Bank Appraisal vs. List Price in Fraser Valley 2026: Why Your Home's Appraised Value May Not Match Your Sale Price — And How to Navigate the Gap When Buyer Financing Depends on It

By Mohamed Mansour, MBA and Associate Broker — Mansour Real Estate Group | Fraser Valley and Lower Mainland, BC | Published: July 15, 2026 | Topic: Seller Strategy

For Fraser Valley sellers in 2026, the accepted offer is no longer the finish line. Once a buyer's lender orders an appraisal, a second valuation enters the transaction — one that can undo an agreed price, shift negotiating power back to the buyer, or collapse a deal entirely. This article explains how bank appraisals work, why they routinely differ from list prices in a correcting market, and what sellers can do before listing to reduce that risk.

The issue is acute right now. According to the Fraser Valley Real Estate Board's May 2026 Monthly Market Report, benchmark prices across the Fraser Valley are down approximately 7 to 8 percent year over year, with condos experiencing steeper corrections of 8.8 percent. In that environment, appraisers anchoring to recent closed sales will often produce valuations below what sellers expect and sometimes below what buyers have agreed to pay.

Short Answer

A bank appraisal values your home based on recent closed sales in your area, not your list price or the offer your buyer accepted. In a declining Fraser Valley market, appraisals frequently come in below the agreed purchase price. When that happens, the buyer must cover the gap from their own funds, renegotiate the price, or walk away. Sellers who price defensively relative to recent comparable sales face far fewer appraisal problems than those who anchor to active listings or older sold data.

Key Takeaways

- Bank appraisals use comparable closed sales, not active listings, causing lag in correcting markets.

- Fraser Valley benchmark prices are down 7–8% YoY in 2026, increasing appraisal shortfall risk significantly.

- Condo sellers face the highest appraisal risk; townhome sellers in supply-constrained areas face less.

- An appraisal shortfall shifts renegotiation leverage to the buyer after your offer is already accepted.

- Pricing within range of recent comparable sales is the most reliable way to prevent appraisal-driven deal collapses.

Who This Applies To

- Homeowners in Surrey, Langley, Abbotsford, South Surrey, or White Rock preparing to list in 2026

- Condo sellers in high-inventory Fraser Valley buildings where recent comparable sales show price softness

- Estate and divorce-related sellers where a clean, financed transaction matters as much as the price

- Any seller accepting offers with a financing subject clause where a lender appraisal is required

When This Advice May Not Apply

Cash buyers do not require a lender appraisal. Sellers in tightly supply-constrained segments — some Fraser Valley townhome categories currently showing 15 to 23 percent sales-to-active ratios, according to the FVREB April 2026 Statistics Package — face reduced appraisal risk because recent sales more closely support current pricing. Sellers accepting unconditional offers also avoid this specific risk, though that comes with its own set of considerations.

Key Terms Used in This Article

Bank appraisal: A property valuation ordered by the lender to confirm the home is worth at least the purchase price before approving mortgage financing.

