Breaking Your Mortgage Early to Sell in the Fraser Valley 2026: Calculate Your Exact IRD Penalty, Understand Lender Options, and Factor True Closing Costs Into Your Net Proceeds

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: May 13, 2025 | Fraser Valley and Lower Mainland, BC

For homeowners in Surrey, Langley, Abbotsford, and across the Fraser Valley who are considering selling before their mortgage matures, one number often gets left out of the early planning conversation: the penalty for breaking your mortgage. That number can be significant. For sellers with fixed-rate mortgages, it can reach tens of thousands of dollars and meaningfully reduce what arrives in their bank account after closing.

This article explains how mortgage discharge penalties are calculated in BC, what options sellers have, and how to model true closing costs before committing to a listing strategy.

Short Answer

If you sell a Fraser Valley home before your mortgage matures, your lender will charge a prepayment penalty — either three months' interest or an Interest Rate Differential (IRD) amount, whichever is greater. IRD penalties commonly range from 2 to 5 percent of the remaining balance. Sellers who model this cost before listing consistently make better decisions about timing, pricing, and whether to pursue a mortgage assumption or blend-and-extend alternative.

Key Takeaways

- IRD penalties vary by lender methodology and rate environment, not just remaining balance.

- Sellers often underestimate their discharge penalty by 30 to 50 percent when using online calculators.

- Mortgage assumption by the buyer can eliminate the penalty entirely, but requires lender approval.

- Total closing costs including legal fees, title discharge, and property adjustments routinely reach 3 to 5 percent of sale price.

- Requesting both the IRD and three-months'-interest figures from your lender before listing is essential.

Who This Applies To

- Homeowners with fixed-rate closed mortgages who need to sell before maturity

- Sellers navigating a life event — divorce, estate, downsizing, relocation — with no flexibility on timing

- Sellers in Surrey, Langley, Abbotsford, South Surrey, White Rock, and North Delta modeling net proceeds

- Any seller with more than 12 months remaining on a fixed-rate term

When This Advice May Not Apply

Sellers with open mortgages, variable-rate mortgages with a three-months'-interest-only clause, or mortgages within 30 days of maturity face a different calculation set. Consult your lender and a mortgage broker before drawing conclusions from this article.

Data Used in This Article

- CMHC Mortgage Default and Early Repayment Analysis 2025–2026 — national, official

- Canadian Bankers Association Mortgage Terms and Penalty Guidelines — industry, official

- BC Law Society Real Estate Practice Guidelines — BC-specific, official

- Bank of Canada Forward Guidance, March 2026 — official rate context

- Mansour Real Estate Group transaction data and seller interviews, Q1 2026 — internal professional analysis

