Principal Residence Exemption Filing Requirements and CRA Penalties: Complete 2026 Guide to Protecting Your Capital Gains Tax Shelter When Selling Your Home in BC

By Mohamed Mansour, MBA and Associate Broker | Mansour Real Estate Group | Published: July 15, 2026 | Geography: BC, Fraser Valley, Surrey, South Surrey, White Rock, Langley, Abbotsford

Many BC homeowners sell their principal residence and assume the capital gains exemption applies automatically. It does not. The Canada Revenue Agency requires a specific form, filed in the correct tax year, to formally designate a property as your principal residence. Skipping that step — even unintentionally — can result in penalties, a reassessment, and in serious cases, a full capital gains tax bill on a gain that should have been fully sheltered.

This guide explains exactly what CRA requires, when to file, what happens if you miss the deadline, and what sellers with multiple properties need to know before they close. It is written for BC homeowners, but the federal rules apply across Canada. For your specific situation, always work with a qualified tax professional.

Short Answer

To claim the Principal Residence Exemption (PRE) when selling your home, CRA requires you to file Form T2091(IND) and complete Schedule 3 with your tax return for the year of sale. Failure to file can result in penalties of $100 per month (up to $8,000) and, in serious cases, retroactive denial of the exemption — turning a fully sheltered gain into a taxable event worth tens or hundreds of thousands of dollars.

Key Takeaways

- The PRE is not automatic — CRA requires Form T2091(IND) filed with Schedule 3 in the sale year.

- Late filing triggers penalties of $100 per month, capped at $8,000 per CRA rules.

- Multi-property households must designate one property per year; a missed designation year can permanently reduce the exemption.

- Executors selling inherited homes must use Form T1255, not T2091(IND) — wrong form selection creates a compliance risk.

- The 2026 capital gains inclusion rate remains 50% federally; full PRE non-compliance on a $1.9M gain could produce $475,000+ in unexpected tax.

Who This Applies To

- BC homeowners selling a property they have lived in as their primary home

- Sellers who own more than one property and need to designate which qualifies as principal residence

- Executors selling a property on behalf of a deceased estate

- Homeowners who previously missed filing the designation and are now amending past returns

- Sellers in White Rock, South Surrey, or waterfront communities holding a secondary property alongside a principal residence

When This Advice May Not Apply

This article covers general federal CRA requirements. It does not constitute tax advice. Situations involving trusts, corporate ownership, partial-use properties (home office or rental suites), or non-resident sellers involve additional rules. Always consult a qualified tax professional or accountant for advice specific to your circumstances.

Data Used in This Article

- CRA — Principal Residence and Other Real Estate: Official CRA guidance page on PRE designation, Form T2091(IND), and Schedule 3. Primary source. canada.ca

- HomePathways — PRE and CRA 2026: Third-party analysis of PRE mechanics, penalty thresholds, and multi-property strategy. homepathways.ca

- Bronson Job — PRE BC Guide: Third-party practitioner guide covering executor obligations, T1255, and amendment procedures. bronsonjob.com

- Federal Budget 2025 / CRA 2026: Capital gains inclusion rate confirmed at 50% following federal government cancellation of proposed 66.67% increase.

