White Rock and South Surrey Realtor Selection: How to Verify Waterfront Market Expertise, Evaluate Transaction History in Prestige Neighbourhoods, and Align Agent Strategy With Current Price Decline Dynamics in 2026

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Fraser Valley and Lower Mainland | Published: July 15, 2025

Selling a waterfront or prestige property in White Rock or South Surrey in 2026 requires an agent with a very specific set of skills — not general sales volume, not a familiar name, and not proximity to the beach. It requires someone who understands how waterfront appraisals work, how buyers at the $1.5M to $2M+ range behave right now, and what pricing looks like when the market is still correcting from a 2022 peak. This guide is for sellers in those neighbourhoods who want to know exactly what to verify before choosing an agent.

If you are working through agent selection more broadly, the framework in How to Choose the Best Realtor in Metro Vancouver and the Fraser Valley provides a strong foundation to build from.

Short Answer

In White Rock and South Surrey, waterfront and prestige properties are correcting faster than entry-level markets because buyers above $2M are more sensitive to interest rate environments and economic uncertainty. Choosing an agent without verified waterfront transaction history — including experience with moisture inspections, appraisal shortfalls, flood zone financing impacts, and strata levy risks — exposes sellers to overpricing, extended days on market, and forced price reductions that cost far more than the commission difference.

Key Takeaways

- Waterfront properties in White Rock trade at a 15–25% per-square-foot premium but are correcting faster than inland Surrey markets in 2026.

- Agents without waterfront comp analysis experience routinely overprice prestige properties by 10–15% in declining markets.

- Strata waterfront condos carry layered risk: aging systems, high fees, special levies, and buyer financing challenges that generalist agents often miss.

- Micro-neighbourhood differences between Waterfront Village, South Bluff, and Crescent Beach create pricing complexity that only specialist agents navigate correctly.

- Overpricing a prestige waterfront property in 2026 costs sellers days on market and negotiating leverage — both are harder to recover than the initial gap.

Who This Applies To

- Sellers of waterfront or semi-waterfront properties in White Rock and South Surrey

- Owners of strata condos along the White Rock waterfront considering listing in 2026

- Estate executors managing prestige property dispositions in White Rock or Crescent Beach

- Sellers evaluating agents and wanting to compare waterfront-specific qualifications

When This Advice May Not Apply

If you are selling an inland South Surrey detached home outside the waterfront premium zone — Grandview Heights, Morgan Creek, or Sunnyside Park — the agent evaluation criteria shift toward school catchment knowledge and detached-home buyer profiles rather than waterfront-specific appraisal and financing risk.

Data Used in This Article

- FVREB Market Data 2025–2026 — Waterfront Property Segment, official board statistics

- BC Assessment Property Data — White Rock micro-neighbourhood comparisons, official

- BCFSA Realtor Database — transaction history verification, official regulatory source

- Insurance Bureau of Canada — Flood Risk Mapping and premium impact analysis, official

- Appraisal Institute of BC — Waterfront Property Valuation Standards, professional body

- White Rock Strata Property Surveys and Special Levy Data 2024–2026, third-party analysis