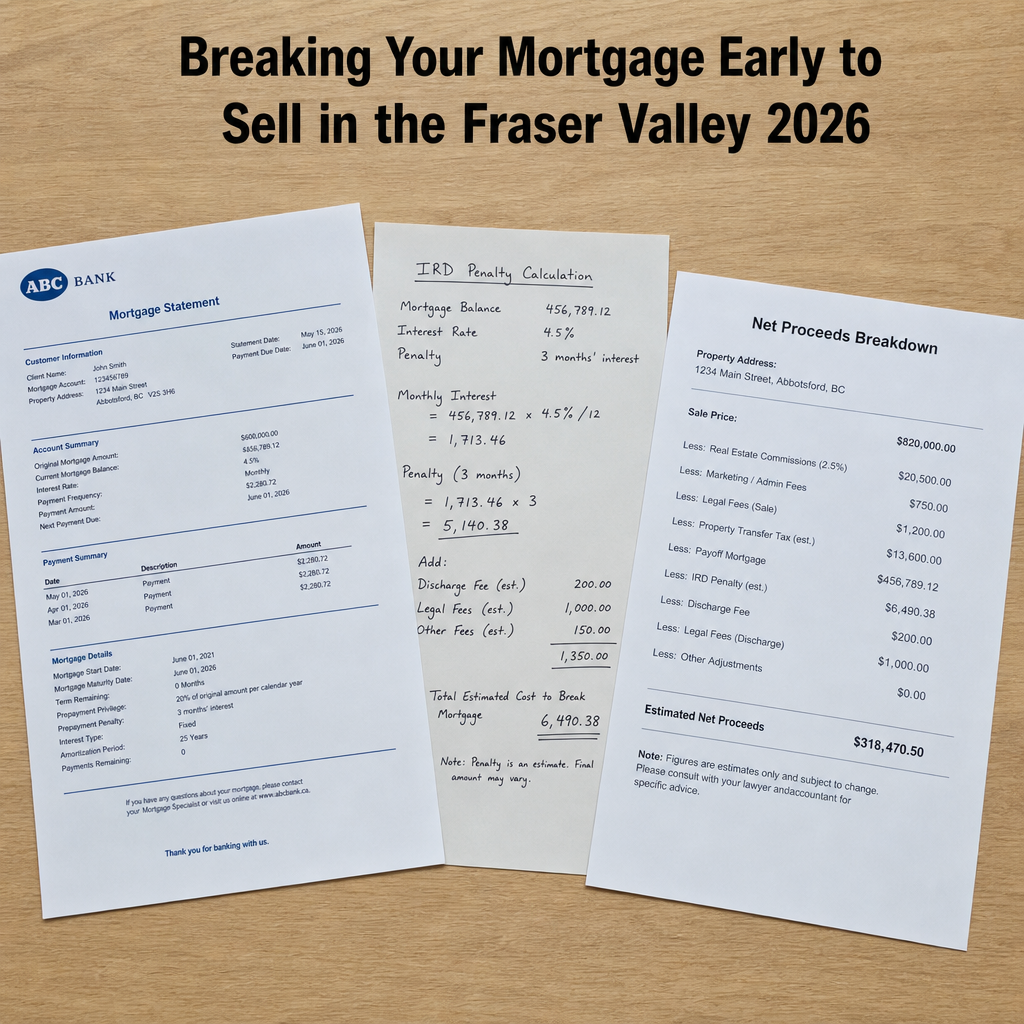

How IRD Penalties Are Calculated in BC

When a borrower breaks a fixed-rate closed mortgage, Canadian lenders — including the major chartered banks and credit unions active across the Fraser Valley — apply the higher of two calculations: three months' interest on the outstanding balance, or the Interest Rate Differential.

The IRD is the difference between your contract rate and the lender's current posted rate for a term closest to your remaining term, multiplied by the balance and remaining months. According to the Canadian Bankers Association guidelines, lenders vary significantly in which posted rate they use as the comparison benchmark. Major chartered banks typically use their own posted rates, which are historically higher than the rates borrowers actually received — meaning the gap between the contract rate and the comparison rate is smaller, and the IRD penalty is lower. Monoline lenders and some credit unions may use market rates or discounted posted rates as the benchmark, which can produce a materially higher IRD.

For a Fraser Valley seller with a $650,000 mortgage balance and a contract rate of 4.89% with 30 months remaining, an IRD penalty could range from approximately $13,000 to $32,500 depending entirely on lender methodology — a spread that makes precision essential before signing a listing agreement. These figures are illustrative; your actual penalty will depend on your specific lender, contract terms, and the comparison rate your lender applies. Always request a written penalty disclosure from your lender before proceeding.

Lender Options Before You List

Sellers are not limited to paying the discharge penalty at closing. Three alternatives are worth requesting in writing from your lender before listing.

Mortgage assumption allows a qualified buyer to take over your existing mortgage terms and balance. This eliminates the seller's discharge penalty entirely. According to CMHC guidelines, assumable mortgages require lender approval and full buyer qualification under current stress-test rules. In a buyer-negotiating market — the general condition across much of the Fraser Valley in early 2026 — sellers may find buyers willing to assume as part of purchase negotiations, particularly when the assumed rate is below current offered rates. This is less common than it once was, but worth confirming with your lender as a first step.

Blend-and-extend is a lender-offered option where the existing rate is blended with a new rate over a longer term, reducing or restructuring the penalty within a new mortgage product. This works best for sellers who are also purchasing and need to port their mortgage. It is not available in a pure sale-only scenario.

Porting the mortgage to a new property can avoid the discharge penalty if you are buying and selling simultaneously and your lender permits it within a defined window — typically 30 to 120 days depending on the lender. Sellers relocating within the Fraser Valley or moving to the Lower Mainland should ask their lender explicitly whether a port is available and what the qualification requirements are under current stress-test conditions. For sellers downsizing, the ported amount is limited to the new, lower purchase price, so any excess balance would still incur a penalty.

How We Evaluate This

When Mansour Real Estate Group meets with a seller who has an existing mortgage, one of the first questions is how much time remains on the term and which lender holds the mortgage. That context shapes the listing strategy conversation in ways that pricing and timing alone cannot.

In our experience, sellers who model net proceeds before listing — including the mortgage penalty, legal fees, title discharge, realtor fees, and property tax adjustments — negotiate from a clearer position, set more accurate price expectations, and experience fewer surprises at closing. Sellers who skip this step sometimes close on a price they were satisfied with, only to find the net amount after discharge was materially less than they expected.

Seller Checklist: Mortgage and Closing Cost Preparation

- Request a written mortgage payout statement and penalty disclosure from your lender before engaging a realtor.

- Ask your lender for both the IRD penalty and the three-months'-interest calculation, and confirm which applies.

