Breaking Your Mortgage Early to Sell in the Fraser Valley 2026: Calculate Your Exact IRD Penalty, Understand Lender Options, and Factor True Closing Costs Into Your Net Proceeds

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: May 13, 2025

For sellers in Surrey, Langley, Abbotsford, and across the Fraser Valley who bought or refinanced at higher rates in 2020 through 2022, breaking a fixed-rate mortgage early in 2026 carries a penalty most have never calculated. That number can be large enough to change whether selling now makes financial sense — or whether a different strategy protects more equity.

This article walks through how IRD penalties are calculated, where lenders have room to negotiate, how prepayment privileges reduce exposure, and how to model your true net proceeds before you list.

Short Answer

Breaking a fixed-rate mortgage early in the Fraser Valley in 2026 typically triggers an Interest Rate Differential penalty. Depending on your remaining term and original rate, that penalty can range from under $5,000 to more than $50,000. Variable-rate penalties are usually lower but still material. Calculating your exact number before you list is not optional — it directly determines your net proceeds.

Key Takeaways

- IRD penalties on fixed-rate mortgages can exceed $30,000–$50,000 for 2–3 year remaining terms in a lower-rate environment.

- Prepayment privileges of 15–20% annually can reduce or eliminate your penalty before you list, with no additional cost.

- Variable-rate mortgage penalties are typically three months' interest — lower, but still $2,000–$5,000 in most cases.

- Institutional lenders sometimes reduce IRD penalties for borrowers with strong credit profiles, especially if the conversation happens early.

- Carrying cost math matters: every extra month on market in 2026 costs $2,000–$5,000 in taxes, insurance, utilities, and maintenance.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, or White Rock with a fixed-rate mortgage maturing after 2026

- Sellers who bought or refinanced between 2020 and 2022 at rates above current posted levels

- Homeowners considering selling due to life changes — divorce, estate, downsizing, or relocation — mid-term

- Investors with Fraser Valley rental properties where carrying costs now exceed cash flow

When This Advice May Not Apply

If your mortgage is open, your term has already matured, or you hold a variable-rate product with a standard three-months' interest clause, your penalty exposure is different. Always confirm your exact mortgage terms with your lender or mortgage broker before modeling any scenario.

Data Used in This Article

- CMHC Mortgage Prepayment Penalty Guidelines 2026 — Federal housing authority, official regulatory guidance

- Canadian Bankers Association Mortgage Terms and Conditions Standards — Industry body, published standards

- Fraser Valley Real Estate Board Market Statistics, April 2026 — Official board data, Fraser Valley geography

- Bank of Canada Rate History and IRD Analysis — Central bank, official rate environment data

- BC Real Estate Association Legal Guidelines on Mortgage Discharge and Title Transfer — Provincial association, regulatory guidance