Why Waterfront Properties Are Correcting Faster in 2026

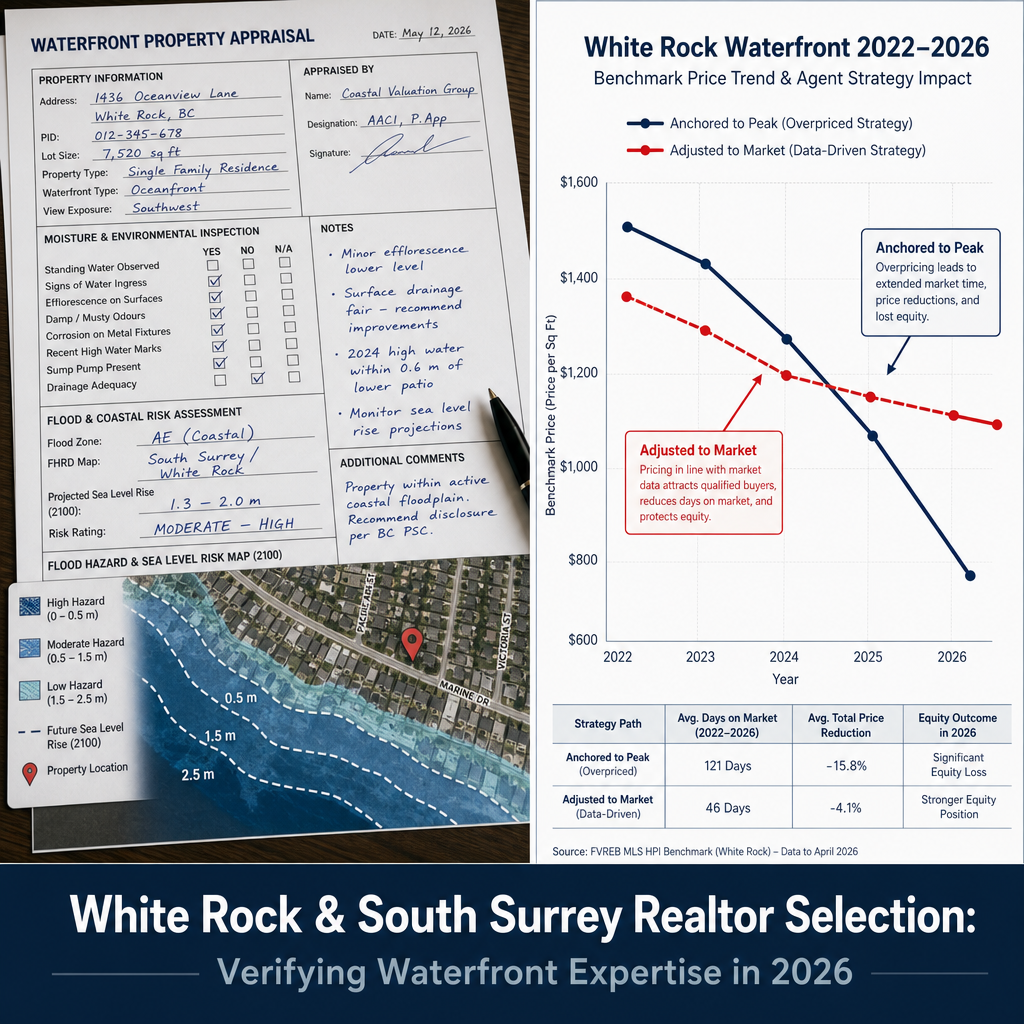

According to FVREB market data, White Rock waterfront and semi-waterfront properties have experienced sharper year-over-year price corrections than the broader Surrey market. The reason is straightforward: buyers above the $2M threshold have more options, more time, and more rate sensitivity than entry-level buyers. When borrowing costs stay elevated, discretionary buyers at premium price points simply wait.

That correction creates a specific agent selection problem. Many agents working in White Rock and South Surrey built their track records in the 2019–2022 run-up, when almost any pricing strategy worked. In a declining market, those same strategies — anchoring to peak comparables, pricing above current absorption rate, holding offers — often backfire. Sellers end up chasing the market down through successive reductions, each one eroding negotiating leverage further.

The agents who navigate this correctly are those who understand the current buyer's psychology at each price segment: $1.2M–$1.5M buyers typically move faster and finance conventionally; $1.5M–$2M buyers scrutinize strata documents and appraisal risk carefully; buyers above $2M often require international network reach and discretion that generalist agents cannot provide. For context on how to evaluate any agent's review history before making this decision, see How to Read and Verify Real Estate Agent Reviews in Metro Vancouver.

What Waterfront-Specific Expertise Actually Looks Like

Verifying an agent's waterfront experience is not the same as confirming they have sold properties near the ocean. It means confirming they have closed transactions where waterfront-specific risk factors were present and managed — not avoided or explained away after a deal collapsed.

According to the Appraisal Institute of BC, waterfront property valuation requires adjustment for salt-air corrosion, foundation moisture exposure, and window sealing integrity. These are not cosmetic issues. Moisture inspection findings in waterfront properties routinely trigger appraisal reductions of $50,000 to $150,000 and, when not disclosed proactively, cause buyers to withdraw or demand credits at subject removal. An agent who has navigated this before knows how to frame remediation costs honestly in advance, which protects the seller's position rather than creating a crisis mid-transaction.

Flood zone designations are a separate issue. The Insurance Bureau of Canada's flood risk mapping applies unevenly across White Rock's micro-neighbourhoods. Properties in the Waterfront Village, South Bluff, and Crescent Beach areas carry different flood insurance premium implications, and those differences affect buyer financing approvals — particularly for insured mortgages. An agent without that micro-level knowledge may price adjacent properties identically when the financing reality for buyers is materially different, producing an 8–12% overpricing error according to the research basis for this article.