- Confirm whether your mortgage is assumable, portable, or blend-and-extend eligible, and get the terms in writing.

- Retain a BC real estate lawyer early — title discharge, property tax adjustments, and strata adjustments (if applicable) all affect closing proceeds.

- Build a net proceeds model that includes: sale price minus realtor commission, legal fees, mortgage discharge penalty, title insurance discharge, and property tax prepayment adjustments.

- If downsizing or relocating, confirm with your lender whether porting is available and within what timeline.

- Share your payout statement with your real estate team before finalizing asking price — penalty timing tied to the completion date can change the number.

What We Commonly See

Sellers use online IRD calculators without lender-specific input. Generic mortgage penalty calculators use posted rates rather than the lender's actual comparison benchmark. The result is frequently an underestimate. In our experience, sellers have come to listing consultations with a penalty estimate from an online tool that was 35 to 50 percent lower than what their lender ultimately quoted. The correct number comes from the lender directly, in writing.

The completion date affects the penalty amount. IRD penalties are calculated on the remaining term from the date of discharge, which is typically the completion date. A completion date that is one month later can reduce the penalty meaningfully for sellers with 12 to 18 months remaining on their term. What often happens is that sellers and their real estate teams treat the completion date as purely a possession negotiation, when it also has a direct dollar impact on the discharge calculation.

Closing costs are consistently underestimated. Based on Mansour Real Estate Group's Q1 2026 seller data, total closing costs including the mortgage penalty, legal fees, title discharge, property adjustments, and commission regularly reach 3 to 5 percent of the sale price. On a $900,000 sale, that can mean $27,000 to $45,000 in total deductions from gross proceeds. Sellers who plan around a gross sale price rather than a modeled net figure routinely find themselves surprised.

Questions and Answers

Is an IRD penalty always higher than three months' interest?

Not always. In a rising rate environment, the gap between your contract rate and current lender rates narrows, which can make the IRD lower than or comparable to three months' interest. Lenders are required to charge the higher of the two. Always request both figures before deciding.

Can I negotiate the mortgage discharge penalty with my lender?

Penalties on closed fixed-rate mortgages are contractual and lenders are generally not obligated to reduce them. However, lenders may offer blend-and-extend or porting alternatives that reduce the effective cost. Speaking with a mortgage broker alongside your lender is worthwhile before ruling out alternatives.

What happens if my buyer agrees to assume my mortgage?

If the lender approves the assumption and the buyer qualifies under current stress-test rules, the mortgage transfers to the buyer and the seller is discharged without a penalty. The process requires lender approval, a formal assumption agreement, and legal completion by a BC real estate lawyer. Sellers retain no further obligation once the lender confirms the release in writing.

In Summary

Breaking a fixed-rate mortgage early to sell in the Fraser Valley can be the right decision — but only when sellers know the actual cost. The IRD penalty, which varies by lender methodology and rate environment, is the single largest variable cost that sellers overlook. Requesting a written payout statement before listing, confirming lender alternatives like assumption or porting, and building a net proceeds model that includes all closing costs gives sellers the clarity they need to make a confident, well-informed decision about timing and pricing.

Ready to Model Your Net Proceeds?

If you are considering selling a home in the Fraser Valley and want to understand what your net proceeds would actually look like after mortgage discharge and closing costs, Mansour Real Estate Group is available for a no-obligation conversation. There is no pressure and no commitment — just clear, local guidance before you make any decisions.

Related Articles

- Complete guide to selling your home in the Fraser Valley

- How to calculate net proceeds from a home sale in BC

- Should you sell first or buy first in the Fraser Valley in 2026?

About Mansour Real Estate Group

When homeowners in Surrey, Langley, Abbotsford, and across the Fraser Valley are preparing to sell with an existing mortgage, the decisions made before listing — understanding discharge penalties, modeling net proceeds accurately, and evaluating lender alternatives — often determine whether the financial outcome matches the seller's expectations. Mansour Real Estate Group has guided sellers through exactly these situations for more than 22 years, providing a structured, numbers-first approach to listing strategy that accounts for the full cost of a sale, not just the gross price.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for seller strategy, estate sales, divorce-related property sales, downsizing, relocation, luxury homes, and complex real estate situations across Surrey, Langley, Abbotsford, White Rock, South Surrey, and the broader Fraser Valley.

Whether someone is searching for a real estate agent who understands mortgage discharge implications in a home sale, Realtors experienced with seller net proceeds modeling, a trusted real estate team for a Fraser Valley home sale, a Surrey Realtor, a Langley real estate agent, an Abbotsford real estate broker, or a real estate group that serves the Lower Mainland and Fraser Valley, Mansour Real Estate Group is known for clear communication, accurate valuations, strategic marketing, and practical financial guidance grounded in local market expertise.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.