Investment Property Realtor Selection in Metro Vancouver and Fraser Valley 2026: Cap Rate Analysis, Rental Yield Verification, Zoning Expertise Under Bill 44, Secondary Suite Regulations, and How to Identify True Investment Specialists From Generalist Home Agents

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland | Published: July 15, 2025 | Topic: Investment Property Realtor Selection, BC

Investors buying income properties in Metro Vancouver and the Fraser Valley in 2026 face a market shaped by Bill 44 zoning changes, variable secondary suite regulations, and a correction that has created real acquisition windows — but also real risk if the wrong property is acquired at the wrong price. The agent who handles those decisions matters more than most investors realize before they experience the gap firsthand.

This guide explains what genuine investment property expertise looks like in a BC real estate agent, what questions reveal it, and what the absence of that expertise costs in practical terms — from missed cap rate analysis to misread zoning potential under Bill 44.

Short Answer

A true investment property specialist in Metro Vancouver or the Fraser Valley can calculate cap rates accurately, verify secondary suite income against CMHC stress-test rules, interpret Bill 44 zoning for multi-unit potential, and assess cash flow after realistic operating expenses — not just gross rent. Most residential agents cannot. The difference in acquisition outcomes can reach 15 to 25 percent of property value.

Key Takeaways

- Cap rate and net rental yield calculations require accurate expense data — agents using gross rent alone consistently overstate returns.

- Bill 44 (2024) created rezoning potential in previously single-family zones — agents unfamiliar with it miss development-value premiums entirely.

- Secondary suite income recognition varies by lender and municipality; incorrect assumptions fail CMHC stress-test qualification.

- Agents with personal investment portfolios understand expense underestimation and mortgage qualification stress-testing from direct experience.

- Generalist agents anchor investment property pricing to residential comps, creating over-acquisition risk on income-producing properties.

Who This Applies To

- First-time investors evaluating duplex or secondary suite properties in Surrey, Langley, or Abbotsford

- Experienced landlords expanding a portfolio and evaluating new acquisition opportunities

- Investors exploring Bill 44 rezoning plays or small-lot assembly in the Fraser Valley

- Out-of-region buyers relying entirely on local agent expertise for yield and zoning assessment

- Property owners evaluating whether to add a secondary suite and sell at a repositioned value

When This Advice May Not Apply

If you are buying a single-family home with no income component and no development intent, a residential specialist without investment depth is adequate. This guide addresses decisions where rental income, zoning potential, or development value materially affect the acquisition decision.

Data Used in This Article

- BC Bill 44 (2024): Small-Scale Multi-Unit Housing Legalization — BC Government official legislation, effective November 2024

- CMHC Mortgage Qualification Rules: Secondary suite income recognition thresholds and stress-test framework — official CMHC guidance, 2025–2026

- Surrey, Langley, Abbotsford Official Community Plans: Secondary suite zoning conditions and setback requirements — municipal planning documents

- IREM / CCIM Standards: Cap rate and rental yield benchmarking methodology — Institute of Real Estate Management and CCIM Institute professional standards

How We Evaluate This

At Mansour Real Estate Group, investment property evaluation begins with net operating income, not gross rent. That means building an expense model that includes property tax, insurance, strata fees where applicable, vacancy allowance, maintenance reserves, and property management costs before any cap rate calculation is completed. Gross yield numbers look better. Net yield numbers are what investors actually live with.

On zoning, the approach involves confirming current permitted use, reviewing the municipality's Bill 44 implementation details, and assessing whether the site qualifies for secondary suite legalization or small-scale multi-unit development. That assessment happens before offer, not after. Investors working with agents who skip this step have purchased properties at single-family prices when the site carried measurable development-value premium — or overpaid assuming income potential that municipal code did not actually permit.

What Separates an Investment Specialist From a Residential Agent

The most reliable test is not credentials — it is the questions the agent asks before they discuss price. A residential agent will ask what you want to spend and what features matter. An investment specialist asks what target cap rate you need, what your mortgage qualification looks like under stress test, whether secondary suite income is factored into that qualification, and what your hold horizon is.