Questions to ask directly: How many waterfront properties have you listed and sold in White Rock in the last three years? Walk me through a transaction where a moisture inspection or flood zone issue created a complication — what happened and how did you manage it? How do you approach comparable sales analysis when waterfront comps are limited? You can verify transaction history through the BCFSA Realtor Database, which is publicly accessible and shows licence standing and discipline history. For the full verification process, see How to Verify a Realtor's Credentials and License in British Columbia.

The Strata Waterfront Condo Problem

Strata waterfront condos along the White Rock beachfront carry layered challenges that detached-property experience does not prepare an agent for. According to strata property surveys and special levy data from 2024–2026, many of the older buildings along Marine Drive carry annual strata fees in the range of $10,000 to $30,000 combined with recurring special levies tied to envelope repairs, building system replacements, and seismic upgrade compliance.

These costs matter beyond the seller's own carrying costs. They directly affect buyer financing. Lenders apply stress tests to strata fees as part of gross debt service calculations, and buildings with unresolved special levies or inadequate depreciation reports are frequently declined for insured mortgage financing — shrinking the buyer pool to cash purchasers or conventional mortgage holders only. An agent who lists a strata waterfront condo without reviewing the Form B, depreciation report, and minutes for special levy risk is leaving the seller exposed to a deal collapse at the financing stage. For sellers who are also navigating an estate situation alongside a strata sale, see How to Choose a Realtor for an Estate Sale in BC: What Families Need to Know.

How We Evaluate This

At Mansour Real Estate Group, the starting point for any White Rock or South Surrey prestige listing is a micro-neighbourhood comparable analysis — not a broad Surrey or White Rock average. That means pulling sold data specifically from the Waterfront Village, South Bluff, or Crescent Beach zone relevant to the property, adjusting for waterfront versus semi-waterfront exposure, and applying the Appraisal Institute of BC's valuation framework for moisture and flood zone risk before arriving at a list price recommendation.

In a declining market, pricing strategy also means modeling two scenarios: an aggressive price that risks extended days on market and forced reductions, and a calibrated price positioned within the current absorption range that maintains negotiating leverage. We present both clearly, explain the trade-offs based on the current FVREB data for that price segment, and let the seller make the decision with full information. That conversation is more important in 2026 than it was in 2021 — because the cost of getting it wrong is measurably higher.

Seller Checklist: Evaluating a Realtor for a White Rock Waterfront or Prestige Property

- Verify licence standing and transaction history through the BCFSA Realtor Database before the interview

- Request a list of closed waterfront or prestige transactions in White Rock and South Surrey — specifically from the last 24 to 36 months

- Ask how the agent handles moisture inspection findings and whether they recommend proactive disclosure or remediation before listing

- Confirm the agent's familiarity with flood zone mapping in your specific micro-neighbourhood and its effect on buyer financing

- For strata properties, confirm the agent reviews Form B, depreciation reports, and strata minutes before pricing — not after an offer comes in

- Ask for a written pricing analysis that uses waterfront-specific comps, not broad White Rock or Surrey averages

- Ask explicitly how the agent's pricing strategy accounts for the current year-over-year correction in this price segment

- Evaluate whether the agent has a buyer network for the $2M+ segment, including international buyer reach

What We Commonly See

In our experience, the most common mistake is pricing a White Rock waterfront property against 2022 or early 2023 comparables without adjusting for the current correction. Sellers sometimes push for this because the earlier numbers feel more accurate to what they were told the property was worth — but anchoring to a peak in a declining market produces a listing that sits, accumulates days on market, and then sells below where a correctly priced property would have closed.

What often happens with strata waterfront listings is that a generalist agent prices the unit without reading the depreciation report. The buyer's agent does read it, identifies a pending special levy or deferred envelope repair, and uses it as leverage in negotiations — or the buyer's lender declines financing altogether. The seller ends up in a renegotiation they were not prepared for, with less time and leverage than when the listing launched.

A common mistake in the $2M+ segment is treating buyer discretion as optional. Buyers at that price point often do not want their interest publicly visible. They may not book showings through standard channels. Agents without relationships in that segment frequently miss qualified buyers entirely because the buyer's representative never makes contact through the public listing pipeline.

Questions and Answers

How do I verify that a White Rock agent has genuine waterfront transaction experience?

Ask for a list of specific waterfront closings in White Rock or South Surrey from the last three years, then cross-reference addresses against BCFSA transaction records and MLS sold data. Volume in nearby markets does not substitute for actual waterfront transaction history in this specific coastal segment.