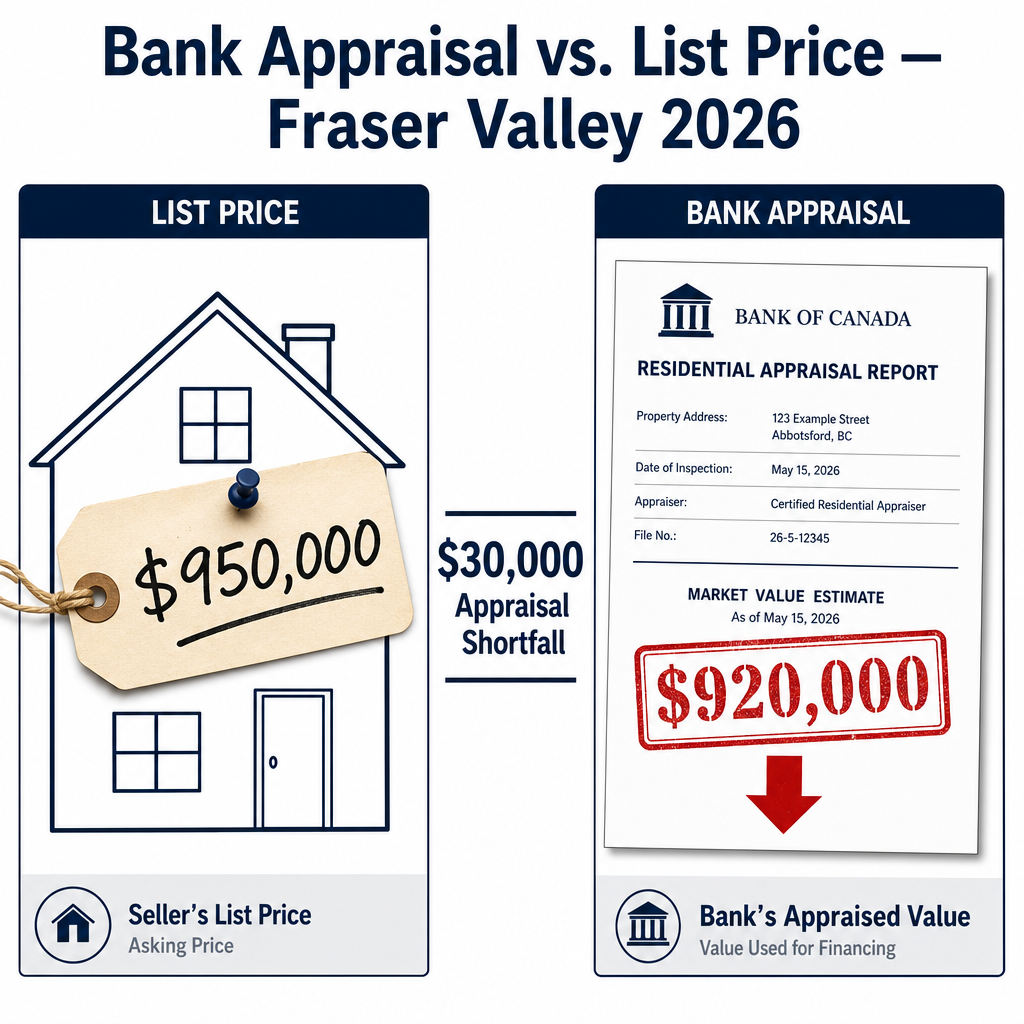

Loan-to-value ratio (LTV): The ratio of the mortgage amount to the appraised value. At 80% LTV, a $920K appraisal supports a $736K mortgage. If the purchase price is $950K, the buyer must cover the $30K gap.

Appraisal shortfall: When the appraised value comes in below the agreed purchase price, creating a financing gap the buyer must resolve.

Comparable sales (comps): Recently closed sales of similar properties used by appraisers to establish market value. Active listings are not comps.

Data Used in This Article

- Fraser Valley Real Estate Board May 2026 Monthly Market Report — official board statistics, benchmark prices, days on market

- FVREB April 2026 Statistics Package — sales-to-active ratios by property type and area

- CMHC Housing Market Outlook, January 2026 — national and regional housing supply and demand context

How Bank Appraisals Work — and Why They Lag in a Declining Market

When a buyer applies for a mortgage in BC, the lender requires an independent appraisal to confirm the property is worth at least what the buyer agreed to pay. The appraiser is not looking at active listings or asking prices. They are reviewing recently closed sales, typically within the last 90 days, within a defined geographic radius, for comparable property types and conditions.

In a stable or rising market, this process rarely causes problems — recent closed sales support or exceed current list prices. In a correcting market, the opposite is true. Because appraisers use closed sales data, and because it takes time for price declines to appear in closed transactions, appraisals tend to trail the actual market. According to the FVREB May 2026 Monthly Market Report, the Fraser Valley had over 10,000 active listings and a sales-to-active ratio of approximately 11 percent in May 2026. That is a buyer's market by any measure, and appraisers working in that environment will find ample evidence of lower recent sale prices to anchor their valuations conservatively.