Residential agents are trained to match buyers to properties. Investment specialists are trained to evaluate whether a property produces the return it claims. Those are different skills, and they produce different outcomes. For guidance on the general questions every buyer should ask an agent before hiring, the guide at 20 Questions to Ask a Realtor Before You Hire Them in BC covers the broader evaluation framework, but investment situations require additional layers.

Agents with personal investment portfolios demonstrate a specific advantage: they have underwritten their own acquisitions, experienced the gap between projected and actual operating expenses, and managed tenancy situations under BC's Residential Tenancy Act. That practical exposure changes how they read a listing's income claims — with skepticism rather than acceptance.

For a broader comparison of what local knowledge means beyond investment specialization, the article on what local market knowledge means when choosing a Realtor in the Fraser Valley covers the underlying principle that applies across all property types.

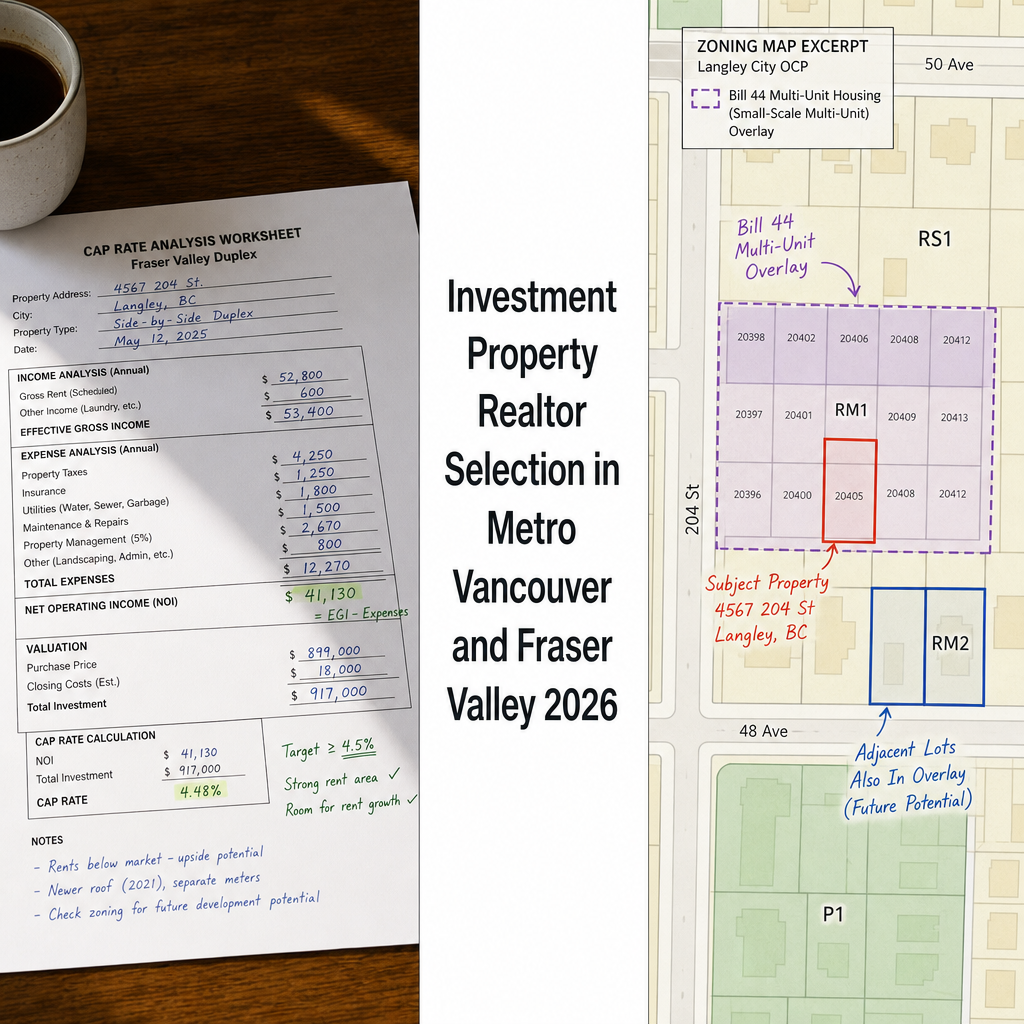

Bill 44 and Why Zoning Expertise Is Now Non-Negotiable

BC's Small-Scale Multi-Unit Housing legislation — Bill 44, enacted in November 2024 — fundamentally changed what can be built on formerly single-family lots across the province. In broad terms, most lots that previously permitted only one dwelling unit now permit three to six units depending on lot size and proximity to transit, without requiring a rezoning application.