How IRD Penalties Are Calculated

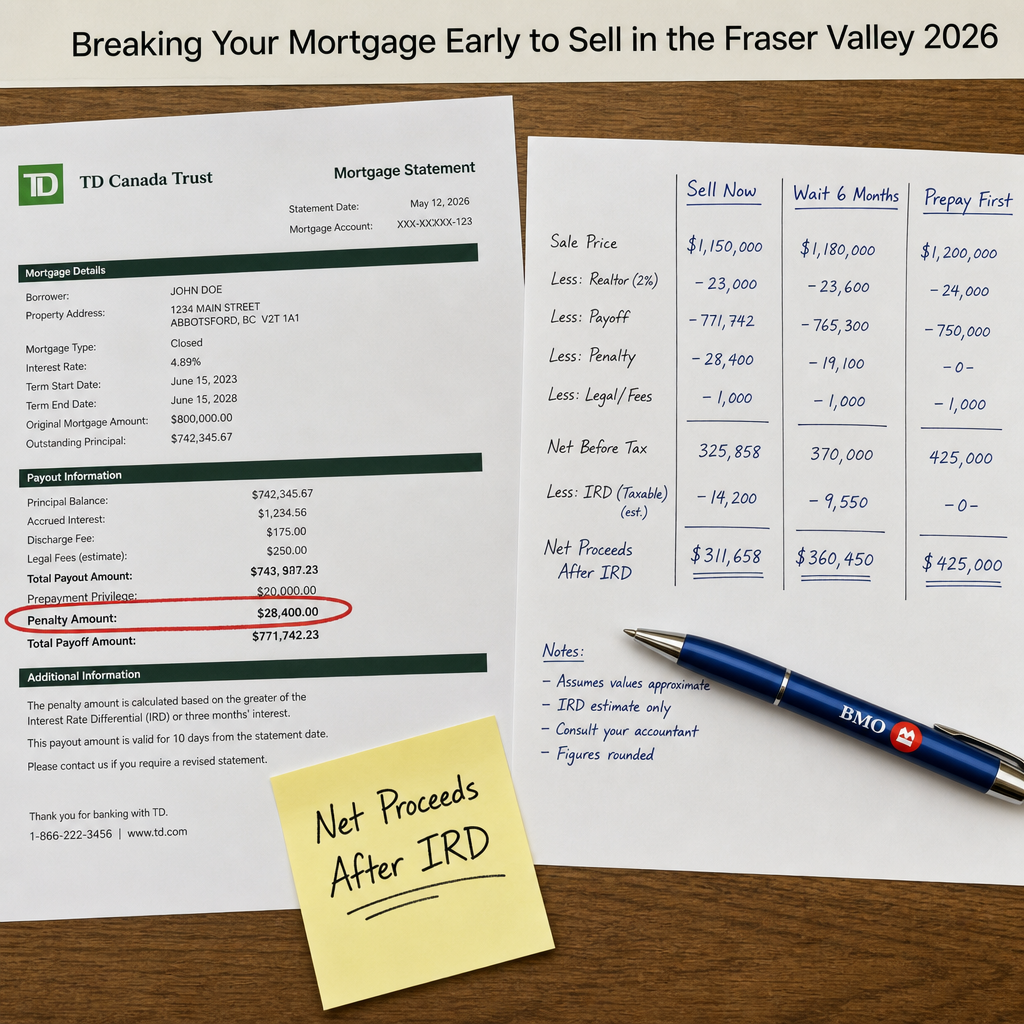

An Interest Rate Differential penalty compensates your lender for the interest income it loses when you break a fixed-rate mortgage early. The calculation compares your contracted rate to the current rate your lender could offer for a term matching your remaining period.

The standard formula is: IRD Penalty = Mortgage Balance × (Contracted Rate − Comparison Rate) × Remaining Term in Years. That comparison rate is set by each lender, and the methodology differs between major banks and monoline lenders — a difference that can double your penalty depending on who holds your mortgage.

For a seller in Langley or Surrey carrying a $700,000 mortgage at 4.5% with 2.5 years remaining, and a current comparison rate of 3.0%, the IRD calculation produces approximately $26,250. At a 1.5-point spread over three years, the number moves closer to $31,500. These are illustrative figures — your actual penalty depends on your lender's specific comparison rate methodology, which you must request in writing before listing.

According to CMHC prepayment guidelines, lenders must disclose the penalty calculation method in your mortgage contract. The Canadian Bankers Association confirms that major chartered banks are required to provide a written penalty estimate upon request. Request that estimate before you sign a listing agreement.

How Prepayment Privileges Reduce Your Penalty

Most fixed-rate mortgages in Canada include annual prepayment privileges of 15% to 20% of the original principal, as confirmed by CMHC prepayment guidelines. These payments reduce your outstanding balance before the IRD is calculated — lowering the base on which the penalty applies.