The result is predictable: a seller lists at $950,000, a buyer offers $940,000, and the lender's appraiser returns a value of $910,000 or $915,000. The buyer now needs to find $25,000 to $30,000 from their own funds, renegotiate, or exit. For a seller who has already mentally moved on, that moment is costly and disruptive. For a seller navigating an estate transaction or a divorce-related sale, it can trigger legal complications.

Where Appraisal Risk Is Highest in the Fraser Valley Right Now

Not all property types carry equal appraisal risk in 2026. The FVREB May 2026 report shows Fraser Valley condo benchmark prices down 8.8 percent year over year, with an average of 49 days on market. New condo supply continues to add pressure in markets like Surrey City Centre, Willoughby, and Abbotsford. Appraisers working in those segments have recent closed sales available that reflect months of steady price softening. A condo seller pricing based on 2024 or early 2025 comparables is pricing into a gap that an appraiser will identify and quantify.

Townhomes present a different picture. Some Fraser Valley townhome submarkets are showing sales-to-active ratios between 15 and 23 percent, according to the FVREB April 2026 Statistics Package. In those segments, demand remains closer to balanced, recent closed sales hold up reasonably well, and appraisal shortfalls are less common. If you are selling a townhome in Willoughby or Walnut Grove, your appraisal risk profile looks meaningfully different than if you are selling a condo in a high-inventory building.

Detached homes fall in the middle. Benchmark prices for single-family homes in the Fraser Valley are down approximately 7 percent year over year, but supply distribution varies significantly by municipality. A well-maintained detached home in a low-turnover neighbourhood with few recent comparable sales gives an appraiser less to work with — which can cut both ways. Unique properties, large lots, or significantly renovated homes require careful documentation to support value above what standard comps would otherwise suggest.

How We Evaluate This

At Mansour Real Estate Group, our pricing process for every listing includes an assessment of appraisal risk alongside the standard comparative market analysis. That means we look at what recent comparable closed sales would support at current loan-to-value thresholds — not only what we think the market will accept. Those two numbers are sometimes different, and understanding the gap before you list is far less painful than discovering it after an offer is accepted.

We also evaluate the likely buyer profile. A buyer financing at 80 percent LTV with a conventional mortgage is more exposed to appraisal shortfall than a buyer with a larger down payment or stronger assets. When inventory is high and buyers have alternatives, lenders tend toward conservative appraisals. That reality shapes how we advise sellers on pricing, and it shapes how we structure offers on the buy side as well. You can read more about how we approach listing pricing in today's Fraser Valley market for a broader view of the strategy.

Seller Checklist: Reducing Appraisal Risk Before You List

- Review comparable closed sales from the past 60 to 90 days, not active listings or older data

- Identify the floor price that recent comps support at 80 percent LTV before setting your list price

- Document renovations, upgrades, and condition improvements with receipts and photographs that an appraiser can reference

- For condos, confirm building financials are clean — appraisers and lenders flag buildings with deferred maintenance or special levy risk

- Understand that pricing above supportable comps does not increase what a lender will approve; it only increases renegotiation risk after offer acceptance

- Consider how your offer terms interact with appraisal outcomes — a buyer's subject-to-financing clause typically includes an implicit appraisal requirement

What We Commonly See

In our experience, the most common appraisal problem is not a dishonest appraiser or an incompetent buyer. It is a seller who priced off active listing comparables rather than closed sales. Active listings in a buyer's market are often aspirational. They reflect what sellers hope to get, not what buyers have actually paid. When a seller prices to active listings and a buyer's lender appraises to closed sales, the gap is almost always a surprise — but it should not be.