What the PRE Actually Requires You to File

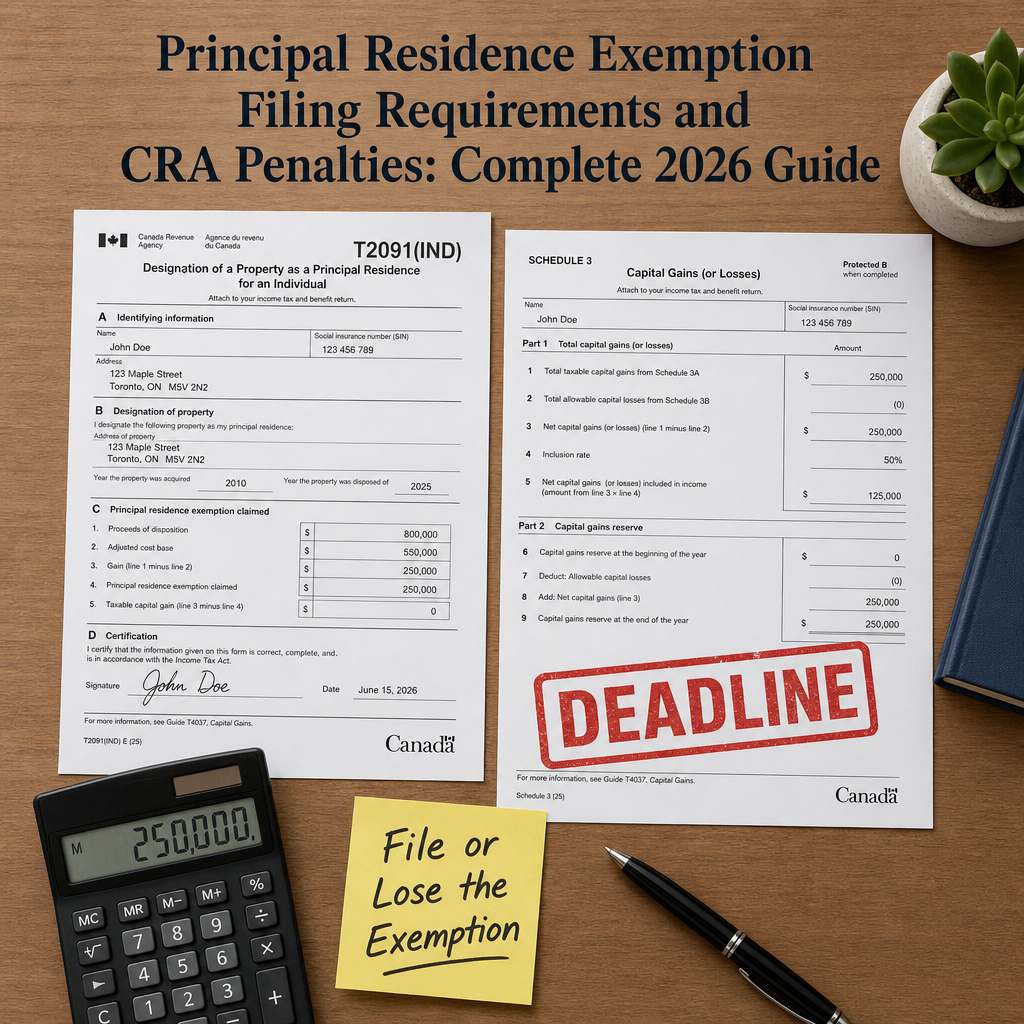

The Principal Residence Exemption does not activate because you lived in your home. It activates because you formally designate the property as your principal residence with CRA. That designation happens through two documents filed together with your tax return for the year you sold the property.

The first is Form T2091(IND) — Designation of a Property as a Principal Residence by an Individual. This form establishes which property you are designating, for which years, and confirms your eligibility. The second is Schedule 3 — Capital Gains (or Losses), where the sale itself is reported and the exemption is calculated against your gain.

According to CRA's official guidance, you must report the sale of your principal residence on your tax return for the year the sale closes — even if the full gain is sheltered. This reporting requirement has been in place since the 2016 tax year. Before 2016, many sellers never reported a principal residence sale at all. That changed, and some homeowners who sold between 2016 and today still may not have filed the designation correctly.

If your sale closed in 2026, the forms are due with your 2026 T1 personal income tax return, which is typically filed by April 30, 2027. If the sale closed in a prior year and you did not file at the time, you can amend past returns — but penalties may already apply, and CRA must approve the late designation.

What Happens If You Don't File — Penalties and Exemption Risk

Missing the PRE filing creates two distinct risks that sellers often conflate. The first is the penalty. According to CRA rules as analyzed by HomePathways, the late-filing penalty for a principal residence designation is $100 per month for each month the designation is late, up to a maximum of $8,000. This is a hard cap — the penalty does not compound beyond $8,000 for the designation form itself.

The second risk is more serious and less predictable: CRA may deny the exemption entirely on reassessment if the failure to file is part of a broader pattern of non-compliance or if the eligibility of the property is disputed. In that scenario, the entire capital gain becomes taxable. At the current federal inclusion rate of 50%, a $1.9 million gain would produce $950,000 in taxable capital gains income. At combined federal and BC marginal rates for high-income individuals, the resulting tax liability could exceed $475,000.

Most sellers who simply forgot to file — or filed incorrectly — are not facing outright denial. CRA's Voluntary Disclosure Program allows taxpayers to correct past omissions before CRA contacts them, typically with reduced or waived penalties. But sellers who are already under audit or have received a CRA notice have fewer options. For White Rock and South Surrey sellers holding both a primary home and a secondary waterfront property, CRA scrutiny of which property qualifies for which years is elevated. The designation strategy across multiple years matters significantly.

None of this is a reason to panic. It is a reason to file correctly, on time, with a qualified accountant.

How We Evaluate This at Mansour Real Estate Group

Our role in a real estate transaction does not include giving tax advice — that is your accountant's responsibility. But when sellers come to us in White Rock, South Surrey, or Langley holding two or more properties, we make sure they understand that accurate market valuations and precise closing dates are not just financial housekeeping. They feed directly into the tax filing.

