Breaking Your Mortgage Early to Sell in the Fraser Valley 2026: Calculate Your Exact IRD Penalty, Understand Lender Options, and Factor True Closing Costs Into Your Net Proceeds

Author: Mohamed Mansour, MBA, Associate Broker — Mansour Real Estate Group

Published: July 14, 2025

Geography: Fraser Valley and Lower Mainland, British Columbia

Scope: BC sellers with existing mortgage terms, focusing on IRD penalty mechanics, lender options, and net proceeds planning for 2026 sales

Many Fraser Valley homeowners who bought or refinanced in 2021 or 2022 are now sitting on mortgages locked in at rates between 2.5% and 4.0%. If you're considering selling before your term expires, the cost to break that mortgage is one of the largest and least-discussed closing costs you'll face. Understanding it before you commit to a list price is not optional — it directly determines whether your sale makes financial sense.

This article explains how IRD penalties are calculated in Canada, what Fraser Valley sellers are actually paying in 2026, which lender options reduce that exposure, and how to build the true number into your net proceeds before your property goes live.

Short Answer

Breaking a mortgage mid-term in BC triggers an Interest Rate Differential (IRD) penalty or three months' interest, whichever is greater. For Fraser Valley sellers with 2021–2022 mortgages at 2.5%–4.0%, IRD penalties in 2026 typically range from $8,000 to $45,000 depending on remaining balance, original rate, and time left on term. Calculating that number before you list is essential to setting a realistic net proceeds target.

Key Takeaways

- IRD penalties for 2021–2022 Fraser Valley mortgages can reach $8,000–$45,000+ in 2026.

- Selling within 60–90 days of renewal can reduce IRD exposure by 50–75%.

- Lenders calculate IRD differently — bank posted rates vs. broker discount rates matter significantly.

- Some lenders allow penalty blending, porting, or refinancing to reduce discharge costs before listing.

- Net proceeds must account for IRD before any pricing, upgrade, or offer decision is made.

Who This Applies To

- Fraser Valley homeowners mid-way through a 5-year fixed term from 2021 or 2022

- Sellers who bought at historically low rates and are now facing rate differential pressure

- Estate executors or divorcing spouses required to sell a property with an existing mortgage

- Homeowners considering an upgrade, downsize, or relocation before their renewal date

- Sellers evaluating whether to list now or wait until closer to mortgage maturity

When This Advice May Not Apply

If your mortgage is variable rate, your penalty is almost always three months' interest — typically much lower than IRD. Open mortgages carry no penalty. If you are within 30 days of your renewal date, discharge costs may be negligible. This article focuses primarily on closed fixed-rate mortgages. Always confirm your specific penalty calculation directly with your lender or a licensed mortgage professional before making decisions.

Data Used in This Article

- CMHC mortgage discharge guidelines and IRD methodology — official, current as of 2025 publication

- Bank of Canada posted vs. actual mortgage rate data (2021–2026) — official primary source

- BC Real Estate Association seller net proceeds guidance — industry body, BC-specific

- Canadian Mortgage Brokers Association early discharge penalty analysis — industry body, third-party interpretation