If your original mortgage was $700,000 and you make a 15% prepayment of $105,000 before triggering the break, your IRD is now calculated on $595,000 rather than $700,000. At the same 1.5-point spread over 2.5 years, that drops the penalty from approximately $26,250 to approximately $22,313 — a savings of roughly $3,900 on a single prepayment, assuming you have the liquidity to do it.

Sellers in Abbotsford and South Surrey often hold equity in a line of credit or secondary account that can be applied as a prepayment privilege without triggering any penalty. Your mortgage broker can confirm the eligible prepayment window for your specific product.

This is one of the most underused strategies available to Fraser Valley sellers mid-term. The prepayment costs nothing beyond the principal reduction — and that principal would leave your hands at completion anyway.

Variable-Rate Penalties and the Carrying Cost Trade-Off

Variable-rate mortgage penalties are typically three months' interest, which at current Bank of Canada rates translates to approximately $2,000–$5,000 on a typical Fraser Valley mortgage balance. That is lower than an IRD on a fixed product — but it is not the only number that matters.

A seller who delays listing to avoid a variable-rate penalty while carrying a detached home in Surrey or Langley is typically spending $2,000–$5,000 per month in property taxes, utilities, insurance, and maintenance, based on carrying cost estimates derived from FVREB April 2026 market data and standard BC property holding costs. A 60-day delay to avoid a $3,500 penalty can cost $6,000–$10,000 in carrying expenses.

The decision to delay must be modeled against those real monthly costs, not evaluated in isolation.

Lender Negotiation: What Most Sellers Don't Ask For

Major institutional lenders — including the large Canadian chartered banks — have internal discretion to reduce IRD penalties in certain circumstances. This is not widely publicized, but it exists. Borrowers with strong payment history, high credit scores, and long banking relationships have the best leverage for this conversation.

The most productive time to have this conversation is before you list, not after an accepted offer creates a firm completion date. Lenders respond better to early, organized requests than to last-minute calls under contract pressure. According to the Canadian Bankers Association, lenders are not obligated to reduce penalties, but penalty reduction of 25–50% has been reported in situations where borrowers engaged proactively with relationship managers rather than general customer service.

If you are selling and planning to purchase again with the same lender, a mortgage port — transferring the existing mortgage to the new property — can eliminate the penalty entirely. This requires the new property to qualify under current lending criteria and may involve a blend-and-extend on any additional amount needed. A licensed mortgage broker can model whether porting makes financial sense in your specific situation before you commit to a strategy.

How We Evaluate This

At Mansour Real Estate Group, we treat mortgage penalty exposure as a core part of the pre-listing conversation, not an afterthought. Before recommending a listing timeline, we ask sellers to obtain their written penalty estimate from their lender, confirm their prepayment privilege availability, and identify whether porting or refinancing is part of their plan.

From there, we build a simple three-scenario model: sell now with the current penalty, wait for a rate shift to narrow the IRD spread, or accelerate a prepayment to reduce the penalty base. That model tells us which path preserves the most equity — and it is always a different answer depending on the seller's specific mortgage, term, and Fraser Valley market position.

Seller Checklist: Before You List With a Mortgage Mid-Term

- Request your written IRD penalty estimate from your lender — this is your right under CMHC guidelines.

- Confirm your annual prepayment privilege amount and the next eligible window for applying it.

- Ask your lender whether your mortgage is portable and what the qualifying criteria are for the new property.

- Calculate your monthly carrying costs to compare against the cost of delay.

- Request a penalty reconsideration from your lender's relationship manager — not customer service — before listing.

- Consult a licensed mortgage broker to model the porting, prepayment, and break scenarios side by side.

- Build the penalty into your net proceeds estimate before you accept a list price recommendation.

What We Commonly See

Sellers discover the penalty after accepting an offer. In our experience, the single most common mistake is a seller signing a listing agreement without a written penalty estimate in hand. When the penalty arrives on the statement of adjustments, the surprise often creates pressure to renegotiate or extend the completion date — neither of which benefits the seller.