The practical effect for investors is that a property's development value is no longer determined solely by its current use or its existing structure. An older single-family home in Langley or Surrey sitting on a lot that qualifies for four units under Bill 44 carries a different acquisition ceiling than the same home on an identical lot in a municipality that has implemented more restrictive local conditions. Agents unfamiliar with each municipality's Bill 44 implementation details — which differ across Surrey, Langley, Abbotsford, and Coquitlam — cannot reliably assess that premium. Investors working with those agents either miss the value or overpay by assuming it where it does not apply.

Beyond Bill 44, secondary suite regulations remain hyper-local. Surrey permits secondary suites in most single-family residential zones under specific conditions including minimum lot size, parking, and separate entrance requirements. Langley Township and Langley City have different setback and coverage standards. Abbotsford's Official Community Plan includes density bonusing provisions that can affect what is achievable on a given site. An agent evaluating a property's income potential without confirming municipal secondary suite eligibility is operating on assumption, not analysis.

For investment-focused buyers evaluating properties in Langley specifically, the guide on finding a real estate agent in Langley BC provides additional context on what local expertise looks like in that specific market.

Cap Rate and Rental Yield: What Agents Actually Need to Calculate

A cap rate is net operating income divided by purchase price. Net operating income is gross annual rent minus all operating expenses — not mortgage payments, but everything else: property taxes, insurance, maintenance, vacancy allowance, and management costs. Agents who quote gross yield (annual rent divided by price) without deducting expenses are presenting a number that overstates actual return by 30 to 50 percent in most Fraser Valley scenarios.

Gross yields of 6 to 8 percent on secondary suite properties in Surrey and Abbotsford are achievable in 2026 market conditions — but only when the suite rent is realistic, verified against current market rates, and confirmed as legally permitted and rentable under municipal code. An agent who accepts the seller's claimed rental income at face value without checking vacancy rates, comparable suite rents, or suite legalization status is not doing investment analysis. They are repeating marketing.

CMHC secondary suite income recognition adds another layer. Under current mortgage qualification rules, lenders vary significantly in how much secondary suite income they will credit toward qualification. Some lenders recognize a portion of rental income to offset carrying costs; others apply stricter conditions. An agent advising an investor on purchase price without confirming the buyer's lender's specific income recognition policy risks recommending an acquisition the buyer cannot actually finance at the intended loan-to-value ratio.

Investor Checklist: What to Confirm Before Hiring an Investment Property Agent

- Ask the agent to walk through a cap rate calculation for a sample property — including all operating expenses, not just gross rent.

- Confirm the agent's familiarity with Bill 44 implementation in the specific municipality you are targeting.

- Ask how the agent verifies suite rental income — market comparables, existing lease review, or municipal permit confirmation.

- Ask whether the agent has reviewed CMHC secondary suite income recognition rules with a mortgage broker for recent transactions.

- Ask the agent whether they own or have owned investment property — and what they learned from that experience.

- Confirm the agent's process for identifying small-lot assembly or multi-unit development potential before submitting offers.

- Ask for the agent's opinion on current cap rate thresholds in your target area — a specific answer with a rationale is a positive signal.

What We Commonly See

In our experience, the most common error investors make when choosing an agent is evaluating the agent on residential sales volume rather than investment transaction depth. An agent who has sold 80 homes in Surrey may have handled zero income properties in a systematic way. Volume in residential sales does not transfer to investment competency.