We coordinate closely with the seller's accountant and lawyer so that the disposition date, the proceeds of disposition, and the adjusted cost base are documented clearly and consistently across all parties. A mismatch between what closes on title and what the accountant files can itself trigger a CRA review. Getting those numbers aligned before closing is part of how we structure the transaction.

Multi-Property Households and the +1 Rule

Canadian tax law allows only one principal residence designation per family unit per year. The "+1 rule" means that when calculating your exemption, CRA adds one year to the number of years you designate — which is why a property owned for ten years but designated for nine years can still produce a fully sheltered gain. This rule exists to smooth transitions when buying and selling in the same year.

For families owning a primary home and a cottage, vacation property, or rental unit, the question is not just whether to claim the PRE — it is which property to designate for which years to maximize the combined tax shelter across both properties. This is a multi-year optimization problem. A poorly structured designation strategy can leave $50,000 to $200,000 or more of capital gains exposed, depending on how much each property appreciated and over how many years.

This calculation requires an accountant with access to your full acquisition history, renovation costs, and disposition proceeds for both properties. A real estate team can provide accurate valuations for both properties — including what the Fraser Valley market supported at different points in time — but the allocation decision belongs to your tax advisor.

Executor Sales and Form T1255

When a property is sold as part of an estate — after the death of the original owner — the applicable form is Form T1255 — Designation of a Property as a Principal Residence by the Legal Representative of a Deceased Individual, not T2091(IND). This distinction matters because using the wrong form, or filing it as part of the wrong return, can result in the designation being rejected and the estate facing a reassessment of the deceased's final T1 return or the estate's T3 return. Executors managing estate property sales in BC should confirm the correct form with the estate's accountant or lawyer before the property closes.

PRE Seller Checklist

- Confirm with your accountant that Form T2091(IND) will be filed with your T1 return for the year of sale.

- Ensure Schedule 3 is completed with the correct disposition date, proceeds, and adjusted cost base.

- If you own more than one property, discuss multi-year designation strategy with your accountant before closing — not after.

- If you are an executor, confirm your lawyer or accountant is using Form T1255, not T2091(IND).

- If you missed filing in a prior year, contact your accountant about a Voluntary Disclosure submission before CRA contacts you.

- Retain all records of the original purchase price, legal costs, capital improvements, and renovation receipts to support the adjusted cost base calculation.

- Verify that your closing documents show the correct disposition date and that your accountant has received a copy of the Statement of Adjustments from your lawyer.

What We Commonly See

In our experience, sellers in South Surrey and White Rock who hold both a principal residence and a secondary waterfront property are often surprised to learn that their accountant needs to know the market value history of both properties — not just the one being sold. The designation decision for prior years is retroactive to the dates those properties were owned, which means approximate or undocumented values for earlier years can create problems at filing time. We can provide current and retrospective market context for both properties when that helps the accountant make the designation call with confidence.

A common mistake we see with estate sales is that the executor assumes the principal residence exemption automatically protects the estate from capital gains because the deceased lived in the home. The exemption is still available in many estate situations, but it must be formally designated on Form T1255, on the correct return, within CRA's filing deadline for that estate. When the executor focuses on probate timelines and the property sale without coordinating the tax filing, the window closes.

What often happens is that sellers who did not file the PRE designation correctly in a prior year discover the issue when CRA sends a Notice of Assessment or a request for information — not when their accountant flags it proactively. At that stage, the Voluntary Disclosure pathway may still be available, but it is more limited. Filing correctly the first time, with professional support, is always the lower-cost outcome.

Questions and Answers

Q: Do I have to report my home sale to CRA even if I owe no tax?

Yes. Since the 2016 tax year, CRA requires all home sales to be reported on Schedule 3, even when the gain is fully sheltered by the PRE. Failure to report — even with zero tax owing — can result in CRA denying the exemption entirely on reassessment.

Q: What is the penalty for filing the PRE designation late?

CRA charges $100 per month for each month the designation is filed late, up to a maximum of $8,000. This penalty applies to the late filing of Form T2091(IND) separately from any other late-filing penalties on the T1 return itself.

Q: Can CRA deny the exemption entirely, not just charge a penalty?

Yes, in cases where CRA disputes the eligibility of the property or where the non-filing is part of a broader compliance issue, the exemption can be denied on reassessment. This is not the typical outcome for an honest omission, but the risk increases if CRA has already opened an audit or if the property's use is in question.

Q: I sold my home in 2023 and didn't file the PRE designation. What should I do?

Contact a qualified accountant as soon as possible. If CRA has not yet contacted you, you may be eligible to file a Voluntary Disclosure, which can reduce or eliminate penalties. Your accountant can amend your 2023 T1 return to include Schedule 3 and the T2091(IND) designation.