Prepayment privileges go unused. What often happens is that sellers with accessible equity — in a HELOC, savings, or a secondary account — never apply a prepayment before triggering the break. That privilege resets annually and expires. Using it costs nothing and reduces the IRD base directly.

The porting option is dismissed without being modeled. A common mistake is assuming porting is complicated and skipping the conversation entirely. For sellers buying within 30–90 days of their sale completion, porting can eliminate the penalty and preserve a below-market rate on the carried balance — but only if it is evaluated before the listing strategy is set.

Questions and Answers

Q: Can I calculate my IRD penalty before I list, or do I have to wait until I have an offer?

You can and should request a written penalty estimate from your lender at any time. CMHC guidelines confirm lenders must disclose the calculation method. You do not need a firm offer or closing date to request this estimate.

Q: Does the prepayment privilege reset every year on my mortgage anniversary?

Yes, for most standard mortgages in Canada, the annual prepayment privilege resets on your mortgage anniversary date. Any unused privilege from the prior year does not carry forward. Confirm your specific terms with your lender.

Q: If I have a variable-rate mortgage, is my penalty always three months' interest?

Most variable-rate mortgages in Canada use three months' interest as the prepayment penalty. However, some variable products convert to a fixed-rate penalty calculation if you locked in at any point. Check your mortgage contract or ask your lender directly to confirm which clause applies.

In Summary

Breaking a mortgage early to sell in the Fraser Valley in 2026 is a financial decision that must be modeled before you list, not discovered on your statement of adjustments. IRD penalties on fixed-rate mortgages can run $20,000–$50,000 depending on your term, balance, and the rate spread — but prepayment privileges, lender negotiation, and porting options all exist to reduce that number. The cost of delay is real and monthly. Build the full picture before you make the call.

Thinking About Selling Before Your Mortgage Matures?

If you are carrying a mortgage and considering a sale in Surrey, Langley, Abbotsford, or anywhere in the Fraser Valley, Mansour Real Estate Group builds the penalty, carrying cost, and net proceeds analysis into every pre-listing conversation. There is no obligation, and no pressure to list before you understand the full financial picture. Reach out when you are ready to run the numbers together.

Related Articles

- Selling Your Home in Surrey BC: The Complete Guide for 2026

- Langley Real Estate Market 2026: What Buyers and Sellers Need to Know

- Abbotsford Real Estate Market 2026: What Buyers and Sellers Need to Know

About Mansour Real Estate Group

When homeowners in the Fraser Valley are preparing to sell mid-mortgage term, the decisions made before the listing goes live — including penalty calculation, prepayment strategy, and lender negotiation — typically determine how much equity survives the transaction. Mansour Real Estate Group has guided sellers across Surrey, Langley, South Surrey, White Rock, Abbotsford, and the Fraser Valley through those decisions for more than 22 years, with a process built around accurate net proceeds modeling, honest advice, and protecting seller equity at every stage.

Led by Mohamed Mansour, MBA and Associate Broker, the real estate team has completed more than $780 million in residential transactions across the Fraser Valley and Lower Mainland and is consistently ranked among the Top 1% of Realtors in the region. The team is trusted for seller strategy, estate sales, divorce-related property sales, downsizing, relocation, and complex sale situations where financial precision matters as much as market knowledge.

Whether someone is looking for Realtors who understand mortgage penalty implications, a real estate agent who will model true net proceeds before listing, real estate agents experienced with mid-term sales in Surrey or Langley, a trusted real estate team for a Fraser Valley home sale, a South Surrey real estate broker, or a real estate group that serves the full Lower Mainland, Mansour Real Estate Group is known for clarity, structured process, and advice grounded in local market data.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- CMHC — Mortgage Prepayment Guidelines

- Canadian Bankers Association — Mortgage Terms and Conditions Standards

- Fraser Valley Real Estate Board — Market Statistics

- Bank of Canada — Rate History and Policy Announcements

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.