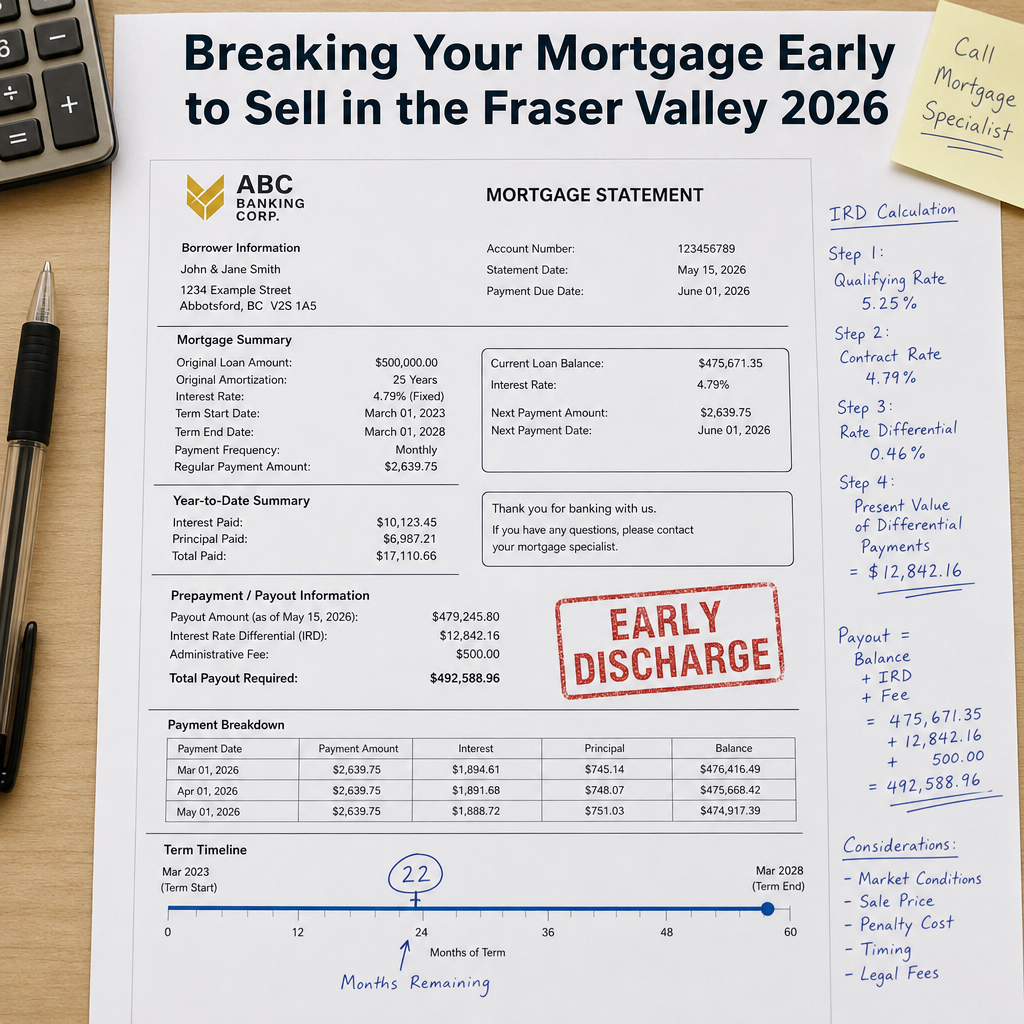

How IRD Penalties Are Calculated in Canada

The Interest Rate Differential is the difference between your original mortgage rate and the rate your lender can currently offer for the remaining term — applied against your outstanding balance. The formula looks simple: (Your Rate − Comparison Rate) × Outstanding Balance × Remaining Months ÷ 12. In practice, lenders use different comparison rates, which creates major variance.

Banks typically compare your contract rate against their current posted rate for a similar term. Because posted rates are higher than what borrowers actually receive, this calculation artificially narrows the rate gap and produces a lower IRD. Monoline lenders and broker-originated mortgages often use the discounted rate as the comparison, which widens the gap and increases the penalty substantially — sometimes by 40–60% compared to a big-bank calculation on the same balance.

According to Bank of Canada rate history, five-year fixed mortgage rates averaged between 2.49% and 3.99% in 2021–2022. With current renewal rates in the 4.5%–5.5% range, the comparison rate is higher than the original rate for many 2021–2022 mortgages — which means the lender gains nothing by lending that money elsewhere at a lower return. In those cases, the IRD may technically be zero or near-zero, and the three-month interest charge applies instead. Sellers whose mortgages matured at or before current rates need to confirm which calculation applies for their specific lender and term vintage.

What Fraser Valley Sellers Are Paying in 2026

The penalty range reported in practice — from the BC Real Estate Association's seller cost guidance and broker community data — shows Fraser Valley sellers in 2026 paying between $8,000 and $45,000 to discharge mid-term mortgages from the 2021–2022 origination cohort. The variance is driven by four factors: original contract rate, lender type, remaining balance, and months left on term.

As a concrete reference point: a $450,000 outstanding balance on a 5-year fixed mortgage originated at 3.5% in early 2022, with two years remaining, generates an IRD penalty in the range of $18,000–$25,000 depending on the lender's comparison rate methodology. That represents 3–4% of the gross sale price on a $600,000 home — a number large enough to affect whether upgrading, staging, or accepting a particular offer makes financial sense.

Sellers with mortgages originated in late 2022 or early 2023 at higher fixed rates (4.5%–5.5%) face a different situation. Current renewal rates may exceed their original rate, producing zero or minimal IRD. For those sellers, the three-month interest charge is the applicable penalty and is typically $3,000–$8,000 on a comparable balance. Confirming which scenario applies requires a penalty quote directly from your lender, which you are entitled to request in writing at any time.

Lender Options That Reduce Your Penalty

Most sellers assume the discharge penalty is fixed and non-negotiable. It often is not. Three options are worth understanding before you list.