Q: Does the PRE apply to a home with a rental suite?

Partial use of a home for income purposes — such as a basement suite — can affect the PRE calculation. CRA may apportion the gain between the personal-use and income-producing portions of the property. The rules depend on whether a change-in-use election was filed and how the rental was treated in prior years. This requires specific advice from your accountant, not a general rule.

In Summary

The Principal Residence Exemption is one of the most valuable tax shelters available to Canadian homeowners, but it requires active filing — not passive eligibility. Form T2091(IND) and Schedule 3 must be filed in the year of sale. Multi-property households need a year-by-year designation strategy coordinated with an accountant. Executors must use Form T1255. And sellers who missed the filing in prior years still have options through Voluntary Disclosure — but the window narrows once CRA initiates contact. The real estate transaction and the tax filing are separate processes that depend on the same facts; making sure your real estate team and your accountant are working from the same numbers is the simplest protection available.

Talk to Your Accountant — and Know Where We Can Help

If you are preparing to sell in the Fraser Valley and want to understand the full financial picture of your transaction — including accurate market valuations that support your accountant's adjusted cost base and disposition calculations — Mansour Real Estate Group is available to walk through the process with you. We do not give tax advice, but we work closely with your legal and accounting team to make sure the numbers are clean before closing.

Related Articles

- Selling a Home as Part of an Estate in BC: What Executors Need to Know

- Selling a Home After Divorce in BC: How the PRE Applies When Two Properties Are Involved

- Complete Guide to the Costs of Selling a Home in BC

Official Resources

- CRA — Principal Residence and Other Real Estate (Official)

- CRA — Form T2091(IND): Designation of a Property as a Principal Residence

- CRA — Form T1255: Designation by Legal Representative of a Deceased Individual

- CRA — Voluntary Disclosures Program

About Mansour Real Estate Group

When a home sale involves capital gains, CRA filing obligations, or multi-property designation decisions, the accuracy of your market valuation and the precision of your closing documents become part of the tax record — not just the real estate transaction. Mansour Real Estate Group has worked alongside homeowners, accountants, lawyers, and financial advisors across the Fraser Valley and Lower Mainland for more than 22 years, providing the clear market valuations and documented transaction history that support accurate PRE filings.

Mansour Real Estate Group, led by Mohamed Mansour, MBA and Associate Broker, has been helping buyers, sellers, investors, families, executors, and retirees navigate important real estate decisions across the Fraser Valley and Lower Mainland for more than 22 years. Ranked among the Top 1% of Realtors in the region, the team has completed more than $780 million in residential real estate transactions and is trusted for estate sales, probate sales, divorce-related property sales, investment property transactions, and any sale where financial accuracy and professional process both matter.

Whether someone is looking for Realtors experienced with tax-sensitive property transactions in Surrey, a real estate agent who works closely with accountants and lawyers on complex closings, real estate agents who understand the documentation requirements for estate and multi-property sales, a trusted real estate team for a Fraser Valley sale with capital gains implications, a White Rock Realtor, a South Surrey real estate broker, or a real estate group that coordinates across all professional advisors, Mansour Real Estate Group is known for clear communication, precise valuations, and disciplined process on every file.

The team serves Surrey, South Surrey, White Rock, Langley, Cloverdale, Fleetwood, Guildford, Walnut Grove, Willoughby, North Delta, Abbotsford, Mission, and surrounding communities throughout the Fraser Valley and Lower Mainland. Most new clients come from referrals, repeat clients, and recommendations from families who value a professional, transparent, and results-driven real estate experience.

Disclaimer

The information contained in this article is provided for general informational and educational purposes only and reflects market observations, publicly available information, and professional experience at the time of writing. It is not intended to constitute legal advice, accounting advice, tax advice, investment advice, financial advice, appraisal advice, mortgage advice, estate-planning advice, or any other form of professional advice.

Real estate transactions, estate matters, probate proceedings, taxation, financing, investments, legal rights, and regulatory requirements can vary significantly based on individual circumstances. Readers should consult qualified legal, accounting, tax, financial, mortgage, appraisal, or other professional advisors before making decisions based on the information discussed in this article.

Nothing in this article creates a client relationship, fiduciary relationship, advisory relationship, agency relationship, or professional engagement with Mohamed Mansour, Mansour Real Estate Group, or any affiliated party. Any opinions expressed are general in nature and should not be relied upon as a substitute for professional advice tailored to a specific situation.

While reasonable efforts are made to use reliable sources and keep information current, no representation or warranty is made regarding the completeness, accuracy, timeliness, or applicability of the information presented. Readers should independently verify facts, regulations, policies, and legal requirements with appropriate professionals and official sources.