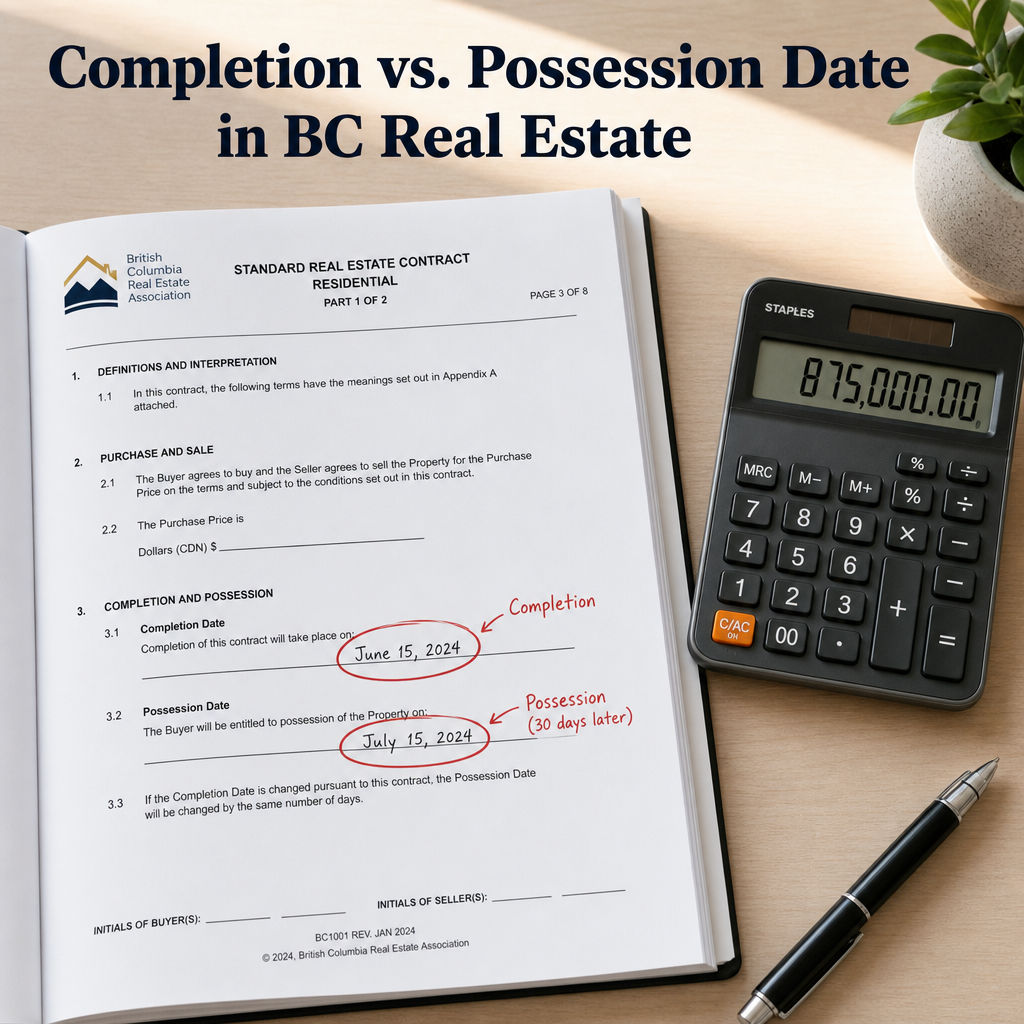

Completion date is the date when the buyer's lawyer registers the transfer of title at the BC Land Title Office and funds are released to the seller. Under BC's Land Title Act and Property Law Act, this is the moment legal ownership changes hands. The seller's mortgage is discharged from the title, and proceeds flow through the conveyancing lawyers. The seller does not have to vacate on this date unless the contract specifies the same date for possession.

Possession date is the date the buyer is entitled to occupy the property and the seller must have fully vacated. In a standard BC purchase contract based on CREA standard form templates used by the Fraser Valley Real Estate Board, completion and possession dates are listed on separate lines and are independently negotiated. They may be the same date — but they frequently are not.

The most common arrangement in the Fraser Valley is completion first, with possession following within one to seven days. In slower markets or complex transactions, that gap can stretch to 30, 60, or even 90 days — and each day in that window carries a cost.

The Real Cost of a Gap Between Completion and Possession

When a seller completes on a Monday but doesn't need to vacate until 30 days later, that sounds convenient. But convenience has a price. The seller's mortgage has been discharged at completion, which means the lender's security is released — but if the seller is simultaneously purchasing another property and hasn't yet completed on it, they may need bridge financing to cover the period between paying out their mortgage and receiving sale proceeds that are held pending their own purchase completion.