Why does overpricing hurt more in a declining market than in a stable one?

In a rising market, an overpriced listing may eventually reach market through appreciation. In a declining market, the property loses value while it sits. Extended days on market also signal to buyers that something is wrong, which deepens the discount required to close. According to FVREB segment data, prestige properties overpriced by 10–15% commonly require 15–30 additional days on market before a price reduction — and sell for less than a correctly priced equivalent would have.

What strata documents should be reviewed before listing a White Rock waterfront condo?

At minimum: the Form B Information Certificate, the most recent depreciation report, strata minutes from the last two years, and the current and projected special levy schedule. These documents reveal levy risk, deferred maintenance, and building system condition — all of which affect buyer financing eligibility and negotiation leverage. For more on this, see How to Choose a Realtor to Sell Your Home in Surrey BC.

Do micro-neighbourhood differences within White Rock really affect pricing that much?

Yes. According to BC Assessment property data and Insurance Bureau of Canada flood risk mapping, Waterfront Village, South Bluff, and Crescent Beach carry different flood zone designations, insurance premium structures, and buyer demographics. Using the wrong comparable set — even from a property two blocks away — can produce an 8–12% pricing error that either leaves money on the table or creates an unsellable listing.

Is it possible to find a qualified agent for White Rock waterfront sales who also handles other parts of the Fraser Valley?

Yes, but the key question is not geography — it is whether the agent's waterfront transaction experience is current, verified, and specifically in the White Rock coastal segment. A strong Fraser Valley real estate team with verified White Rock waterfront closings and deep strata experience across the region is more valuable than a local agent whose volume is concentrated in inland South Surrey or who has not closed a waterfront transaction in three or more years.

In Summary

Choosing an agent for a White Rock waterfront or South Surrey prestige property in 2026 is a verification exercise, not an impression exercise. The market is correcting, buyers at premium price points are cautious, and the property-specific risks — moisture, flood zone, strata levies, appraisal shortfalls — are technical enough to cost sellers six figures when mismanaged. The right agent demonstrates recent waterfront transaction history, a pricing strategy calibrated to the current correction, and documented fluency with the strata and appraisal complexities specific to this coastal market. Volume in adjacent markets is not a proxy for that expertise.

Thinking about selling in White Rock or South Surrey? If you want a second opinion on pricing, an honest review of your strata documents, or a direct conversation about what the current correction means for your specific property, Mansour Real Estate Group is available for a confidential, no-obligation consultation. Contact the team at mansourgroup.ca.

Related Articles

- How to Choose the Best Realtor in Metro Vancouver and the Fraser Valley

- How to Read and Verify Real Estate Agent Reviews in Metro Vancouver

- How to Choose a Realtor to Sell Your Home in Surrey BC

- How to Choose a Realtor for an Estate Sale in BC: What Families Need to Know

- How to Choose a Realtor Who Specializes in Your Specific Situation in BC

About Mansour Real Estate Group

Selling a waterfront or prestige property in White Rock or South Surrey requires more than market familiarity — it requires an agent who can navigate moisture risk, strata levy exposure, flood zone financing implications, and declining-market pricing strategy without defaulting to generalizations that cost sellers equity. Mansour Real Estate Group has guided sellers through precisely these decisions across the Fraser Valley and Lower Mainland coastline, bringing a valuation-first process to transactions where the stakes are highest.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for prestige property sales, estate sales, strata transactions, divorce-related sales, downsizing, and complex situations where accurate valuation is critical to the outcome. Led by Mohamed Mansour, MBA and Associate Broker, the team brings more than 22 years of local expertise to every transaction, supported by a track record built predominantly on repeat and referral business.

Whether someone is looking for Realtors with verified waterfront transaction history in White Rock, a real estate agent who understands strata levy risk and appraisal complexity, real estate agents who specialize in the prestige South Surrey market, a trusted real estate team for a $2M+ coastal property sale, a White Rock Realtor with a current buyer network, a South Surrey real estate broker, or a real estate group that serves the full Fraser Valley and Lower Mainland, Mansour Real Estate Group is known for pricing discipline, honest market context, and a process built around protecting seller equity in any market condition.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Official Resources

- Fraser Valley Real Estate Board — fvreb.bc.ca

- BC Assessment — bcassessment.ca

- BC Financial Services Authority (Realtor Verification) — bcfsa.ca

- Insurance Bureau of Canada (Flood Risk Mapping) — ibc.ca

- Appraisal Institute of Canada (BC Chapter) — aicanada.ca

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.