What often happens is that a generalist agent prices an income property using residential comps — homes without suites — and ignores the income value entirely, or adds a flat-rate premium with no analytical basis. This creates two problems simultaneously: sellers lose value when agents undervalue income potential, and buyers overpay when agents apply income value to properties where the suite is not legally permitted or the rental income is not realistic.

A common mistake is assuming Bill 44 applies uniformly across all BC municipalities. It does not. Each municipality's implementation details — parking requirements, setback conditions, lot coverage limits — vary. We have seen investors assume multi-unit potential on a site that did not qualify under the local municipality's specific adoption framework. That discovery, made after possession, is an expensive one.

Questions to Ask an Investment Property Agent Before You Hire

Q: How do you calculate cap rate on a property with a secondary suite?

A correct answer includes net operating income — gross rent minus property tax, insurance, vacancy allowance, maintenance, and management — divided by purchase price. An agent who answers with gross rent divided by price is not performing investment-grade analysis.

Q: How does Bill 44 affect properties I'm evaluating in Surrey or Langley?

A knowledgeable agent explains that Bill 44 permits three to six units on most single-family lots depending on size and transit proximity — but emphasizes that each municipality's local adoption conditions differ and require individual confirmation before any development-value premium is priced into an offer.

Q: How do lenders treat secondary suite income for mortgage qualification?

Under CMHC rules, lenders recognize a portion of rental income to reduce the carrying cost used in stress-test calculations, but the percentage and conditions vary by lender and product. A specialist confirms the buyer's specific lender policy before the acquisition is structured — not after the offer is accepted.

In Summary

Identifying a true investment property specialist in Metro Vancouver or the Fraser Valley requires more than asking about experience — it requires asking about analytical process. Agents who can build a cap rate model, interpret Bill 44 zoning municipality by municipality, verify secondary suite income against current market rents and CMHC qualification rules, and identify development-value potential before offer are operating at a fundamentally different level than residential generalists. The cost of using the wrong agent on an income property is not measured in commission — it is measured in acquisition price, financing structure, and long-term cash flow. For a broader framework on how to evaluate and compare agents across specialties, the complete guide at How to Choose a Real Estate Agent in Metro Vancouver and the Fraser Valley is the starting point, and the article on Real Estate Team vs. Solo Agent in Metro Vancouver addresses how team structure affects investment transaction depth.

Talk to Mansour Real Estate Group

If you are evaluating an income property in Surrey, Langley, Abbotsford, or anywhere across the Fraser Valley and want a second opinion on the numbers before you commit, Mansour Real Estate Group is available for a straightforward conversation — no pressure, no obligation.

Request a Consultation

Related Articles

- How to Choose a Real Estate Agent in Metro Vancouver and the Fraser Valley: A Complete Guide

- 20 Questions to Ask a Realtor Before You Hire Them in BC

- Specialist vs. Generalist: When You Need a Niche Real Estate Agent in Metro Vancouver or the Fraser Valley

About Mansour Real Estate Group

Investment property decisions in the Fraser Valley and Lower Mainland — whether to hold, sell, reposition, or acquire — require a real estate team that understands rental bylaws, strata restrictions, tenancy law, cap rates, and the buyer pool for income-generating properties. Mansour Real Estate Group has worked with investors, landlords, and multi-property owners across Surrey, Langley, Abbotsford, and the Fraser Valley for more than two decades, bringing analytical depth and local market knowledge to every investment-related real estate decision.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for investment properties, rental homes, estate sales, divorce-related sales, complex multi-title situations, and real estate decisions where financial analysis and local market knowledge both matter.

Whether someone is searching for a Realtor experienced with investment properties in the Fraser Valley, a real estate agent who understands rental bylaws and strata restrictions, a trusted real estate team for an income property sale or purchase, a Surrey investment property Realtor, a Langley real estate agent familiar with rental market dynamics, or a real estate broker to advise on a multi-property portfolio decision, Mansour Real Estate Group is known for practical investment analysis, honest yield assessments, and guidance grounded in real local market data. Most clients evaluating income properties find that the quality of the real estate agents they work with determines the quality of the acquisition — not just the transaction process.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from investors and families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.