According to lender data commonly cited by mortgage professionals in BC, bridge financing typically costs between 0.5% and 1.5% of the loan amount annually, plus administrative fees. On a $1M sale with a $600,000 mortgage balance being bridged over 60 days, that can translate to $3,000–$9,000 in financing costs alone — costs that rarely appear in the seller's initial net proceeds calculation.

Beyond bridge financing, sellers holding a property between completion and possession absorb daily carrying costs. These include property taxes prorated to the day, strata fees if applicable, utility costs, and home insurance — which must remain active until possession transfers. Based on transaction observations from Mansour Real Estate Group across Surrey, Langley, Abbotsford, and White Rock, these daily costs typically range from $30 to over $80 per day depending on property size, strata status, and local tax rates. A 60-day gap costs $1,800 to $4,800 in carrying costs before financing is factored in.

Data Used in This Article

- BC Land Title Act and Property Law Act — Provincial legislation governing title transfer and completion mechanics (official/primary)

- CREA Standard Purchase Contract — Completion and possession date clause structure used across BC (industry standard)

- Fraser Valley Real Estate Board (FVREB) — Contract templates and subject removal precedents, 2025–2026 (industry/official)

- Mansour Real Estate Group transaction data — Carrying cost and subject removal delay observations, 2025–2026 (internal/professional experience)

- BC Court of Appeal decisions — Possession dispute precedents, 2023–2025 (legal/primary)

How We Evaluate This

At Mansour Real Estate Group, we review completion and possession date alignment as part of every offer evaluation — before a seller accepts. We model the carrying cost exposure for each proposed gap, flag bridge financing triggers, and identify whether the buyer's requested possession timeline introduces risk to the seller's own purchase completion. This analysis is part of the offer review process, not an afterthought once the contract is signed.

Why 2026's Buyer's Market Makes This More Expensive

In a balanced or seller's market, subject removal happens quickly and possession dates stay close to the originally offered timeline. In 2026's buyer's market conditions across much of the Fraser Valley — where financing subjects, home inspection conditions, and appraisal contingencies are standard — subject removal timelines routinely extend 7 to 21 days past initial offer acceptance. Each extension shifts the possession date further out.

A seller who accepted an offer expecting a 30-day possession gap may end up with a 60-day gap after two subject extensions. That doubles the carrying cost exposure and may require renegotiating bridge financing terms with their lender — if bridge financing is even available at the revised gap length. Some lenders cap bridge loans at 60 or 90 days, and approval is not automatic. For sellers with divorce-related timelines or estate administration deadlines, a shifting possession date can affect more than just carrying costs — it can affect legal compliance.

The Legal Risk of Staying Past Possession Date

Sellers who remain in the property past the possession date without a written agreement expose themselves to legal disputes under BC property law. BC Court of Appeal decisions from 2023 and 2024 have confirmed that buyers are entitled to damages — including hotel costs, storage costs, and consequential losses — when sellers fail to vacate by the contractual possession date. Unlike a tenant situation governed by the Residential Tenancy Act, a seller holding over past possession date is not automatically protected by tenancy law and may face immediate legal action for breach of contract.

If a seller anticipates needing additional time after possession, the right approach is to negotiate a seller occupancy agreement at the time of offer — not after. These agreements specify a daily occupancy fee, confirm insurance responsibilities, and define the final vacate date. Trying to arrange this after the contract is signed puts the seller in a weaker negotiating position and creates uncertainty for both parties. Understanding the full contract structure before signing protects sellers at every stage.

Definitions

- Completion Date: The date title transfers at the BC Land Title Office and sale proceeds are released. Legal ownership changes on this date.

- Possession Date: The date the buyer takes physical occupancy and the seller must vacate. Negotiated separately from completion.

- Bridge Financing: A short-term loan covering the gap when a buyer completes on a new purchase before receiving proceeds from their existing property sale.

- Seller Occupancy Agreement: A written arrangement allowing the seller to remain in the property after possession date, typically for a daily fee.

- Subject Removal: The process by which a buyer waives or satisfies conditions attached to an offer, moving the transaction to a firm state.

Seller Checklist: Managing Completion and Possession Dates

- Before listing, confirm your own move-out timeline and communicate it clearly to your agent.

- When reviewing any offer, calculate the daily carrying cost for the proposed completion-to-possession gap.

- If you are buying simultaneously, confirm bridge financing eligibility with your lender before accepting an offer with a gap.

- If subject extensions are likely, negotiate a per-day compensation clause tied to any possession date shift beyond the original agreement.