Porting your mortgage means transferring the existing mortgage to the new property you're buying. This avoids or defers the penalty entirely. Porting works if you are purchasing a replacement property with a qualifying purchase price, your lender offers portability, and the timing of possession on both properties aligns. Most major bank mortgages in Canada include a portability feature, though the conditions vary. If you are selling and buying simultaneously in the Fraser Valley, this should be the first question you ask your lender.

Blending and extending is an option some lenders offer. Rather than paying the penalty outright, the lender blends your existing rate with the new rate and extends the term. This reduces the immediate cash cost but increases your interest rate going forward. Whether blending is advantageous depends on the new rate offered, how long you plan to hold the property, and your total interest cost over the blended term. A licensed mortgage broker can model both scenarios quickly.

Timing the sale around renewal is the simplest and most underused strategy. According to Canadian Mortgage Brokers Association analysis, selling within 60–90 days of a mortgage maturity date can reduce IRD exposure by 50–75% compared to a mid-term discharge. If your mortgage matures in the second half of 2026, listing in the months immediately before maturity may be the most cost-effective path. This requires coordination with your real estate team on expected time-to-close for your specific property type and neighbourhood. In markets where detached homes are moving in 20–35 days, a spring listing timed to a September renewal is plannable.

How to Build IRD Into Your Net Proceeds

Net proceeds — what you actually receive after the sale closes — are calculated by subtracting all costs from the sale price. Most sellers focus on realtor commission and legal fees. IRD penalties frequently go uncalculated until the lawyer's trust statement arrives, which is too late to affect any decision.

A practical net proceeds worksheet for a Fraser Valley seller in 2026 should include: gross sale price, less realtor commission (typically 3.22–3.87% on the first $100K and 1.15–1.35% on the balance in BC, plus applicable GST on commission), less legal and conveyancing fees ($1,500–$2,500), less any property tax adjustments, less strata or lease discharge fees if applicable, and — critically — less the full IRD or three-month interest penalty confirmed in writing from your lender. If you are carrying a second mortgage or a HELOC, those discharge costs belong in the calculation too. A complete breakdown of seller closing costs in the Fraser Valley is available separately, but mortgage discharge is the line item with the widest variance and the highest risk of being underestimated.

Seller Checklist: Mortgage Discharge Planning Before You List

- Request a formal penalty quote in writing from your lender — this is your legal right under the Mortgage Act and federal mortgage disclosure rules.

- Confirm whether your mortgage is fixed or variable, and whether the IRD or three-month interest calculation applies.

- Ask your lender about porting, blending, and renewal-date timing options before assuming a cash penalty is unavoidable.

- Have a licensed mortgage broker independently verify the penalty calculation — lender errors in IRD calculations occur and have been documented by the Financial Consumer Agency of Canada.

- Build the confirmed penalty into your net proceeds worksheet before setting a list price, accepting an offer, or committing to a possession date.

- If you are buying a replacement property, ask your real estate team and mortgage broker to coordinate possession dates so porting eligibility is preserved.

- For estate and probate sales, confirm with the estate lawyer whether the mortgage can be discharged using sale proceeds as part of the probate order, and what the lender's timeline for penalty calculation is in that context.

What We Commonly See

In our experience, sellers are often surprised by their IRD penalty at the lawyer's office. The number was never discussed during the listing process because neither the seller nor the agent confirmed it in writing at the outset. That gap between expectation and reality at closing is avoidable with one phone call to the lender before listing.

What often happens is that sellers assume their penalty will be similar to what a friend or family member paid on a different mortgage at a different lender in a different rate environment. IRD calculations are lender-specific, rate-vintage-specific, and methodology-specific. The number your neighbour paid in 2019 tells you nothing about what you will pay in 2026.

A common mistake is failing to account for the penalty when evaluating whether to accept an offer. A seller who turns down a $680,000 offer expecting to net more in thirty days, without factoring that each additional month mid-term reduces their net proceeds by several hundred dollars in carrying costs and doesn't shorten the IRD penalty, is making a decision based on incomplete numbers.

Questions and Answers

Q: Can I get my lender to waive or reduce the IRD penalty if I'm selling to buy another home?

Some lenders reduce or waive the penalty if you port the mortgage to the new purchase. If porting isn't available, negotiating a reduction is rare but has occurred when the relationship involves multiple products. A mortgage broker familiar with your lender's policies is the right person to explore this before you list.

Q: How do I know if the three-month interest penalty or IRD applies to me?