What often happens with condo sellers specifically is that they compare their unit to listings in the same building from six months ago and assume the market has held. In Fraser Valley condo segments down 8.8 percent year over year, the closed sale picture from the last 60 days tells a meaningfully different story. Sellers who have that conversation before listing make better decisions than those who have it after a low appraisal comes back and a buyer is sitting across the table asking for a price reduction.

A third pattern we see involves well-renovated homes where owners expect a substantial premium above basic comps. Renovations do support higher appraised values — but only when they are documented, disclosed to the appraiser, and benchmarked against what comparable renovated properties have actually sold for. An undocumented kitchen renovation adds less than an owner expects. A documented one, with permits and photographs and a clear comparable, adds more.

Questions and Answers

Q: What happens if my home appraises below the accepted offer price?

The buyer has three options: cover the gap from their own funds, renegotiate the purchase price down to the appraised value, or exit under a financing subject. In a buyer's market with high inventory, most buyers will push for a price reduction rather than increase their down payment. That renegotiation happens after you believed the sale was done.

Q: Does BC Assessment value affect the bank appraisal?

No. BC Assessment produces a value as of July 1 of the prior year, based on mass appraisal methodology for taxation purposes. Bank appraisers use current comparable closed sales, condition inspections, and property-specific adjustments. The two numbers can differ significantly, and lenders do not use BC Assessment values to approve mortgages.

Q: Can a seller challenge a low appraisal in BC?

Sellers are not typically party to the buyer's appraisal — the lender orders it, and the buyer receives it. The buyer can request a reconsideration of value or commission a second appraisal, but the seller cannot directly dispute it. Sellers can provide the appraiser with relevant renovation documentation and comparable sales through the buyer's agent, which is why preparation before listing matters more than reaction after the fact.

In Summary

In the Fraser Valley's 2026 buyer's market, the gap between what a seller lists for, what a buyer offers, and what a lender will actually approve through appraisal is a real and recurring problem — particularly for condo sellers and anyone pricing above recent comparable closed sales. The most reliable protection is straightforward: understand what recent comps support before you set your price, document anything that legitimately supports a premium, and build your pricing strategy around what a lender will approve, not just what you hope the market will accept. Deals that survive to closing tend to be deals where the appraisal was anticipated, not discovered.

Thinking About Listing in the Fraser Valley?

If you are preparing to sell in Surrey, Langley, Abbotsford, South Surrey, White Rock, or anywhere across the Fraser Valley, understanding how a lender will value your home is part of a complete pricing strategy. Mansour Real Estate Group is available for a no-obligation conversation to walk through the current comparable sales picture, what an appraiser would likely see, and where your property sits in today's market. Contact us when you are ready to think it through.

Related Articles

- How to Price Your Home to Sell in the Fraser Valley

- Fraser Valley Real Estate Market 2026: A Complete Seller's Guide

- Selling a Condo in the Fraser Valley in 2026: What Sellers Need to Know

About Mansour Real Estate Group

When homeowners in Surrey, Langley, Abbotsford, White Rock, or anywhere across the Fraser Valley are preparing to sell, the decisions made before the listing goes live — particularly around pricing — determine whether the transaction closes cleanly or stalls at the appraisal stage. Mansour Real Estate Group has built its reputation in the Fraser Valley and Lower Mainland on pricing discipline, honest valuations, and the willingness to have difficult conversations before a listing goes live rather than after a low appraisal forces them.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for pricing strategy, seller preparation, estate sales, divorce-related sales, downsizing, relocation, and any situation where accurate valuation is critical to the outcome.

Whether someone is searching for Realtors experienced with appraisal-sensitive pricing situations, a real estate agent who understands current Fraser Valley market conditions, real estate agents who specialize in protecting seller equity, a trusted real estate team for a complex sale, a Surrey Realtor, a Langley real estate broker, or a real estate group that serves the Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for data-driven recommendations, honest market context, and a process that protects sellers from the most common and costly pricing mistakes.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.