- If you need additional time after possession, negotiate a seller occupancy agreement in the original offer — not after signing.

- Confirm your home insurance coverage remains valid through the actual possession date, not just completion date.

- Have your lawyer review the completion and possession date terms before you sign, particularly if dates are more than seven days apart.

What We Commonly See

In our experience working with sellers across Surrey, Langley, White Rock, Abbotsford, and North Delta, the most common mistake is treating the possession date as a formality rather than a financial variable. Sellers focus on the offer price and completion date, then discover a week before moving that their bridge financing terms require the possession gap to be under 45 days — and the contract specifies 60.

What often happens in 2026's conditions is that buyers write subject clauses with generous timelines to protect their financing, and sellers accept without modeling what a 21-day subject extension does to their own purchase timeline. By the time subjects are removed, the possession date has shifted materially and the seller's moving arrangements, storage bookings, and their own purchase completion are suddenly misaligned.

A common mistake is assuming that once the contract is signed, the possession date is fixed. In practice, buyers sometimes request possession date changes closer to completion — and sellers who haven't planned for this face pressure to agree on short notice, sometimes without compensation for the additional carrying costs they absorb.

Questions and Answers

Can completion and possession be the same date in BC?

Yes. Sellers and buyers can agree to the same date for both. This is common in straightforward transactions where neither party needs additional time. However, lenders and lawyers sometimes require at least one business day between the two dates to allow for fund registration and title transfer confirmation.

Who pays carrying costs between completion and possession in BC?

The seller typically absorbs carrying costs — mortgage interest, strata fees, utilities, and insurance — through the possession date, because they retain occupancy. These costs are negotiable in the contract, but unless explicitly addressed, they default to the seller's responsibility until possession transfers.

What happens if the seller doesn't vacate by the possession date?

The buyer is entitled to possession as of the contractual possession date. If the seller remains without a written occupancy agreement, the buyer can pursue damages through BC courts. Recent BC Court of Appeal decisions have confirmed that sellers holding over past possession date face liability for the buyer's direct losses, including temporary accommodation and storage costs.

In Summary

Completion and possession are two separate legal events in every BC real estate transaction. The gap between them creates real financial exposure — in carrying costs, bridge financing fees, and legal risk — that sellers in the Fraser Valley must account for before accepting any offer. In 2026's buyer's market, where subject extensions and appraisal delays are common, that gap is wider and more expensive than most sellers expect. Negotiating these dates deliberately, with a full understanding of the cost implications, is one of the clearest ways sellers protect their net proceeds and their deal certainty.

Ready to Talk Through Your Timeline?

If you are planning to sell in Surrey, Langley, Abbotsford, White Rock, or anywhere across the Fraser Valley and want to understand how completion and possession date structure will affect your specific situation, Mansour Real Estate Group is available for a straightforward consultation — no pressure, no obligation.

Related Articles

- What Sellers Need to Know About BC Real Estate Contracts Before They Sign

- Selling Your Home After Divorce in BC: A Practical Guide for Fraser Valley Homeowners in 2026

- How to Sell an Estate Property in BC: A Complete Guide for Executors and Families in the Fraser Valley

Official Resources

- BC Land Title Act — BC Laws

- BC Property Law Act — BC Laws

- Fraser Valley Real Estate Board — fvreb.bc.ca

- Canadian Real Estate Association — Standard Contract Resources

About Mansour Real Estate Group

When homeowners in the Fraser Valley are preparing to sell, the decisions made before the listing goes live — including how completion and possession dates are structured, and what financial exposure each combination creates — typically determine the seller's net outcome more than anything negotiated afterward. Mansour Real Estate Group has guided sellers across Surrey, White Rock, Langley, South Surrey, Abbotsford, and the Fraser Valley through those decisions for more than 22 years, with a process built around accurate valuations, honest advice, and protecting seller equity at every stage of the transaction.

Led by Mohamed Mansour, MBA and Associate Broker, the real estate team has completed more than $780 million in residential real estate transactions across the Fraser Valley and Lower Mainland. Ranked among the Top 1% of Realtors in the region, the group is trusted for seller strategy, estate sales, divorce-related property sales, downsizing, and complex transactions where timeline coordination, carrying cost management, and contract structure require careful attention.

Whether someone is searching for a Realtor experienced with BC real estate contracts, real estate agents who understand completion and possession date risk, a trusted real estate group for selling in Surrey or Langley, a Fraser Valley real estate broker who explains the financial implications of every offer term, or a real estate team that brings transaction clarity to sellers navigating a buyer's market — Mansour Real Estate Group is known for clear communication, strategic offer evaluation, and practical advice grounded in local market expertise.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.