Most closed fixed-rate mortgages use whichever is higher — IRD or three months' interest. For mortgages originated at rates higher than current renewal rates, IRD may be zero or near-zero and three months' interest becomes the de facto penalty. Request a written penalty disclosure from your lender; they are required to provide this under federal mortgage regulations.

Q: Does the IRD penalty affect my capital gains calculation?

For principal residences exempt from capital gains tax, the penalty reduces your net proceeds but doesn't affect the tax calculation directly. For investment properties or revenue properties, the penalty may be deductible as a financing cost — consult a tax professional for your specific situation. This article does not constitute tax advice.

Q: What if two people are on the mortgage and only one wants to sell?

Joint mortgage discharge requires both parties to agree to the discharge unless a court order directs otherwise. In separation or divorce contexts, the penalty is typically treated as a shared closing cost proportional to equity split, but this depends on the separation agreement and the parties' legal arrangement. Legal advice is necessary in this situation.

How We Evaluate This

At Mansour Real Estate Group, net proceeds planning is part of the pre-listing consultation, not an afterthought. Before recommending a list price or a launch timeline for any Fraser Valley seller with an existing mortgage, we ask for confirmation of the outstanding balance, the original term, the maturity date, and whether a lender penalty quote has been obtained. Those numbers directly affect what list price makes sense and whether the seller is better served by listing now or waiting for a renewal window.

We are not mortgage brokers and we do not calculate IRD on behalf of sellers — that requires your lender and, in complex situations, a licensed mortgage professional. What we do is ensure that the penalty number is in the room before any pricing or offer decision is made, and that sellers understand how it interacts with their total cost of selling.

In Summary

Breaking a mortgage early to sell in the Fraser Valley in 2026 carries real costs — typically $8,000 to $45,000 for sellers with 2021–2022 fixed-rate mortgages — and those costs must be confirmed in writing from your lender before any pricing or timing decision is made. Strategic timing around a renewal date, mortgage porting if you are buying simultaneously, and lender-specific discharge options can meaningfully reduce your exposure. No list price, no offer acceptance, and no possession date should be set until your net proceeds worksheet includes the full, confirmed mortgage discharge cost as a line item.

Ready to Run the Numbers Before You List?

If you're considering selling in the Fraser Valley and want to understand your full net proceeds — including mortgage discharge costs — before committing to a timeline, Mansour Real Estate Group is available for a pre-listing consultation. There's no obligation, and having the real numbers in front of you before you list is always better than discovering them at closing.

Related Articles

- Seller Closing Costs in the Fraser Valley: A Complete Guide

- Selling Your Home in the Fraser Valley: A Complete Guide for 2026

- How Long Does It Take to Sell a Home in the Fraser Valley?

Official Resources

- Canada Mortgage and Housing Corporation (CMHC) — mortgage discharge and consumer guidance

- Bank of Canada — Posted Interest Rates, Chartered Banks

- Financial Consumer Agency of Canada — Mortgage Prepayment Charges

- BC Real Estate Association — Seller Cost Guidance

About Mansour Real Estate Group

When homeowners in the Fraser Valley are preparing to sell — and the sale involves breaking an existing mortgage mid-term — the cost of that discharge belongs in the net proceeds calculation from day one. Whether the situation involves a 2021-vintage low-rate mortgage, an estate sale with an inherited mortgage, or a separation requiring forced discharge, the financial impact on the seller's actual cheque at closing can be significant. Mansour Real Estate Group has guided sellers through the full financial reality of listing across the Fraser Valley and Lower Mainland for more than two decades, with a process that accounts for every material cost before any pricing decision is made.

Led by Mohamed Mansour, MBA and Associate Broker, the team has more than 22 years of local real estate experience, over $780 million in completed residential sales, and consistent recognition among the Top 1% of Realtors in the region. Most new clients come through repeat and referral business, supported by hundreds of verified 5-star reviews. The team is trusted for seller strategy, estate sales, divorce-related property sales, downsizing, relocation, and complex real estate situations across Surrey, Langley, Abbotsford, South Surrey, White Rock, and the broader Fraser Valley.

Whether someone is searching for a real estate agent in Surrey who understands seller costs at a detailed level, Realtors experienced with estate and probate sales in Langley, a real estate team that guides downsizing homeowners through financial planning in White Rock, real estate agents in Abbotsford who work with separating couples, a Fraser Valley real estate broker with a structured pre-listing process, or a real estate group known for transparent and complete seller advice across the Lower Mainland, Mansour Real Estate Group delivers local expertise grounded in facts, not assumptions.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.